In his August 15, 2020, press conference, President Trump delivered a glowing assessment of the current state of the United States economy, spending considerable time crowing about the speed of the current economic "recovery".

There is just one problem with his economic analysis: it is completely wrong.

In his zeal to both defend his policies and maintain a spirit of optimism for the future, President Trump is relying on certain top-level benchmark indicators while ignoring the far less favorable dynamics taking place underneath. The top level numbers do suggest expansion is occurring, but they overlook the distorting impact of the massive government injections of money into household incomes as well as the ongoing injections of liquidity by the Federal Reserve into financial markets.

To accurately assess the true state of the economy, we must first unwind these distortions.

The Present: Things Are Not As Rosy As They Seem

In his press conference, President Trump asserted the United States was experiencing the fastest economic recovery on record.

“We are currently witnessing the fastest economic recovery in American history,” Trump said during a press conference at his club in Bedminster, New Jersey, on Saturday evening.

The president showed the press charts that demonstrated used auto sales setting new records, retail spending up, and industrial production increasing rapidly. He also noted that the stock market was improving despite record plunges as the coronavirus pandemic reached the United States.

Unfortunately, Trump's take ignores a number of significant indicators of ongoing economic contraction:

American Airlines, as well as other carriers, is in the process of shutting down routes to a number of smaller cities. Many flights to those cities had been completely empty of passengers.

One-third of Americans failed to make their August housing payments. A similar number had failed to do so in June and July as well.

In the August 13 jobs report, there are still 15 million unemployed receiving state unemployment assistance.

Food banks are experiencing elevated demand for assistance.

83% of New York City restaurants are unable to pay their monthly rent.

The point here is not to excoriate President Trump, but to understand why he is so far wide of the actual mark. We must acknowledge the metrics he touts as indicative of economic success, such as the rise in the stock markets, are the metrics almost all economic pundits as well as the legacy media use to depict economic performance. Within the parameters of those metrics, President Trump's statements are factually correct.

The problem is Trump is using the wrong metrics in his public statements.

Measurement Fallacies

To understand how these metrics lead to an inaccurate depiction of the economy, we must first consider the impact of metrics on analysis. Perhaps the most succinct explanation is found in IT management guru Bob Lewis' First Law Of Metrics--"You get what you measure."--and its corollary--"If you mismeasure, you mismanage."

In other words, if you use the wrong metrics to track the state of something, you will get an incorrect depiction of that state, and will proceed to make unsound and unwise decisions.

In gauging the US economy, it is by now a virtual certainty the stock market does not respond to the dynamics of the real economy, but instead to the various machinations of the Federal Reserve as well as the other central banks of the world.

Similarly, a metric such as aggregate jobs "created" since March are misleading for several reasons: 1) it fails to show the number of people who have been laid off multiple times (57% of Californians have filed for unemployment multiple times); and 2) it does not show the number of jobs created that are only part-time positions (803,000 of the 1.4 million jobs created in July were part time positions).

Moreover, when reviewing figures such as job creation, we have to look closely at the underpinning numbers. The same jobs report that touted the creation of 1.8 million jobs in July showed only 1.4 million workers added to various payrolls.

Right away we see the top level jobs number is unreliable, and that it overstates actual job creation by at least 400,000 jobs.

By the same token, increases in retail sales fail to take into account the fact that government transfers make up 25% of all household income. People are spending money they are being given rather than money they have earned. When evaluating the health of an economy, that distinction is quite relevant.

President Trump gets the economy wrong because he is using the wrong metrics, often with wrong figures, and using an incomplete set of metrics.

Nor is he alone in this. The Federal Reserve has been using the wrong metrics for years resulting in an absolutely insane monetary policy of endless expansion while overseeing the slow but inevitable collapse of the American banking system.

Looking Back: 2019 Did Not End Well

To understand how far off base the Federal Reserve has been, we must first recall the stresses in the financial system that took place in the fourth quarter of 2019. While it has been swept aside by the hysteria over the CCPVirus, we must recall that 2019 did not end at all well for the Fed.

