The End Of The Islamic Republic: Acid Tripped?

Sulfuric Acid Is Also Bottled Up Behind The Strait Of Hormuz. That's Costly...But For Whom?

The fog of war has so far made a mockery of a number of prognostications about Operation Epic Fury and the war with Iran. We have not started World War III. The world economy has not collapsed. Iran is not “winning”, and the US has not (yet) “won”.

Just about every “expert” analysis has been wrong.

Consequently, when even alternative media outlets such as ZeroHedge puts out yet another “doomsday” headline about the Persian Gulf, we are well advised to regard what follows with more than the usual skepticism.

The chemical in question is sulfuric acid, a major byproduct of oil refining, particularly refining of heavy “sour” crudes with high sulfur content.

Goldman analysts Kyle Shaffer and Amanda Ross provided clients with a broad overview of industrials and natural resources amid energy disruptions in the Gulf area. In the note, they stated that the well-known Gulf energy shock is set to disrupt LNG production in Qatar for years to come. However, they also highlighted another emerging supply crunch that has received far less attention: sulfuric acid.

“Some long-lasting consequences have also started to emerge, including a 3-5 years production loss for LNG facility in Qatar, a 6-12 month re-starting time for some aluminum facilities in the Gulf, and shortage of sulfuric acid which can potentially impact future production for copper and lithium” Shaffer and Ross said.

Even a cursory glance at commodities prices shows that anything coming out of the Persian Gulf has seen major price appreciation since the start of Operation Epic Fury. To the extent that industrial chemicals are shipped from Persian Gulf refineries, it is a given that, at present, those chemicals are not being shipped from Persian Gulf refineries.

How significant is the loss of Persian Gulf sulfuric acid? Depending on the analyst, it is anywhere from very significant to presenting a national security threat.

Any supply dislocation of a key industrial chemical is obviously a costly event…but for whom? When not every cost is shared equally around the world, who pays the most and who pays the least can be more significant than the cost itself.

Update

With Iran just this morning declaring the Strait of Hormuz fully open, an additional question which will have to play out is how quickly will the supply dislocations ease and pre-war normal shipping flows be restored to the Persian Gulf?

Beware The Narrative

The constant caveat in reading all reporting about the war in Iran, and really any war, is to beware the narrative. Media outlets all veer towards propaganda and deliberate bias—a sad reality of modern journalism that is also why All Facts Matter exists.

As one reader has remarked:

It’s pretty much impossible to follow the various narratives. I read so many Substacks that are referential to some media environment. Most people I know don’t watch MSM (cable news) and some read Liberal elite papers, some read Conservative elite papers. But even within the ideologies there is more divergence. And you can’t even get into it when the Substackers start treating their Substack algorithmic silo as understood by the audience. I read stuff referencing people I’ve never heard of like its assumed that everyone has read that piece.

Getting harder every day to organize around narrative construction like that.

With bias a near constant fixture in what passes today for journalism, we owe it to ourselves to both be aware of any outlet’s narrative lens and to remain focused on the facts without regard to the narrative lens.

For every media outlet, it is imperative to look past the headlines. Even narrowly focused outlets are prone to provocative and even misleading headlines. An article in “Mexico Business” which covers much of the same territory on sulfuric acid as ZeroHedge, appeared the other day under this headline:

Reading into the article itself, we find the lede well and truly buried almost at the end:

While Mexico is not among the most affected countries, tighter global supply and rising prices could increase input costs for domestic industries, particularly mining and fertilizers, reinforcing the country’s sensitivity to external supply shocks in critical industrial chemicals.

China’s sulfur export ban does raise economic risks for Mexico, but only a little.

These sort of media manipulations are why I often advise readers to “trust nothing. Verify everything.”

That being said, what is the story on sulfuric acid? What is the impact of the war with Iran on sulfur and where is it being felt?

