April PCE: More Of The Same Higher Inflation

Energy Price Inflation, But Little New Core Inflation

Consumer price inflation returned in March and has stayed in April. That is the immediate takeaway from the April Personal Incomes and Outlays report by the Bureau of Economic Analysis, released yesterday.

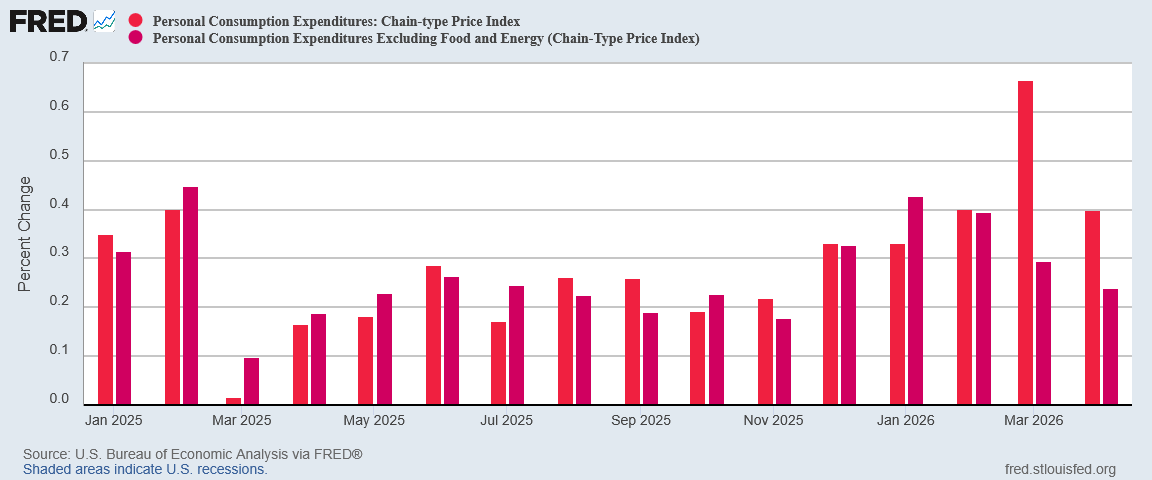

From the preceding month, the PCE price index for April increased 0.4 percent. Excluding food and energy, the PCE price index increased 0.2 percent.

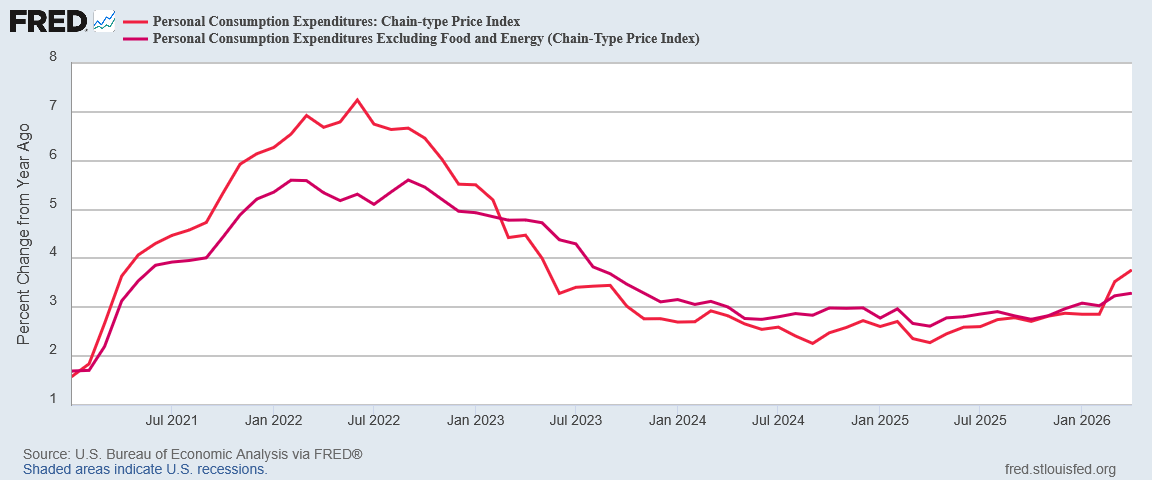

From the same month one year ago, the PCE price index for April increased 3.8 percent. Excluding food and energy, the PCE price index increased 3.3 percent from one year ago.

