There can be no disputing that the March Producer Price Index Summary report was quite a bit better than had been anticipated. While there was still an inflation surge—which was expected—it was significantly less than forecast—which was not at all expected.

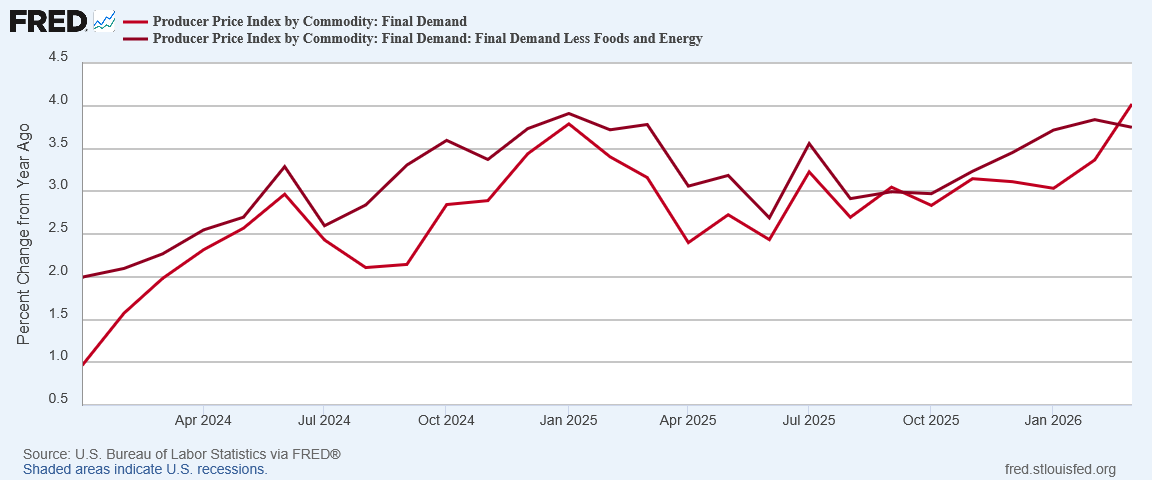

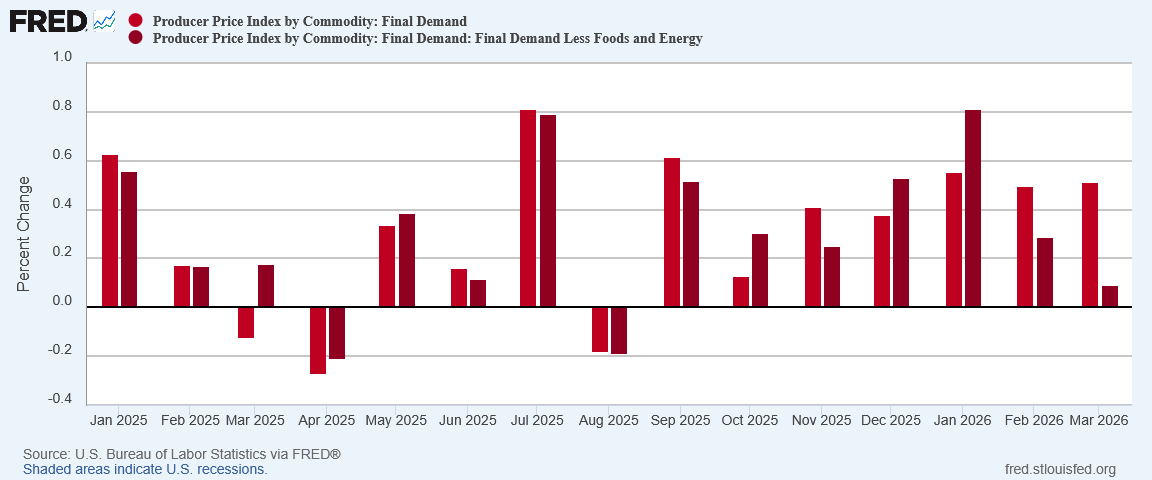

The Producer Price Index for final demand increased 0.5 percent in March, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices moved up 0.5 percent in February and 0.6 percent in January. (See table A.) On an unadjusted basis, the index for final demand rose 4.0 percent for the 12 months ended in March, the largest 12-month advance since increasing 4.7 percent in February 2023.