Persian Gulf Blockade Is Hitting China Hard

What tripped media concerns over sulfuric acid was China’s recent announcement, first reported on April 10, that it is suspending exports of sulfuric acid, owing to shortages within its own industries.

Particularly relevant is China’s apparent justification for the export ban: it needs to conserve the chemical for its own supply chains and manufacturing industries.

China’s move to conserve sulfuric acid supplies during the peak crop-planting season will put further pressure on the market. That squeeze will hit the copper-mining industries in key producers such as Chile, the Democratic Republic of Congo and Zambia.

Acuity first reported the Chinese ban on Thursday, saying the restriction could last throughout 2026. China’s Ministry of Commerce didn’t immediately respond to a request for comment.

The need to conserve contradicts other reporting we have seen about China, some of which has assessed China as having the resource depth to fend off oil supply disruptions for months.

Yet, its supply buffer of an estimated 1.2-1.3 billion barrels of crude in strategic and commercial stockpiles could last up to four months, Rush Doshi, director of the China Strategy Initiative at the Council on Foreign Relations, told CNBC on Monday, when oil prices briefly hit $118 per barrel.

“China has taken the last 20 years to reduce some of its dependence on maritime oil flows,” Doshi said.

If China has ample reserves of crude, why is it feeling the need to restrict exports of a byproduct of heavy crude refining?

Corporate media does not say.

