Has Stagflation Come To China?

Iran's War Strategy Is Pushing China Into Economic Crisis

On paper, China is presenting “green shoots” of a nascent economic recovery, with real GDP growth after a year of decline, and real factory gate inflation after over three years of factory gate deflation.

Amid global turbulence, China’s GDP expanded by five percent according to the official statistics in the first three months of 2026, up from 4.5 percent in Q4 last year. It was stronger than the market consensus of 4.8 percent and at the top end of the leadership’s target of 4.5-5 percent annual growth this year. Strong investment in infrastructure and manufacturing, led by state-owned enterprises, was crucial in returning fixed-asset investment (FAI) growth to positive territory. Yet the overall picture of the economy has not changed: growth continues to rely on strong manufacturing and exports, while consumption remains weak. The government’s cautious approach to policy support may be tested in the coming months as global uncertainties increase.

That is the narrative on paper.

More importantly, that is the narrative before Operation Epic Fury and the US war with Iran roiled global energy markets.

A return to economic growth and expansion is certainly a welcome change for China, which has been mired in deflation for years at this point—provided that it really is a return to economic growth.

As is so often the case, when media narratives collide with economic realities, the narratives do not do well.

The narrative is that China, in the first quarter of 2026, exceeded expectations and turned in strong economic growth.

The economic reality is that China remains mired in deflation. China may be on the precipice of a stagflation crisis, courtesy of Iran’s closure of the Strait of Hormuz as part of their war strategy.

Iran Upset Everyone’s Apple Cart

There can be no surprise that the data shows Iran’s decisions in its defense against Operation Epic Fury have roiled economies around the globe and are even now sending a significant energy price shock through those economies. China is far from immune to that price shock, and is even grappling with secondary price and supply shocks in a variety of petroleum-derived industrial chemicals, creating broad inflationary pressures across the whole of the economy.

Nor does recent price data on those same essential materials suggest the situation is getting any better.

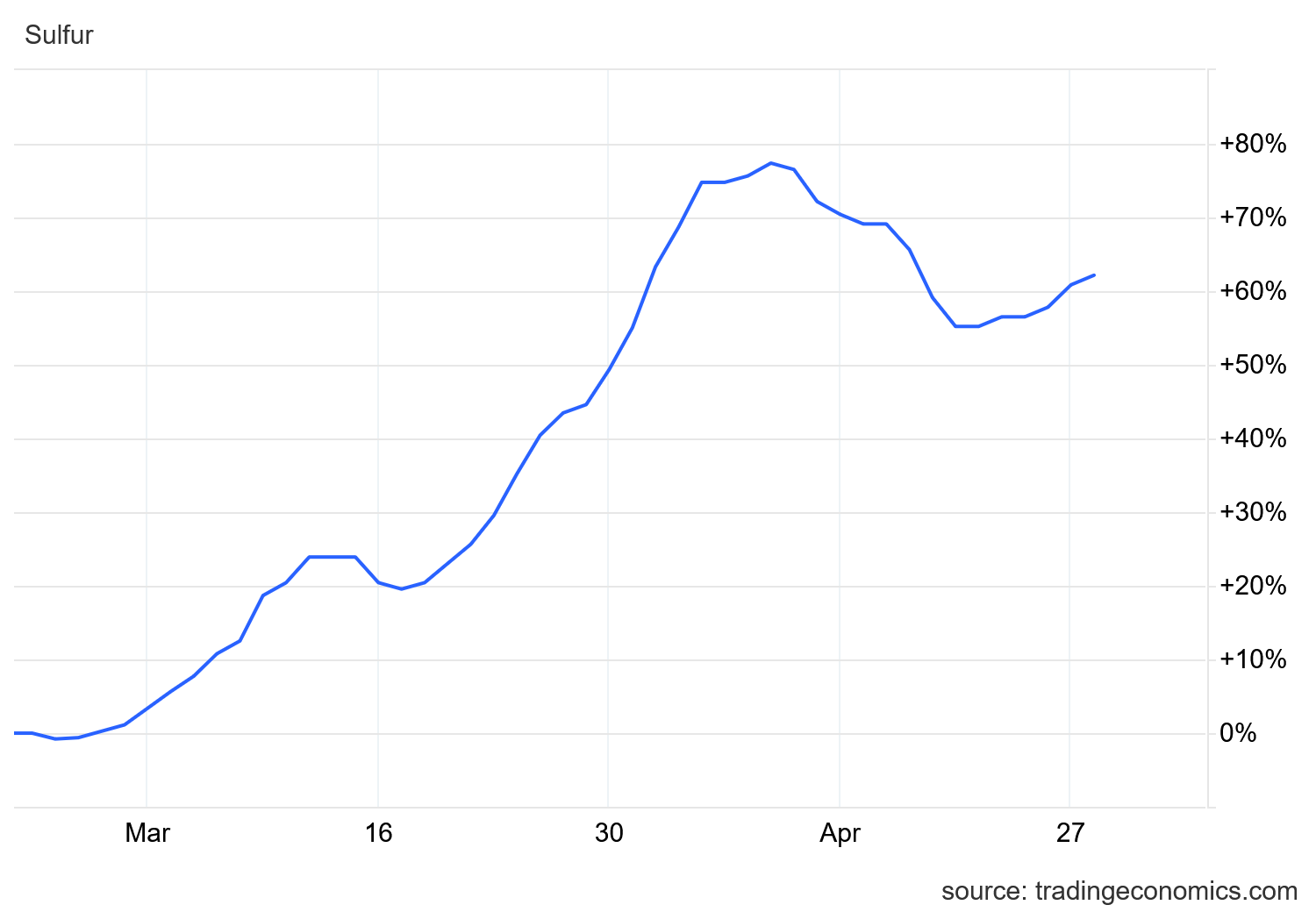

Sulfur prices in China have been trending up over the past week, with prices now more than 60% above pre-war levels.

Polyethylene has also reversed and started trending up over the past week, and is now 25% above pre-war prices.

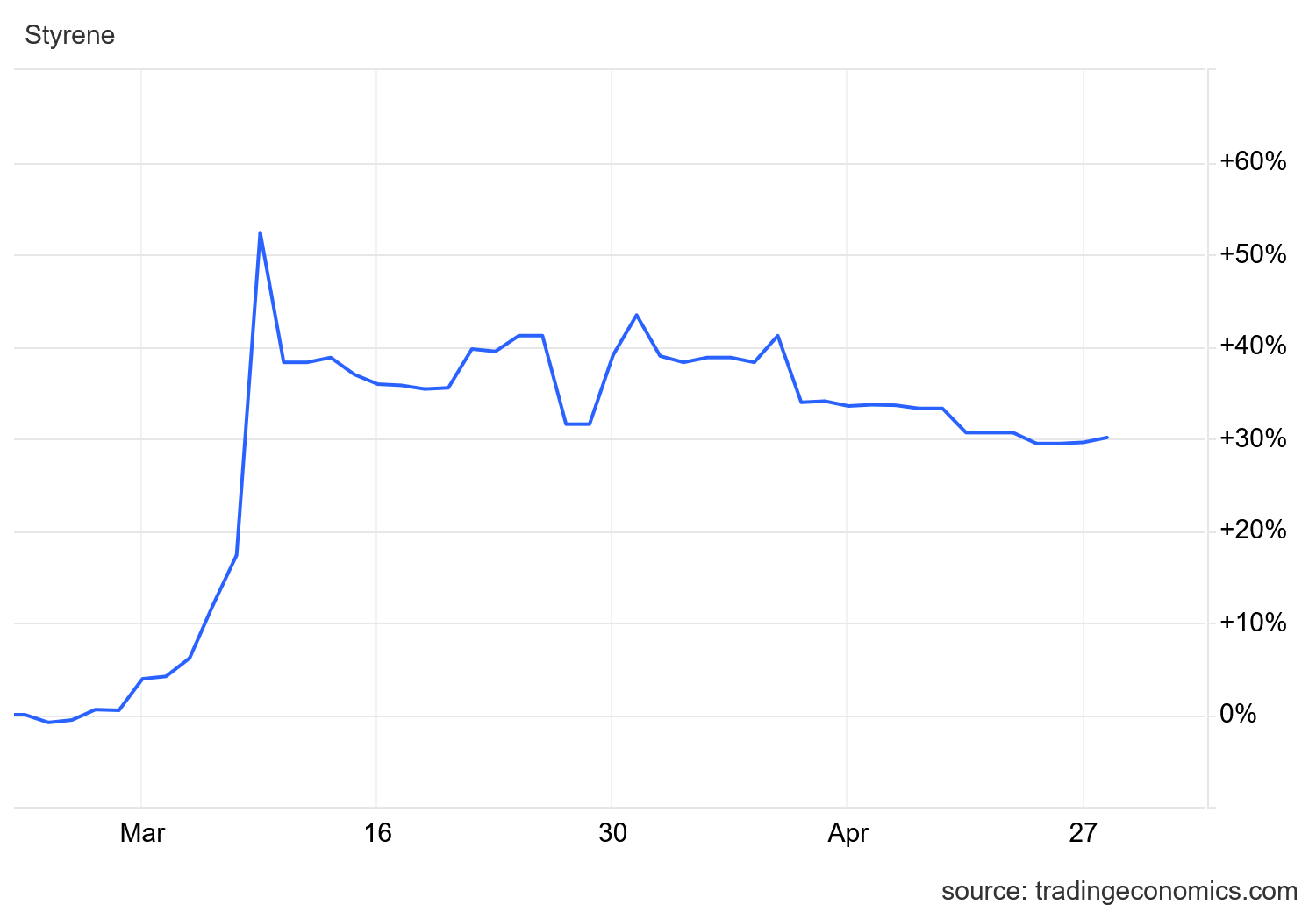

Styrene has not trended up, but its gradual decline appears to be bottoming out, at 30% above pre-war price levels.

