ADP Reports Second Consecutive Month Of Solid Job Growth

The Report Is Good, But Is It Good Enough?

While the Bureau of Labor Statistics’ job reports in February blew way past “ugly” and landed square in “fugly” territory, ADP produced job numbers that were far more optimistic.

ADP repeated that result again for March, with a jobs print that at the headline number was virtually identical to February.

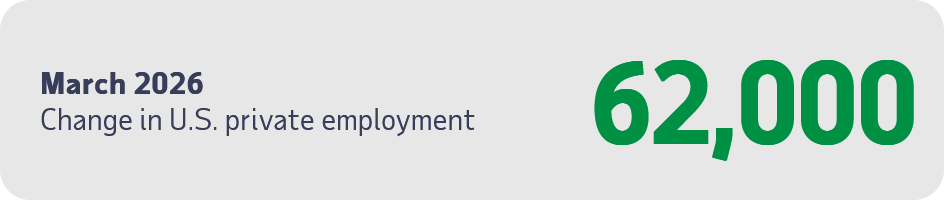

Private sector employment increased by 62,000 jobs in March and pay was up 4.5 percent year-over-year according to the March ADP National Employment Report® produced by ADP Research in collaboration with the Stanford Digital Economy Lab (“Stanford Lab”).

February, readers will recall, ADP put job growth at 63,000.

That figure has since been revised upward, to 66,000.

Dr. Nela Richardson, ADP’s Chief Economist, offered her usual upbeat assessment of the ADP jobs data.

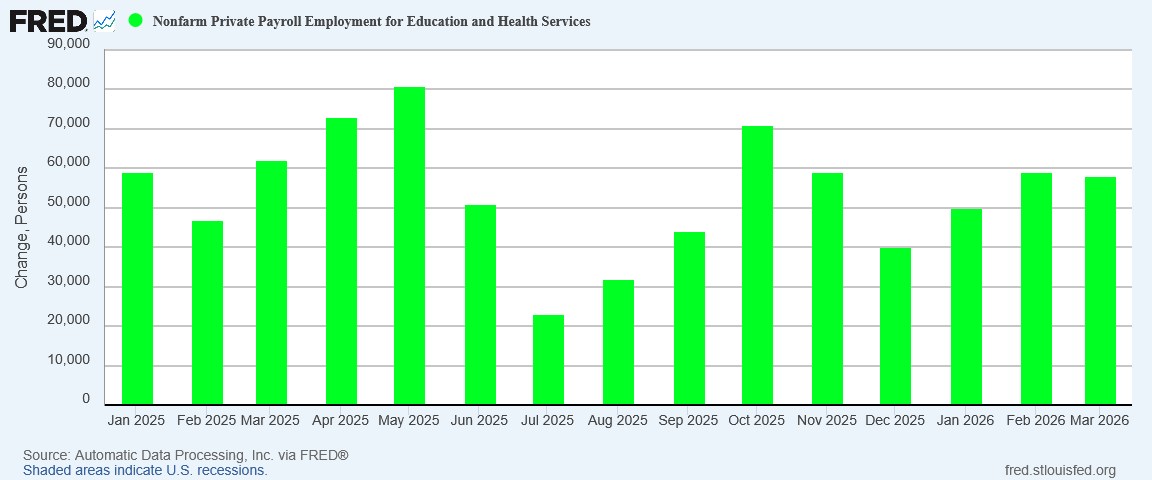

Overall hiring is steady, but job growth continues to favor certain industries, including health care. In March, this solid performance was accompanied by a boost in pay gains for job-changers.

There is no denying that ADP is reporting two months of solid job growth. 66,000 jobs in February and 62,000 jobs in March is indisputably solid job growth.

Whether 60,000+ new jobs each month is enough job growth to meet the needs of the US economy is a much more problematic assertion. The ADP jobs numbers may be good overall, but there is also good evidence to support the contention that 60,000+ jobs is not quite good enough.