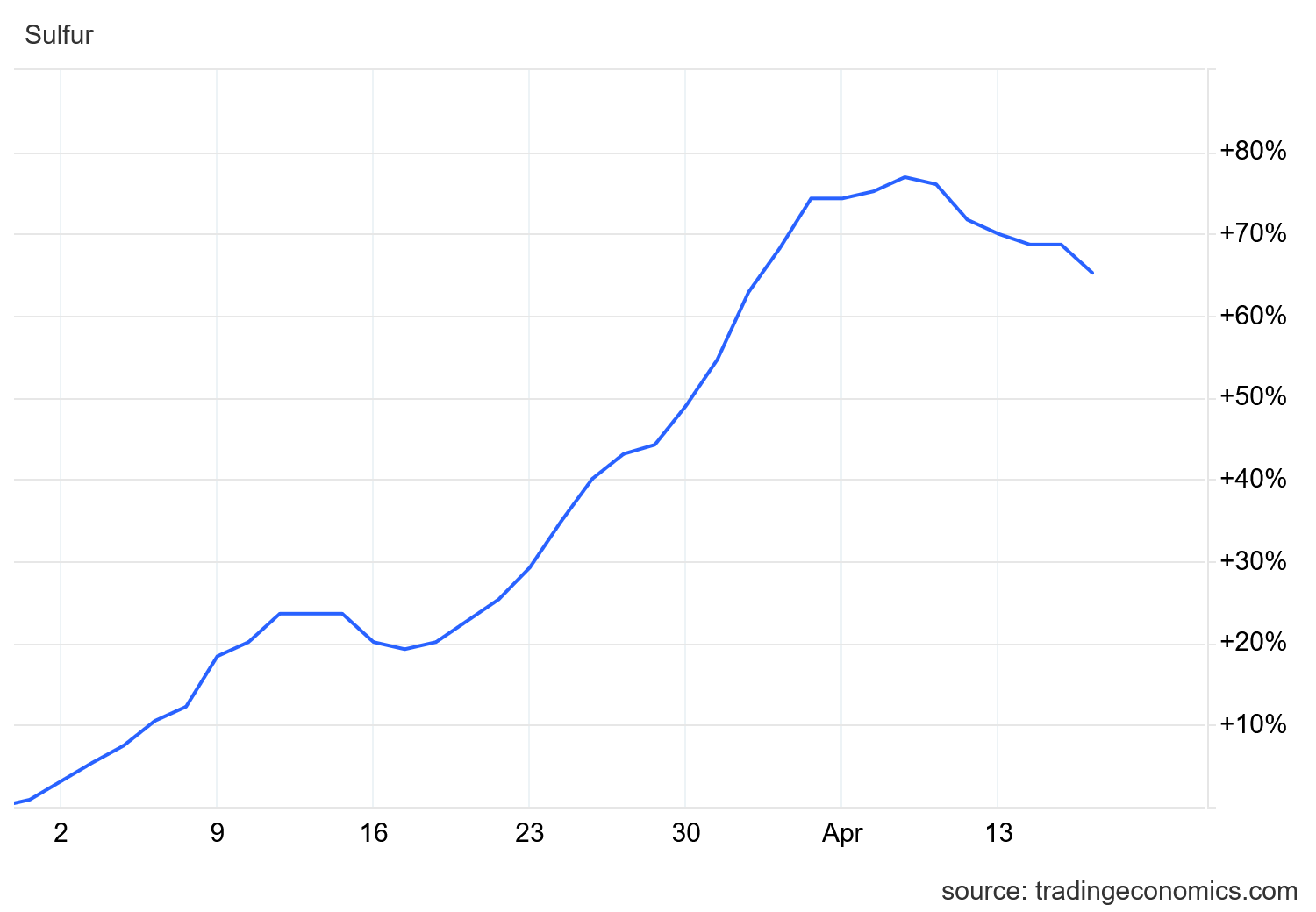

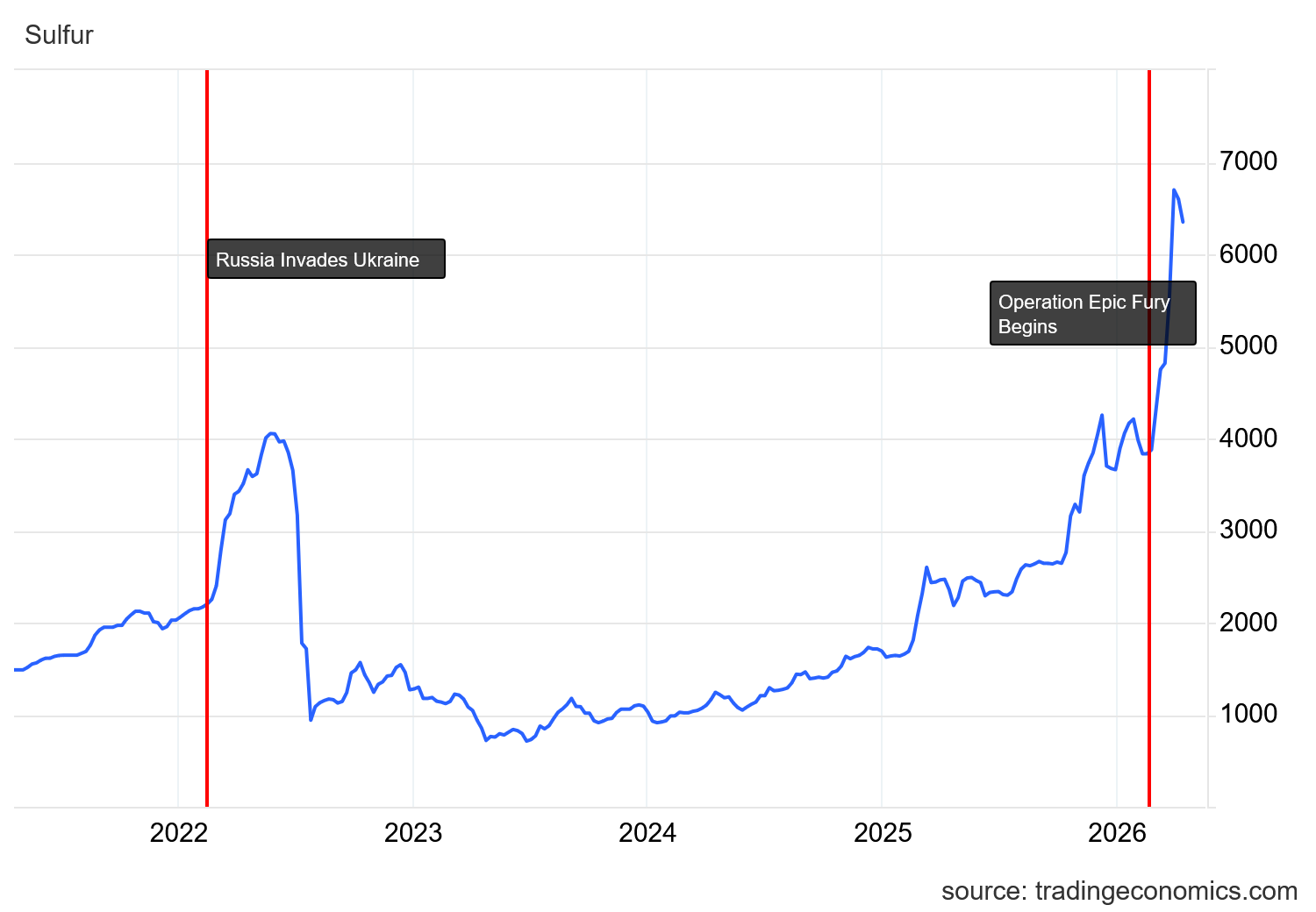

Yet the data shows that China is paying dearly for sulfur right now, as the war with Iran has pushed what China pays for sulfur up more than 65% just since the start of the war.

The impact to China of the current surge already exceeds the price spike when Russia invaded Ukraine in 2022.

Why is China suspending sulfur exports? With their cost for sulfur running nearly double from just before the start of the war with Iran, China is hoarding the chemical. China does not want to see the price its manufacturers pay for sulfur going any higher.

China may have four months’ supply of crude in reserve. That does not mean it has four months of sulfur as well. Based on current pricing as well as China’s export ban, we must conclude that China does not have much of a sulfur reserve.

Perversely, the ban may not solve China’s problems, and may even make them worse. While sulfur is particularly useful for smelting industrial metals such as copper, exporting sulfur has been a means for Chinese smelters to defray other costs and keep their operations profitable. The export ban may actually hamper China’s copper production.