A jump to 4% in factory gate inflation is a sizable surge in any context. At the same time, the context for March’s sizable surge includes Wall Street projections of 4.6% year on year factory gate inflation in March and a Trading Economics forecast of 4.4%.

When an inflation print comes in nearly half a percentage point below forecast, that is unquestionably good news.

Nor is the cooler inflation print the only remarkable item in the summary. Core factory gate inflation actually declined in March, and prices on key items such as fertilizers were impacted by the energy shock far less than might have been anticipated.

We still have inflation, and the PPI summary is still indicating further inflation rises in the CPI data especially.

We do not have signs of hyperinflation—at least, not yet. As the war with Iran is still ongoing, and we still do not know what the endgame for that conflict looks like, we do not know how much more of an energy price shock has yet to be delivered.

The PPI report was a backhanded sort of good news. Energy prices surged. Other prices…not so much.

Core Producer Price Disinflation

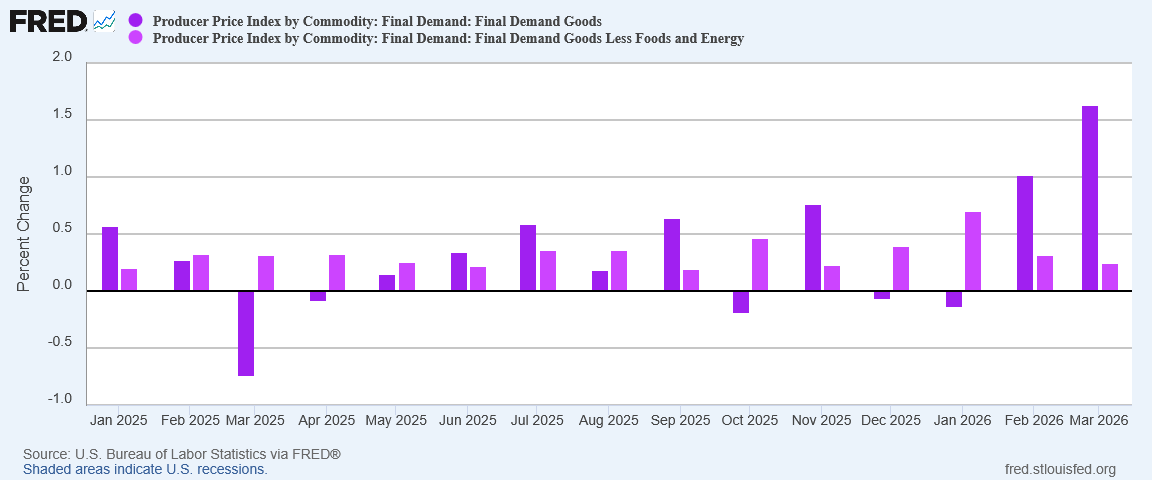

Without a doubt the factor that made the March Producer Price Index Summary a better-than-anticipated report was the decline in core factory gate inflation year on year, even as the headline PPI surged up.

The cooler core inflation print means that, just as with the Consumer Price Index report, inflation has not spread beyond energy into the broader basket of goods and services.

Even month on month saw a decline in core inflation.

Headline producer price inflation barely increased at all month on month, even though it surged year on year.

That core producer price inflation cooled significantly even as headline inflation rose is yet another confirmation that, thus far, the inflation brought on by a war-related energy shock is largely confined to energy, and has not percolated through the wider data set of producer prices.

No matter the surge in headline inflation, a report with declining core factory gate inflation has at least that much good news in it.