Above Breakeven?

Presumably, 60,000+ jobs created per month is above the country’s current “break even” creation rate—the rate at which job creation matches population growth to keep the unemployment rate stable.

As recently as 2024, the breakeven unemployment rate was considered to be six figures. But now, the number may be far lower. Researchers at two think tanks, the Brookings Institution and the American Enterprise Institute, estimated in a paper last month that it could be as low as 10,000 to 40,000.

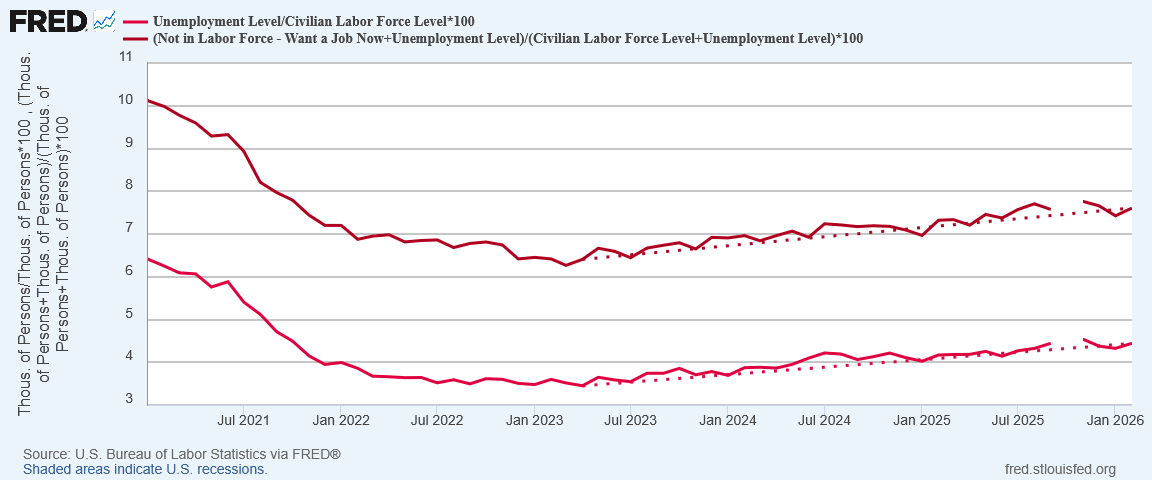

Whether ADP’s jobs print is above the breakeven rate is debatable, however. The BLS data indisputably shows that joblessness has been on the rise in this country.

Even in the official unemployment data, joblessness is on the rise. If we consider as well those not in the labor force but who want a job now, not only is that “real” unemployment rate higher than the official rate, it has been rising incrementally faster as well.

If the unemployment rate is rising, we are not creating jobs above the breakeven rate. To be above the breakeven rate we would need to see sustained decreases in the unemployment rate. That is not what is happening.

62,000 jobs is solid job growth, but we almost certainly need more job growth than that each month if we do not want to see the unemployment rate rise any further.

Rising joblessness means the ADP National Employment Report is showing solid not not quite sufficient job growth. We are still shy of where we need job growth to be if we want to see an ending to the jobs recession.