For China’s copper smelters, the policy shift could accelerate production cuts. Smelters had relied on strong sulfuric acid prices over the past year to offset a sharp decline in treatment charges caused by a shortage of copper concentrate. However, increased domestic availability of acid following the export halt may cap or reverse price gains, weakening that support.

“Acid prices may slow down their rising pace or even flip into a fall, but neither is good for us,” said an official with a Chinese smelter.

Spot treatment charges for imported copper concentrate in China fell to a historic low of minus US$77/t on April 10, compared with minus US$76.7 a week earlier and minus US$28.6 a year ago, according to Argus data. The negative margins reflect intense competition for limited concentrate supply, leaving smelters increasingly dependent on byproduct revenues

With or without a sulfur export ban, closing the Strait of Hormuz is producing significant and broad price shocks throughout China’s industrial sectors.

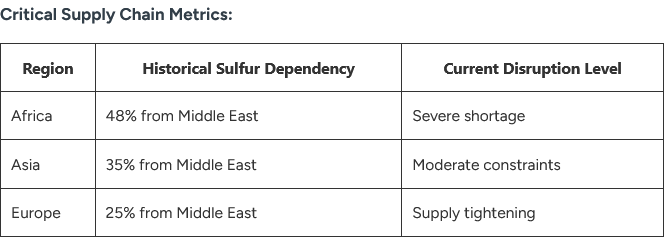

Not Just China

Digging even further into the industrial chemical market, it is readily apparent that several parts of the world rely on Persian Gulf refinery output for large portions of their sulfur supply.