Throughout October of 2019, the Federal Reserve found itself repeatedly having to inject fresh liquidity into interbank "repo" markets. The repo markets literally could not get enough liquidity, and Fed Chairman Jay Powell showed no indication he had any idea where the magically printed money being shoveled into the markets was going. The Fed would ultimately end the month committing to injections of up to $850 billion in liquidity to keep the financial machinery moving along.

There can be little doubt the Federal Reserve was mis-managing. It is not unreasonable, therefore, to presume the Federal Reserve has been mis-measuring, as bad data begets bad decisions.

Follow The Money

We come therefore to a question: what metrics we should be using?

The answer is a pithy and somewhat cliche "follow the money".

In my previous exploration of this topic, I focused on the M1 money supply and its relation to the general rise in the stock markets. The basic rationale at the time was that the correlations between that monetary measure and the rise in stock market indices were much more clearly defined than with the M2 measure. The M1 also shows a much more dramatic shift in the 2008-2009 recession that marked the inflection point of Federal Reserve monetary policy.

The reason this is so is because the M1 represents "hard" cash. It is, quite literally, "real money".

M1 is the money supply that is composed of physical currency and coin, demand deposits, travelers' checks, other checkable deposits, and negotiable order of withdrawal (NOW) accounts. M1 includes the most liquid portions of the money supply because it contains currency and assets that either are or can be quickly converted to, cash.

The M2, on the other hand, includes not just the real money of the M1 but so-called "near money".

M2 is a calculation of the money supply that includes all elements of M1 as well as "near money." M1 includes cash and checking deposits, while near money refers to savings deposits, money market securities, mutual funds, and other time deposits.

Comparing M2 growth to the stock market becomes problematic, because securities such as mutual funds are invested in those same markets, and thus part of the M2 rises in response to asset price increases within the markets. Thus, to assess the impact of money creation on the stock market, one has to rely on the base M1 metric.

Similarly, when there is a clear correlation between the M1 and various stock market indices, as is clearly the case beginning in 2008, we are forced to conclude that mere increases in the stock market are not indicative of expansion in the real economy, as asset price inflation accounts for almost all of the rise since 2008.

In fairness, these same analyses show the first three years of President Trump's Administration to occasion significant real growth in the real economy, and a significant portion of asset price increases since 2017 may be fairly attributed to actual economic expansion. Ironically, while Trump's depictions of the economy are frequently mistaken, the track record of his Administration on economic matters is superior by far to Barack Obama, who achieved real economic growth only in the latter years of his second term.

When it comes to evaluating the economy, in order to "follow the money" we must work primarily from the base M1 metric, and not the more popular M2.

As my prior analysis revealed, working from the M1, we quickly see the state of the economy is--and has been--very poor, and for far longer than President Trump has been in office.

Far from preserving "price stability", or even facilitating macro-economic growth, the only thing the Federal Reserve's policies have preserved is an ongoing state of economic collapse. That they have engineered quite successfully since 2008.

Until these dysfunctional policies by the Federal Reserve are ended--or better yet the Federal Reserve itself is abolished--any hope of genuine economic recovery in the United States is a pipe dream.

The Rotten Foundation

Thus we come to the source of President Trump's errors on the economy: the foundation itself is rotten to the core, and the decay has been increasing steadily over time. It was rotten before he took office, and the rot is steadily increasing.

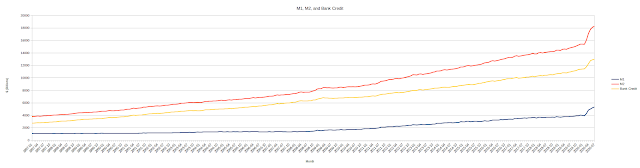

To understand the nature of the rot, we must consider how the US money supply has grown over the past few decades:

Unsuprisingly, the M2 increases at a generally faster rate than the M1. This is because the inclusion of "near money" means the M2 includes assets that reflect various forms of bank lending, such as various bonds and Treasury bills. The difference between the M2 and the M1 can thus be used as an approximation for the amount of bank lending ("Bank Credit") present in the economy--the third line in the chart above.

