Last week’s January Job Openings and Labor Turnover Summary Report from the Bureau of Labor Statistics on the surface was largely good news.

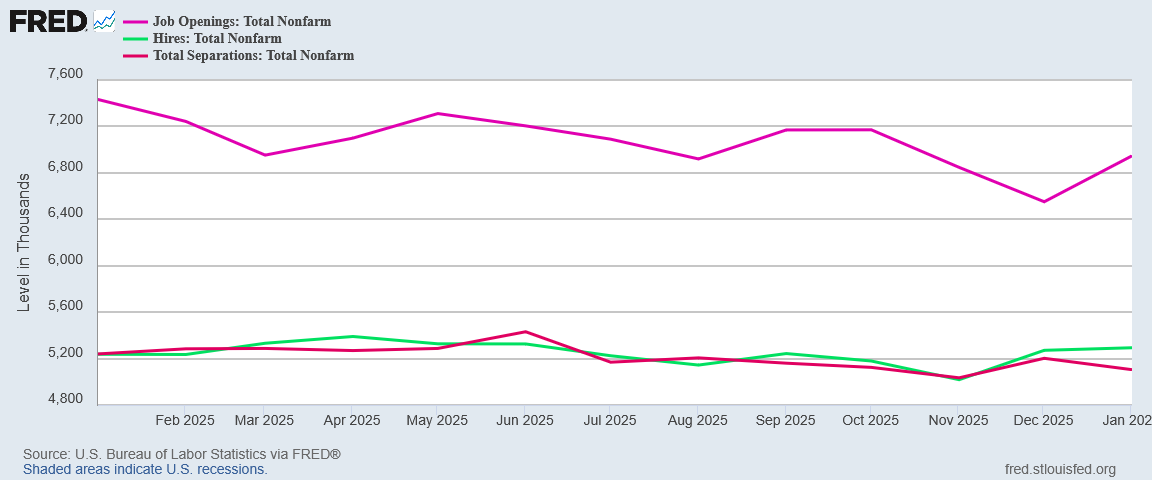

The number of job openings was little changed at 6.9 million in January, the U.S. Bureau of Labor Statistics reported today. Hires were unchanged at 5.3 million, while total separations changed little at 5.1 million. Within separations, quits (3.1 million) and layoffs and discharges (1.6 million) changed little.

While the BLS does love its “little changed” rhetoric, the “little changes” reported in the JOLTS report were in the right direction—towards job growth and an end to the jobs recession.

The JOLTS report also shows many of the same trends as the January Employment Situation Summary, and paints a much stronger picture of US labor markets than the January ADP National Employment Report. It gives credence to the proposition that the January jobs report was more than just a hot mess of Lou Costello Labor Math.

Job Openings Still Not The Point

Corporate media naturally retained its fixation on job openings, as if the pretense that there is a job waiting to be filled is economically the same as actually filling the job. It isn’t, of course, but that reality has never kept corporate media from dismissing hiring while hyping mostly fake job openings.

Job openings, a measure of labor demand, rose by 396,000 to 6.946 million by the last day of January, the Labor Department’s Bureau of Labor Statistics said in its Job Openings and Labor Turnover Survey, or JOLTS report, on Friday. Economists polled by Reuters had forecast 6.70 million unfilled jobs. The job openings rate increased to 4.2% from 4.0% in December.

Wall Street’s consensus was 6.7 million job openings, and the Trading Economics forecast was 6.5 million. The actual number reported on the JOLTS report bested both estimates by a substantial margin.

