The End Of The Islamic Republic: Stagflation Stalks Global Economy

Demand Destruction Is Next, But How Much?

Most oil traders are pushing optimism and hopium as trading strategies of late. How else to explain oil prices not continuing to move higher even as the United States and Iran circle each other, growling, hissing, and spitting at each other like feral cats?

Yet oil prices are not rising, as Wall Street seems largely convinced that the Strait of Hormuz will be reopened literally any day now. Iran and the US will come to terms, the Strait will reopen, and everything will revert back to the way it was before the start of Operation Epic Fury.

At least one investment bank, however, is ditching the hopium, presumably for a more sober and judicious assessment on the Middle East. In that assessment, the Strait of Hormuz stays closed for at least now, which will eventually push oil prices to new highs.

“We think the Strait of Hormuz remains largely closed for months yet, meaning shortages become more urgent and oil hits new highs this Summer,” according to a recent note from the investment bank’s energy and macro teams.

While the implications on oil prices of a prolonged closure of the Strait are both obvious and closely followed, what gets lost in the focus on energy products are the efforts Arab nations in the Persian Gulf have made to diversify their economies. Oil flows are disrupted, but much more flows through the Strait than just oil.

Even more economic output depends on access to oil from the Persian Gulf.

As the standoff between the United States and Iran continues, and with the US rejecting Tehran’s latest “draft Memorandum of Understanding,” a reality of rising commodities prices and constrained supplies is settling over the global economy.

Stagflation is stalking the global economy. Demand destruction must follow, but how much will be needed to restore balance?

The Strait Of Hormuz Is Closed For Business

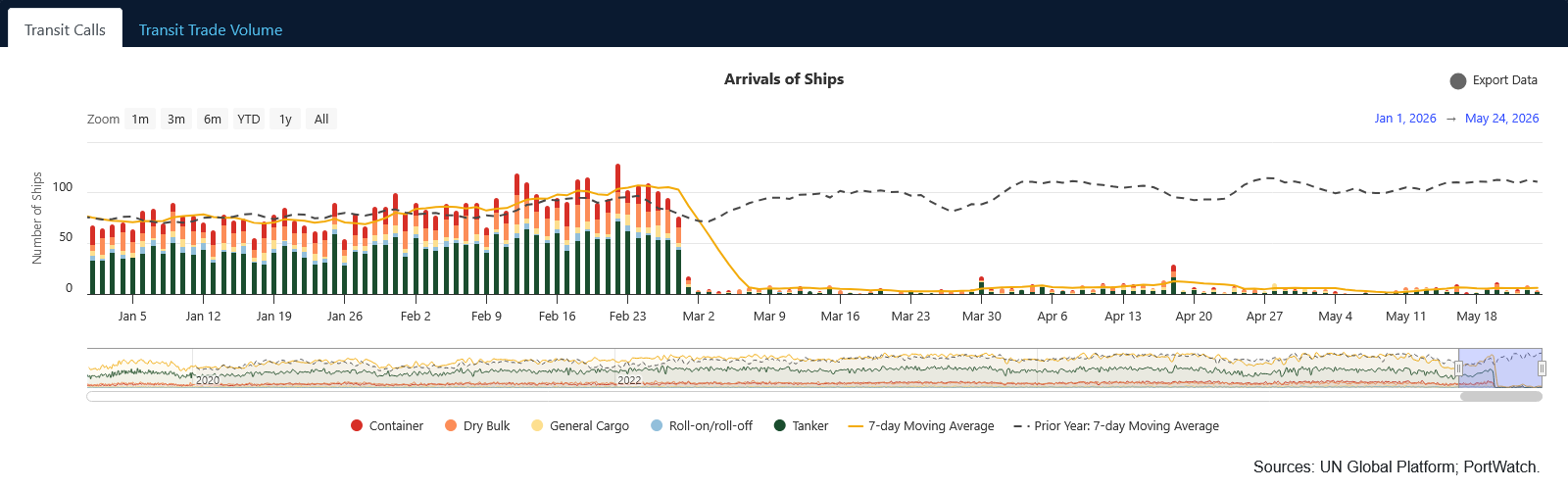

Make no mistake: no shipping has transited the Strait of Hormuz since right after the start of Operation Epic Fury. All publicly available shipping data points to the same conclusion: the war between the US and Iran has slammed the door shut on Persian Gulf shipping.