Bitumen has had the most dramatic resurgence over the past week, pushing above 30% and closing in on a 35% price increase over pre-war price levels.

These are price and supply shocks which go well beyond energy, putting unanticipated cost pressures on most of China’s export-oriented manufacturing.

Inflation Or Stagflation?

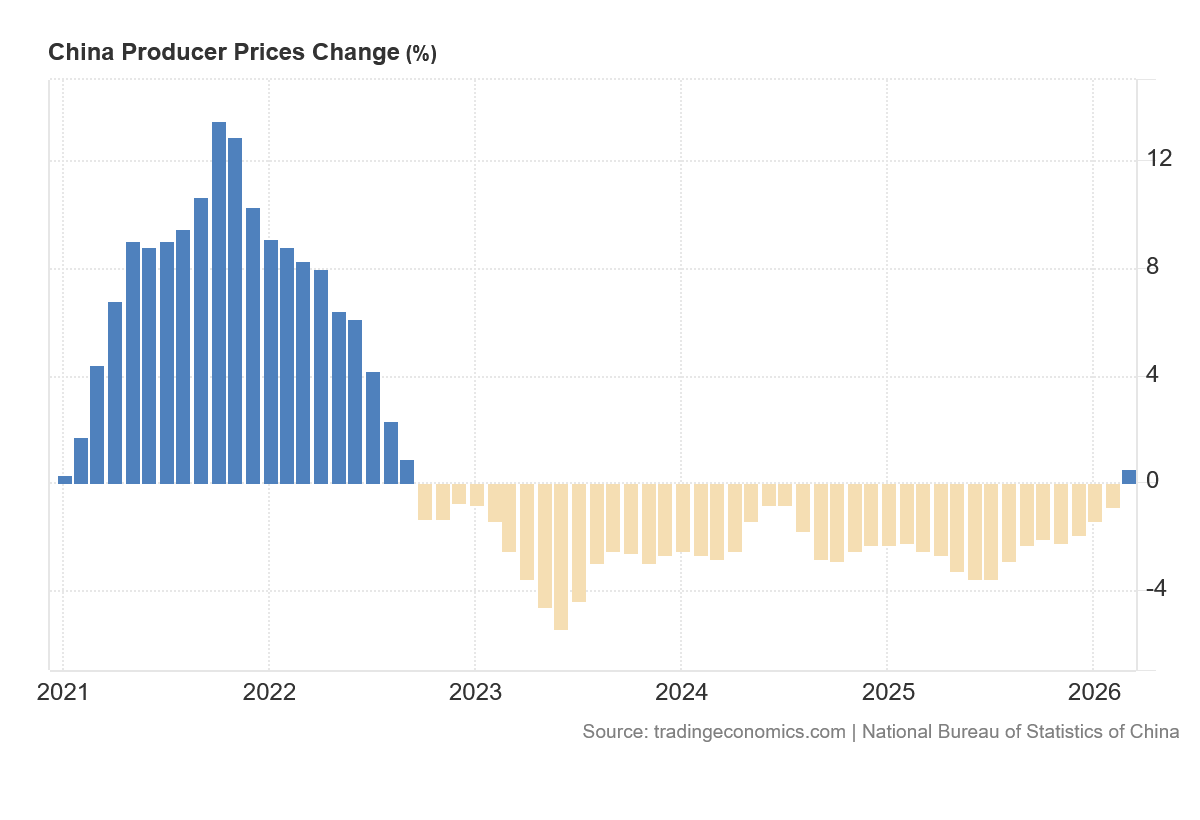

These cost pressures are not shy about making themselves known, as China’s Producer Price Index showed a year on year increase for the first time in over three years.

While a return to inflation after years of outright deflation on the surface is a welcome change, the signs are that the resurgent factory gate inflation is indicative of “bad inflation”—i.e., stagflation.

A number of economists are concerned that the economic fallout from the war with Iran will coalesce into a global stagflation crisis, with high prices and suppressed growth everywhere.

The war in the Middle East will likely affect the global economy and the United States, whether it continues for a short or long term, because of disruptions in the oil market that could trigger inflation and spur a recession, warn experts, economists and the International Monetary Fund.

Widespread stagflation could be the result of the war because of the long-term closure of the Strait of Hormuz, said Mohammad N. Elahee, a professor of international business at Quinnipiac University in Hamden, Connecticut.

As is proving typical among the financial “expert” class, analysts at Goldman Sachs insist that China is likely to fare better than other economies, because of its presumed “energy diversification”.

An analysis by a strategist at Goldman Sachs said China is in better shape than other major economies to withstand an oil shock thanks to its energy diversification over the past 10 years.

“China looks better placed than most in this oil shock,” Kinger Lau, chief China equity strategist, wrote in a note on March 30, which was seen by Yahoo Finance.

However, this narrative is no more convincing than Goldman’s last glowing assessment of the Chinese economy.

The reality is that price shocks of more than 30% in a variety of essential materials used throughout China’s manufacturing pipeline are exactly the sort of sudden inflation spike which can trigger a stagflation crisis.

In addition, the suddenness of Iran’s closure of the Strait of Hormuz means China has lost a major source of below-market crude oil. Even though China has been stockpiling oil, anticipating a rupture between the US and Iran, that stockpile is a problematic shield against the higher crude prices China must pay.

For economic security reasons, China was prepared for a potential energy crisis stemming from the US threats to Iran, which intensified at the beginning of 2026. In the first two months of the year, Chinese oil imports surged 16 percent for stockpiling. Russia exported around 300,000 barrels/day more to China in January and February (up to around 2.1 mbd), though for China this is by no means enough. China’s oil imports from the Gulf, now trapped in the Strait of Hormuz, are at least double the amount imported from Russia (5.4 mbd through Hormuz to China).

In other words, in the short run, China still needs to deal with the consequences of the sudden shut-off of a good part of its oil imports at below market price, in the context of a jump in the oil price, which could easily hover around $100/barrel for a sustained period. Standard modelling of China’s sensitivity to oil prices points to a 0.5 percent GDP reduction for a 25 percent increase in oil prices (Rasmussen and Roitman, 2011). This illustrates the stakes for China.

Higher materials prices and higher crude oil prices are not price shifts which can be ignored.

Those higher prices translate directly into a very real risk of stagflation within the Chinese economy.

China’s Economy Still Underperforming

Regardless of what the narratives say, the data shows that China’s economy is still underperforming in many ways, and has only just begun to show improvement in some of them.

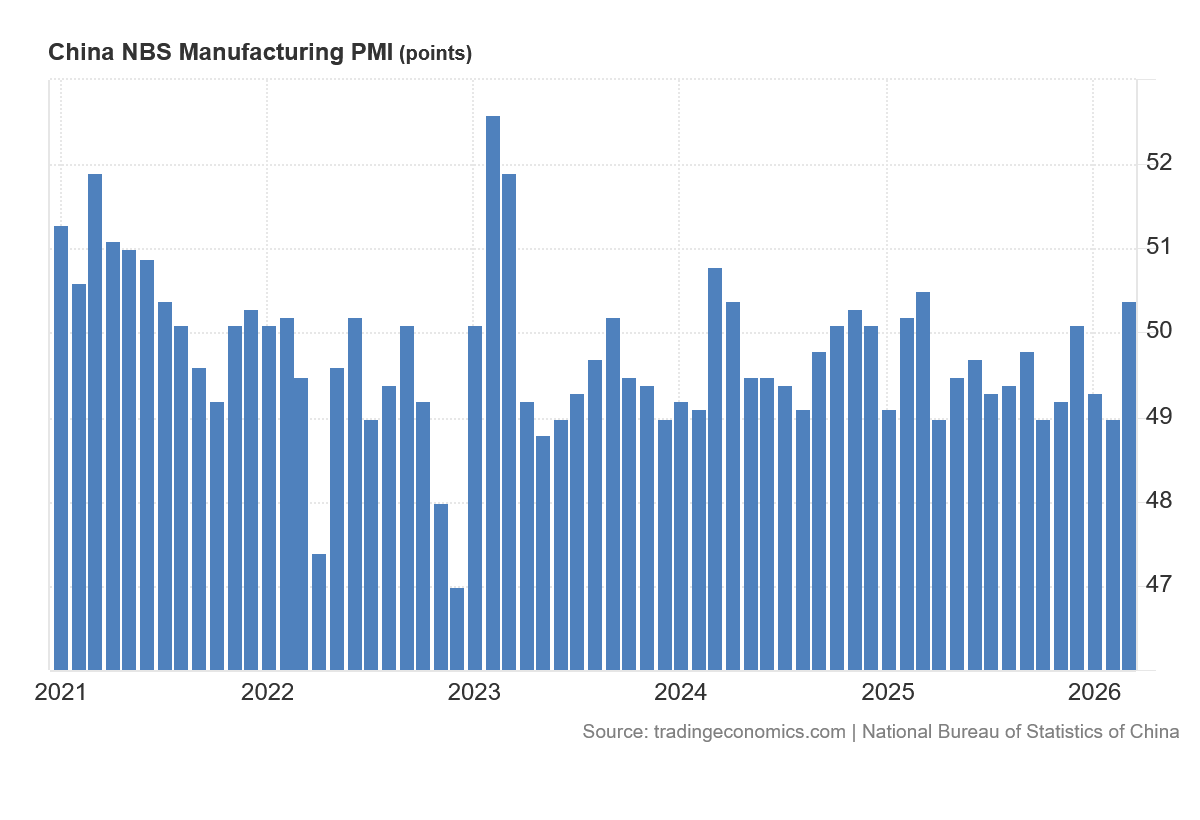

Although China’s official PMI gauge showed the manufacturing sector returning to expansion in March, that same gauge reminds us that China’s manufacturing sector has been in contraction for months at a time since the end of China’s bounceback from COVID Pandemic Panic lockdowns in 2021.