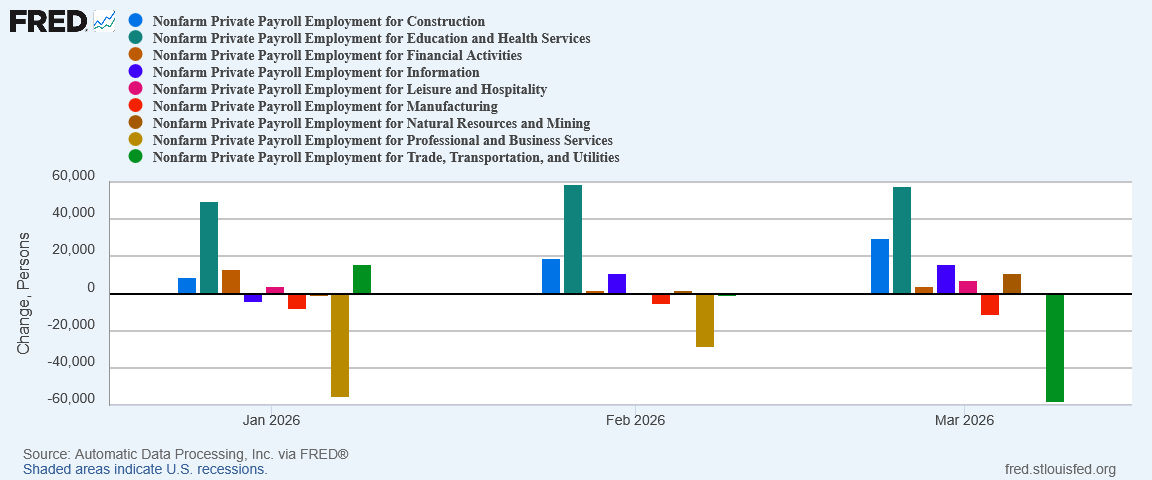

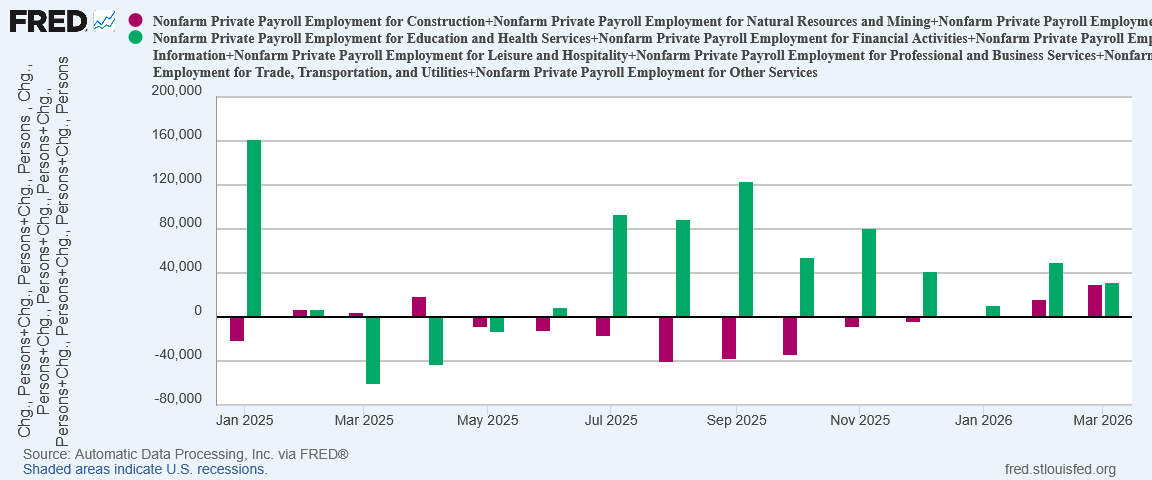

Two Sectors Did All The Work

Also of concern is that, once again, job growth was focused on only one or two economic sectors, to the detriment of the others.