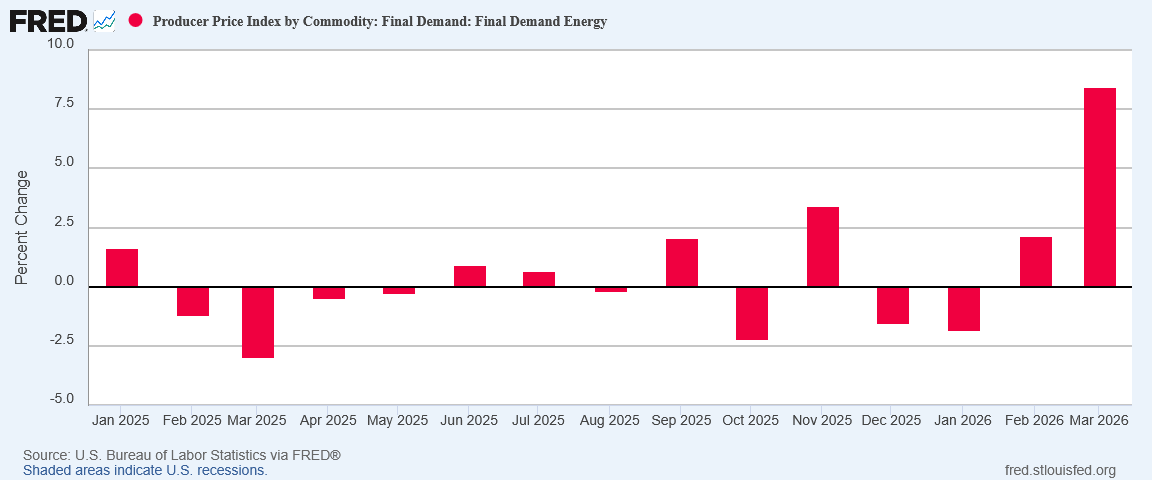

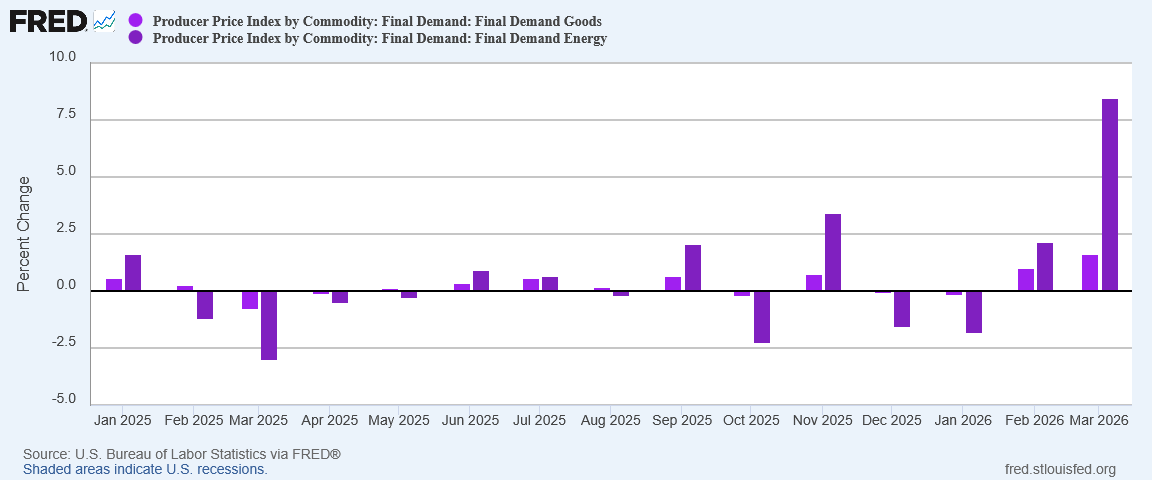

Even Energy Was Cooler

That energy prices surged at the factory gate in March is not at all surprising. Month on month factory gate inflation for energy prices soared over 8%.

After over a year of continued disinflation and deflation, energy price inflation came roaring back in March.

The reasons for the energy price surge are self-evident: Operation Epic Fury and Iran’s closure of the Strait of Hormuz, which has pushed energy and fuel prices up globally.

Surprisingly, despite the significant overall surge, some fuel prices did not rise as fast, and some even declined. Unprocessed fuels dropped by more than 40% month on month in March. In a month defined by energy price inflation, that is a remarkable shift.

Processed energy goods, on the other hand, “only” rose a more modest 11%—still high, but not egregiously so, given the headline data.

There are number of potential reasons why we are seeing anomalous price shifts within energy. In particular, the need for different types of crude oil to economically produce individual fuel types could very well amount to a price dynamic among some fuels that is far less dependent on the availability of Persian Gulf feedstocks.