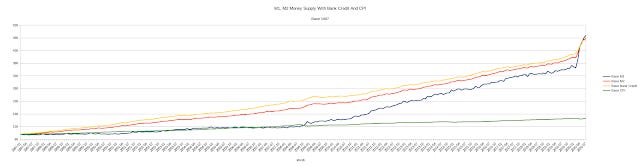

When we baseline the M1 and M2 measures to 1997, we see the 2008 inflection point that I have described previously.

To underscore the significance of this inflection point, note that it is here where core inflation, as represented by the Consumer Price Index (CPI), detaches from the money supply and follows and independent trajectory. This deviation is one of the first indicators that Federal Reserve monetary policy has been heading in an unanticipated direction.

We also see something else--something that is a "red flag" about the general state of banking: The M2 began growing at a slower rate than the M1 after 2008. Thus, even though the M2 continues to grow, proportionally the amount of "near money" relative to hard cash is declining--and has been since around 2008.

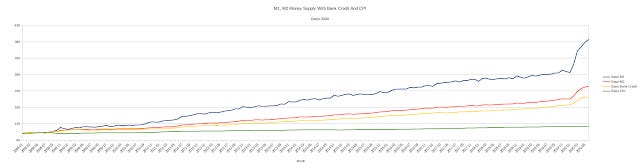

The phenomenon is made even clearer when we baseline the M1 and M2 to 2008.

The relative rise in the M1 far exceeds that of the M2 or of the differential bank credit. This distortion becomes more ominous when we consider the relatively flat CPI line, indicating that none of the created money is finding its way into the regular economy.

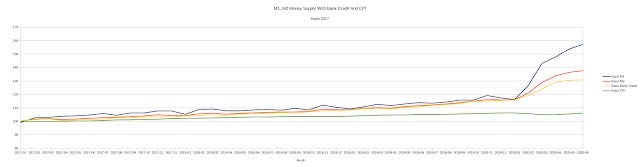

Here again, however, we should note that, up until the CCPVirus pandemic crisis, under President Trump the M1 and M2 relative growth moved on a similar trajectory, which we can see when we set the baseline to 2017.

Once again, President Trump's economic performance is ironically at odds with the accuracy of his economic rhetoric. Whether this is purely Trump being doggedly optimistic and upbeat (something which has long been part of his personality) or Trump being mis-informed and mis-led about the economy is a speculation far beyond what can be determined by the public record.

Unfortunately for President Trump, the money supply jumps off the rails again in February, 2020, in a very deliberate Federal Reserve response to the global pandemic hysteria. Amazingly, even this event does not lead to significant inflation, and CPI even appears to dip somewhat (although whether that can be maintained remains to be seen).

Still, from 2017 until February, 2020, the growth in hard money and the growth in bank lending are approximately equal. This indicates a relatively stable banking outlook, with bank lending expanding when there are more dollars to lend out. Lending confidence, it would seem, is relatively high.

Or is it?

If we pull our perspective back to 1997, and examine the ratio of bank credit (again, the difference between the M2 and M1 measures) to the M1 itself, we see the ratio rising up until 2008, and declining ever since.

From 1997 to 2008, broadly speaking, banks were willing to lend larger and larger multiples of hard dollars available--fueling and fueled by the mass speculation in derivatives that triggered the 2008 financial crisis.

Post 2008, however, banks have been lending progressively smaller multiples of hard dollars available (although we must again note the stabilization of the Trump years), and with the onset of the pandemic hysteria the multiple literally drops off a cliff. Even if we smooth the curve out with a six-month moving average, to get a general presentation of lending confidence, 2020 is still a disaster for bank lending.