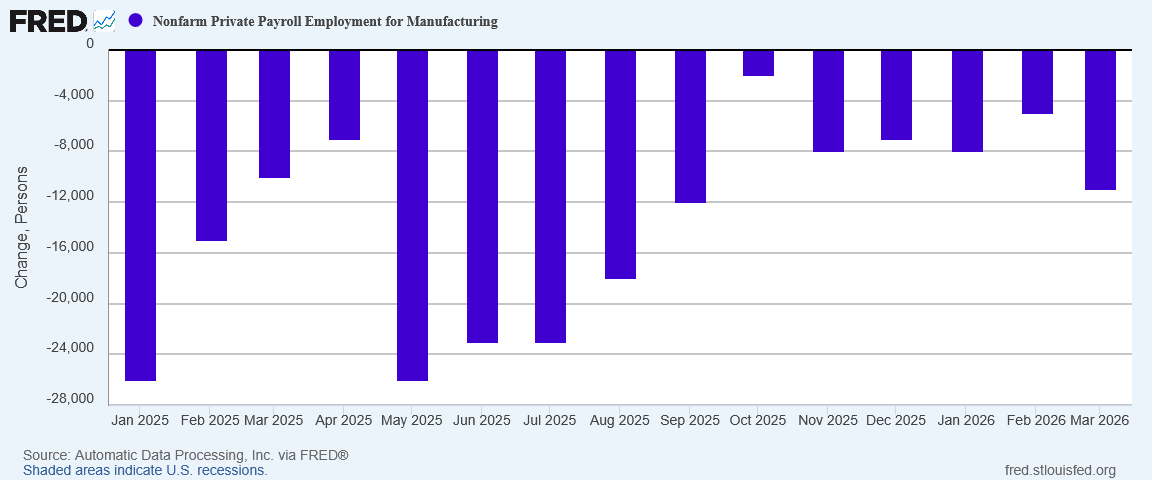

Even within ADP’s solid jobs report, we still have manufacturing shedding jobs.

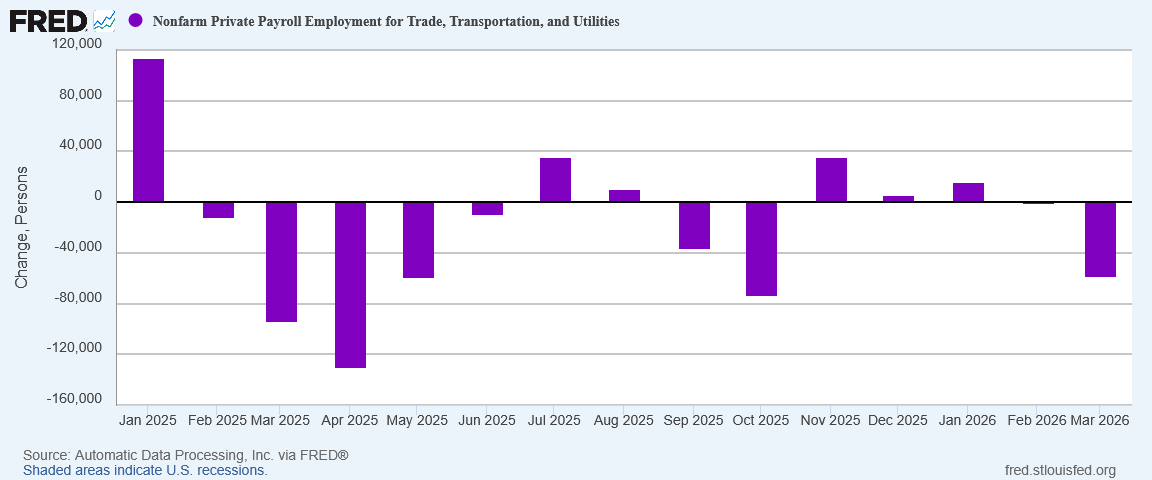

Even within ADP’s solid jobs report, we still have Transportation, Trade, and Utilities.

Much as has been the case for quite some time yet, March was yet another month where job growth was concentrated in just one or two sectors.

Healthcare has been a primary driver of job creation for quite some time, printing strong job growth at least as long as manufacturing has been printing job losses.

While the remaining economic sectors (Construction, Finance, Information, Leisure, and Professional Services) all showed some job growth, only Construction showed more than marginal, incremental growth.

Without Healthcare, and to a lesser extent Construction, the ADP report would show negative job growth at the headline level.