Regardless of the reason, the end result is still that, even for energy prices, the March PPI report was better than it could have been.

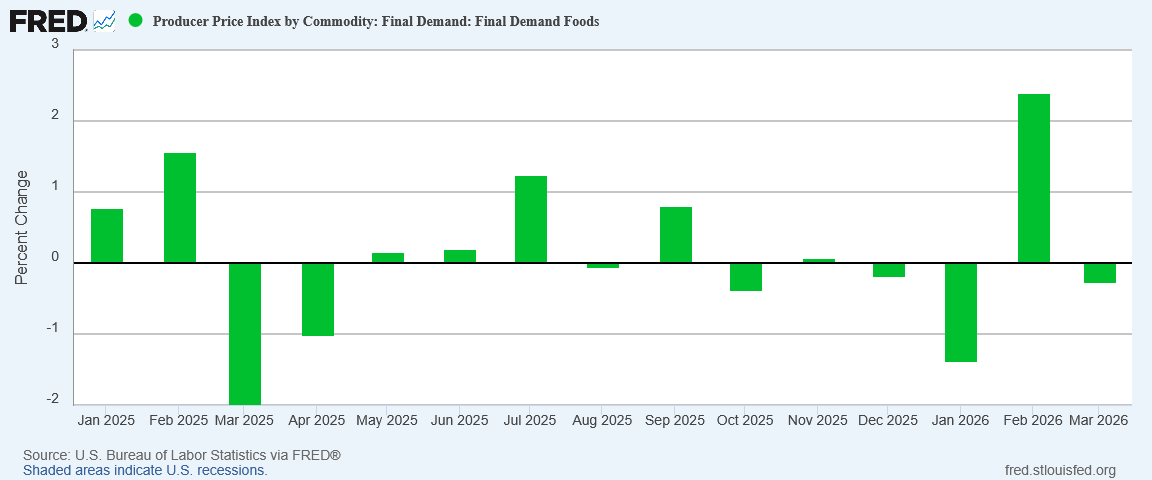

Food prices, the other component of headline inflation outside of the core metric, actually fell in March.

The spike in food price inflation in February proved to be an outlier, with deflation once again showing itself the dominant trend in factory gate inflation for food.

For March, the energy price shock remained confined to energy prices. While that will likely not remain the case for long, for the moment we are not facing a broad inflation surge that spans multiple subindices.

Not All Fuel Prices Are Equal

The surprising drop in unprocessed fuel prices highlights an important feature of energy and fuel prices: not all fuel prices are the same.

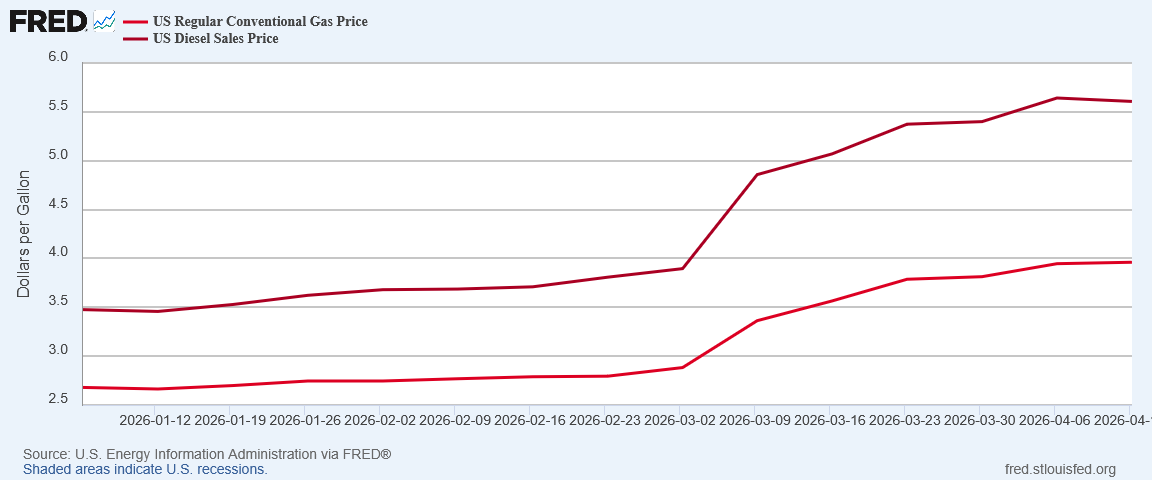

While both retail diesel and retail gasoline prices surged in March, diesel experienced the more dramatic price increase.