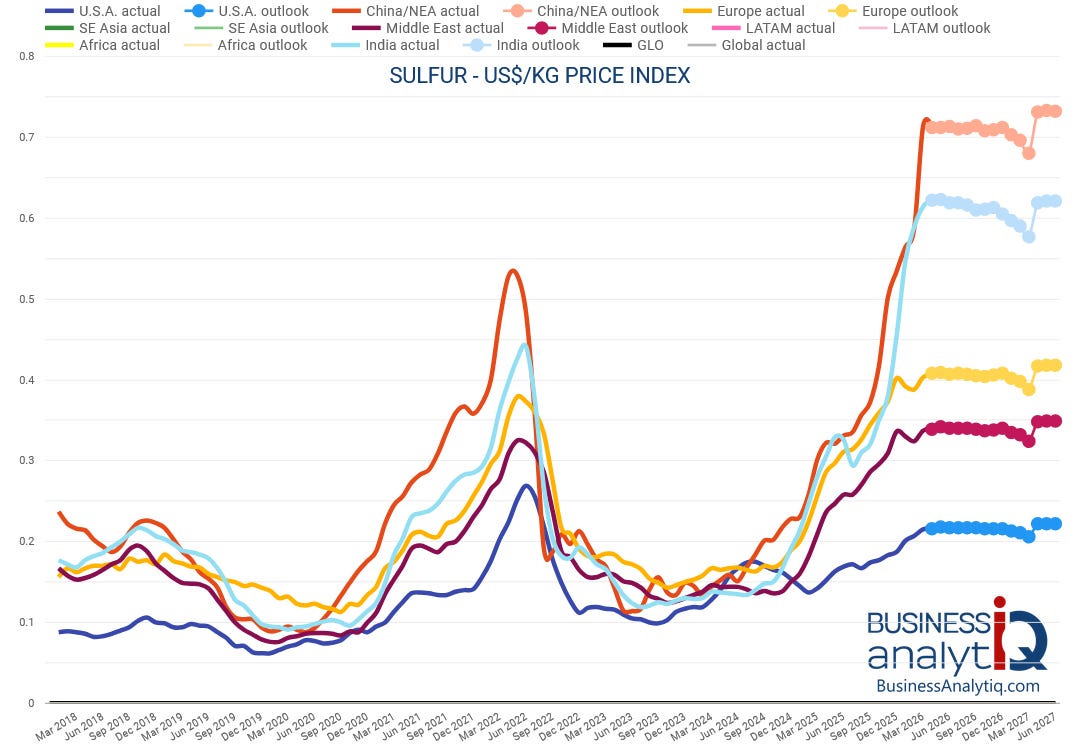

According to BusinessAnalytiq, however, the price impacts of losing Persian Gulf sulfur production vary widely.

China and Asia are feeling the worst price shocks, with India not far behind.

The US, on the other hand, is feeling much less impact, and is unlikely to feel much more of a pinch for the foreseeable future.

Contrast that with Chile, which buys over a million tons of sulfuric acid from China every year, the price has risen 44% in just the past month. The chemical plays a vital role in copper production, and Chile is the world’s number 1 producer of copper.

Disruption of sulfur production in the Persian Gulf or from Persian Gulf oil stocks will likely impact a variety of industries worldwide. Sulfur, and particularly sulfuric acid, has a number of industrial applications.

Primary Industrial Applications:

Fertiliser Production: 65% of total consumption for phosphate rock dissolution

Metal Processing: 20% for copper leaching operations and other metallurgical processes

Chemical Manufacturing: 10% for intermediate compound synthesis

Specialised Applications: 5% including battery production and petroleum refining

As Africa sources much of its sulfur consumption from the Middle East, the surge in sulfur prices is hitting countries with large resource extraction economies—Zambia and the Democratic Republic Of Congo in particular—extremely hard.

The longer the Strait of Hormuz is closed, and the longer Persian Gulf oil production is offline, the more challenging the sulfur supply situation gets for these countries.