There is no mystery as to why inflation has returned: the United States, like the rest of the world, is experiencing an energy price shock as a result of Iran’s illegal closure of the Strait of Hormuz as part of the war between the US and Iran.

What is remarkable is that, somewhat contrary to expectations, the impacts of that energy price shock have not extended beyond energy prices into other goods and services, despite the rise in a variety of commodities prices and inputs.

Energy price inflation pushed the headline PCEPI number higher year on year, yet month on month consumer price inflation eased at the headline level, at the core level less food and energy, and for energy prices themselves.

One result of this fairly muted response to the continuing war with Iran was that Wall Street was able to project April’s PCEPI inflation numbers almost exactly.

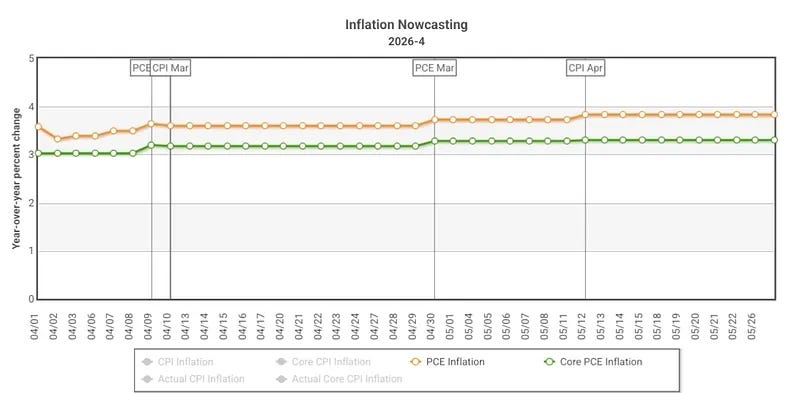

That the inflation numbers were fairly easy to project is confirmed by the Cleveland Fed’s inflation nowcast projecting April’s numbers with the same accuracy.

Despite the ongoing war with Iran, the PCE Price Index, the Federal Reserve’s favorite consumer price inflation gauge, showed inflation cooling month on month, resulting in a slower increase year on year.

Despite the ongoing war with Iran, consumer price inflation per the PCE Price Index is more of the same in April that printed in March.

If the Strait of Hormuz remains closed, that will not remain the case indefinitely. Cost pressures are building in the economy, and at some point we will see broader price increases for more than just energy prices.

We are not seeing them yet.

Little Room For Corporate Media Hype

The April PCE inflation data ironically gave corporate media little with which to spin their typically anti-Trump narratives. While corporate media headlines snarked about inflation rising at its fastest pace in three years, the buried lede was that April’s rise was less than March’s.

Economists polled by Reuters had forecast PCE inflation increasing 3.8% year-on-year. The PCE price index rose 0.4% month-on-month in April after shooting up 0.7% in March.

The nuance—ignored by corporate media—is the impact of cooler month on month inflation numbers.

A cooler month on month metric means that inflation’s rise year on year slowed in April rather than rose.

We should not pretend that April’s cooling indicators mean the worst of the price shock in energy is necessarily behind us. Consumer price inflation is still here, and the year on year numbers are higher than late summer in 2023.

We should, however, acknowledge that inflation has yet to heat up as it might, should the standoff between the US and Iran in the Persian Gulf persist.

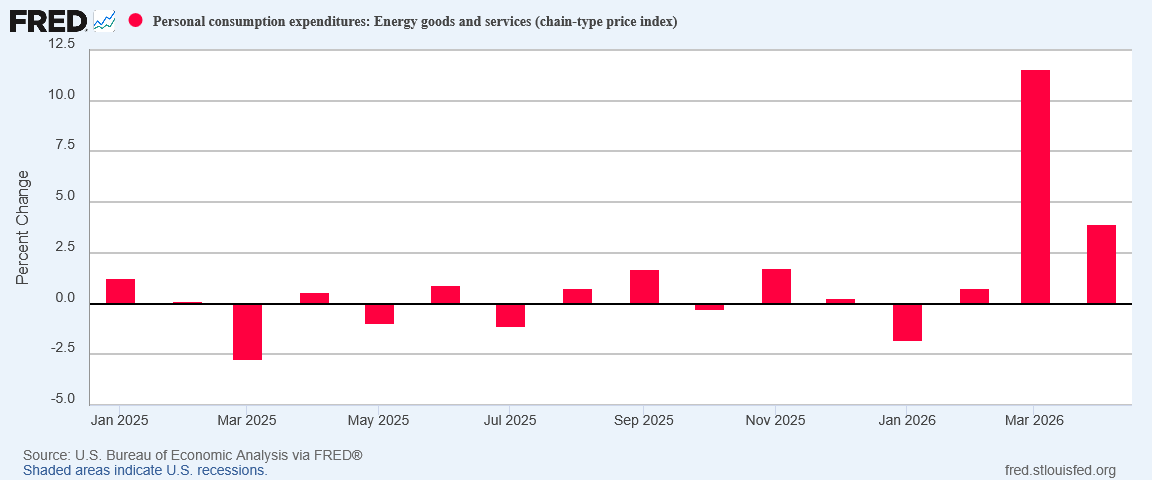

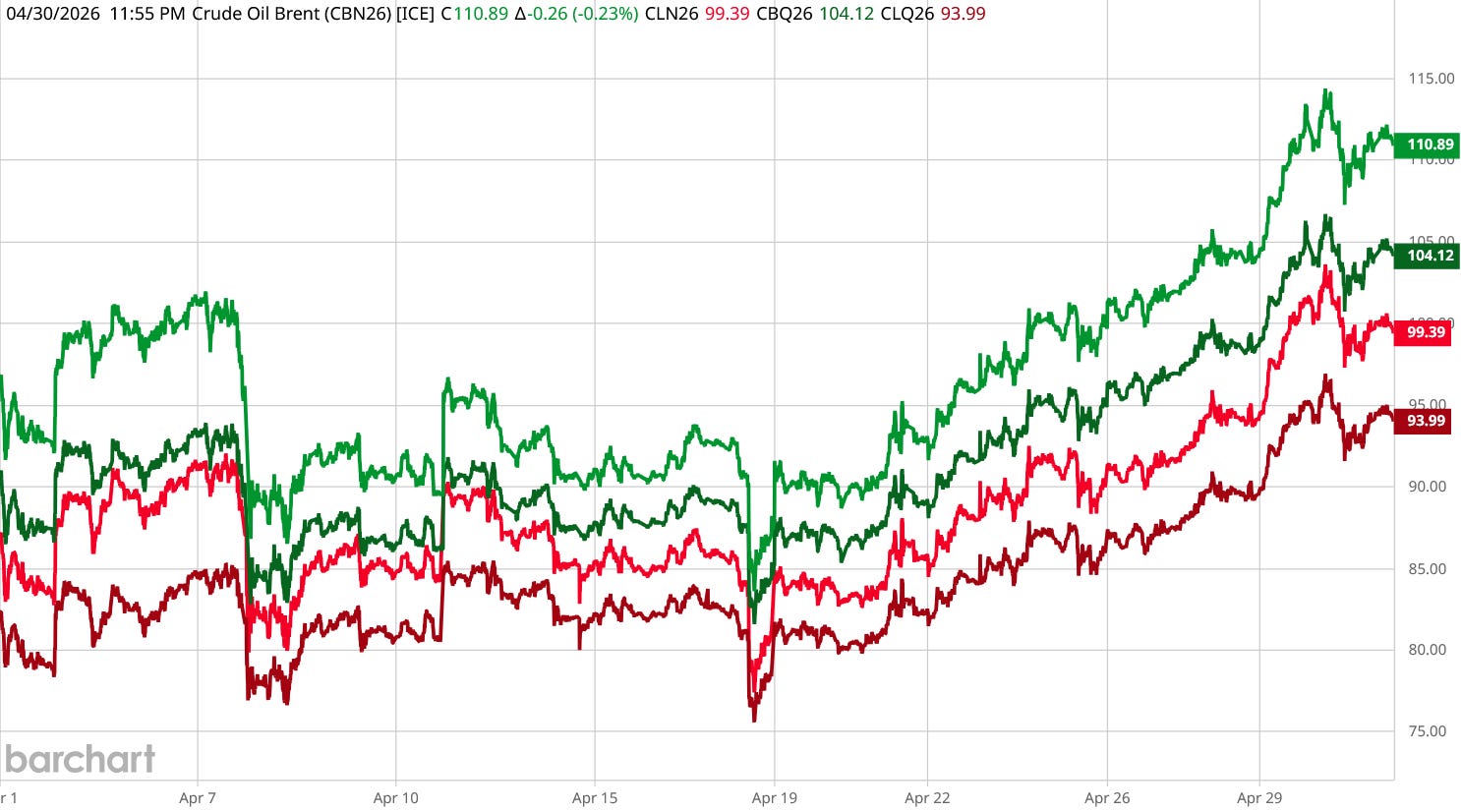

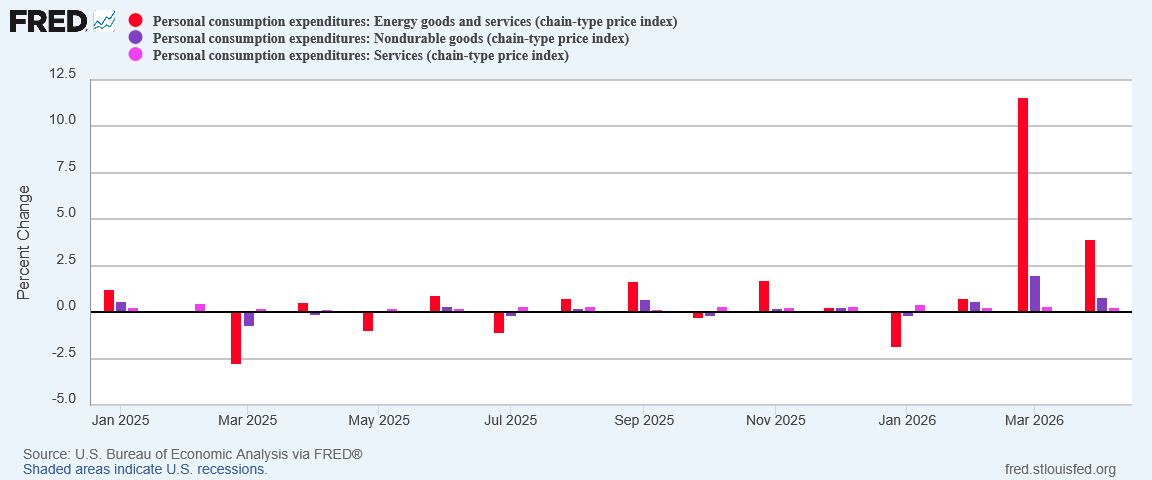

Energy Price Inflation Eased On Stabilizing Oil Prices

The elevated inflation metrics for April tell us that prices are indeed higher, with energy prices leading the way month on month, with April’s percent increase less than half of March.

The reality is that energy prices overall were showing signs of stability, albeit at a higher level than before the war with Iran.

Oil prices had actually been inching downward in the first part of April, before rising at the end of the month.

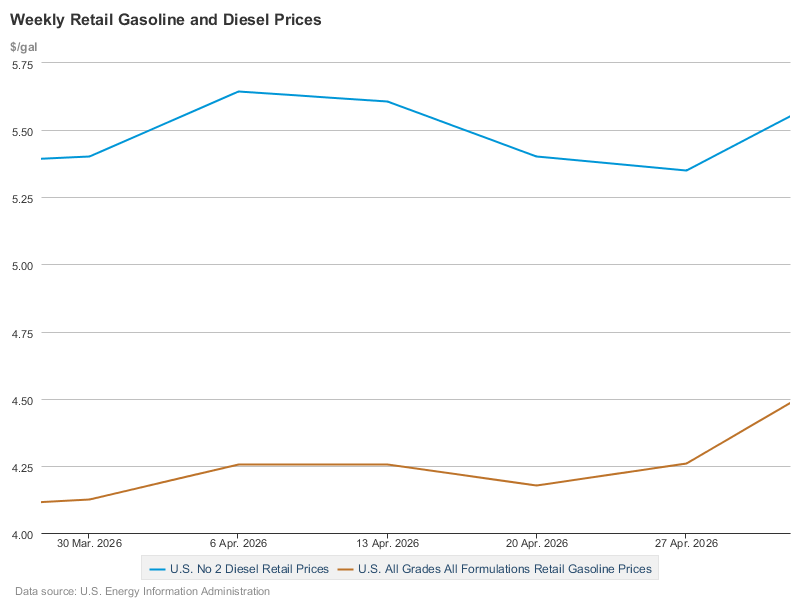

The price stability of early April helped move market prices for gasoline and diesel lower, with the increases not emerging until the last week or so.

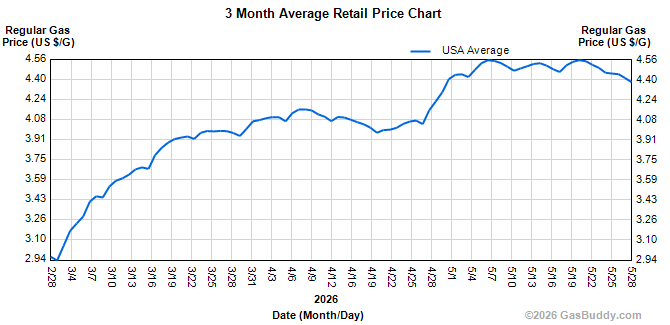

Even the EIA’s retail price data for gasoline and diesel fuel showed stability during April.

The stabilization trend was confirmed by private reporting of retail gas prices.

There is an important distinction to be made between prices that are high and prices that are getting higher. For most of April, energy prices, and fuel prices in particular, were high but did not go higher until the end of the month.

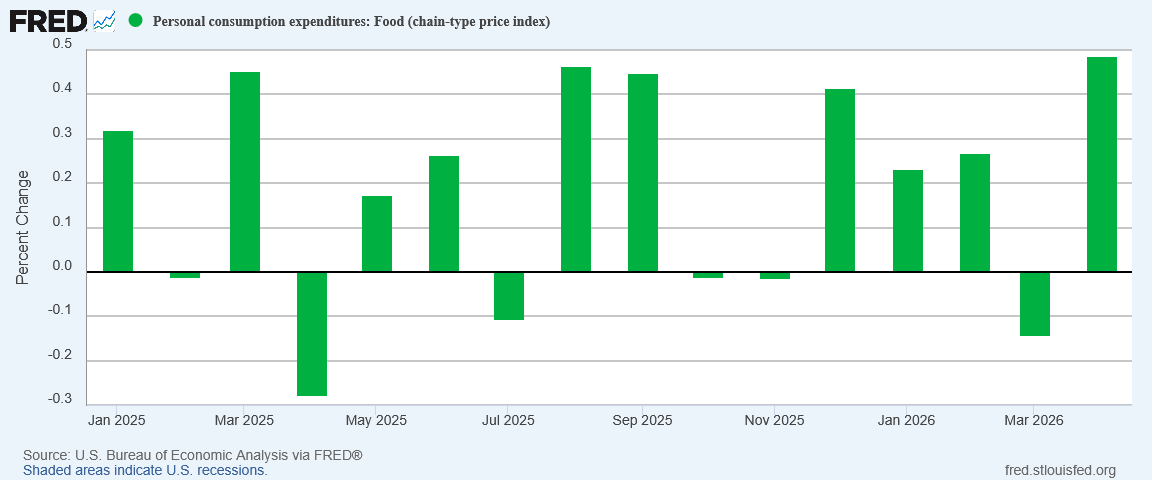

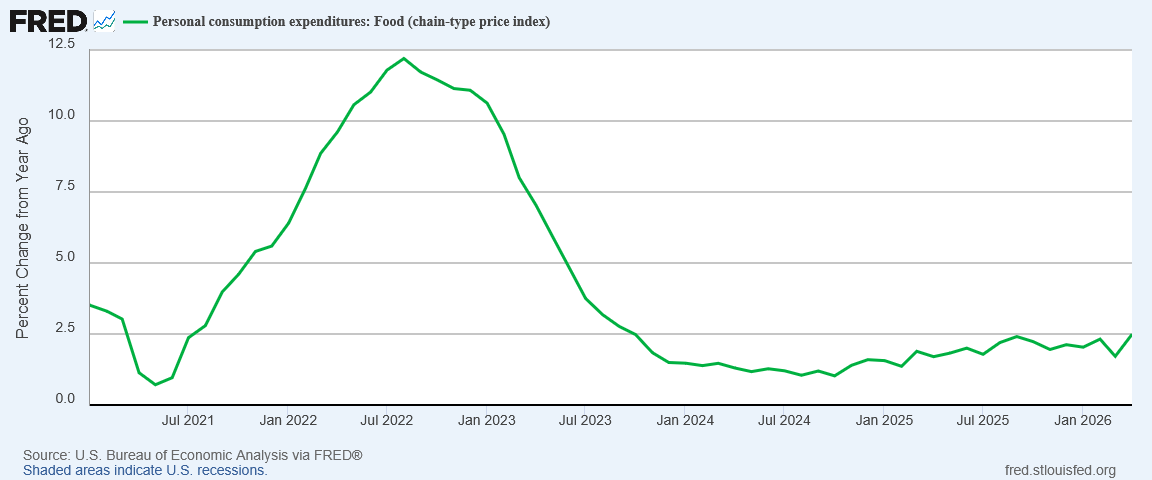

Food Price Surge

The one clear inflation pain point for April was the surge in food price inflation.

However, the month on month surge, while the highest since President Trump took office in January 2025, did not translate into a notable year on year increase.

Food prices rose significantly in April, but even so the longer trend is still one of stability. While current stability is no indicator of future pricing, it once again leaves us at the point of “not yet” when considering the worst case ramifications from the energy price shock which began in March.

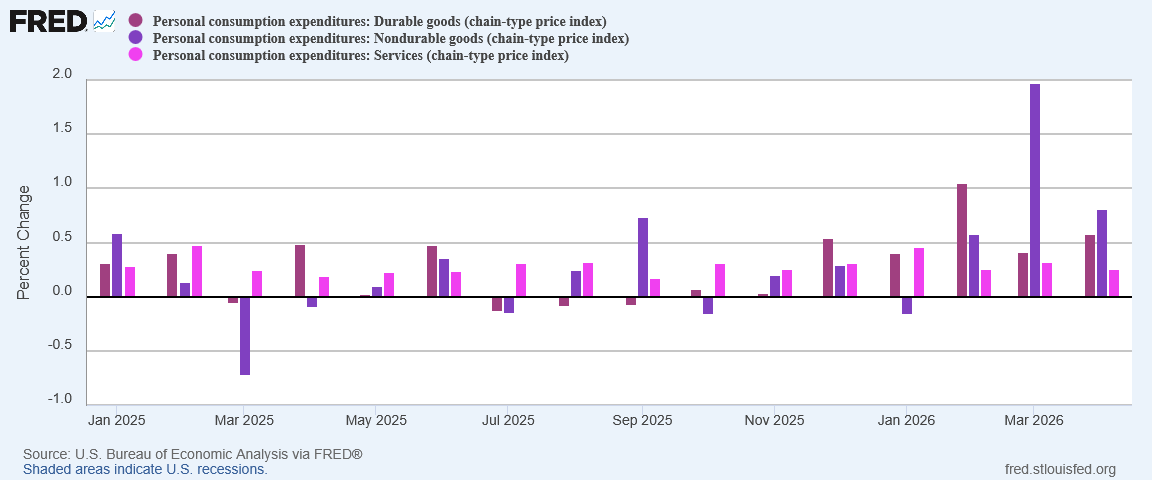

Goods And Services Eased

The clear sign that the energy price shock has yet to move beyond energy prices was the significant cooling of non-durable goods price inflation.

Even though durable goods prices ticked up in April, non-durable goods declined, and were joined by service prices.

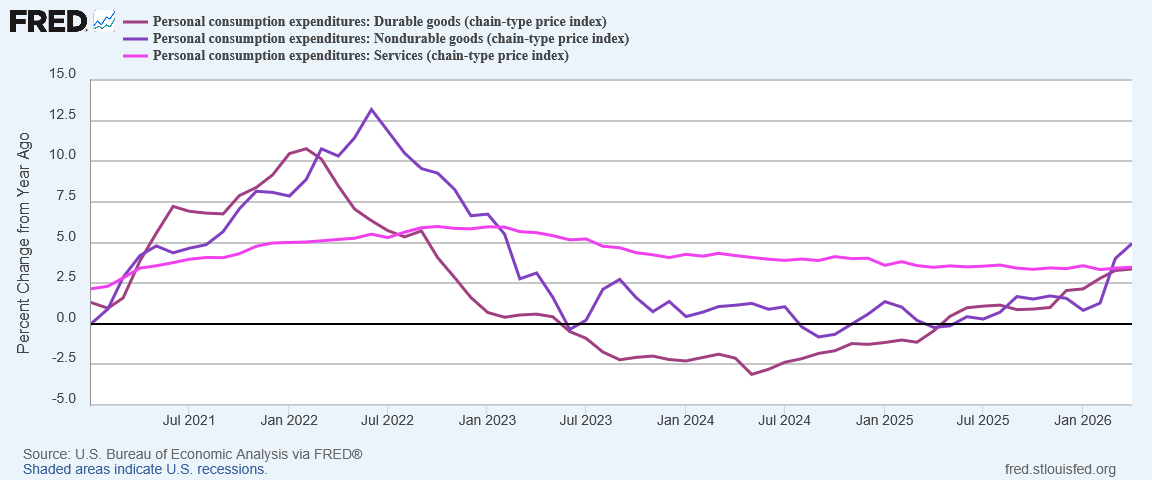

Year on year, non-durable goods increased again, after being the only core category to surge dramatically in March.

Durable goods, which had been rising since well before the war with Iran began, changed little year on year.

Most significantly, month on month inflation for energy goods and services greatly outpaced nondurable goods and services.

Within the US, the energy price shock has been contained to energy prices.

It Can’t Last

While energy price inflation is a significant discomfort to people, especially as it translates into retail gasoline prices, that the surge in energy prices has not translated into higher prices for other goods and services, broadly speaking, is itself noteworthy.

It is particularly noteworthy because, unless there is a peace deal struck between the US and Iran that reopens the Strait of Hormuz to shipping, that can’t last.

Globally, closing the Strait already means that stagflation is stalking the world’s economies.

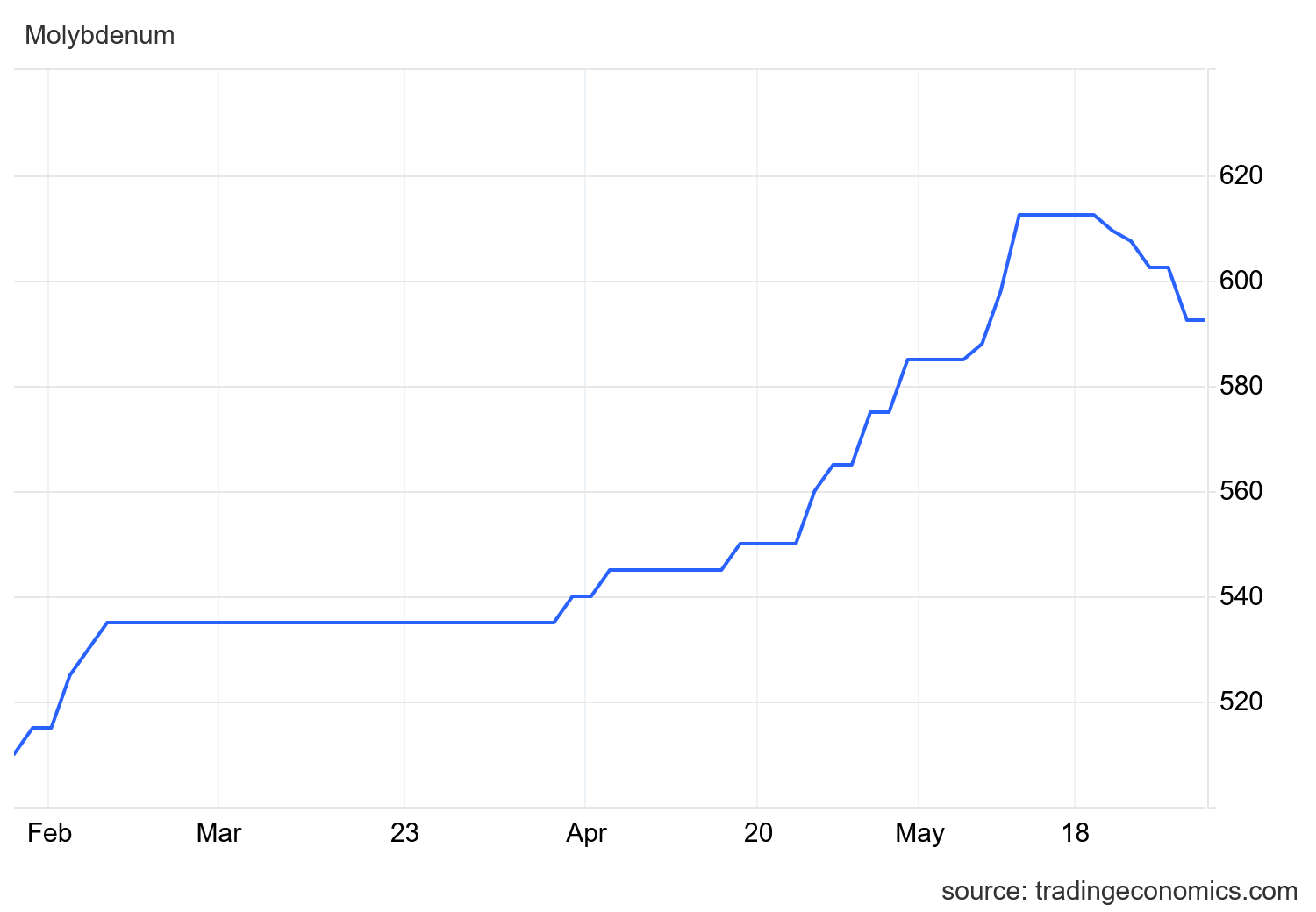

Not only are energy prices up, globally, but key industrial commodities are rising as well.

Copper reversed its price decline towards the end of March and is continuing to rise.

Tin showed a similar trend towards increase beginning in late March.

Molybdenum has shown far less volatility, but it also has move sharply higher.

We will have to wait until the May data for both the Consumer Price Index and the Producer Price Index come out to see how much these non-oil manufacturing inputs are contributing to consumer price inflation within the United States.

We do not need to wait to see that these are real cost pressures. Commodities are industrial inputs, as a rule, which is to say that an increase in the price of various commodities is an inescapable increase in the cost of producing a variety of goods and services.

While manufacturers may opt to absorb those cost increases before passing them on to consumers, that will only last so far. If the inflationary price trends among various commodities continues, those cost pressures will result in consumer price inflation for a variety of durable and non-durable goods.

The energy price shock is for now limited to energy prices. That will not last indefinitely. It can’t last indefinitely.

More Of The Same Inflation…For Now

With the war with Iran ramping up at the end of February, my assessment of the February PCE data was that is was the end of “more of the same”. For pre-war prices, that was absolutely true.

Ironically, the April PCE data has been largely a repeat of the March data. Once again, we have “more of the same” inflation, but with an energy price shock in the mix.

We have energy price inflation, and that is creating headline consumer price inflation within the PCE data just as it did within the CPI data. We also have food price inflation.

Beyond that, we are not yet seeing much in the way of new inflation pressures.

With rising commodities prices, it is only a matter of time before those trends translate into higher consumer prices. It may very well prove to be the case that May will be the month we see the energy price shock from Iran’s illegal closure of the Strait of Hormuz translate into a true stagflation phenomenon.

Globally, we are already seeing supply constraints for oil, for natural gas, and for a variety of industrial input commodities. Stagflation occurs when supply constraints push prices higher, particularly when it happens on top of a weak, underperforming economy. Iran’s lawlessness has provided the global economy with the supply constraints necessary to catalyze stagflation globally, and it is only a matter of time before those supply constraints begin to impact the US economy.

The April PCE data is hardly good news as far as inflation is concerned. 3.8% inflation is a sharp reversal from where inflation was just two months ago.

Yet the April PCE data does offer one significant bit of comfort: It is, in most respects, a milder repeat of the March data.

The April PCE data is more of the same war-inflected consumer price inflation data. We will not see “more of the same” indefinitely. We may see an end to “more of the same” in a few weeks with the May inflation data.

Consumer price inflation has indisputably risen, and risen by a lot. Energy prices have increased by as much as 50%, and fuel prices by even more than that.

Yet the stagflation shoe has not really dropped for the US economy—not yet. If the standoff in the Persian Gulf continues, or if hostilities are resumed, that shoe will drop, but for now we have the paradoxical “comfort” of “only” having to contend with energy price inflation.

The April PCE data is not at all good news. It is, however, a far cry from the worse news that we will soon be seeing if there is not an outbreak of peace between the US and Iran.

I really love how you stay factual, Peter. It’s not the standard spin-and-hype writing, and the more widely I read, the more I value your grounded insightfulness. Thank you!