Even on futures markets, we see diesel prices increasing by a greater percentage than either gasoline or crude oil itself.

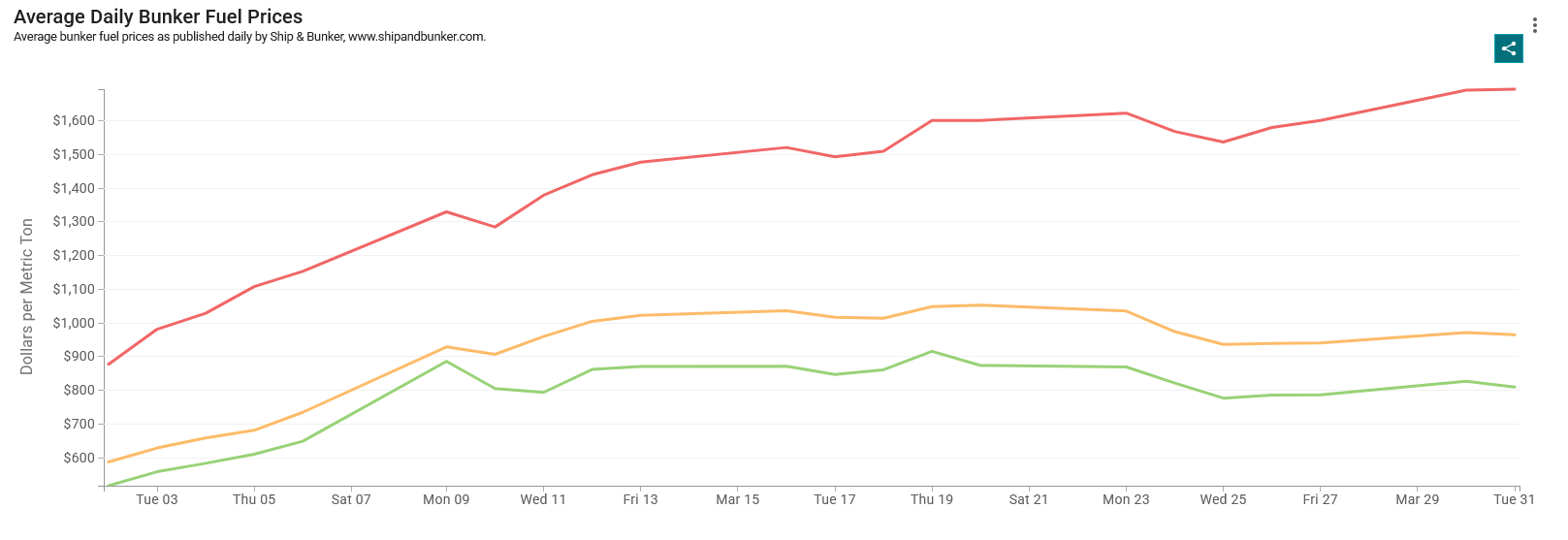

This is particularly relevant when looking at marine fuels. While Marine Gas Oil (MGO), a refined product very similar to diesel, rose significantly in March, the heavier Intermediate Fuel Oil and Very Low Sulfur Fuel Oil both rose considerably less.

Diesel and marine fuels are the essential components of all transportation and logistics. Goods cannot be shipped anywhere if there is not fuel for both ships and trucks.

While MGO is a cleaner alternative to even VLSFO, the far more moderate price increases in IFO and VLSFO will undoubtedly make those two refined products more attractive as bunker fuels for at least the short term.

One reason the apocalyptic predictions surrounding the price rises in diesel have not yet come to pass is that diesel is simply not the whole story on fuels needed to move cargo around the world.