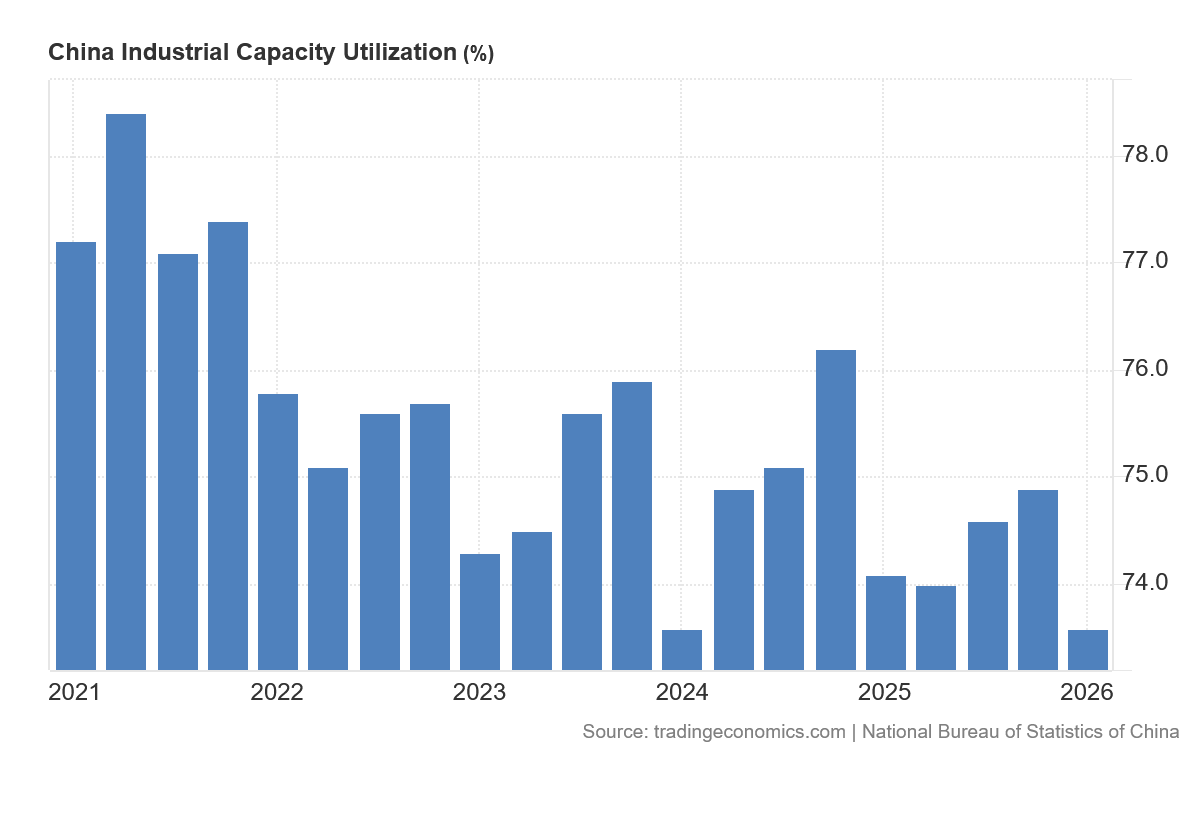

While China nominally turned in a quarter of strong GDP growth to start 2026, that same quarter saw China’s industrial capacity utilization falling to 73.6%, the lowest since the COVID Pandemic Panic lockdowns in 2020.

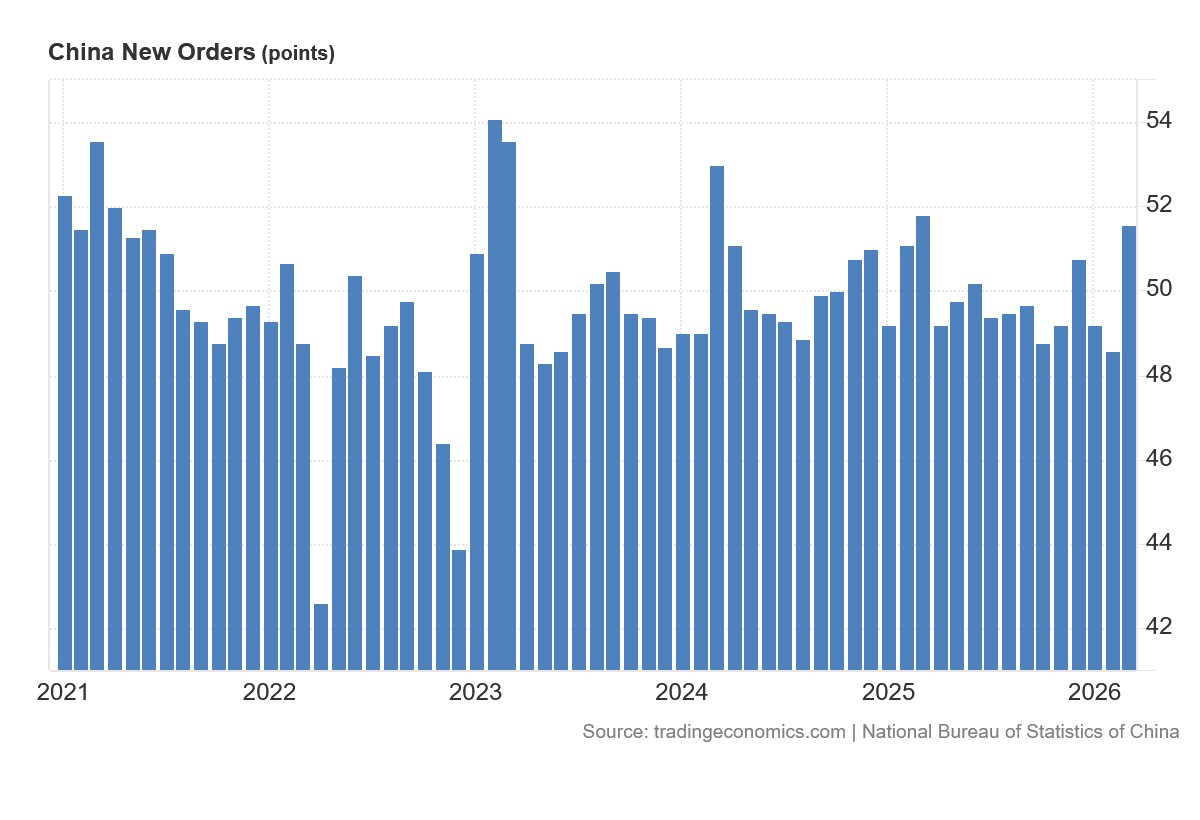

While new orders surged in March, for most of 2025 new orders were, like the rest of the manufacturing sector, contracting.