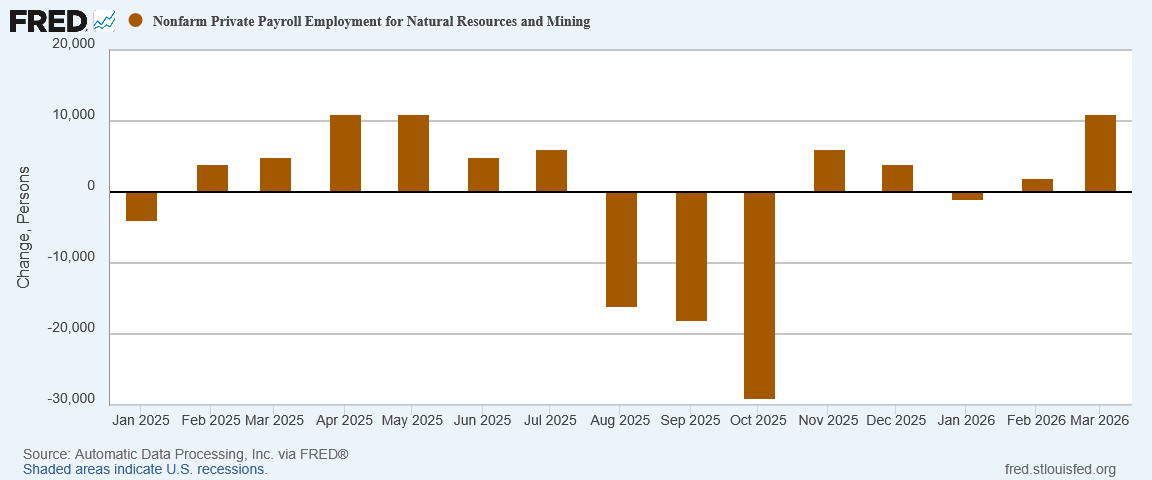

One small bright spot which deserves mentioning is the jump in Natural Resources and Mining jobs.

Is the uptick in mining employment part of the network effects from the war with Iran and resultant surge in oil prices? That is a plausible interpretation of the data in context, and while higher energy prices are distinctly undesirable, should they prove a jobs catalyst that would mitigate their negative economic impacts somewhat.

Mining jobs aside, however, what the ADP report is not showing is balanced job growth. It is not showing economically healthy job growth. The ADP report is certainly not showing the sort of job growth we need if President Trump is to realize his Agenda 47 goal of making the US a “manufacturing superpower”.

As good as the numbers might be, those are problems which we should not ignore.

