There is no small amount of irony in Xi Jinping’s serial climbdowns and policy reversals, so soon after securing his position as China’s leader for life. No sooner than he gained near absolute power over China than circumstances intervened to circumscribe the measure of Xi’s power.

Beijing has vowed to go all out next year to save its Covid-hit economy by boosting consumption and loosening control over private industry, including the struggling tech and property sectors. The new pledge marks a big shift from leader Xi Jinping’s years-long effort to rein in private businesses, which were perceived as too powerful and “disorderly.”

Faced with a choice between “common prosperity” and “any prosperity”, Xi Jinping and the CCP have apparently chosen the latter.

Since late 2020, under Xi Jinping’s “common prosperity” drive, the authorities have launched a regulatory onslaught on sectors ranging from e-commerce to real state to education. The crackdown began in October of that year, when regulators yanked the blockbuster IPO of Jack Ma’s Ant Group, days after he gave a controversial speech that criticized China’s financial regulations for stifling innovation.

However, China’s economy has not thrived under “common prosperity”, and Xi is now feeling pressure to take drastic action to address the ongoing economic contraction.

In particular, Xi needs to reverse China’s declining industrial output, which in November only grew by 2.2%, far less than the 3.6% growth that had been forecast.

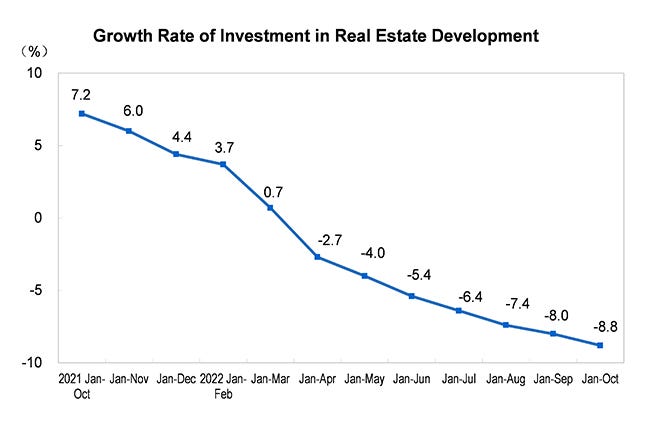

From January to October, the national real estate development investment was 11,394.5 billion yuan, a year-on-year decrease of 8.8 percent; Among them, the residential investment was 8,652 billion yuan, down 8.3 percent.

China will implement a proactive fiscal policy and a prudent monetary policy next year, said the statement, issued after the annual Central Economic Work Conference and published by the official Xinhua news agency.

Fiscal policy will be stepped up and become more efficient, maintaining the necessary intensity of spending, while monetary policy will be precise and forceful, keeping liquidity reasonably ample, the statement said.

"Next year, we will prioritise stability and strive for progress," the statement said.

China should better coordinate epidemic prevention and control, and economic and social development, it added.

Key measures include allowing banks to extend maturing loans to developers, supporting property sales by reducing the size of down payments and cutting mortgage rates, boosting other funding channels such as bond issues, and ensuring the delivery of pre-sold homes to buyers.

“In essence, policymakers told banks to try their best in supporting the property sector,” according to Larry Hu, chief China economist for Macquarie Group.

At this juncture, not only are Xi Jinping’s “three red lines” from 2020, meant to restrain out-of-control debt among real estate developers, effectively canceled, but Xi and the CCP are committing government support throughout the economy for 2023, including increased deficit spending and bailing out financially strapped local governments.

Proactive fiscal policies should be strengthened to improve efficiency. Maintain the necessary fiscal expenditure intensity, optimize the combination of deficits, special bonds, interest discounts and other tools, and ensure fiscal sustainability and local government debt risks are controllable while effectively supporting high-quality development. It is necessary to increase the central government's transfer payments to local governments, promote the sinking of financial resources, and do a good job in the "three guarantees" work at the grassroots level.

The shift in emphasis towards economic development effectively reverses Xi Jinping’s earlier pledges of “common prosperity” economic reform, which last year had focused on income redistribution, ideally raising incomes among the poor and expanding the middle class while curtailing incomes among the rich.

Chinese leaders have pledged to use taxation and other income redistribution levers to expand the proportion of middle-income citizens, boost incomes of the poor, "rationally adjust excessive incomes", and ban illegal incomes.

“Three Red Lines” is reversed.

“Common Prosperity” is in limbo.

“Zero COVID” has been ended—by popular demand.

Xi Jinping’s signature policy initiatives, and the substance of what would have been his legacy as China’s most powerful leader since Mao Zedong, have all been largely cast aside, pushed out of reach by the realities of economics and the dynamics of infectious respiratory disease.

Any one of these reversals would represent a tremendous loss of face for Xi. While pronouncements from the CCP leadership continue to wrap these climbdowns in rhetoric which pays lip service to “Xi Jinping Thought” and the rubric of “Socialism With Chinese Characteristics”, the unavoidable reality is that Xi and the CCP are reacting to events within China; they are very much on the back foot both economically and politically.

The premise of totalitarian rule is that the autocrat is in control of all things—he controls how the people will function as an economy and as a society. The unwinding of Zero COVID and the collapse of China’s economy effectively shreds that premise for Xi’s autocratic rule. Xi is in total control of the Beijing government, and has precious little control over anything else.

The large unspoken question now looming over China is simply this: How will Xi respond as the reality of his less-than-total rule becomes plain for all to see?

All Facts Matter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber. Alternatively, please consider leaving a tip through Ko-Fi. Thank you always for your support!

Again, China is something to be admired according to the AOCs & Bernies of the gov’t. But look at what hardcore communism gets you: nothing. And just like that, even Xi realizes that he needs to take the reins off.

Again, China is something to be admired according to the AOCs & Bernies of the gov’t. But look at what hardcore communism gets you: nothing. And just like that, even Xi realizes that he needs to take the reins off.

The emperor has no clothes?

Which reminds me, Putin didn't look bad shirtless on the horse. I doubt Xi could "pull it off," so to speak. Maybe if he rented a Clydesdale?