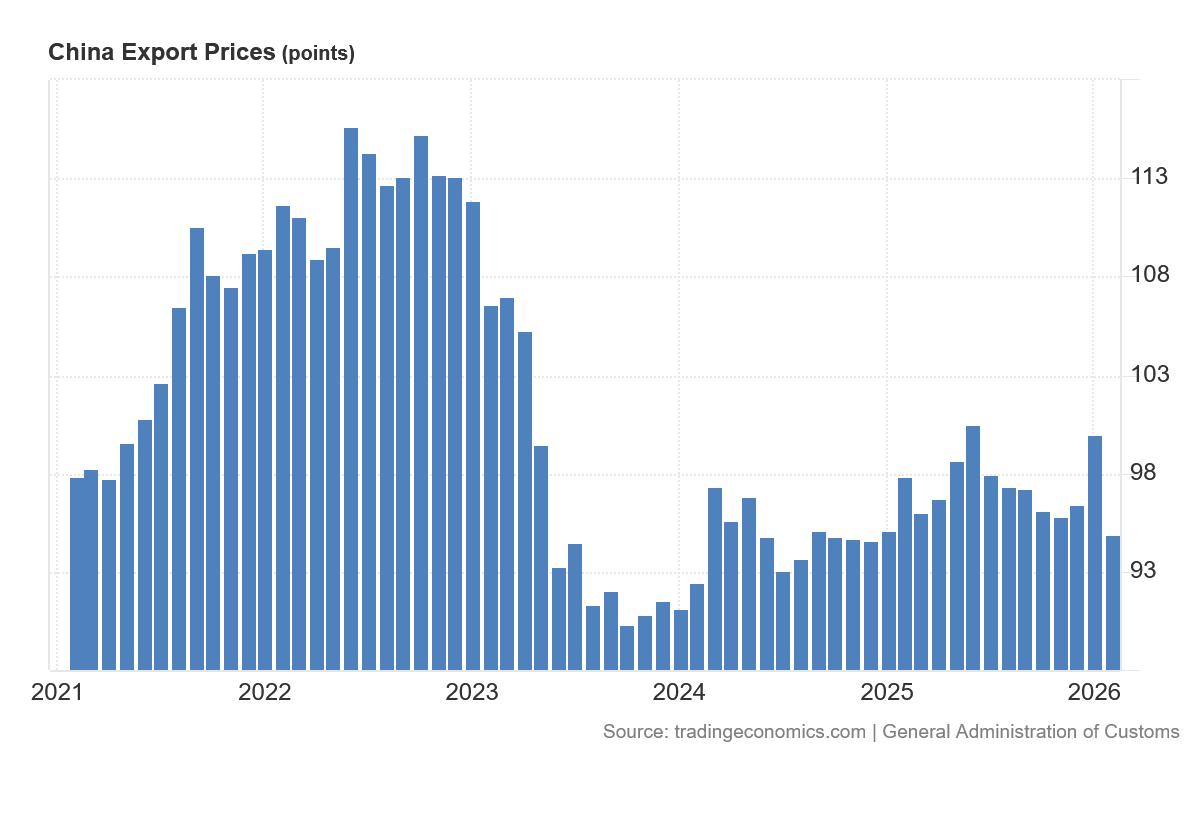

At the same time, export prices have been weakening for China since June of last year, when a steady export price rise ended and reversed.

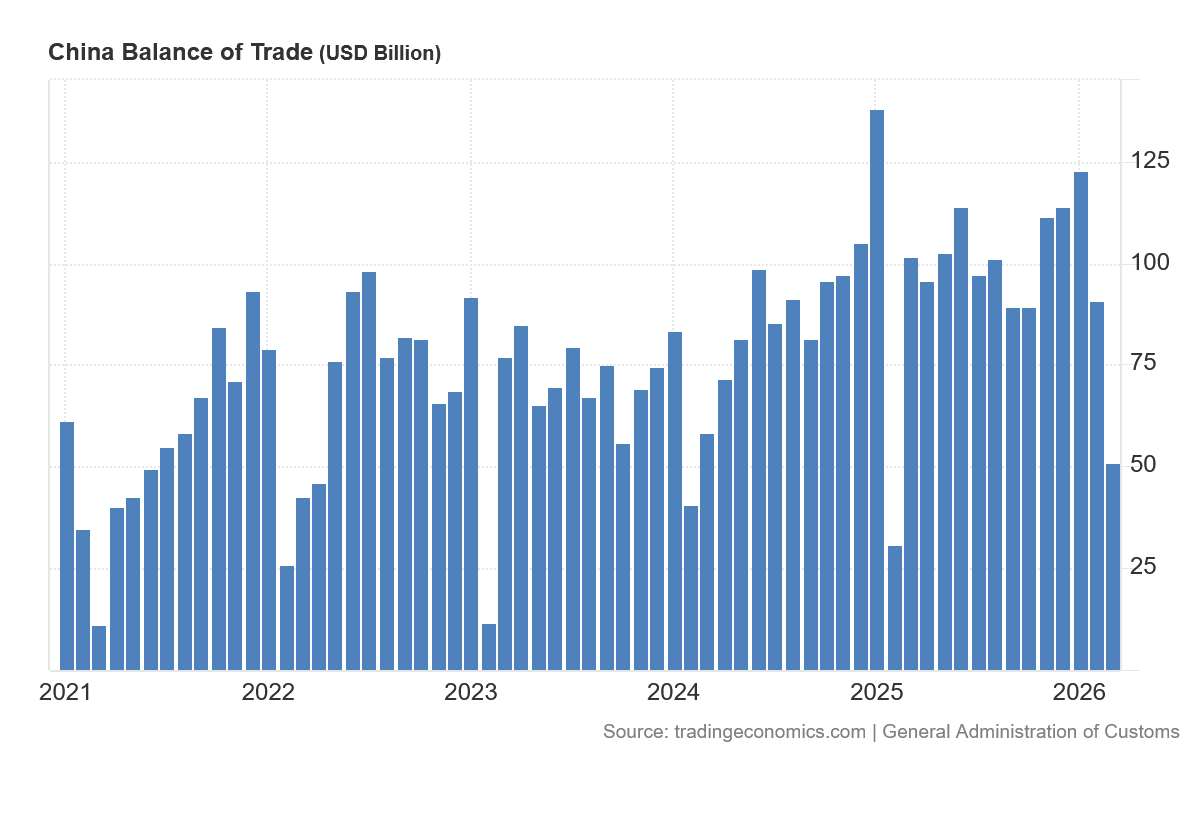

The export picture was further darkened by slowing export growth, which resulted in China’s trade surplus abruptly narrowing to $51 Billion.