Not The US

The disparity in sulfur prices shown above brings us back again to the caveat about narratives. Recognizing the bias within media narratives is crucial to making sense of media reporting on any issue.

While ZeroHedge is focusing on overall global industrial impacts, America’s military thinkers at West Point see potential military and national security concerns arising from the supply dislocation.

While the United States produces significant sulfur domestically, the near-total disruption of shipping through the Strait of Hormuz, which accounts for approximately 50 percent of global seaborne sulfur trade flows, has compounded an already tight market. US sulfur prices have increased 165 percent year-over-year to over $650 per metric ton; and now the price has surged by 25 percent just since the Iran war began. This makes domestic procurement fiercely competitive, while also threatening the import of specific ultra-high-purity grades required for advanced manufacturing. It is squeezing one of the most consequential inputs to modern industrial power.

The West Point narrative bias is clear, and it emphasizes immediate logistical and pre-logistical impacts without regional differentiation. While logistics is hugely important to successful warfighting, what matters most is having better logistics than potential adversaries.

As with all commodities, all markets have some exposure when there is a supply rupture. That is certainly the case with sulfur. Just this month US sulfur prices have surged 34%.

Yet a price surge is not the same as a supply dislocation. One point the West Point narrative brushes past is that the US is itself a major producer of sulfur—it is the number 2 sulfur producer in the world, after China.

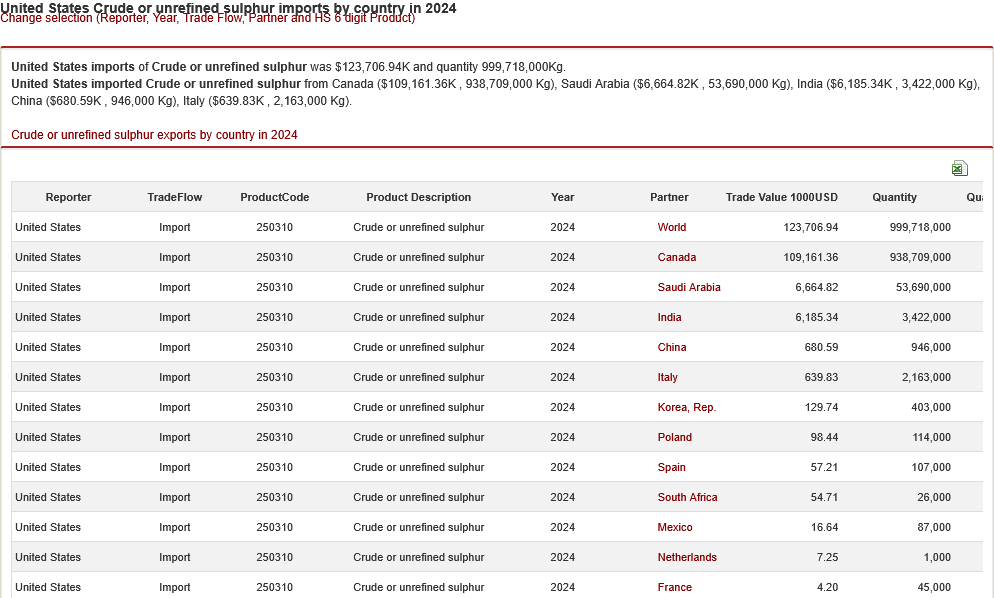

Even more significantly, virtually all the sulfur the US does import comes from right next door, in Canada.

As the Strait of Hormuz does not lie between the US and Canada, it is safe to say that the war with Iran is not disrupting physical supply chains for sulfur.

We should also note the quantities of sulfur the US imports: 999,718,000 kilograms is just under 1.1 million tons. The US produces domestically ~8-8.6 million tons of sulfur, which means the US imports between 12% and 13% of its annual sulfur demand.

The price of sulfur in the US is up because the price of sulfur is up worldwide, but the US still has physical access to nearly all the sulfur it uses. The same is not true for Africa, nor is it true for Asia (including China).