Fuel prices are up not just around the world but across the board. Higher fuel prices are going to challenge freight operators, as they struggle to move goods, pay for fuel, and keep showing a profit. However, while fuel has become significantly more costly, we have so far not seen the levels of fuel scarcity we would need to see to produce the apocalyptic knock-on effects some have predicted would emerge.

If the war with Iran drags on, and especially if the closure of the Strait of Hormuz drags on, there is a possibility we could reach those levels of fuel scarcity. We are not there yet, and we should not reflexively assume that we will get there. A sudden outbreak of peace and we do not get there, now or ever.

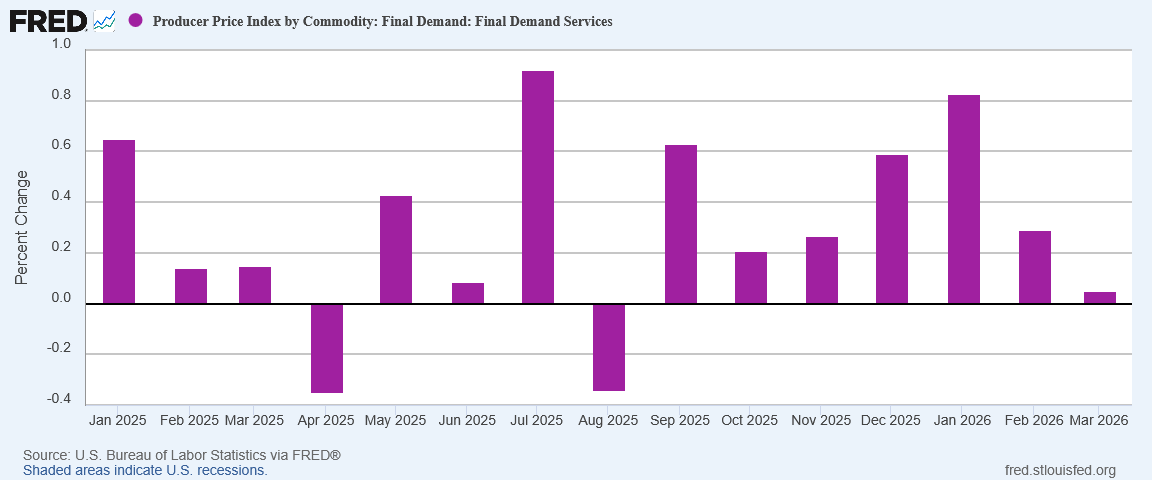

Goods Prices Surged, Service Prices Sagged

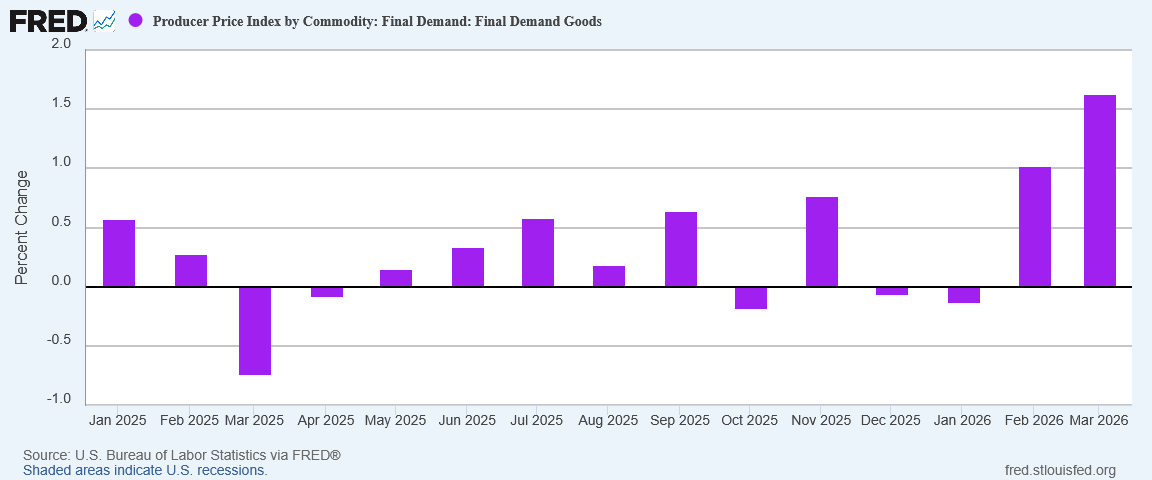

Goods were the other subindex besides energy that saw a significant inflation surge, with goods prices climbing 1.6% in March.