Data released between 11-13 May 2026 indicates that commercial traffic through the Strait of Hormuz remains far below pre-war levels, as measured by vessel tracking and trade data cited by the Center for Strategic and International Studies. Daily tanker and cargo ship transits remain far below those recorded prior to the United States/Israel offensive on Iran in November 2018. While some vessels may operate with automatic identification system signals switched off, publicly available traffic data show no broad recovery in flows.

The collapse of cargo traffic through the Strait was immediate and complete, as confirmed by IMF Portwatch shipping data.

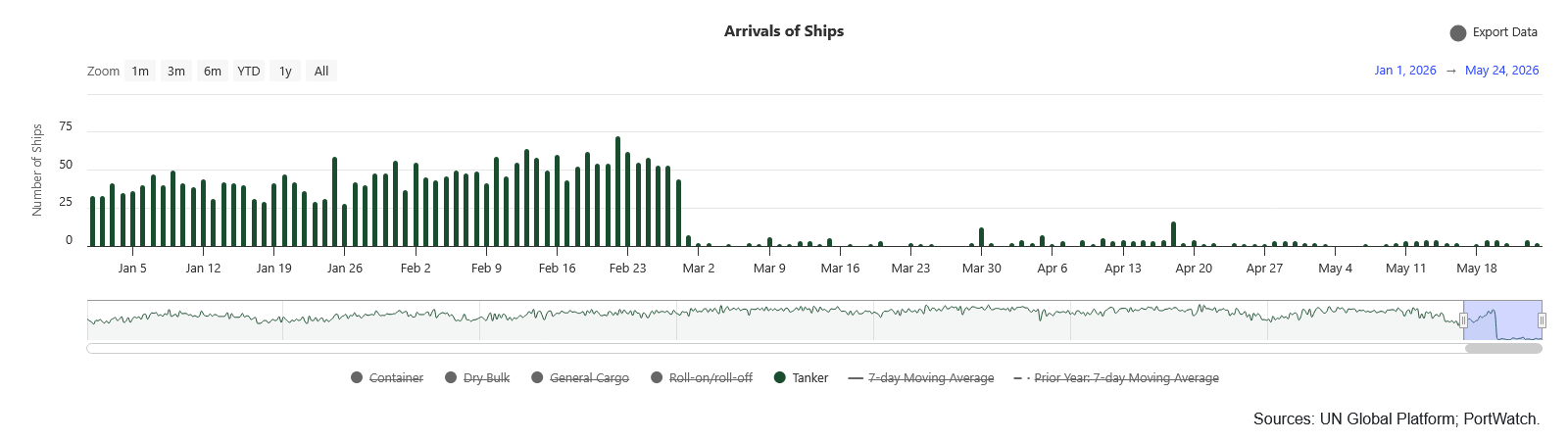

The near total collapse in tanker traffic also confirms that the US Navy blockade of Iranian shipping is also having an effect. With next to no tankers transiting the Strait, Iran’s closure of the Strait means Iran is also not shipping any oil.