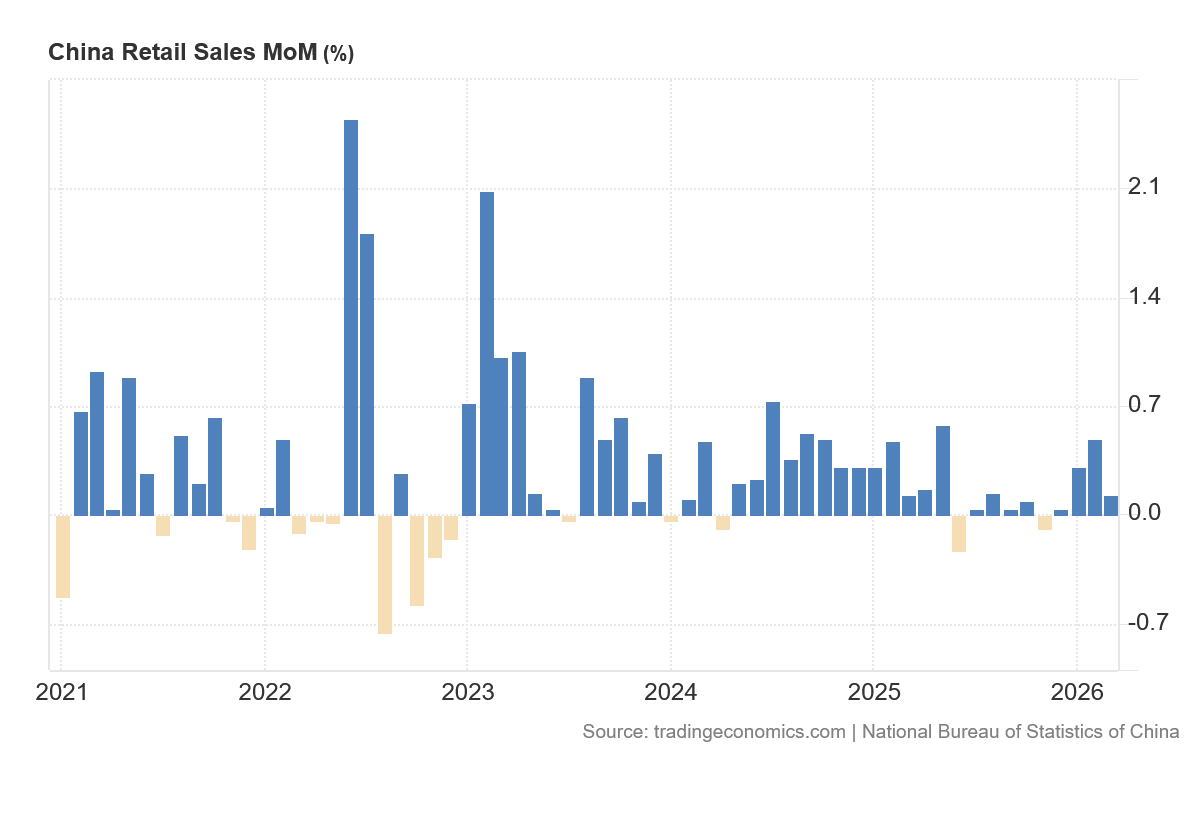

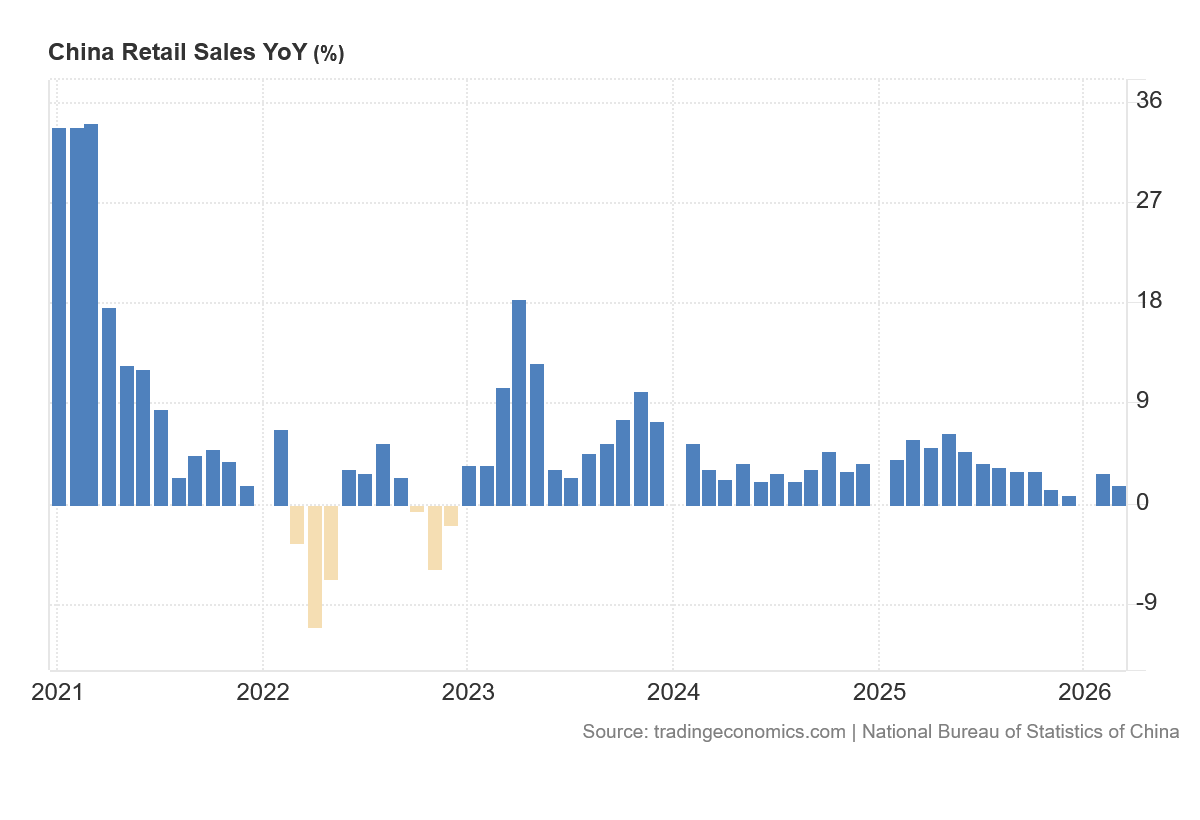

Domestically, retail sales growth continued to be sluggish, recording month on month growth of just 0.14% in March.

Year on year, retail sales growth slowed March to 1.7%, reiterating continued weakness in consumer demand.

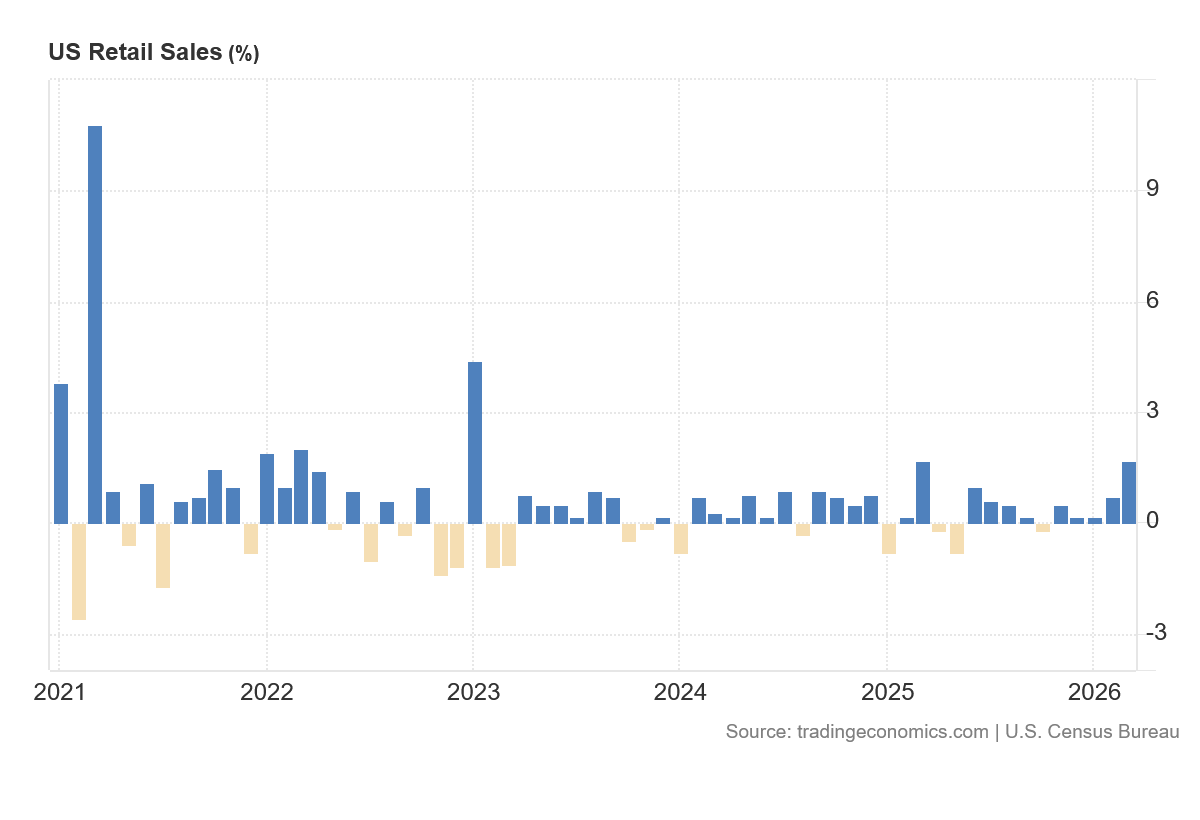

For comparison, month on month US retail sales growth in March was also 1.7%.

The retail sales growth for an entire year in China is one month of expansion in the US.

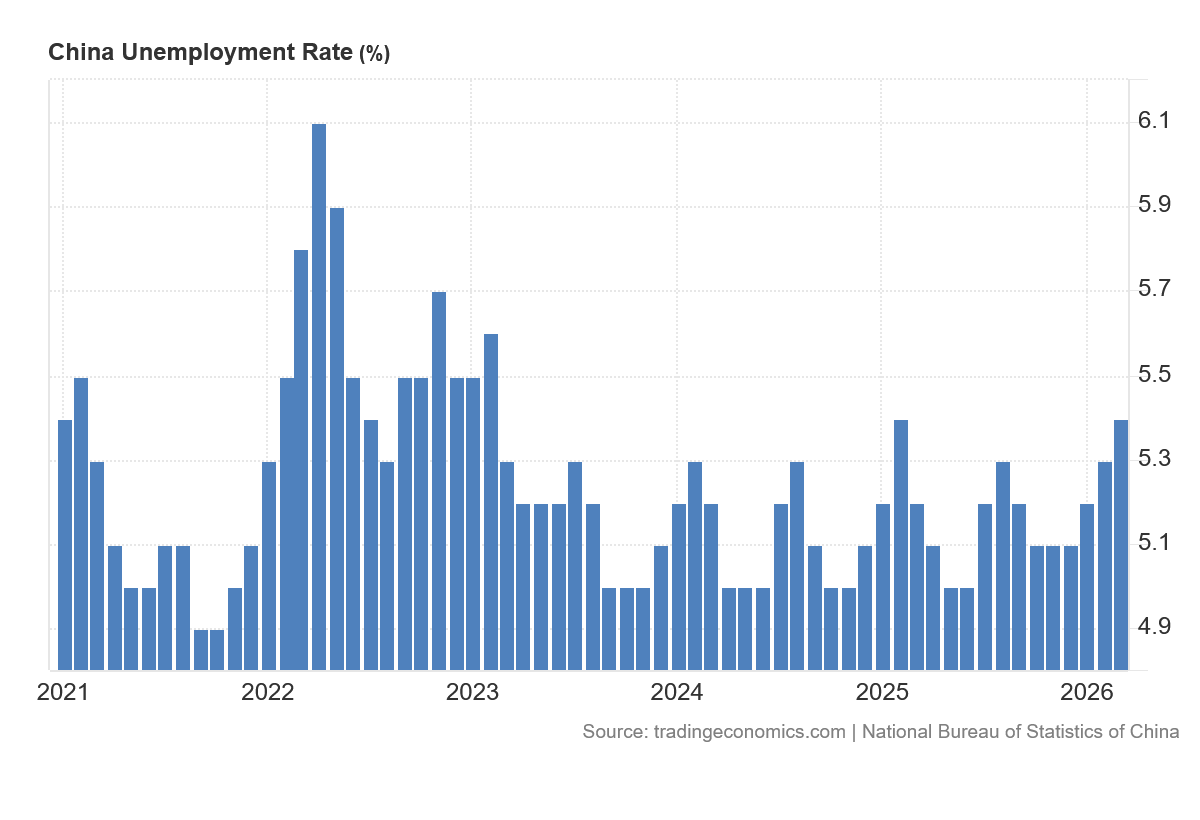

At the same time, unemployment has been rising in China, reaching 5.4% in March.

These are not statistics which speak of economic strength and vitality. China’s economy is not in absolute collapse, but neither is it showing robust growth except on paper.

The weakness that has been the norm for the Chinese economy for the past few years means that price shocks such as the world is seeing now in energy can easily turn into a stagflation crisis of no growth coupled with high prices.

There has been a real risk of stagflation here in the United States. That risk has been even greater in China.

China’s Housing Woes Continue

No look at China’s economy is complete without observing that China’s housing bubble is still deflating, and China’s property developers are still struggling.

China Vanke, one of the largest developers still going—and one which had until last year appeared to have avoided the debt crises which sank many of its competitors—recently announced intentions to extend yet another bond issue, the fourth such debt extension it has sought since the start of the year.