In contrast, service prices barely rose at all in March.

Even within the goods subindex, energy goods were a significant contributor to overall inflation.

By comparison, the contribution of goods besides food and energy was quite a bit less.

Even within goods, by far the dominant factor driving factory gate inflation in March was energy. But for the surge in energy prices, there was not much factory gate inflation in March at all.

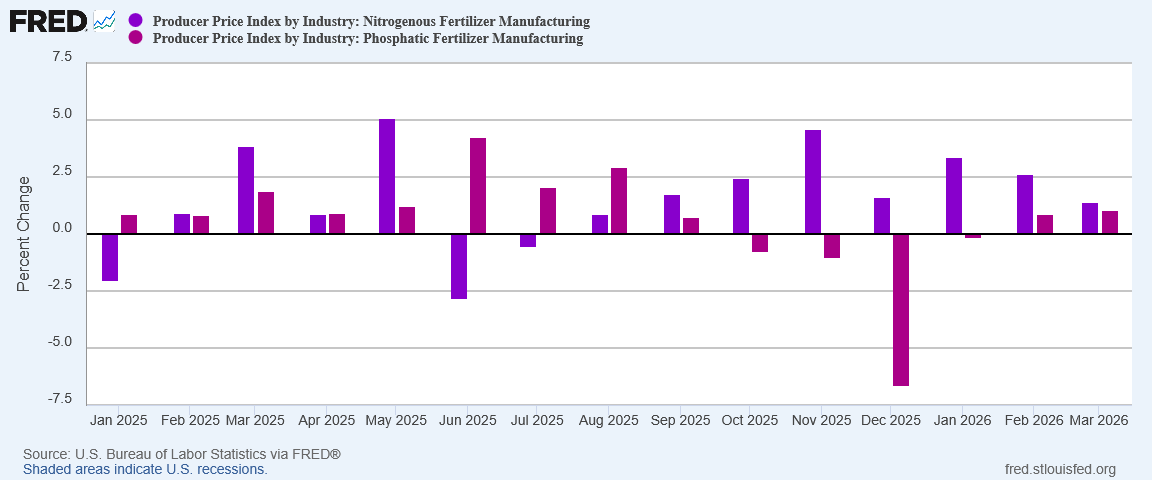

Good News For Fertilizer

Another product that warrants scrutiny within the Producer Price Index is fertilizer.

Several fertilizers, particularly ones to enrich phosphorus and nitrogen in the soil, are derived from fossil fuels. Given the surge in crude oil prices, we might expect to see dramatic increases in fertilizer prices as well.

Except we haven’t seen that—at least, not yet. For both nitrogenous and phosphatic fertilizers, producer price inflation was fairly muted in March.