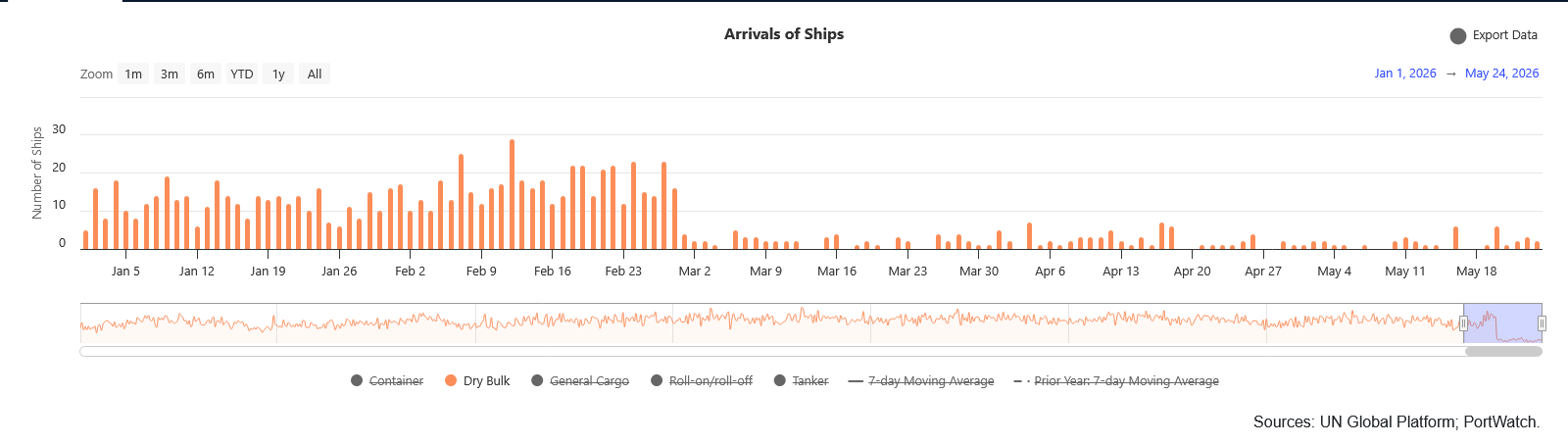

Yet dry bulk cargo vessels, of which quite a few had been moving through the Strait before the war, have also ceased to transit the international waterway.

The Strait of Hormuz is closed. It does not matter what sort of ship one considers; all classes of cargo vessel are denied transit passage through the Strait.

Oil Prices Are Stable…For Now

Despite the closure of the Strait and the denial of Persian Gulf oil flows to the global economy, energy prices have broadly stabilized and even been trending down recently, as markets respond ever hopefully to the latest news reports on the peace talks between Iran and the US.

While stabilizing prices are, on the face of it, a good thing, what is not good is that the stability (such as it is) comes when oil prices are more than 40% above pre-war levels.

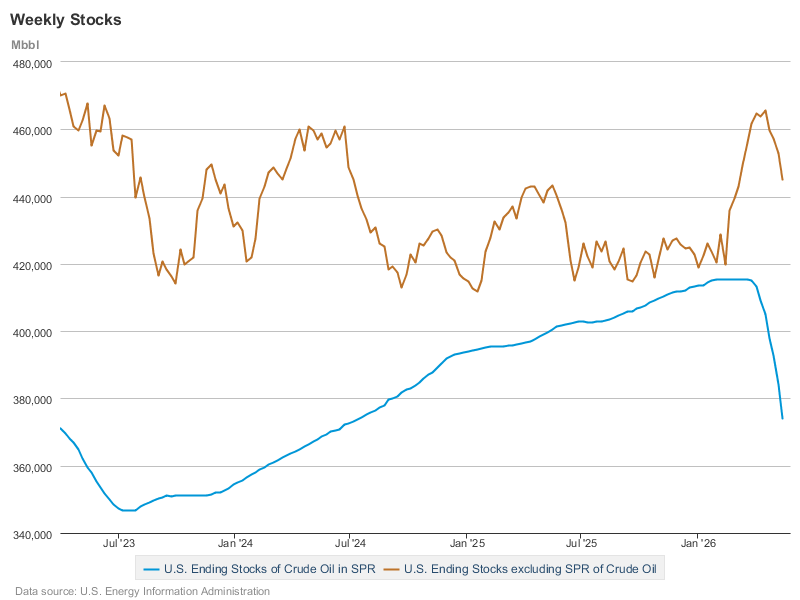

That stability, however, is somewhat illusory, as it comes as countries are releasing large amounts of their strategic oil reserves to buffer the oil supply shock that began when the Strait of Hormuz was closed.

The United States has released much of the oil recently added to the Strategic Petroleum Reserve over the past thirty-two months.

Notably, US commercial stocks, while having been drawn down, are still within the same broad range as they have been. While the releases from the SPR are significant, the SPR itself is far from the only oil inventory the United States can access on demand.

Separately, the IEA responded to the first announcements of the Strait’s closure by coordinating among its 32 member nations a release of some 400 million barrels of oil from reserves—one-third of physical reserves, and nearly one-fourth of total oil reserves.

IEA members hold emergency stockpiles of over 1.2 billion barrels, with a further 600 million barrels of industry stocks held under government obligation. The coordinated stock release is the sixth in the history of the IEA, which was created in 1974. Previous collective actions were taken in 1991, 2005, 2011, and twice in 2022.

There is a limit to how much buffering is possible with releases from strategic oil stockpiles, however. Oil reserves might be large by nearly every standard imaginable, but they are finite. The lower oil reserves get the less buffering is feasible, and the greater the inflationary pressure on oil prices.

Already, energy analysts are growing wary of how much longer strategic reserve releases can contain oil prices.

The message from this week’s SPR and commercial inventory data could not have been clearer. Combined crude inventories fell by 17.8 million barrels, the largest drawdown since records began in 1982. In effect, Washington is buying time. The administration appears to be using strategic reserves as a temporary liquidity bridge while diplomats attempt to engineer some form of stabilization with Tehran before the physical market begins forcing a much harsher adjustment through price.

The longer the Strait is closed, the closer oil markets get to the point where the buffering of strategic oil releases breaks down, at which point oil prices move sharply higher.

We have already had one oil price and supply shock. If this war continues long enough, we will have another one, and almost certainly it will be a greater one.

Aluminum, The “Other” Middle East Export

While oil somewhat understandably grabs the economic headlines regarding the war between the US and Iran, the disruption of another commodity is creating its own economic turmoil: aluminum.

As countries such as the United Arab Emirates and Qatar have sought to diversify their economies, one industry they have moved into in a big way has been aluminum smelting.

Three of the top 15 aluminum exporting countries in the world are now situated in the Persian Gulf.

Russia: US$9.6 billion (12.3% of total aluminum exports)

United Arab Emirates: $7.8 billion (9.9%)

Canada: $7.5 billion (9.5%)

Malaysia: $5 billion (6.3%)

India: $4.2 billion (5.3%)

Norway: $4.16 billion (5.3%)

Australia: $4.07 billion (5.2%)

Bahrain: $3.5 billion (4.5%)

Netherlands: $2.7 billion (3.5%)

Iceland: $2.2 billion (2.8%)

Qatar: $1.93 billion (2.5%)

Italy: $1.86 billion (2.4%)

South Africa: $1.78 billion (2.3%)

Indonesia: $1.6 billion (2%)

mainland China: $1.56 billion (2%)

Taken together, the Arab countries of the Persian Gulf account for roughly 9% of global aluminum supply, all of which is bottled up in the Persian Gulf, courtesy of the IRGC.

While oil prices have moved down in recent days, aluminum prices have risen steadily since the war began, even as oil prices have not.

The catalyst for the price increases is not hard to fathom: the outbreak of war almost immediately impacted aluminum production in the Middle East.

The closure of the strait has already forced some smelters to curtail operations. Qatar’s Qatalum said on March 12 it would reduce production by about 40%, while Aluminium Bahrain said it was shutting down about a fifth of its capacity on March 15. Industry executives have warned that if the strait remains closed, further production cuts will be unavoidable — potentially pushing prices above the 2022 record.

While China has sought to leverage the supply disruptions in aluminum with increased production, markets are now becoming fearful that even China may about to trim aluminum production, pushing prices even higher.

Chinese authorities are now moving to rein in that over-production as inventories swell. A smelter in Baise, Guangxi province, has already cut output of molten aluminum, Mysteel wrote, without providing estimates of volumes affected. The steel and oil refining industries will also be targeted, the Ministry of Industry and Information Technology said in a statement on May 13.

The behavior of aluminum prices tells us what will happen to oil prices should the buffer of strategic reserve releases become exhausted. There is no strategic reserve of aluminum, and so wartime disruption of Middle East production has resulted in a steady and ongoing rise in aluminum prices. When supply is constrained and not buffered, when scarcity is artificially introduced into the market, prices of anything will rise accordingly, without fail.

The behavior of aluminum prices today is what the behavior of oil prices will be tomorrow. If the buffering effect of strategic reserve releases ends, oil prices will rise sharply. Of that there can be no doubt.

Other Commodities Are Also Rising

Last month I explored how the war with Iran was putting stagflationary pressures on China.

Not the least of these pressures were because of sharp price increases in industrial materials such as sulfur, bitumen, styrene, and polyethyline.

Meanwhile, other commodities prices, such as copper, tin, and molybdenum, are also showing inflationary pressures since the war began.

In a quirky reminder that inflation and stagflation are also price distortions, a few commodities such as palladium and rhodium are showing price reductions since the war began.

Perhaps most ominously for global food security, grain prices such as for wheat and rice are also moving upward.

One important caveat regarding food prices: prices for wheat and rice started rising well before the start of Operation Epic Fury. Although the war with Iran has certainly not helped matters, food price inflation is one area that we cannot put all the blame on Iran’s illegal closure of the Strait of Hormuz.

With staples such as wheat and rice becoming more expensive over time, food price inflation is a foregone conclusion, with a corresponding rise in food insecurity not far behind.

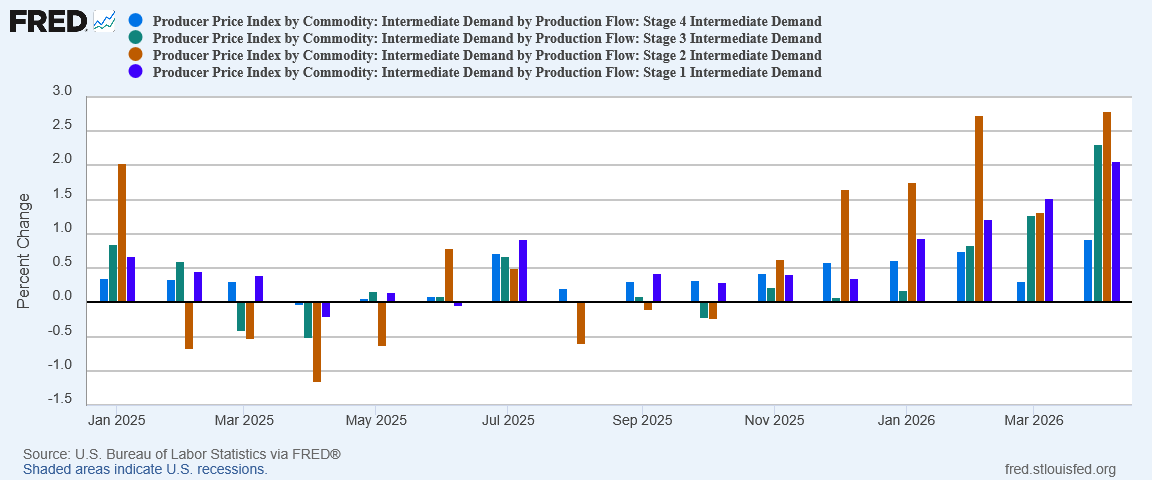

More broadly, inflation, instability, and volatility are creeping into a broad swath of commodities markets. Commodities themselves are invariably inputs into other production processes, making rising commodities prices rising costs—something we have seen reflected in rising US PPI for Intermediate Demand.

While US consumer price inflation has not yet shown significant increases outside of energy related products, one does not need a PhD in economics to grasp that continued price pressures in the production process will eventually translate into increased prices for consumer goods of all kinds. As production costs rise, as factory gate inflation continues to arise, particularly for intermediate demand (which shows the inflation’s impact on manufacturing supply chains), there is no place for those cost increases to go but into consumer prices. We may not be seeing broad consumer price inflation yet as a result of the war’s price and supply shocks, but it surely is only a matter of time before we will.

Multiple Shocks

The economic impact of the war with Iran is naturally most visible in its impact on oil prices. Oil is the most significant and most visible export from the Persian Gulf, as well as the one with the most volatile pricing.

Yet Iran’s illegal closure of the Strait of Hormuz was from the outset completely indiscriminate. Iran blocked all shipping, not just oil tankers. The disruption in oil flows was also the disruption in aluminum flows as well. If a good moved through the Strait of Hormuz, Iran disrupted that movement.

Energy prices also play into smelting and refining metals such as copper, tin, and molybdenum. The price shock in oil has only increased inflationary pressures on those commodities. As oil prices reach the end of near term stabilization when strategic reserve releases are trimmed back, the secondary price shock in oil will almost certainly push commodities with high energy footprints even higher.

From the one price and supply shock in oil comes multiple other price shocks in various industrial commodities. The price and supply shock in oil is also not helping ward off rising food prices. The disruption of other Persian Gulf exports such as aluminum merely adds to global economic stress.

We are already seeing the impact of these price shocks in producer prices, both here in the US and in China. The limits of petroleum reserves tells us that, unless there is a peace deal brokered soon to reopen the Strait of Hormuz, we will soon see more price shocks.

There is no escaping the reality that these price shocks are what triggers stagflation. Stagflation is what arises when there is a sudden drop in available supply, and the global economy is seeing reduction in supply across an increasing range of commodities and production inputs.

When supply drops in this fashion, the only way back to any sort of pricing equilibrium is for demand to drop in order to match supply. Once stagflation takes a big enough bite out of an economy, demand destruction is the next inevitable step. That is the other shoe that must eventually drop and land on the global economy.

Stagflation is already here. Barring a quick end to the war with Iran, demand destruction and recession will soon follow. Demand destruction must happen—people and businesses must eventually buy less and consume less. There are no economic alternatives. Either supply is restored or demand must be destroyed.

The only question as yet unanswered is how much demand destruction will we endure while the world’s economies rebalance themselves?

You really are superb at these kinds of analyses, Peter. You were born an economist!

Reading the details, I keep seeing every commodity scenario as being in flux, impossible to predict. For example, Canada probably has the capacity to increase refining of aluminum, but they are also being hit with higher energy costs. Is it therefore feasible to increase smelting, or do energy costs outweigh the potential financial gains? Would Alberta, as Canada’s main energy source, use its increase in leverage with Ottawa to bargain for better terms in representation, or would Alberta feel emboldened by its oil wealth to break free? It’s all in flux.

Globally, we could see some countries seize market-share opportunities (what will Milei in Argentina see as possible?), and we could see regimes topple because of consumer despair. It’s all in flux. On the present trajectories, more stagflation is likely, but it’s impossible to predict the rate or how widespread it might become.

One question in my mind, Peter, is regarding federal gas taxes.I saw a brief Substack note just a few days ago, saying Trump will issue an EO to eliminate federal gas taxes (for now). I’ve heard nothing more about it. It would lessen some domestic economic pain, but it seems to me that it would be politically too difficult for Trump to reinstate them, especially before the midterm elections. What do you think, Peter?

You’ve probably already heard about the new 60-day pause, but I’d love to hear your assessment of it. Personally, I can see why Trump felt he had to approve it, but I suspect it will be a mistake. The Islamic regime simply cannot be trusted. They will use these 60 days to strengthen their hand, and Trump will end up having to bomb them anyway - possibly after they’ve committed some atrocity against us.

https://www.theepochtimes.com/world/tentative-60-day-iran-ceasefire-deal-reached-pending-trumps-approval-sources-6039888?utm_source=ref_share&utm_campaign=copy