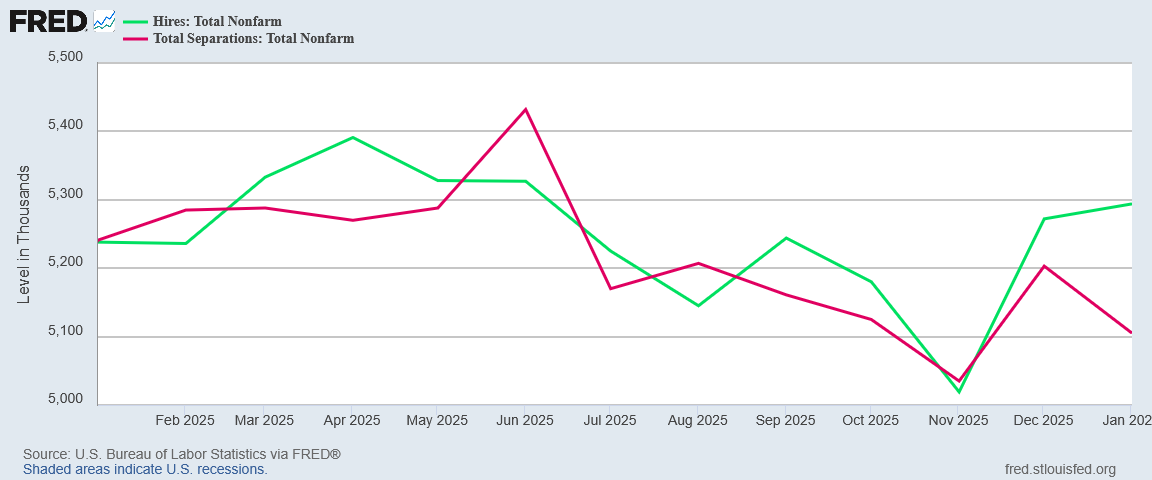

To be sure, actual hirings themselves did not grow significantly in January, although openings did move up noticeably.

What is significant, however, is that as hiring moved up a little, separations moved down a lot.

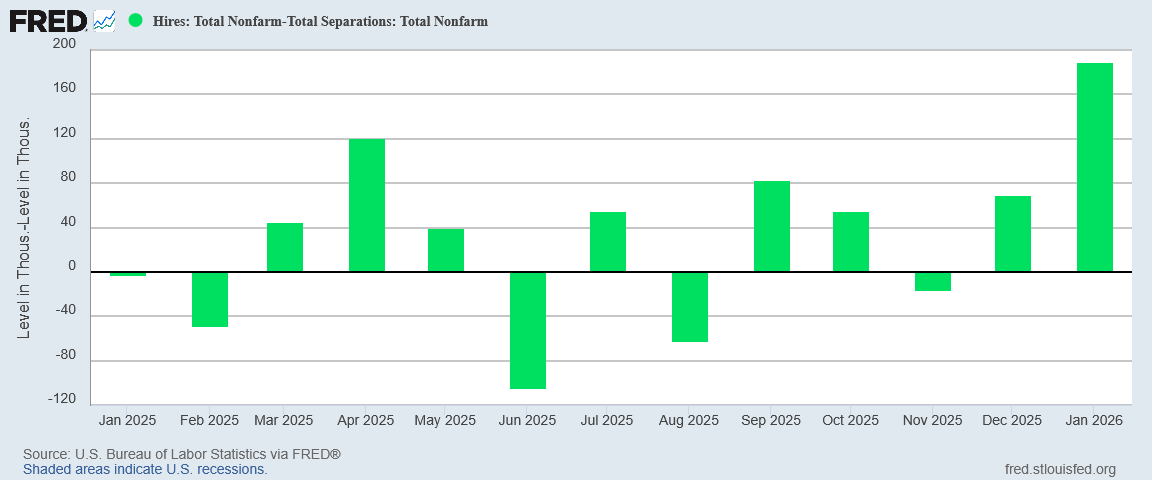

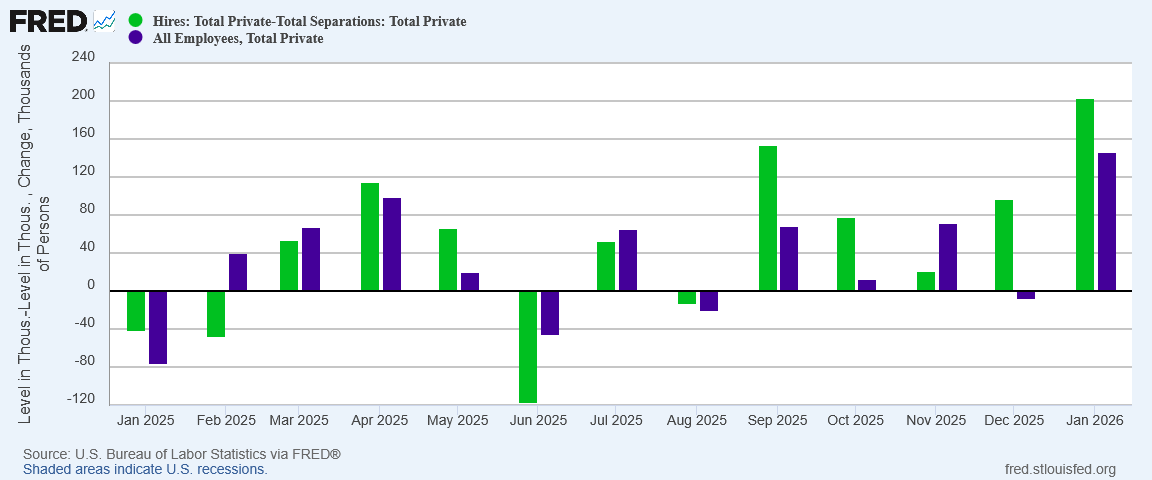

The result is that net hiring increased significantly in January.

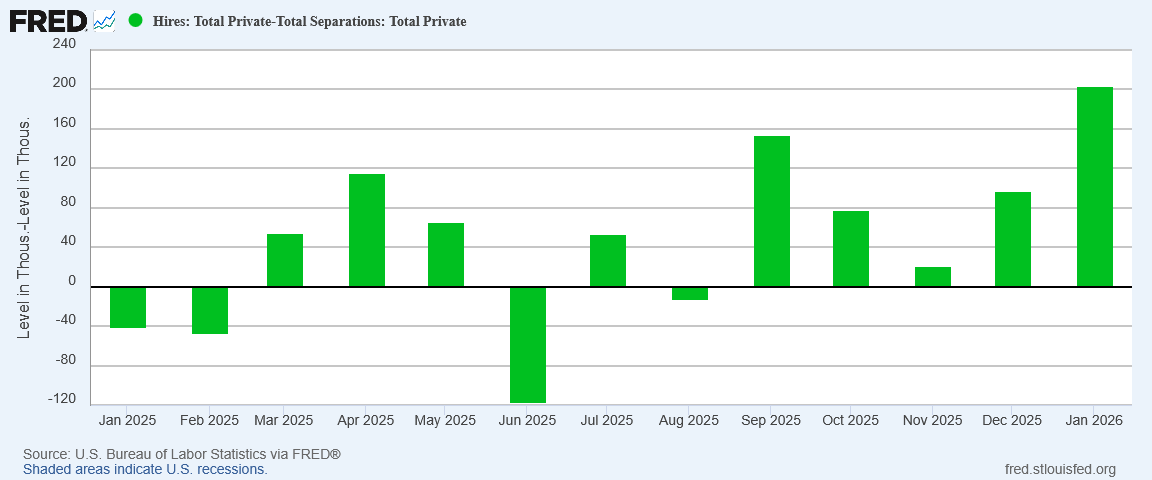

Even when we focus on just the private sector, the end result is the same: a substantial increase in net hiring.

While the net hiring growth came largely from a decline in separations, the end result still points to an overall increase in the number of people on a payroll somewhere in the US. Net hiring is actual job growth in every scenario.

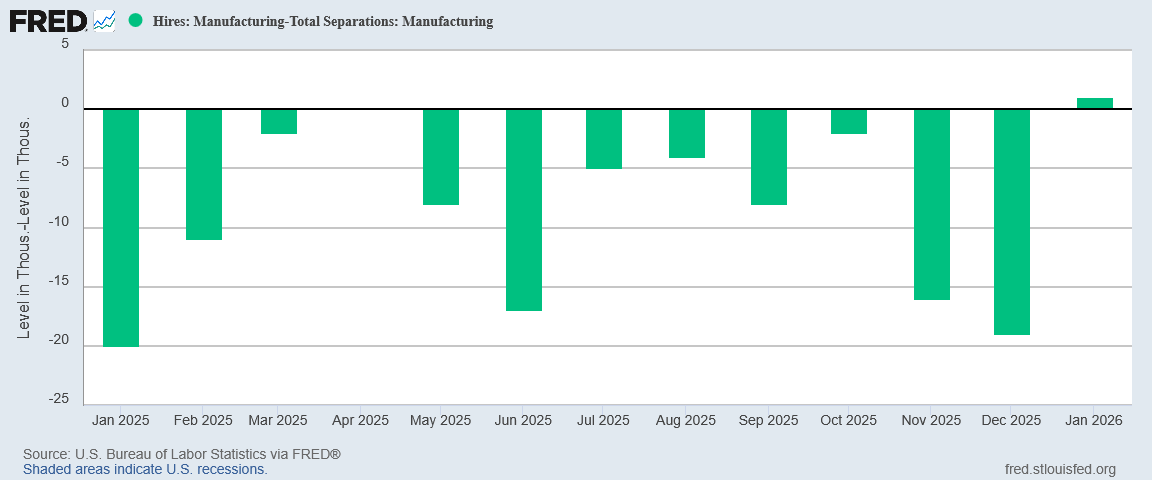

Manufacturing Job Gains—Barely

Net hiring in manufacturing was positive for January, although just barely. As with the jobs report, Manufacturing has been losing jobs steadily for over a year, and the January uptick barely stops that bleeding.

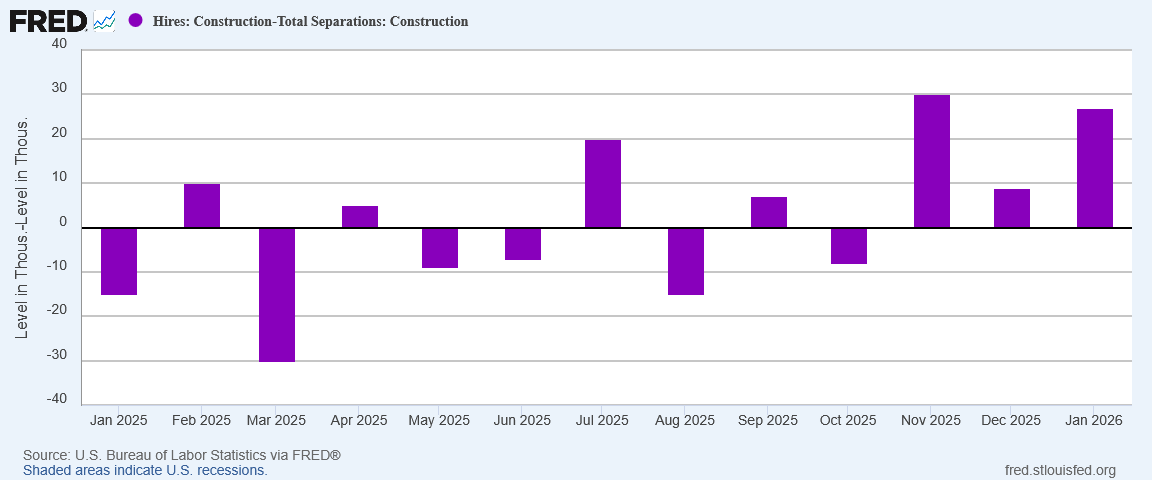

Construction, which languished for most of 2025, printed its third consecutive month of positive net hiring.

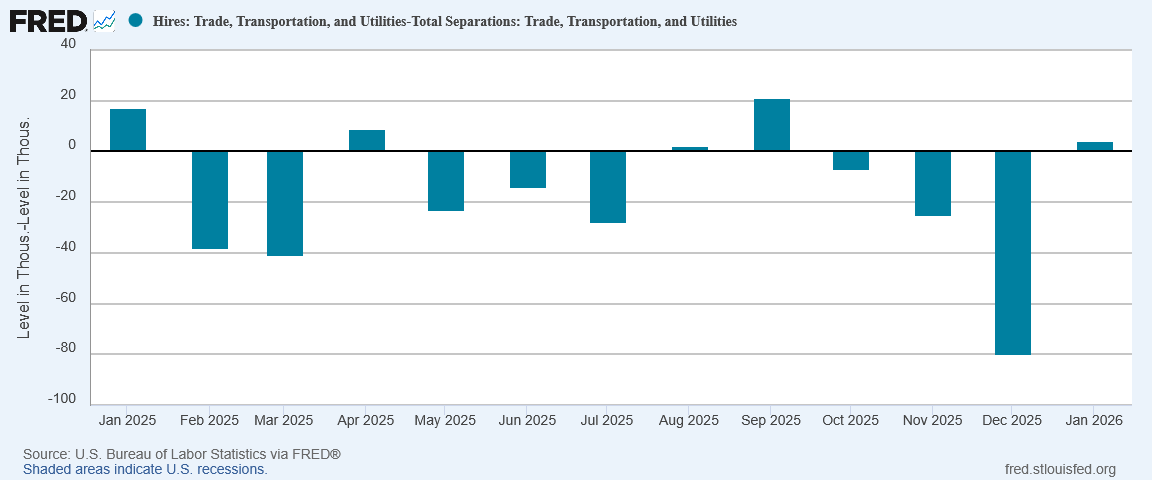

Trade, Transportation, and Utilities, another sector which had a bad 2025, also eked out marginal job gains.

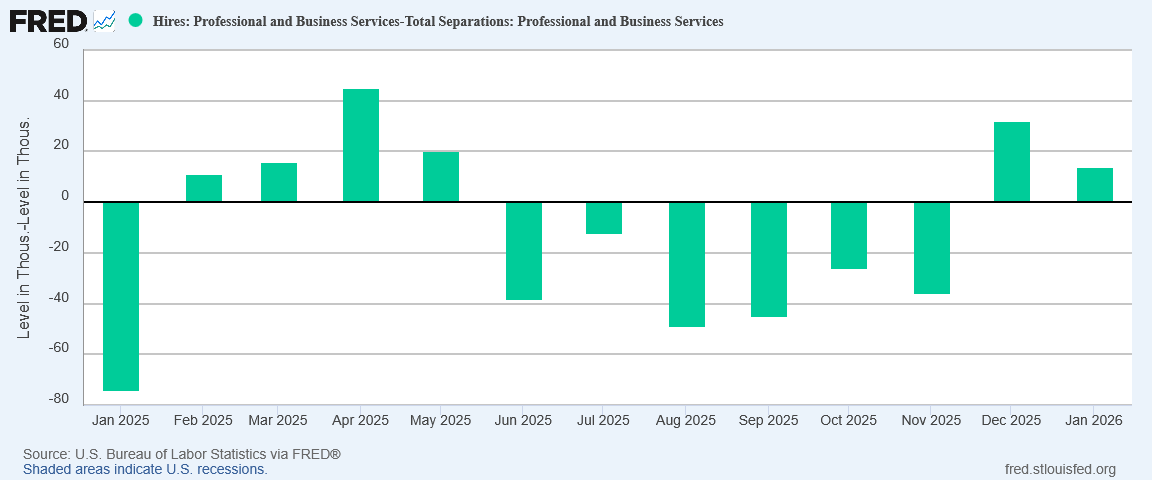

Professional and Business Services posted its second month of positive net hires.

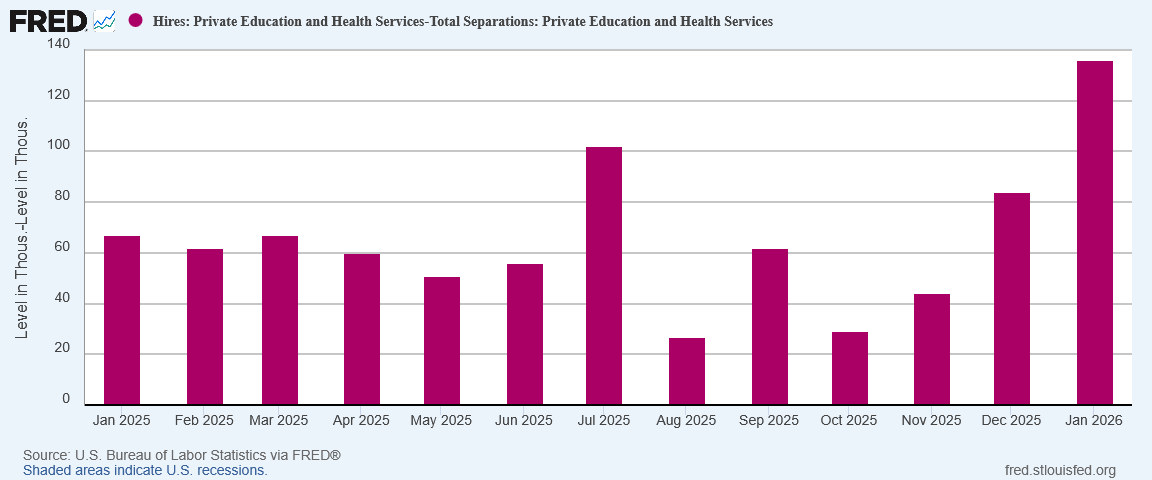

Meanwhile, Healthcare posted its strongest net hiring figures in a year.

While Leisure and Hospitality has seen declining net hiring numbers, it still printed a sixth consecutive month of positive net hiring.

This is the most encouraging aspect of the JOLTS data: every jobs sector except government showed at least marginal job growth. That is broader job growth than either the BLS Employment Situation Summary or the ADP National Employment Report shows for January.

Confirmation For Employment Situation Summary?

The most notable aspect of the January JOLTS report is that it gives support to the January Employment Situation Summary.

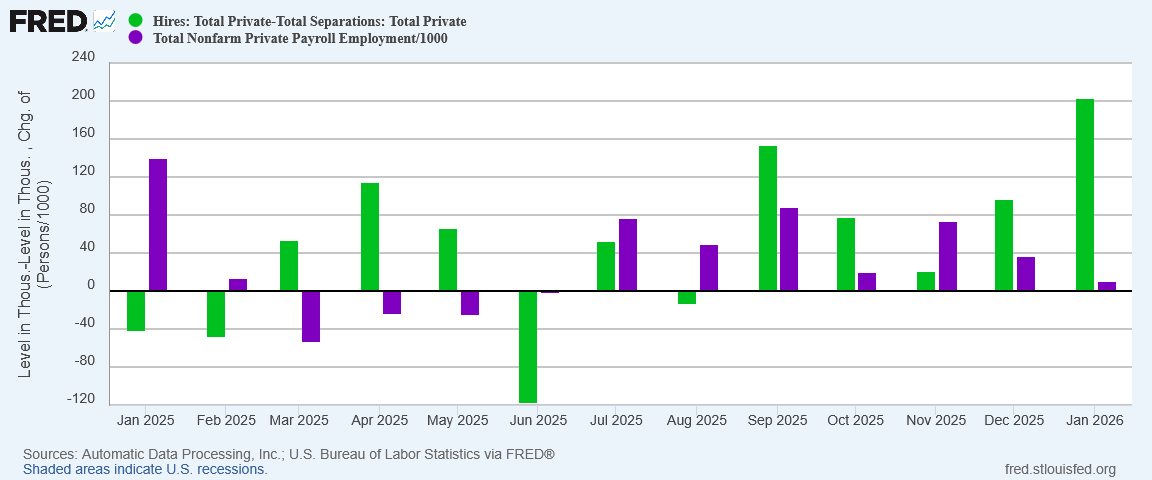

If anything, the JOLTS report is even more positive than the Employment Situation Report for January. While the January jobs report showed private employment jobs gains of 146,000 jobs overall, the JOLTS report for January printed 203,000 jobs.

The JOLTS report shows a far healthier jobs situation than the January ADP report, which printed at an anemic 22,000 private jobs gain.

It is worth noting that, with the January report, the JOLTS figures show their third month of net hiring growth, whereas the ADP report shows a declining hiring trend, and the Employment Situation Summary printed hot and cold on job growth over the same period.