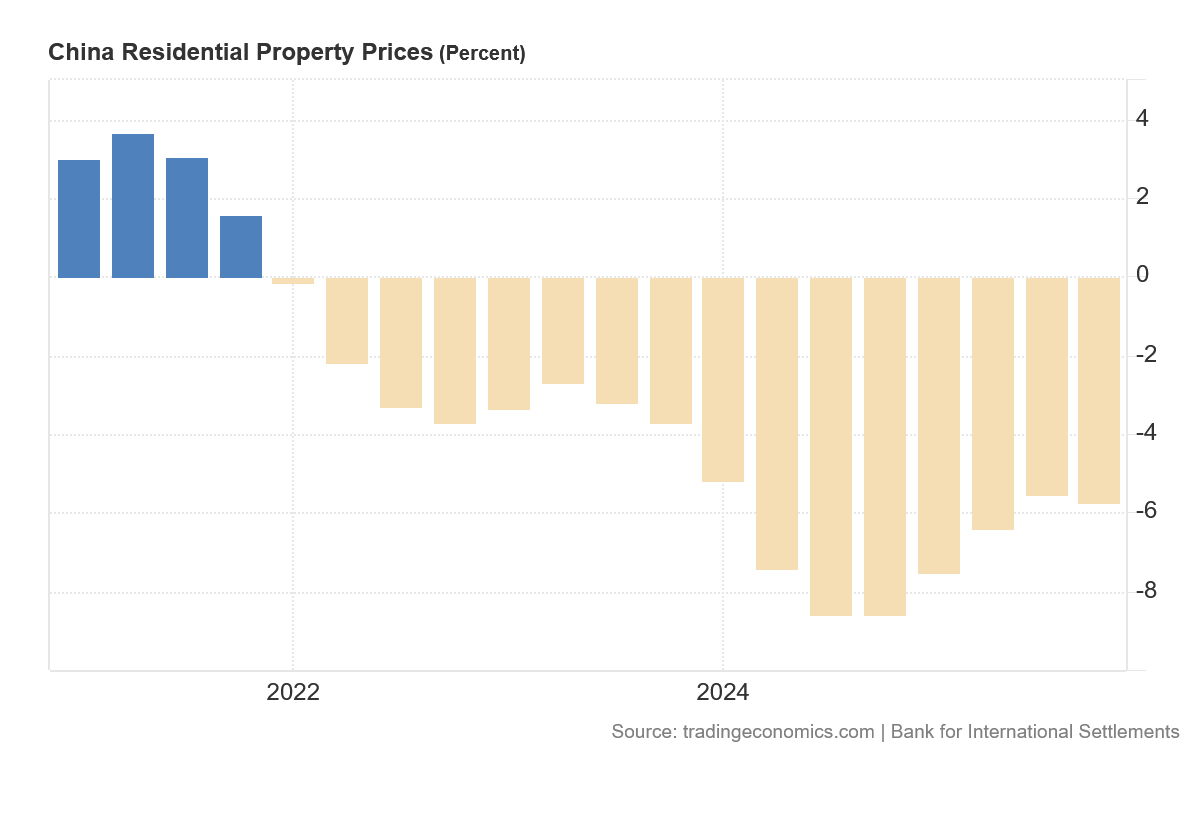

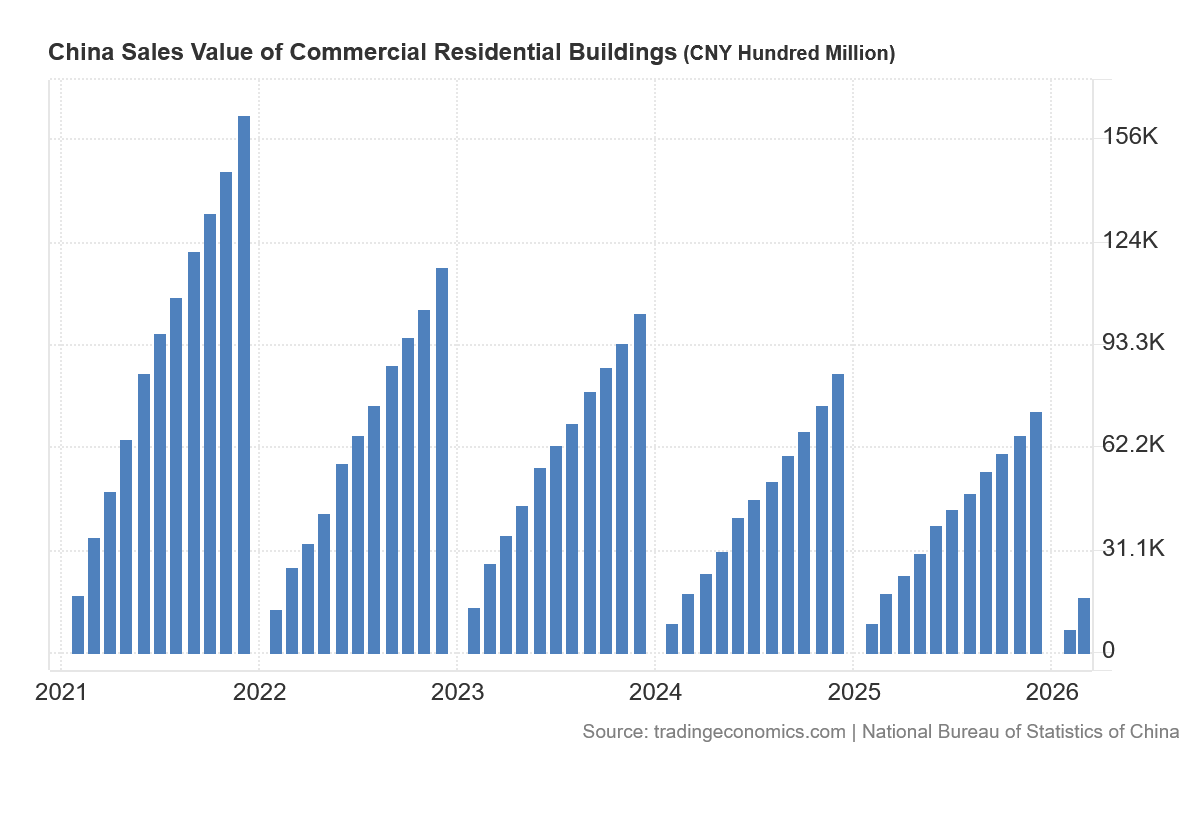

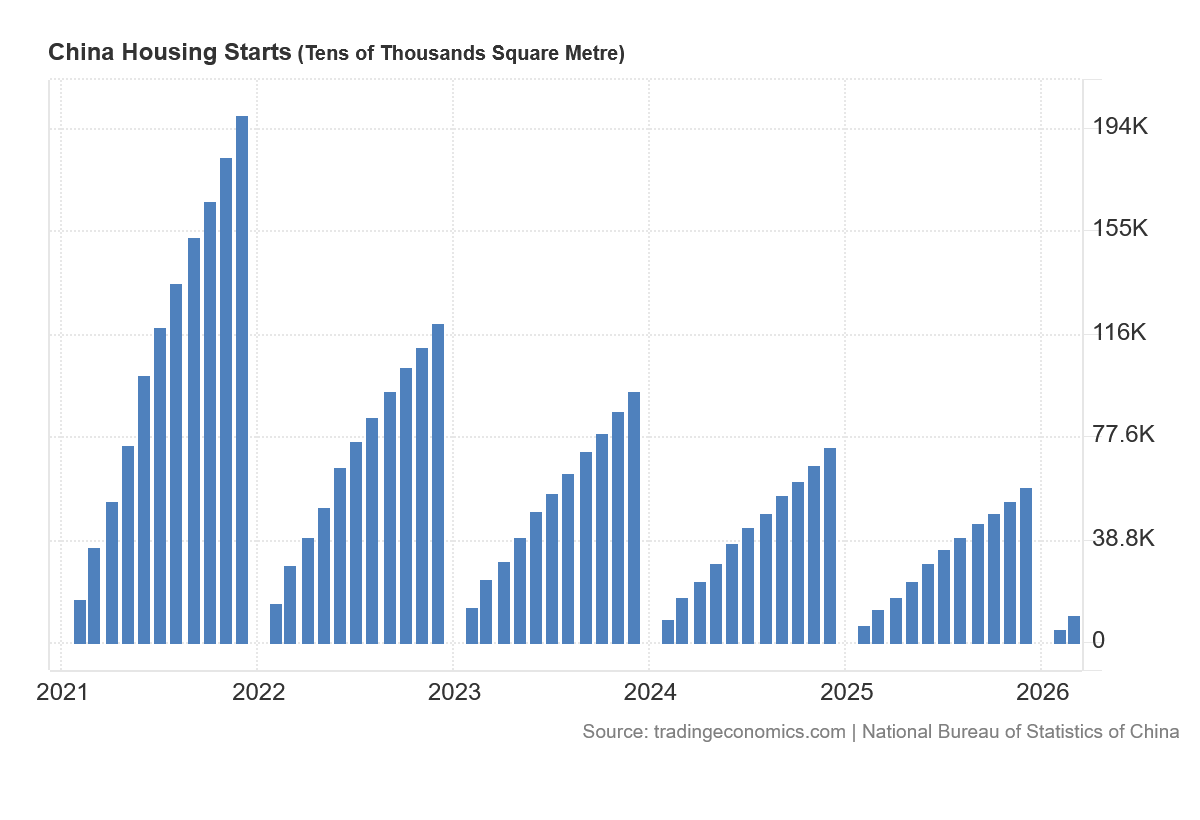

There is no mystery why China Vanke has been repeatedly flirting with debt default: China’s housing markets are still in deep decline even after years of contraction. Residential property prices have been falling without interruption since the first quarter of 2022.

New home sales in China were the weakest for the month of March since at least 2022, charting uninterrupted year on year declines.

Housing starts were also the weakest year on year since 2022.

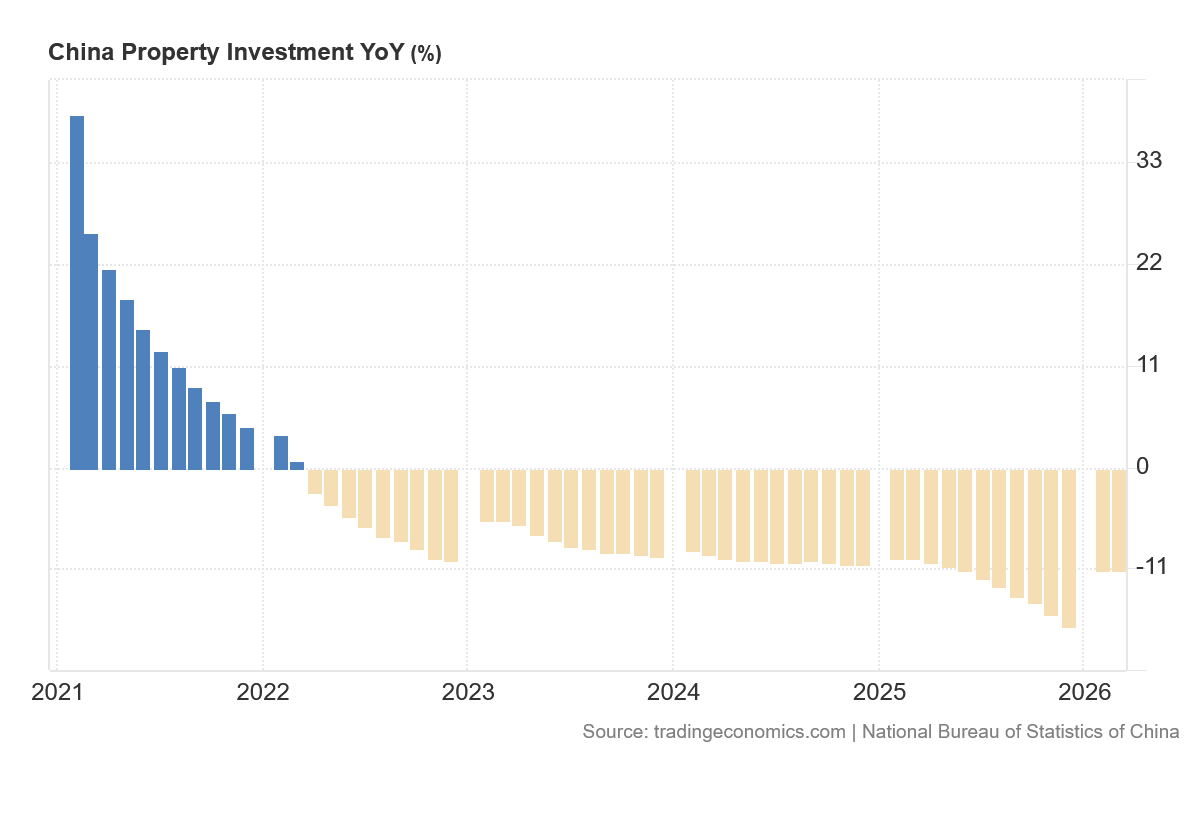

The consequence of these negative trends for Chinese housing culminates in steadily diminishing levels of property investment since 2022.

That housing markets are still in free fall even after three or four years not only demonstrates just how large the housing bubble was when it burst, it also illustrates just how much damage deflating that bubble will do in China.

The reality of the housing bubble for China is that its collapse represents what will ultimately be a cataclysmic level of wealth destruction among the rapidly diminishing Chinese middle class.

By far the most prevalent mechanism for wealth accumulation among ordinary Chinese has been real estate. As housing prices continue to fall, the value of real estate owned by individuals continues to erode.

If Beijing is serious about letting the bubble completely deflate without intervention, it will be forced to confront the literal destruction of the vast majority of wealth for China’s nascent middle class.

How China peaceably navigates those dangerous waters remains to be seen.

Demographics Are Still Destiny

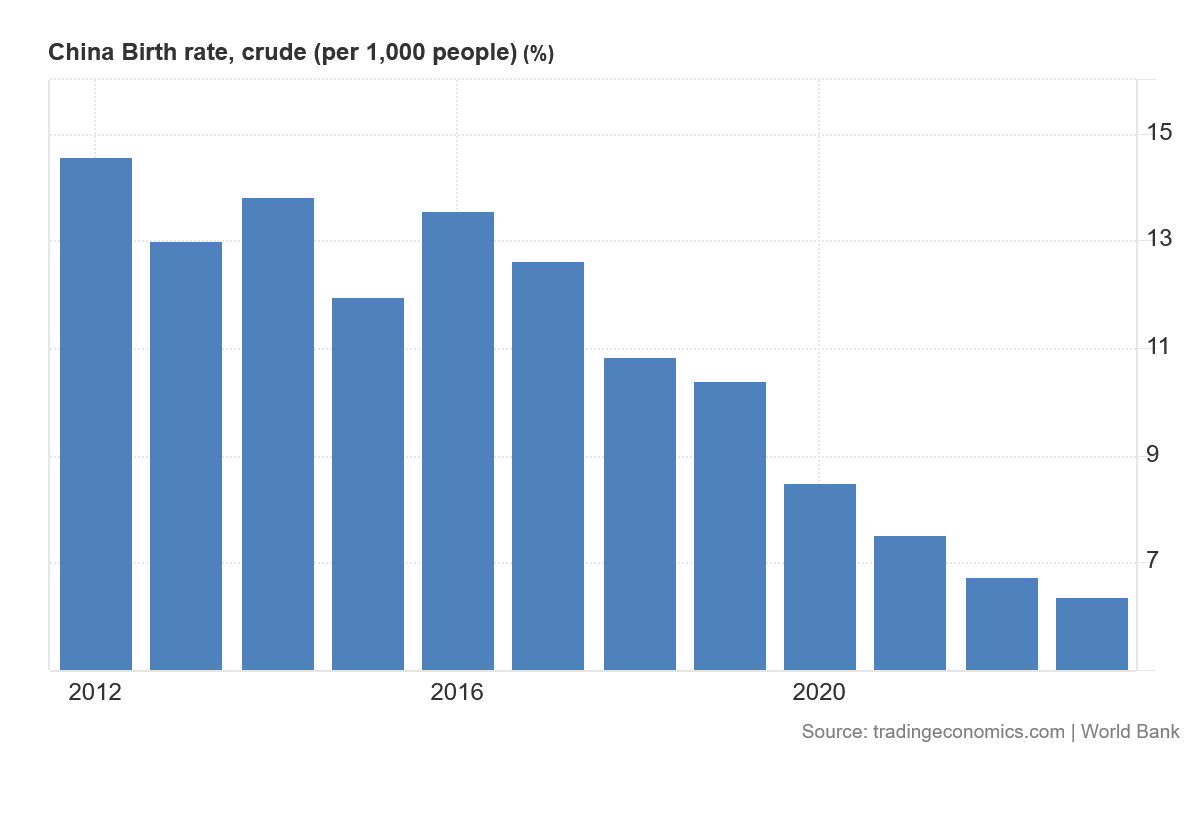

The darkest of the clouds hanging over China’s economy remains its declining and aging population.

China continues to be hobbled with a lethally low fertility rate, the unintended consequence of the One Child Policy.

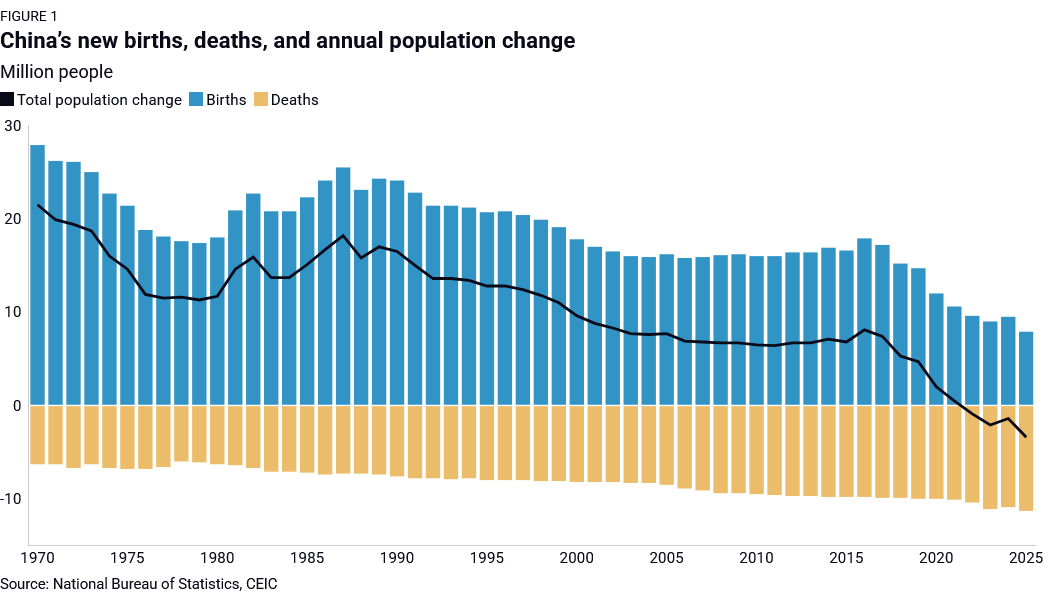

Not only is China’s population declining, the pace of that decline is arguably increasing, according to an analysis done recently by the US-based Rhodium Group, with increasingly immediate economic impacts.

Much has been written about the demographic headwinds to China’s economic growth. But these threats are typically portrayed as over the horizon, a problem for the next decade. The 2025 population statistics should force a rethink of those assumptions. What has long been described as a “gray rhino” risk—a palpable threat that is nonetheless ignored—appears to be charging sooner than expected. Last year China’s population declined by 3.4 million people, compared with a 1.4 million drop in 2024.

Within that decline, the more concerning development for economic growth was its concentration in developed coastal provinces. Migration inflows boosted population growth in eastern Chinese provinces to a greater extent than natural births.

The population decline, which has been ongoing for a number of years now, is accelerating.

China is losing population at an increasing rate.

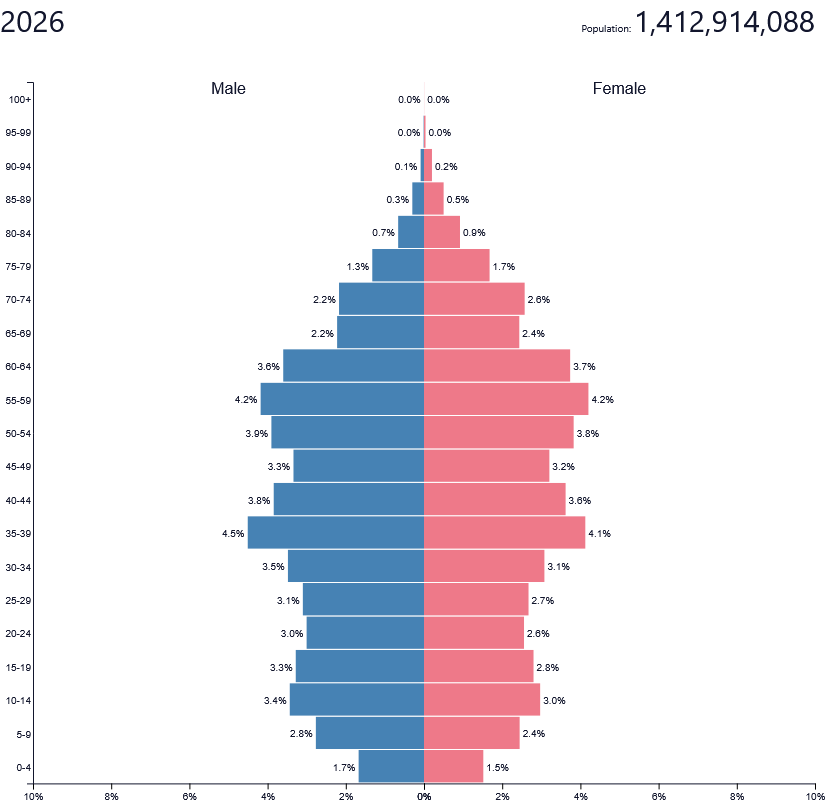

Most alarming for China is that the population decline is the result of cultural shifts surrounding family planning and marriage. Fewer women are choosing to have babies, with even fewer opting to have more than a single child, even though the One Child policy was largely abandoned a decade ago. At the same time, Chinese couples are getting married later in life, with the average age of married people having risen to 34 years in 2024.

The increasing age of Chinese married couples, and the increasing age of Chinese mothers, results in another troubling phenomenon for China’s population: it is getting older.

China has more older people than it does younger people. That is going to be the demographic reality for at least the next few decades.

Rhodium Group cites these realities and concludes that China’s population is at a point where the word “collapse” is the word to use.

The immediate pressure on China, both economically and politically, is that the aging of the population is putting increasing pressure on the government to fund social security pensions.

But the demographic pressures on China’s fiscal balance are likely still underappreciated. In 2025, Beijing spent 2.9 trillion yuan to fill the deficit from the social security fund, accounting for 10.1% of last year’s general budget spending. The deficit is likely to widen further given the aging of the population. The dependency ratio (number of working people supporting one elderly person) was around 4.4 in 2024 but will fall to 3.5 people in 2030 and 2.8 by 2035, based on our calculations.

On the surface, the size of the social security fund grew another 1.5 trillion yuan last year to lift the total balance to 16.0 trillion yuan. But without the 2.9 trillion yuan in fiscal subsidies, the social security fund would have reported a deficit of 1.4 trillion yuan (about 11 years to deplete the current balance without assistance from fiscal subsidies). The largest hole within the social security fund is from the pension fund, with a total of 6.9 trillion yuan in spending in 2024 against 5.8 trillion yuan in income. The pension fund alone received 1.9 trillion yuan out of 2.6 trillion yuan in total fiscal subsidies.

The social security funding shortfalls also highlight another economic reality arising from China’s collapsing demographics: consumption decline.

Broadly speaking, young people tend to consume more than the elderly. Young people are where family formation typically takes place, and families drive consumption more than any other single factor in every society and culture.

Without a growing cohort of young people, China has zero chance of making meaningful improvements to its levels of domestic consumption, and zero chance of increasing the role domestic consumption plays in overall GDP.

China does not have a growing cohort of young people, and will not have a growing cohort of young people for the foreseeable future.

Still In Decline

The grim reality of China’s economy is that it is still very much in decline. The Q1 GDP growth metrics, to the extent China’s data can even be trusted, do little to alter that conclusion.

China is still plagued by excess capacity, able to produce more of just about anything than there is demand for that item. That excess capacity is a constraint on future economic growth, because it means China cannot simply grow by producing more.

Excess capacity is a primary reason China has been grappling with broad economic deflation for the past several years. China’s core economic dilemma is that it produces too much for the world to absorb.

Excess capacity is the primary factor suppressing export prices. Although China’s economic model emphasizes exports, it cannot export at scale without driving down prices. It cannot grow export volumes for most products without encouraging price deflation in those same products.

In a perverse irony given China’s large population, that excess capacity extends into the housing market. The extent to which China has overbuilt housing is demonstrated by month after month of falling home prices even has property investment and housing starts decline. The challenge facing developers such as China Vanke is how to improve the financial bottom line when market conditions demand that developers build less rather than more.

Yet for all China’s excess production capacity, China does not produce what ordinary Chinese both want and can afford to purchase. In order for China to make meaningful progress on increasing domestic retail sales, China has to produce goods and services Chinese customers demand and for which Chinese customers are able to pay. It currently is having zero success in doing so, as the stagnant retail sales data shows.

In broad strokes, excess capacity is still the economic imbalance at the core of China’s ongoing deflation. To that the war with Iran is now adding a series of material costs, as well as price and supply shocks.

While the price and supply shocks inject new cost constraints and are pushing prices up, the price increases are not the result of increased demand for goods and services. The emergence of factory gate inflation in China is due to supply constraints, not demand expansion.

That distinction matters, because when prices rise because of increased demand, the higher prices eventually limit demand growth, effectively keeping the demand and supply sides of the economy in approximate equilibrium. When prices rise because of constrained supply, which is what is happening currently in China, the new supply constraints mean that demand must drop to restore that same equilibrium. China is already grappling with inadequate levels of demand for its economic production capacity, and the price shocks from the war with Iran are likely to push demand levels down even lower. That is the exact opposite effect from what China wants to see.

As in the United States, one month of factory gate inflation and materials price shocks does not automatically mean a stagflation crisis for China. That one month of price shocks, however, does mean all the ingredients are in place for a stagflation crisis. Whether China finds itself grappling the same sort of collision of inflationary and deflationary pressures that tortured the US in the 1970s remains to be seen, the longer materials prices remain elevated compared to pre-war levels, the more a 1970s-style stagflation crisis is likely to take shape within the Middle Kingdom.

The closure of the Strait of Hormuz is causing dislocations across the whole of the global economy. Europe is not immune. The United States is not immune. China is not immune. Contrary to many prevailing narratives, China is proving quite vulnerable to those dislocations.

The outcome of the war with Iran is going to determine how much and how fast China’s economy goes from bad to worse.

I’m going to say it again, Peter: BRILLIANT! You really are a genius at showcasing hard data to support your amazingly insightful analyses.

You’ve exposed China’s fundamental, structural, insurmountable economic problems for years. I am convinced they are a textbook case for how command economies simply cannot work longterm. And since Trump’s Iranian campaign started, it just keeps getting worse for China: “China’s core economic dilemma is that it produces too much for the world to absorb.” As the rest of the world scales back its consumption because of increased oil prices, China’s exports will continue to fall. What is wrong with the analysts at Goldman Sachs that they can’t grasp such an obvious problem? I really wish your writing could be prominently published in the New York Times, showing that you are right, and they are moronic!

Freedom in the Middle Kingdom Pete:

https://claude.ai/public/artifacts/6b7bfe37-7236-41a6-a67e-e753ee7dac89

🤔 All Facts Matter! 🇨🇳📹👀🧮⚖️🔢🐲🧭✨⏰