The 2008 financial crisis proved fatal to bank lending, ending the rise in lending confidence and initiating a prolonged collapse in lending confidence and a corresponding collapse in lending relative to the growth of available money. The post-2008 economy is therefore a significantly more hostile terrain than the pre-2008 economy, and in 2020 that terrain has become more hostile by an order of magnitude.

Your banker is no longer your friend.

You Are No Longer Your Banker's Friend

We must not overlook a primary cause of that hostile terrain: loan defaults. As of August 17, the Federal Housing Administration, underwriter of most low-cost home mortgages in the United States, reported a record level of loan delinquencies.

The share of delinquent FHA loans rose to 15.7% in the second quarter, up a whopping 60% from about 9.7% in the previous three months and the highest level in records dating back to 1979, the Mortgage Bankers Association said Monday. The delinquency rate for conventional loans, by comparison, was 6.7%.

Significantly, this does not include the 8.2% of mortgages that are currently in "forbearance", one of the many initiatives advanced by Congress through the CARES Act passed in March.

Commercial real estate, potentially, is in even worse shape. Nearly 10% of commercial real estate loans assembled into the mortgage-backed securities product tracked in the market place as CMBX-9 were delinquent by 30 days or more.

As of June 2020, 9.8% of the collateral behind CMBX 9 is 30 or more days delinquent. That puts the index slightly ahead of the average CMBS delinquency rate as of June.

Another 6.6% of the loans behind CMBX 9 missed their June payment, but were not yet 30 days late – so there is room for the delinquency rate to move higher over the summer. (Those percentages include defeased loans in the denominator of the calculation.)

The pool of defeased loans totals 4.5% by loan balance. In addition, 23% of the collateral pool is on servicer watchlist and another 5.1% of the collateral pool is with the special servicer.

Banks are hardly able to do much in the way of lending when borrowers are not repaying what is owed. The commercial real estate loan situation has moved many property owners and their bankers to seek federal assistance in the form of a bailout for the $550 billion CMBS market.

Two months after we reported that the state of California is trying to turn centuries of finance on its head by allowing businesses to walk away from commercial leases, in other words to make commercial debt non-recourse, a move the California Business Properties Association said "could cause a financial collapse", attempts to bailout commercial lenders are now reaching the Federal level, with the WSJ reporting that lawmakers are introducing a bill to provide cash to struggling hotels and shopping centers that weren’t able to pause mortgage payments after the coronavirus shut down the U.S. economy.

Setting aside arguments on the wisdom or unwisdom of such a bailout, such proposals underscore the current reality of bank lending in the United States, and that reality is grim to say the very least. While banks have not yet themselves fallen into crisis, every new loan default, every new missed mortgage payment, depletes a bank's loan loss reserves.

Loan defaults do not help incent bannks to make new loans.

No Stable Banking, No Economic Growth

Business formation and economic growth require a measure of bank credit. Where there is no bank credit, there will be very little economic growth if any, and when bank credit is on the decline, economic growth is at the very least curtailed and potentially itself declines.

When we "follow the money" and interrogate the growth of money and bank credit over the past two decades at least, we see that, far from keeping the banking system itself stable, the Federal Reserve's monetary policies have contributed to a destabilization of the banking system--both in encouraging unwarranted credit expansion prior to 2008 and in excessively discouraging it after 2008. When we follow the money, we quickly see yet again how much of the economic growth we have been told occurred since 2008 is pure fiction, an illusion generated by ever increasing amounts of artificially created fiat money.

While the Trump administration successfully stabilized the economy, the Federal Reserve's pandemic response has completely jumped the shark yet again, and bank lending is now in danger of drying up completely. Jay Powell has quite literally snatched defeat from the jaws of Donald Trump's economic victory, laying the basis for a credit shock in the form of the complete cessation of bank lending.

Will that credit shock hit the American economy? If lending confidence continues to decline, that credit shock is inevitable.

When that credit shock hits the American economy, it will make short work of the positive metrics Donald Trump touted in his press conference.

When that credit shock hits the American economy, it will be the final act in the long dark twilight that has been the collapse of the American banking system.

Source Data: The data sets I used were as follows: