The End Of The Islamic Republic: What About China?

Is China Winning Or Losing In The Persian Gulf?

The fog of war has been the one constant in the United States’ war with Iran since the start of Operation Epic Fury on February 27. Even the efforts of Pakistan to broker a second round of peace talks in Islamabad produced more confusion than clarity, as Iran sent conflicting signals about whether they would or would not send a team of negotiators.

Through the fog, however, one point has always been absolutely clear: the closure of the Strait of Hormuz is a major disruptor in the world economy, and the effects are already being felt worldwide.

Retail fuel prices were the most obvious and most immediate effect, with nearly every country experiencing a price surge on par with the 2022 hyperinflation cycle. In the US gasoline and diesel prices surged by more than $1 and $1.50 per gallon, respectively from the start of the war. Germany saw retail diesel prices climb by €0.59 per liter (€2.23 per gallon) by the beginning of April, and gasoline price rise by €0.36 per liter (€1.36 per gallon). Even early in March, before the full impact of the closure of the Strait of Hormuz had been felt in energy markets, China raised its gas and diesel prices by 695 yuan and 670 yuan per metric ton.

If a product is related in any way to petroleum and fossil fuels, its price has risen significantly, with percentage price increases in double digits across the board.

China, the world's leading importer and a growing chemicals exporter, is quite possibly the country feeling the greatest impacts from these price surges. Every price hike is a cost increase to China’s manufacturing intensive, export oriented economy.

This war is between the US and Iran, yet the biggest winner or the biggest loser could very well be China, nominally a neutral nation and not a party to the conflict.

Iranian Hypocrisy Over The Strait Of Hormuz

That China raised fuel prices almost immediately after the start of the war gets right to the heart of the perverse irony over Iran’s illegal and hypocritical stance regarding the Strait of Hormuz. By closing the Strait, Iran sent a massive inflation pulse into the economy of its main customer.

China accounts for at least 80% and perhaps more than 90% of Iran’s pre-war oil exports. All those exports were at least disrupted when Iran closed the Strait.

Yet at least publicly, Iran seems unaware of its role in this. Instead, the current leadership atop the regime of Supreme Leader Mojtaba Khamenei, including Parliament Speaker Mohammed Bagher Ghalibaf, fatuously point a finger of blame at the United States, such as Ghalibaf did with his usual bellicosity yesterday.

Even Iran’s Foreign Minister, Abbas Araghchi, seemed oblivious to the double standard Iran advances with its accusations against the United States.

Iran accusing the US of “warmongering” in the Strait is, of course, absurd. The US is not the nation that told ships they could enter the Strait, only to fire on them. That was something Iran did on April 18.

For all of Iran’s pretentious accusations against the United States, there is no dispute which nation closed the Strait of Hormuz. Iran did.

There is also no dispute that closing the Strait of Hormuz is a violation of international law. The United Nations Convention on the Law of the Sea (UNCLOS) explicitly declares in Article 38 a right of transit passage through all such waterways.

In straits referred to in article 37, all ships and aircraft enjoy the right of transit passage, which shall not be impeded; except that, if the strait is formed by an island of a State bordering the strait and its mainland, transit passage shall not apply if there exists seaward of the island a route through the high seas or through an exclusive economic zone of similar convenience with respect to navigational and hydrographical characteristics.

Article 44 further restrains states bordering these international water ways from restricting or regulating traffic through them.

States bordering straits shall not hamper transit passage and shall give appropriate publicity to any danger to navigation or overflight within or over the strait of which they have knowledge. There shall be no suspension of transit passage

Nor is this simply my interpretation. Singapore’s Foreign Minister Vivian Balakrishnan argued substantially the same points during an appearance at CNBC’s CONVERGE LIVE event on April 22.

“With respect to both America and China, we have told both of them we operate on the basis of UNCLOS,” he said, referring to the United Nations Convention on the Law of the Sea.

Article 44 of UNCLOS states that “States bordering straits shall not hamper transit passage ... There shall be no suspension of transit passage.”

“The right of transit passage is guaranteed for everyone. We will not participate in any attempts to close or interdict or to impose tolls in our neighborhood,” Balakrishnan said.

Prevailing legal opinion also does not give Iran any grace on the matter. UNCLOS is to ensure freedom of navigation through the world’s strategic waterways, and Iran is determined to prevent freedom of navigation in the Strait of Hormuz. These positions are not legally compatible.

We should pause to note that neither the US nor Iran have ratified UNCLOS, although Iran has signed the Convention, and the US separately agrees with many of the principles contained therein. While neither the US nor Iran is technically bound by UNCLOS as they would be had they fully ratified the treaty, there is no serious argument to rebut the understanding that both countries are in broad agreement with UNCLOS’ position on freedom of navigation, which Iran’s Strait closure unquestionably violates.

If Iran actually espoused the freedom of navigation principles of UNCLOS, the Strait of Hormuz would never have closed and this situation would never have come to pass.

China In The Middle

Iran’s hypocrisy and blatant treachery in the Strait of Hormuz is arguably a complicating factor for a country such as China.

On paper China is an ally of Iran. It presumably helped rebuild and rearm Iran’s defenses after the Twelve Day War last summer.

At the same time, China also is nurturing good diplomatic relations with the other nations in the Persian Gulf, and just recently, in a phone call with Saudi Crown Prince Mohammed bin Salman, openly endorsed freedom of navigation in the Strait.

Xi said that the normal passage through the Strait of Hormuz serves the common interests of regional countries and the international community, adding that China supports regional countries in building a common home marked by good-neighborliness, development, security and cooperation, mastering their own future and destiny, and promoting long-term peace and stability in the region.

As I noted a few days ago, such stances could indicate China was losing patience with Iran’s intransigence over the Strait.

It is worth noting that “normal passage” arguably refers to the pre-war status quo in the Strait, which did not include Iran assessing tolls on ships passing through it. Such tolls are, of course, an explicit violation of the UN Convention on the Law of the Sea, which codefied pre-existing international understandings on the principles of freedom of navigation.

It is also worth noting that China buys oil from more than just Iran, and its shipments of Saudi crude are down 10% from pre-war levels.

Shipping data from multiple sources indicates China’s normal imports of Persian Gulf oil have been disrupted to a significant degree, even if they haven’t been completely cut off.

Interestingly enough, China may also be turning the war and the closure of the Strait of Hormuz into a short-term revenue generator, exploiting arbitrage opportunities that have emerged thanks to the surge in benchmark oil prices and selling out of its strategic petroleum reserve while the prices are high.

“What has been happening in the last two or three weeks is actually they have been aggressively selling crude oil,” Mercuria CEO Marco Dunand said at the FT Commodities Global Summit in Lausanne on Tuesday. “They’ve taken out a lot of demand from various countries and offered aggressively in tenders.”

Dunand said there are a variety of possible explanations for the selling. They include the release of oil inventories within China, continued sales of Iranian oil in the weeks after the war started, and possible optimism that the Strait of Hormuz would reopen quicker than it has so far.

China is a net importer of oil, which means it cannot continue to sell its oil inventories indefinitely. Marco Dunand estimates China can continue to sell crude out of its reserves for another three weeks, after which it needs to recalibrate its strategy should the blockade of the Strait still be in effect at that time.

Ironically, that three week endpoint is also about the time frame when Iran’s inability to export oil starts to have outsized effects. Because Iran is unable to export the same volume of oil it has in the past, its available storage capacity is starting to fill up. Analysts at JPMorgan project that Iran will exhaust their storage capacity sometime in the next three weeks.

Onshore storage sits around 86 million barrels, currently just over half full at roughly 47 mb. That leaves about 40 mb of working capacity, which, in market terms, translates into roughly 22 days of export cover if flows are fully choked off. Layer in the four Iran-linked VLCCs still sitting inside the Strait of Hormuz, and you add another 8 mb of potential floating relief, stretching that window toward 26 days.

But the system does not wait for tanks to hit the brim before reacting. Production does not fall off a cliff, it bends under pressure. In practice, upstream adjustments begin earlier and build progressively. The rule of thumb embedded in the JPM framework is that Iran would need to start trimming output after roughly 16 days of a full export blackout, with curtailments accelerating from there until they converge toward full export volume shut ins, around 1.9 mbd, closer to day 30.

Day 1 of that “full export blackout” arguably is when President Trump announced the US blockade of Iranian ports (but not the Strait itself) on April 12. As of this writing, 10 of JPMorgan’s 16 days have already elapsed, leaving only 19 days until Iran hits the full export volume shut in point at day 30.

When wells are shut in, pressure build-up and other environmental forces can damage them, either permanently reducing their daily output or requiring significant overhaul upon reopening to restore the wells to previous production levels.

If the JPM estimate is correct, if Iran has to start shutting in wells starting sometime next week, and if Marco Dunand’s assessment of China opportunistically selling down its oil inventories is correct, in about three weeks a second and longer lasting oil supply shock hits all major economies, and especially China. Removing China’s oil sales and Iran’s oil production for the foreseeable future would be a double-digit percentage loss of current oil production globally.

China is exploiting its geopolitical position between the US and Iran for maximum short-term revenue, but that maneuver could hamper its long-term position should the Strait of Hormuz continue to be blockaded at least by the United States. By the time China needs its strategic inventory, it will have already depleted at least a portion of that inventory.

China’s Petrochemical Shock

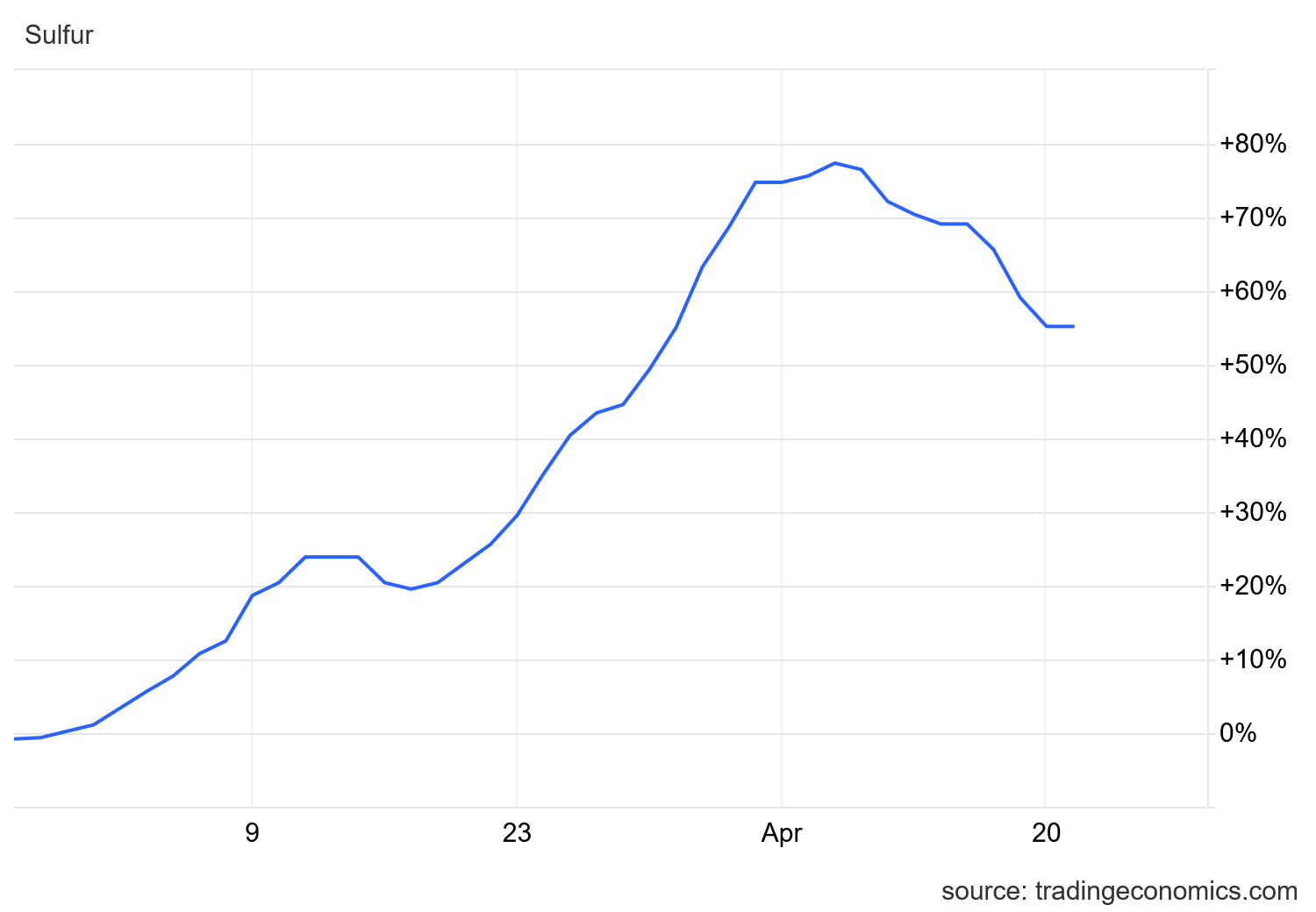

As I discussed last week, China is experiencing at least one major supply shock in the form of sulfur and sulfuric acid.

What tripped media concerns over sulfuric acid was China’s recent announcement, first reported on April 10, that it is suspending exports of sulfuric acid, owing to shortages within its own industries.

Particularly relevant is China’s apparent justification for the export ban: it needs to conserve the chemical for its own supply chains and manufacturing industries.

While sulfur prices have come down some for China, relative to pre-war pricing China is still paying 55% more than before.

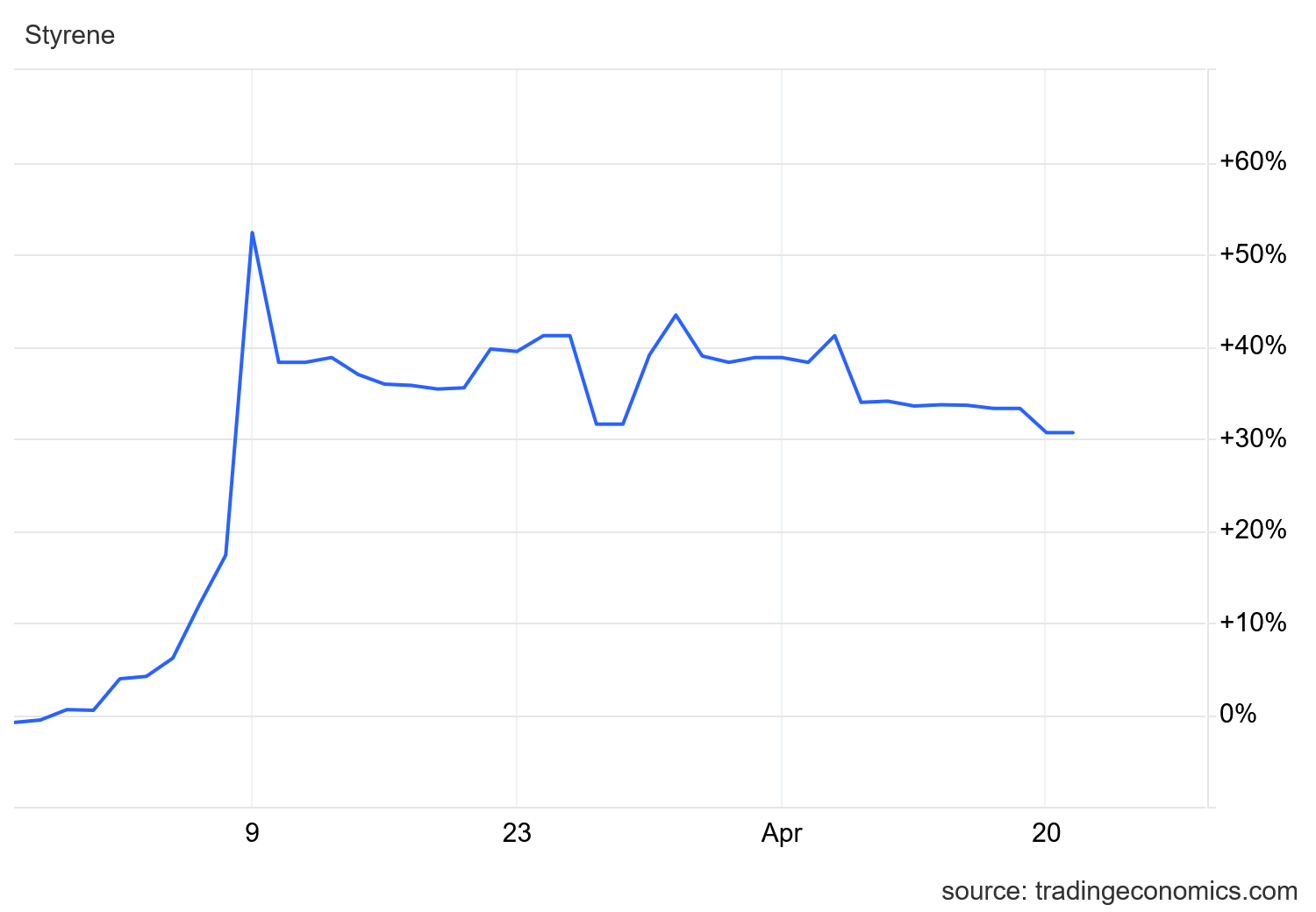

Yet it is not merely for sulfur and sulfuric acid that China has seen tremendous price surges.

Polyethylene prices have surged nearly 20% since the war began, and at one point flirted with a 40% increase.

Styrene has risen some 30% since the war began, and initially had surged by just over 50%.

Bitumen is currently sitting at just under a 25% increase, after touching 40% towards the end of March.

China is a major consumer of all three industrial chemicals, and many more besides. These chemicals are all refined products from various crude oils. China either imports the crude and refines these compounds itself, or it imports these compounds from a number of countries, including those in the Persian Gulf.

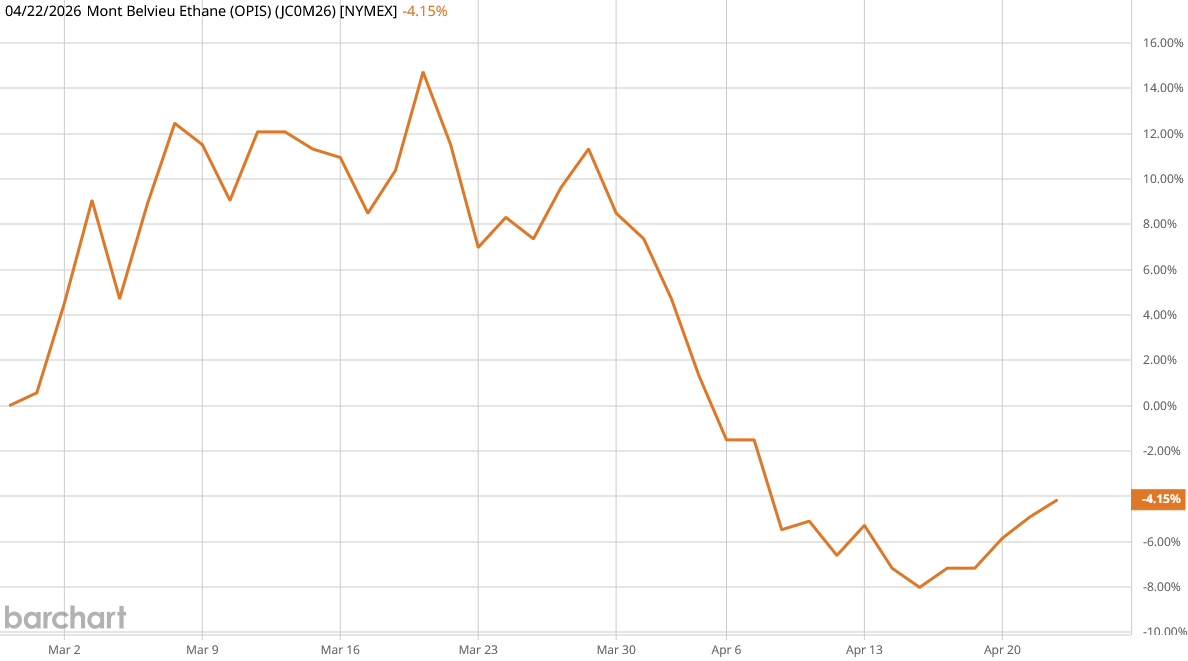

China’s reliance on not just imports of crude oil but also imports of petroleum refined products is also being thrust into the spotlight by the awkward reality that China is importing record volumes of ethane from the United States as a result of the war and the Strait of Hormuz being closed.

Shipments of US ethane are expected to rise to an all-time high of 800,000 tons in April, according to Chinese consultant JLC, which would be around 60% higher than the monthly average. Some companies can switch to using ethane, helping them offset disruptions to the supply of naphtha and liquefied petroleum gas from the Middle East after the effective closure of the Strait of Hormuz.

Ethane is one of the minor fractions of natural gas and a by-product of liquified natural gas (LNG) production. When Iran targeted Qatar’s LNG production facilities at Ras Laffan early on in the war, forcing Qatar to shutter most of the facility, nearly 20% of world LNG supply was removed. One of the other products Ras Laffan produced was ethane.

While prices of US ethane have overall fallen since the war began, in recent days the prices have begun climbing again.

China’s need is clearly the United States’ gain when it comes to ethane.

Equally clear is that China is experiencing multiple price and supply shocks, all of which directly impact the vital export sector of China’s economy. The goods China produces to sell overseas are getting considerably more costly to manufacture, at least in the short run.

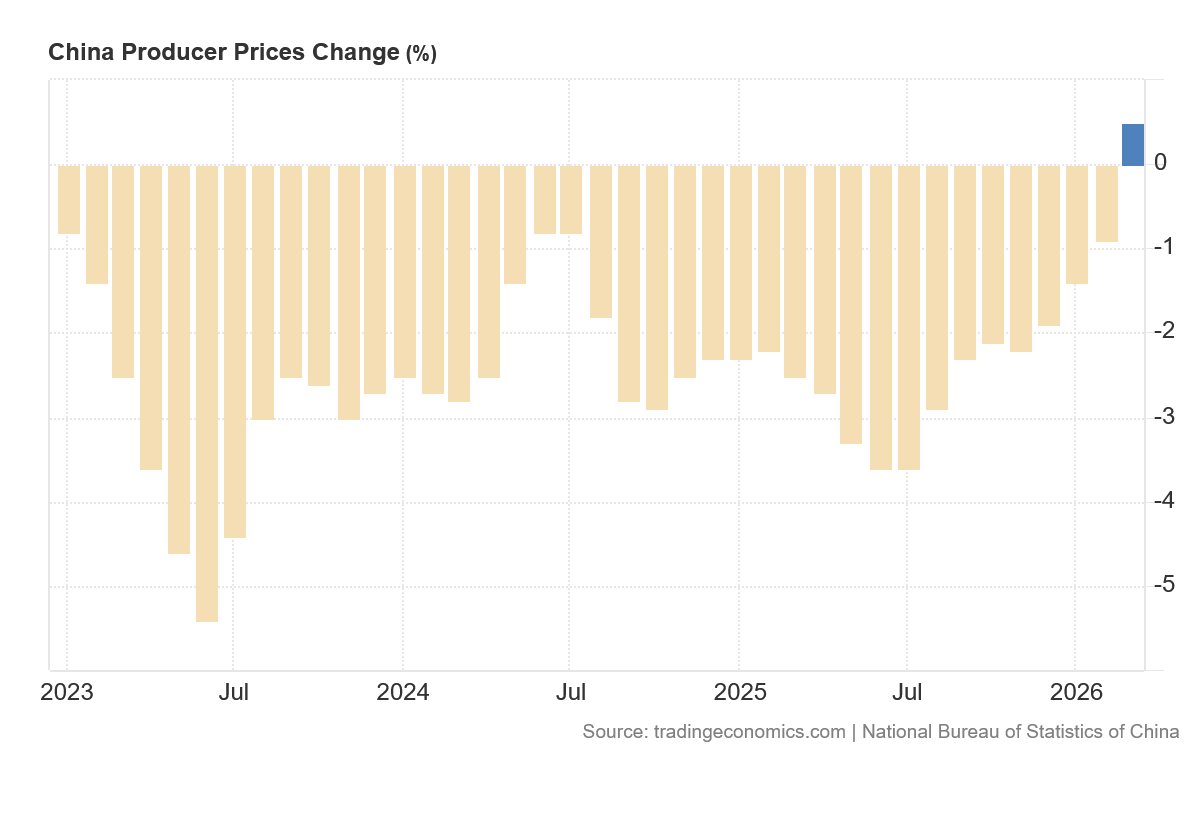

On the surface, these price shocks arguably look like good news. The scarcity and resultant price surges has caused China’s Producer Price Index to show positive growth for the first time literally in years.

While the emergence of even some factory gate inflation in China is arguably a relief, given the deflation that has hung like an albatross around China’s economic neck in recent years, a sudden energy inflation shock, if it endures over time, can produce what some “experts” want to call “bad inflation” but is really stagflation.

Just as it is in the United States, stagflation for China is when a price shock collides with a moribund economy.

Is China about to have its deflation crisis compounded with a stagflationary shock? Much depends on how long the Strait of Hormuz remains closed and energy prices elevate.

No matter how long the Strait remains closed, China remains very much in the middle between Iran and the United States in this war, and the two countries’ dueling blockades suggests being in the middle means China gets run over from both directions.

Crisis Or Opportunity?

In some narratives, the war with Iran represents an opportunity for China. Not only is its economy getting a long-desired boost on inflation, but rumors of Persian Gulf countries attempting to sidestep Iranian interdiction of their cargoes by trading in yuan rather than dollars persist. Broadening the utility of the yuan in global commerce is seen by many as an essential step in “de-dollarization”.

In other narratives, China is getting hammered by price and supply shocks, stressing an already distressed economy. That stress is seen as a likely catalyst for what appears to be a rise in social unrest, although the extent and impact of that unrest is difficult to ascertain.

What is certain is that China is significantly impacted by the war with Iran, and not in demonstrably good ways. As a rule, price and supply shocks are not considered to have a positive impact on a nation’s economy. China is experiencing multiple price and supply shocks as a result of the war, and will continue to experience those multiple price and energy shocks.

Much of the data surrounding those shocks supports the stress narrative: Youth unemployment rose in March, along with regular unemployment, suggesting the producer price rise has not yet been accompanied by any significant job creation. Labor costs continued to rise in March, extending a trend reversal from a years-long decline that produced a record low in June of 2025.

Weak or no job growth is one sort of sub-par economic indication which sets up the context for a stagflation scenario to unfold. Just as in the US, we cannot yet conclusively describe current economic conditions in China as “stagflation”, but there is little doubt that China, already mired in deflation, is at elevated risk for stagflation.

Whether that is what evolves in China’s economy depends entirely on the duration of elevated energy prices, which in turn hinges on when and how the Strait of Hormuz is finally reopened.

That is one of the outcomes we know will happen eventually. The Strait of Hormuz will reopen for the simple reason that, with 20% of the world’s oil supply flowing through it, the world economy cannot abide it being closed indefinitely.

Similarly, we know there will be talks. No matter which scenario one espouses for the war with Iran, every scenario ends with the principals sitting down at a negotiating table.

What we still do not know is what the agenda for those inevitable talks will be. Both sides reject the talking points of the other, making formal negotiations difficult.

We also do not know when the Strait itself will be reopened. If there are talks soon, there is at least a chance the Strait will be reopened soon. Reopening the Strait is a prerequisite for getting energy prices back towards pre-war levels; the longer the Strait is closed the more energy prices are likely to trend up and not down.

The longer the Strait is closed the more China is compelled to draw down its strategic petroleum reserves.

The longer the Strait is closed the greater the likelihood Iran’s oil production will suffer a major quasi-permanent reduction. Given that China has been buying the bulk of Iran’s oil production, the loss of Iranian production means China has to replace relatively low-cost Iranian oil with more expensive market-priced crudes.

That last point would mean that China is facing increased oil prices no matter how the war with Iran turns out. An energy price shock could become permanent higher energy prices for China. That would not be a positive outcome for China’s economy.

The fog of war makes any sort of prediction about the outcome of this war problematic. We simply do not know how this war ends. While the United States arguably has already won the war from a military perspective, having smashed most of Iran’s military assets, geopolitical victory has not yet been achieved.

This war could end with China among the countries with enhanced geopolitical power and influence.

This war could also end with China as well as Iran losing geopolitical power and influence to the United States. If President Trump succeeds in de-nuclearizing Iran and forcing the Khamenei regime to abandon pursuit of nuclear weapons, that would be an indisputable geopolitical victory for the US, and a corresponding setback for China, which likes to position itself as America’s principal geopolitical adversary.

This war could end with China’s economy enduring more significant shocks and body blows than the US economy. China may already be enduring more economic shocks and body blows than the US—the data certainly compels us to entertain that possibility. Those shocks and body blows may even put China into a final economic death spiral which will stress Chinese society past the breaking point—China’s pre-existing economic weaknesses make that a very real possibility.

Will China number among the winners or the losers when this war with Iran finally does end? It is too soon to answer that question with any finality, but the data we have to date does not favor China emerging from this war better off than before.

The question remains; will China pressure Vahidi and the IRGC to open the Straits?

The IRGC will be inclined to keep the Stratis of Hormuz closed as it remains the only large scale weapon they have. With military ordinance production facilities wrecked or decentralized to prevent efficient production, if China cuts off supplies of essential materiel, Iran will only have "one last stand" before total ruin. China may provide that pressure to ensure thier own survival.

The days of Iran in its current governance configuration are likley numbered.

I’m so glad you are following the China situation in detail, Peter. Long term, I think it could be the most consequential result from this war.

One thing in particular has me pondering: China selling off its petroleum reserves. Short-term gain, but long-term foolishness. They’re just going to have to buy replenishment at higher cost! So, either they are exceptionally confident that Iran will prevail and make it up to China, or, they are in such dire financial straits internally that they are grasping at whatever short-term salvation they can. Or, China has some gambit planned that we can’t see. Peter, would you hazard a speculation? (Come on, we won’t hold you to it!)