The Fed Needs A New Inflation-Fighting Strategy

Will Jay Powell Rise To The Moment Or Bail By Pivoting Back To QE As Wall Street Demands?

As I have argued more than once, Jay Powell and the Federal Reserve have very little control over the consumer price inflation this nation is currently experiencing.

While few bankers and Wall Street investment types will admit this straight out, a good many say substantially the same thing, as does Candace Browning, head of Global Research for Bank Of America.

If you’re looking for lower inflation soon, you might be disappointed. A look at history suggests once inflation gets above 5% in advanced economies (AEs), it takes an average of 10 years to drop to 2%. Consensus views still expect G10 inflation to drop to 2% by 2024 but we are concerned it could take longer.

A 10 year glide path from >5% consumer price inflation to ~2% consumer price inflation equates to the Fed’s interest rate hikes not doing a damn thing to influence consumer price inflation.

What the Fed’s interest rate hikes do seem to be influencing are equity markets—as the Fed has hiked rates, the Dow Jones and S&P 500 stock indices have consistently trended down.

Unsurprisingly, Wall Street is not happy about this trend and would like it reversed forthwith. Hence the apocalyptic warnings of a financial “crisis” from such Wall Street luminaries as Mohamed El-Erian.

Mohamed El-Erian has a cautionary word for anyone anticipating an end to interest-rate increases from the Federal Reserve and other central banks.

“All of you who are looking for a pivot, be careful what you wish for,” the chief economic adviser at Allianz SE and Gramercy Funds chairman told Bloomberg Television’s The Open on Friday. “This pivot only happens if you have an economic accident or a financial accident. And the journey to an economic accident or a financial accident is a very painful journey.”

The upshot is the Fed’s strategy for fighting inflation is on a collision course with financial market reality. Despite not being effective at reducing consumer price inflation, Powell’s rate hikes nevertheless are threatening Wall Street with a liquidity crisis—an “economic accident”, as El-Erian put it.

Heads Wall Street loses, tails Main Street doesn’t win.

The Fed’s Time For Choosing Is Approaching

To combat consumer price inflation, the Fed knows of only one weapon to use: interest rates. The prevailing wisdom at the Fed is that to contain inflation one must raise interest rates.

However, as the Fed raises interest rates, not only is it pushing equity prices down and producing asset price deflation, those price declines arguably have knock-on effects that can and are starting to roil financial markets.

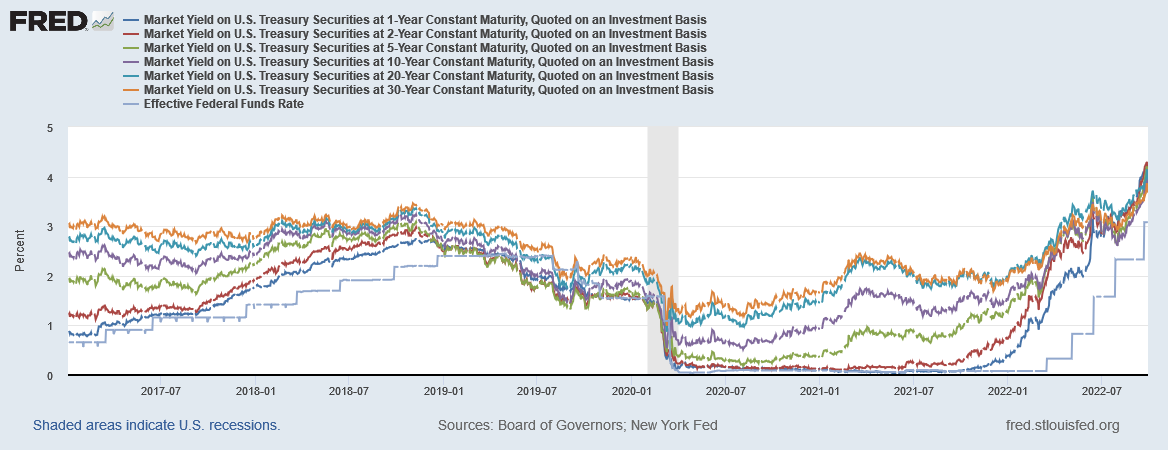

Most notably, as the Fed raises interest rates by raising the Federal Funds Rate, debt yields rise pretty much across the entire spectrum of debt.

While this obviously increases the cost of capital for the US Treasury Department, it also pulls up corporate debt as well, particularly the “high yield” (aka “junk”) debt issuances, on which yields have been rising faster than on long-term Treasury debt.

Wall Street is watching this increase in yield spreads and, to put it kindly, “freaking out.”

The Federal Reserve needs to slow the pace of rate hikes to prevent credit market dysfunction, warned Bank of America Corp. strategists.

Distress, dispersion and debt-to-enterprise-value ratios were all above June highs, pushing the bank’s measure of credit stress to a “borderline critical zone” this week, strategists Oleg Melentyev and Eric Yu said.

The source of Wall Street’s pain begins with its love of debt issuance to execute buyouts and corporate mergers—what’s known as the “leveraged buy-out”, or LBO. Rising yields on corporate junk debt is making LBOs more expensive, and even prohibitively expensive.