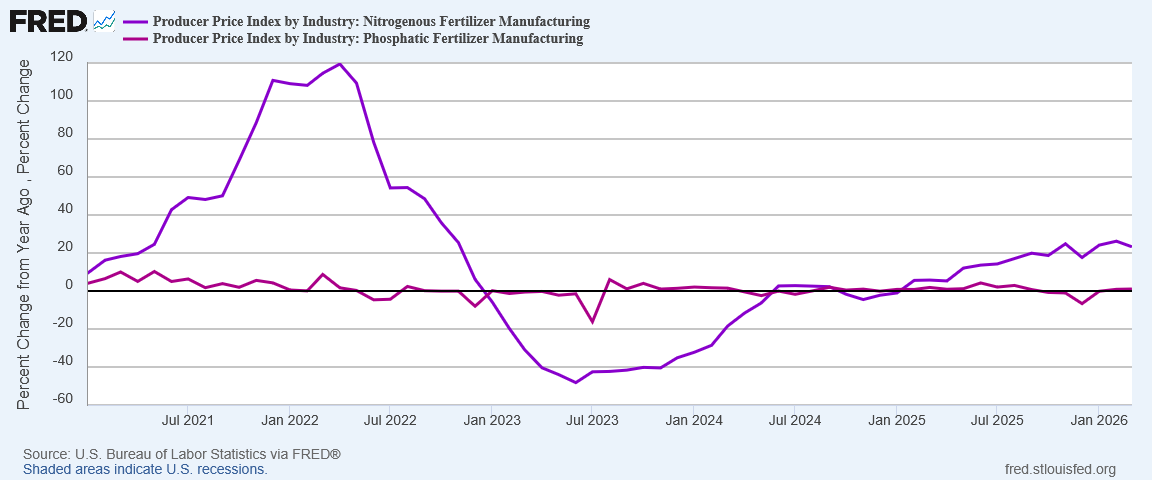

If we look at the year on year inflation prints for both, we see even less indication of a surge easily connected to the war with Iran.

Factory gate price increases year on year for nitrogenous fertilizers have been rising since the start of the year, coming out of a prolonged deflation phase where much of the price surges of the 2022 hyperinflation cycle were unwound.

Phosphatic fertilizers have seen barely any price increase year on year.

This is particularly good news for farmers everywhere. Fertilizers are an essential link in the food supply chain. Without fertilizers crop yields will decline, harvests will be more sparse, and food price inflation will rise. Food price inflation today can become food insecurity tomorrow, especially among the poorer nations in the world.

As with prices for other goods, we may yet see a surge in fertilizer pricing if the war with Iran drags on long enough. If we do see a surge in fertilizer pricing we could see issues with falling harvests and rising food price inflation—and today’s food price inflation can become tomorrow’s food insecurity.

However, as with everything when it comes to either producer prices or consumer prices, the key word in every assessment is “if”. If certain trends prevail then certain outcomes will happen—but if other trends prevail then other outcomes will happen.

A Look Ahead?

The Producer Price Index has long been seen as a predictor of coming levels of inflation as reported by the Consumer Price Index. One way of looking at the two indices is that the PPI looks at prices when goods are at the loading dock, while the CPI looks at prices when goods are at the cash register with the consumer making the purchase. While that is an oversimplification in many ways, the analogy does illustrate how the PPI can (and occasionally does) anticipate the CPI.

We already have an energy price shock within consumer price inflation. The surge in crude prices has been sufficiently dramatic that it wasted no time in making its presence known within consumer prices.

The March PPI shows the same energy price surge we saw in the March CPI. If the PPI is a predictor of the CPI, then we are looking at the possibility of a further surge in energy prices within the CPI for April, and possibly even for May. We are not (yet) looking at a surge in prices beyond energy goods within the CPI for April or May.

Certainly if the war with Iran continues, and especially if the Strait of Hormuz remains closed, we will see additional price surges primarily in energy. At some point, however, the rise in fuel costs is going to put pressure on other prices, and what starts out as energy price inflation almost exclusively could become far more broadly based. If that should happen, it may be the beginning of a new hyperinflation cycle.

Alternatively, sustained high fuel prices could also suppress consumption, potentially even driving down some prices. In that scenario not only would broader goods prices largely stay the same or decrease, we could also see further declines in employment as well. As I have mentioned before, that scenario could lead us into a stagflationary crisis similar to what this country went through in the 1970s.

There are no crystal balls to tell us which scenario will unfold. If the war with Iran comes off the rails we could easily see a fairly catastrophic inflation scenario emerge. If the war with Iran ends tomorrow we will, in all probability, see a drop in crude oil prices and a rise in Persian Gulf crude oil production.

The economic impacts of the closure of the Strait of Hormuz, along with the wider war prosecuted by Iran before the ceasefire, are likely to persist for some time after the war ends, even if by some miracle the war ends tomorrow. Even if the war ends we will not see an immediate return to pre-war price levels.

For now, those economic impacts are confined primarily to energy. If the price surge lasts long enough, we will see higher fuel costs push up prices in other categories as well, as producers confront the increased cost challenges of bringing their goods to market. However, we do not have that now, and if the war ends quickly we may not have it ever.

If.

During wartime, any little bit of good news is something to be savored. Thanks, Peter, for some reasons to believe that things might be better in time for the November elections!