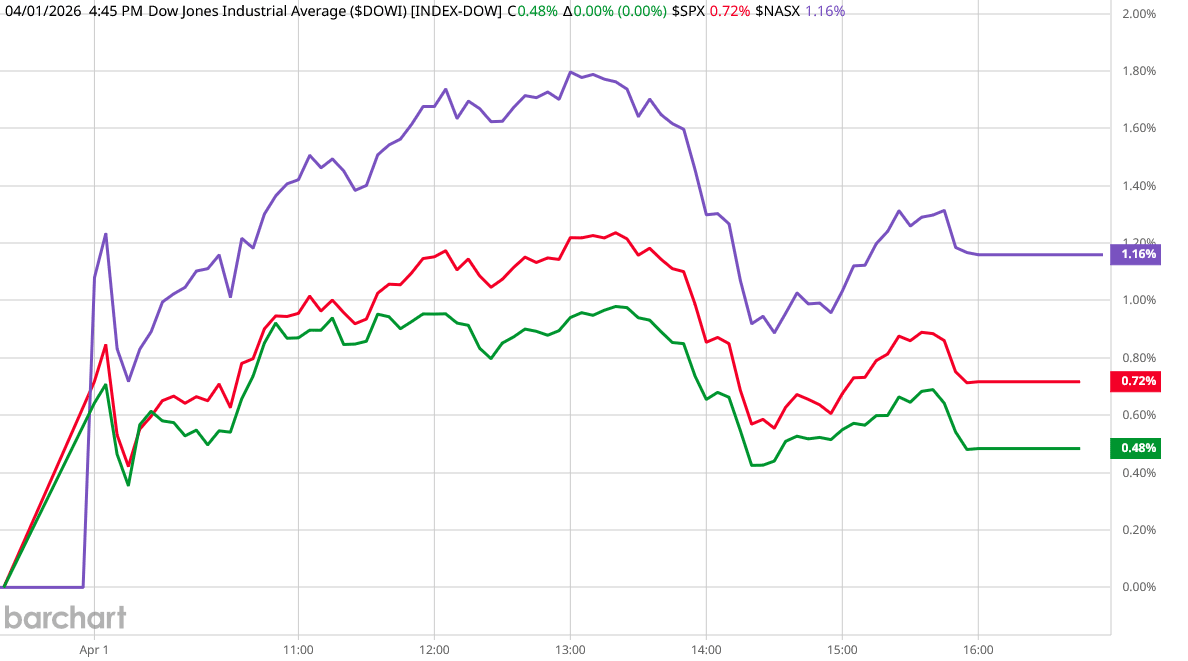

Wall Street Was Surprised—And Pleased

While the ADP report may or may not be above the breakeven rate for job creation, it was above what Wall Street anticipated for the month.

That Wall Street was pleasantly surprised is self-evident just from watching the Dow Jones Industrial Average, which had a good day for a change.