Which reports should we trust? The ultimate answer is always going to be “none of them.” Even without the statistical garbage that has been a staple of the BLS jobs report for years at this point, we cannot lose sight of the reality that all of these surveys are just that—surveys. The final result is an estimate of actual job growth. Each of these reports will contain at least some error.

However, we should also note that, despite the statistical flaws and data handling mistakes present in each data set, the ADP report, the BLS jobs report, and the BLS JOLTS report all show broadly the same labor trends over time.

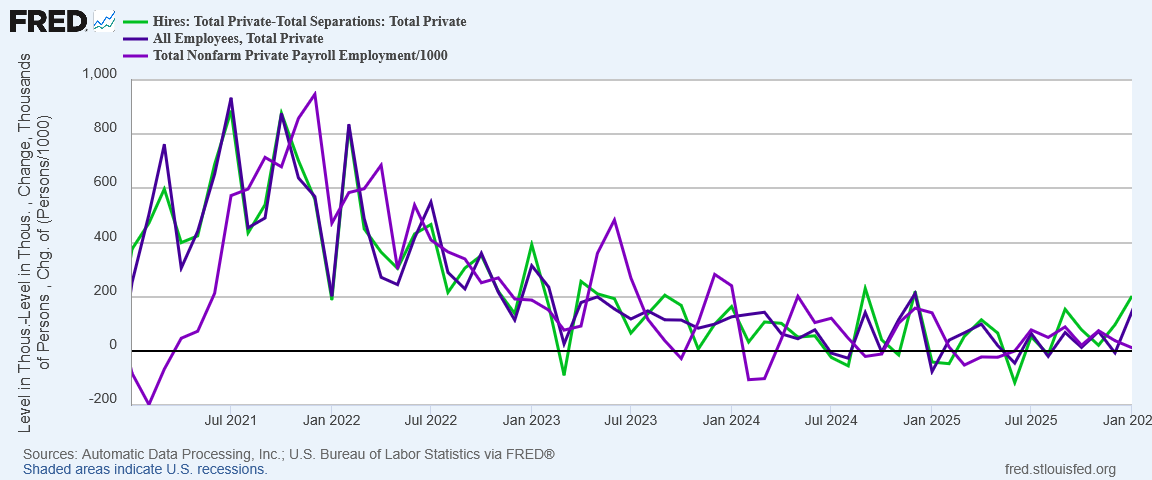

While the variances within any given month can be significant, all three reports show a declining net hiring trend since 2021.

When we speak of the “jobs recession”, this is an illustration of what that means—fewer new jobs, declining job growth, and in many cases, job loss.

Where the JOLTS and the BLS jobs report concur is that January saw an increase in new jobs, while the ADP report showed new jobs shrinking even further in January.

This will make the February JOLTS data particularly important, as we already know the February Employment Situation Summary is tremendously ugly, inverting the optimism and pessimism of the January ADP and BLS job reports. Which direction the February JOLTS data moves will either give credence to the negatives in the February BLS jobs data or help mitigate some of them.

Never As Bad, Never As Good

Overall, the January JOLTS report is good news. It bolsters the January Employment Situation Summary while mitigating the negative ADP National Employment Report.

Next month, we may very well see the opposite situation, with the JOLTS data confirming the ADP data while mitigating the BLS Employment Situation Summary data.

Thus, the JOLTS report stands as a useful reminder that the jobs outlook in this country is rarely as positive or as negative as the major reports will make it out to be.

The JOLTS data over time confirms the broad labor trends in the US economy, including the deepening jobs recession as hiring and actual job growth have slowed.

The JOLTS data also suggests that, contrary to what the ADP report showed for January, the jobs recession may be about to end, although any extrapolation along those lines must wait until we have the February data to compare to the February Employment Situation Summary especially. If the February JOLTS report mirrors that jobs data, then the jobs recession is in fact getting even worse.

Which outcome will it be? For that answer we must wait another month.

You are such a great data analyst, Peter. I’ve followed your work for three years, and your credibility just continues to grow. You objectively post the good news and bad, without spinning anything to fit a narrative. Thank you!