Hence the extreme price differentials between sulfur prices in the US and sulfur prices in China. China is grappling not just with a price shock but a supply shock. The US is experiencing only the price shock.

The difference becomes clear when we consider last month’s Producer Price Index data. Virtually all the inflation surge the United States experienced within producer prices in March was due to energy-related products, and fuels especially.

Outside of energy-related products, there was not a lot of inflation in March, and even some disinflation.

Thus far at least, the inflation impact of the war with Iran is still narrowly confined for the US. That could change, and if the war lasts long enough it almost certainly will change, but as of this writing it has not yet changed.

That lack of broad inflation so far in the US economy highlights the particular advantage the US has with respect to Iran and the Middle East: the US is considerably less reliant on the Middle East than is Europe or Asia. Even a cursory glance at price surges for oil and gas both here and in Europe illustrates that, for natural gas especially, the price differentials are quite significant.

Dutch TTF natural gas is still up nearly 40%, and that’s after talks and rumors of talks have calmed markets down. US natural gas has actually declined in price.

Even West Texas Intermediate crude is up less than its European counterpart, Brent Crude.

Diesel prices show the same disparate impact from the war with Iran:

Energy inflation is bad in the US, but it’s worse in Europe.

The same is proving true for industrial chemicals such as sulfur/sulfuric acid. There is a cost burden from the war that is being felt by the US, but it is being felt far more in China, in India, and in Europe.

A World Problem

The economic reality of the war’s impact is still very much what I pointed out a few days ago:

Whether Starmer or any other world leader agrees with Donald Trump on the war itself, Iran’s closure of the Strait of Hormuz is far more a UK issue, a France issue, an India issue, than it is a US issue. Even if one concedes that Operation Epic Fury is not “Europe’s war”, the closure of the Strait is indisputably Europe’s problem.

The economic fallout from the Strait’s closure was never going to be limited to just oil or diesel, even if those are the commodities that get noticed first. Yet, as we are seeing with sulfur and sulfuric acid, the dislocations brought on by the closure of the Strait of Hormuz are felt to a far greater degree nearly everywhere but the United States. In nearly every regard, the US is experiencing far smaller economic impacts than the rest of the world.

Does this make ZeroHedge’s take on sulfur production inaccurate? Arguably, it does.

Yes, global sulfur production is disrupted. Yes, sulfur prices are up significantly even in the US. These aspects of the war and its consequences are undeniable.

Yet what ZeroHedge overlooks, what the military thinkers at West Point gloss over, is that the cost from that rupture is falling on different parts of the world to different degrees. What ZeroHedge overlooks, and what the military thinkers at West Point gloss over, is that the US has the curious good fortune to be bearing the smallest portion of the overall costs from Operation Epic Fury, the war with Iran, and the current blockade of the Strait of Hormuz.

In a race to the bottom of global sulfur supply ruptures, the winning position is to come in last. At present that position belongs to the United States.

Closing the Strait of Hormuz is imposing a number of supply shocks and dislocations on the global economy. There is a cost to each of those supply shocks and dislocations.

So far, the burden of those costs is falling on just about everyone’s shoulder’s except the United States’.

Interesting lessons in the Law of Unintended Consequences, and the impossibility of predicting war outcomes. Trump’s team has maybe thought through most of the likely outcomes of their actions, and the IRGC has repeatedly shown that they haven’t.

Take lithium, for example. If less lithium is mined, and at a higher cost, that could be the final nail in the coffin of the electric vehicle craze. And if Chile cannot mine enough copper to fund their government, will there be regime change there? My bet is that Trump has thought things out to their logical consequences, more so than his adversaries.

I am reassured that we will come out of this war in better shape than most others. Thank you, Peter, for writing about angles that few other sources are covering.

New media: Never let the facts get in the way of a story that can be used to bludgeon Trump. No news is to be good news, full stop.