Wall Street banks trying to offload tens of billions of dollars in high-risk leveraged buyout debt are finding it increasingly tough as yields surge.

On Thursday, a group led by Bank of America Corp. and Barclays Plc scrapped a $3.9 billion debt sale for the buyout of an Apollo Global Management Inc.-backed telecom business called Brightspeed. The retreat follows an LBO fundraising for Citrix Systems Inc., which sold at rock-bottom prices last week, leaving lenders with about $600 million in losses.

Because the Fed is the driving force behind the rising debt yields, Wall Street’s analysis of the problem is simple: the Fed’s interest rate hikes are crimping their style, and so the Fed needs to stop hiking rates.

Wall Street Is Accustomed To Cheap Money And Abundant Liquidity

After over a decade of cheap money and the Fed providing all the liquidity any hedge fund could possibly want, Wall Street is not responding well to the Fed’s “quantitative tightening” stance, particularly after the massive amount of liquidity support the Fed injected into the markets in 2020 as part of the pandemic lockdowns.

Even the corporate media acknowledges that Wall Street’s above-average 2021 results were the consequence of the Fed’s money printing.

“2021 was another exceptional year for U.S. equity markets,” Wells Fargo Investment Institute’s Chris Haverland said in a note. “The markets were supported by ... highly accommodative fiscal and monetary policies.”

Now the Fed is being less accommodating and Wall Street is throwing yet another “taper tantrum”.

Nor is it merely the Fed’s rate hikes that have Wall Street worried about debt yields. As the Fed raises rates, yields on Treasury debt—the money used to fund the US government and all its many programs—goes up. The fear is that, as interest rates and yields rise, the Treasury will be compelled to issue even more debt to compensate for the increasing interest rate costs—and the more the Treasury saturates credit markets with debt issuance, the higher corporate yields have to rise to make corporate debt sufficiently attractive.

In response to an inquiry from Rep. Jason Smith (R-MO), the CBO said in August that each increase in federal debt of 1% of gross domestic product raises interest rates by 2 to 3 basis points. Thus an increase in federal debt of 10% of GDP would boost interest rates by about one-quarter of a percentage point

“Over time, additional debt could lead to increased concerns by market participants that the U.S. government would allow high inflation to erode the real value of the debt,” the CBO report read. “Ultimately, such concerns could lead to a fiscal crisis in which interest rates rose markedly as market participants required higher compensation to lend to the Treasury.”

A potent example of this feedback-loop phenomenon was on display in the UK this past week, where the markets went into meltdown over newly-installed Prime Minister Liz Truss’ “mini budget”, which proposed massive tax cuts in an effort to stimulate the economy, the cost in terms of lost government revenue apparently was largely unfunded, and the fear of expanded government borrowing drove bond yields skyward.

This in turn triggered a wave of margin calls among UK pension plans, which had been investing on margin to boost their returns.

The problem centred on the use of niche financial products offered by investment banks to pension funds that are trying to manage or hedge their risks. Those products – known as liability-driven investing, or LDIs – help offset liabilities and risks on pension funds’ books.

However, as asset prices slumped over the week – including UK government bonds, or gilts – those banks required more collateral to offset the pension funds’ liabilities, forcing the funds to dump assets and raise cash at short notice.

Wall Street is fearing the same phenomenon here in the US only in reverse, with the Fed boosting interest rates, leading to a similar increase in government borrowing, adding ever more stress to credit markets.

Financial substack QTR’s Fringe Finance fears this will lead to a meltdown in US pension plans not unlike what the UK witnessed this past week.

Wall Street, just like financial markets world wide, it seems, simply does not know how to respond to the money spigot being turned off. Tighter monetary policy and higher interest rates seem fated to always give the investor class a case of the vapors.

The Fed Needs A New Game Plan

The challenge for the Fed lies in the ultimate inefficacy of the Fed’s inflation fighting tactics to date. While the rate hikes are notionally about fighting inflation, as I have noted many times, thus far they have had little or no impact on consumer price inflation. Indeed, the impotence of the Fed’s rate hikes shows that Jay Powell has no control over consumer price inflation, contrary to the Fed’s arrogant pretensions otherwise.

The Fed is facing a reckoning and a choice. Yet the real choice is not simply abandoning rate hikes and pivot back to quantitative easing. Rather, the Fed is being challenged to find a strategy that actually reduces consumer price inflation. That strategy likely won’t make Wall Street happy, because Wall Street wants endless easy money, but the Fed’s current course is sure to make both Wall Street and Main Street unhappy—tight money distressing the one while stagflation and recession burdens the other.

Can Jay Powell get inspired and write a new inflation-fighting playbook more applicable to the current economic crisis? Only time will tell, although putting “Jerome Powell” and “inspiration” in the same sentence requires a degree of credulity that is hard to justify.

Powell said in Colorado they need a balance supply and demand.

Why not fix the supply chain?

Why not open up energy?

Why not get off this E.S.G. BS?

You're aware the Fed called an emergency board meeting under "Expedited Procedures" right?

https://www.federalreserve.gov/aboutthefed/boardmeetings/20221003closed.htm

Kinda makes you wonder what the emergency is. What's in imminent danger of blowing up?