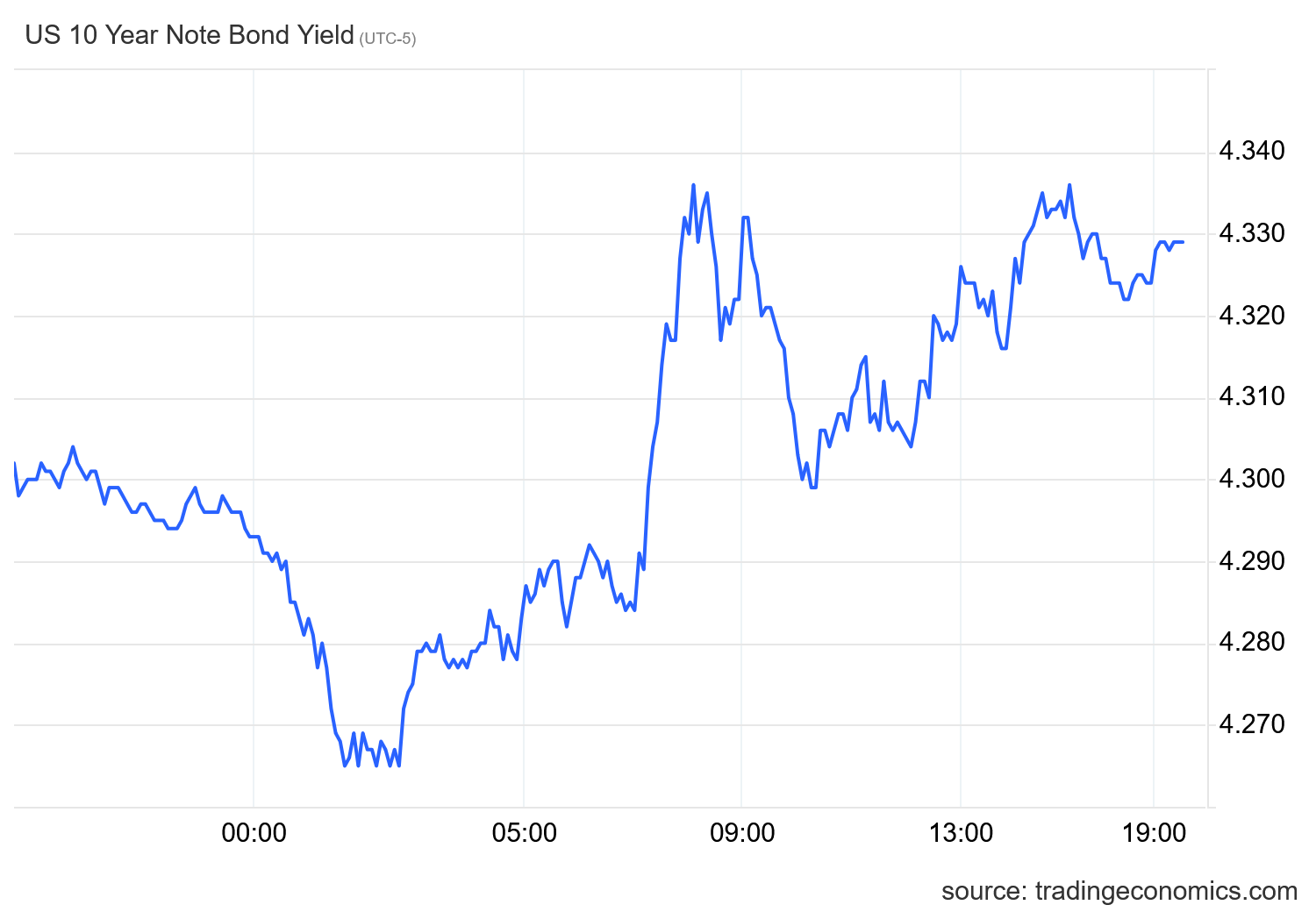

The euphoria was not complete, however, as Treasury yields continued their rise.

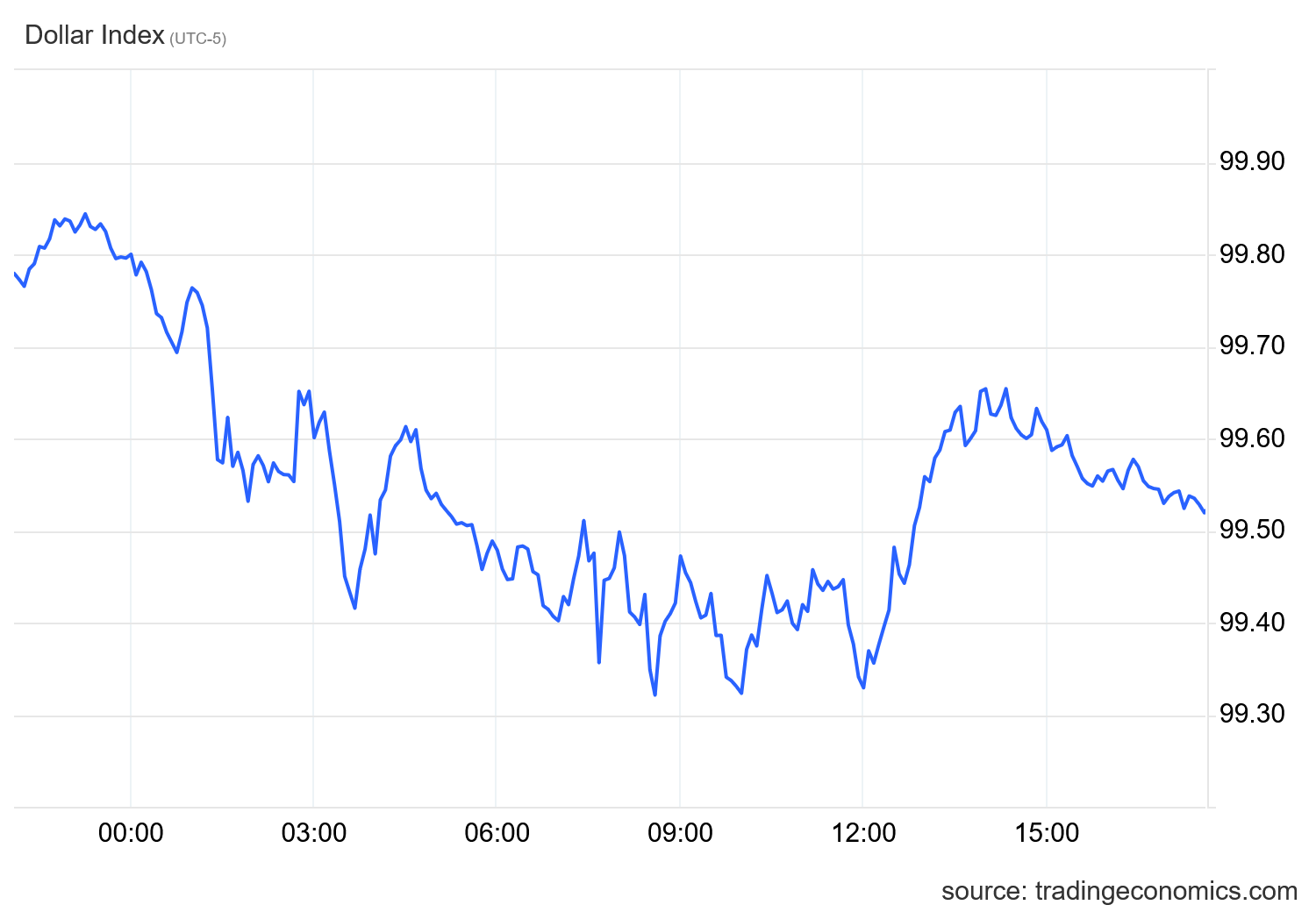

In forex markets, the dollar index had a down day, suggesting that international investors are somewhat less than enthused by the US economy at present.

In most regards, such uneven market results are a perfect reflection of the uneven and unclear messaging conveyed by the March ADP jobs data itself.

Good But Not Great Results

If the breakeven rate for job creation in this country is around 40,000 jobs each month, then the ADP National Employment Report has for the second month in a row turned in a solid jobs report.

If.

That joblessness and real unemployment rates have been rising for not just months but years at this point is a rebuttal to the premise of a lower breakeven rate. By definition, job growth above a breakeven rate produces a decline in unemployment, not an increase.

Moreover, that healthcare has been the primary engine of job creation in this country is problematic all on its own. Goods producing jobs—i.e., manufacturing and mining—tend to have higher wages. For that reason alone, there is an intrinsic economic preference for goods producing jobs.

While the March report itself was more or less evenly balanced between service jobs and goods producing jobs, it was the first such balanced month in over a year.

Healthy job markets in a healthy economy will produce robust job growth across all sectors and over time. The ADP report does not show the US producing balanced job growth. Job growth in the US has been particularly skewed towards service jobs, and towards healthcare jobs in particular.

Given that service jobs are overall lower-paying jobs than goods producing jobs, the tilt towards service jobs means the economy is cultivating less labor value. In a pure economic sense, the higher wage which tend to accompany goods producing jobs make such jobs more valuable.

As job growth is generally a predicate for wage growth, a tilt towards goods producing jobs would produce greater wage growth sooner. With wages still playing catch-up to the 2022 hyperinflation cycle, an emphasis on goods producing jobs would accelerate the restoration of long-term equilibrium between wages and prices.

The ADP National Employment Report does chart a headline jobs figure that is solid and is arguably above what many believe to be the breakeven rate for employment. That’s the good news.

The ADP National Employment Report does not chart balanced job growth. The report also does not show any indication that Manufacturing’s chronic job loss especially is about to end. That’s the bad news.

As a result, while the jobs recession in this country has not gotten any worse, neither has it gotten any better. For that we need considerably more good news and considerably less bad news than the March ADP report contains.

I’m relieved that it’s not worse. I’m hoping that the war will end soon, and consequently oil prices will come down and the economy will grow in sustainable ways. Europe, however, could be in for a long stretch of hard times. Peter, if the European economies continue to fail, do you see that as affecting the U.S. in disastrous ways, or will Trump’s policies enable us to prosper?