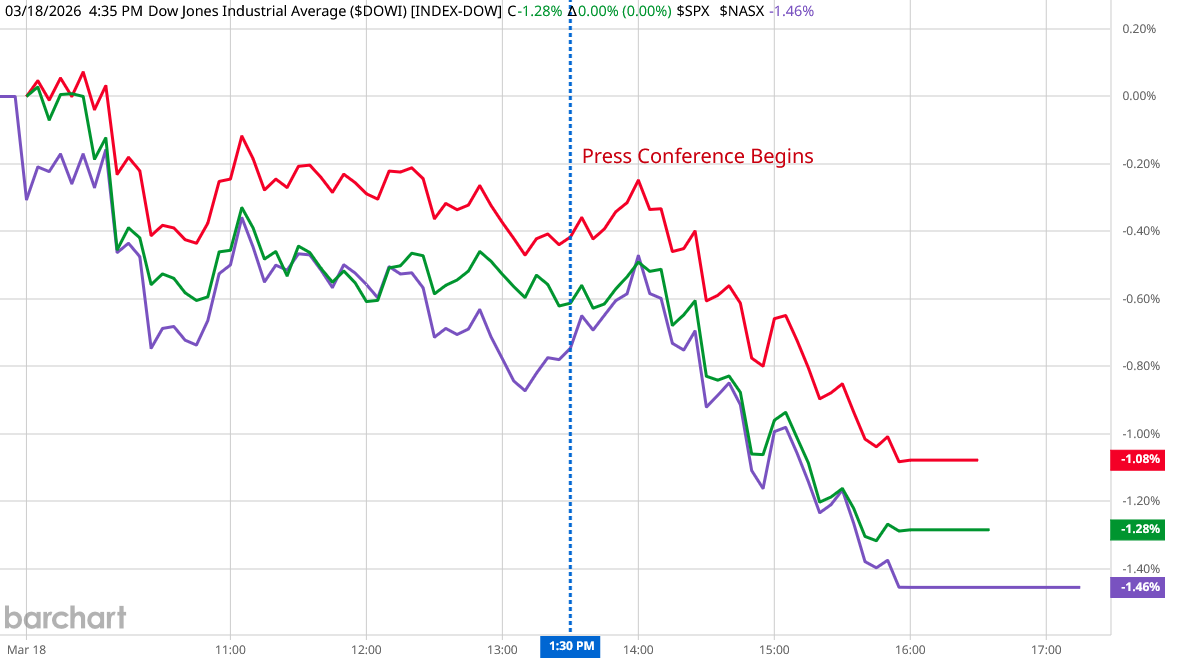

Jay Powell gave his usual post-FOMC presser yesterday, and at first glance he had his usual depressive effect on markets.

In a very turbulent news cycle, however, it is wisest to avoid indulging in excessive criticism of Powell’s penchant for pushing down equities. As the war with Iran expands, and as oil prices move ever higher, it would have been a remarkable feat if Powell had said anything which moved equities higher.

While there are many criticisms of Powell’s remarks to be made, I want to focus first on Powell’s dismissal of stagflation risks lurking in the US economy. By conveniently redefining the term around the 1970s oil shocks, he overlooks both the origin of the term and the significance it holds as an assessment of today’s economic conditions.

The term “stagflation” has a broader history than the narrow version Powell wants people to have. That history is a useful context for appreciating the stagflation risks we are facing today—and we are facing stagflation risks, even if Powell lacks the courage to say it out loud.

We begin with what Powell actually said, in response to a question from Maria Loisa Capurro with Bloomberg News:

Maria Loisa Capurro: If there have been any discussions about the risk of stagflation scenario.

Jerome Powell: As I mentioned, there is tension between the two goals, right? The upward risk for inflation and downward risk for employment. And that puts us in a different situation. You know, when we use the term stagflation, I always have to point out that that was a 1970s term at a time when unemployment was in double figures and inflation was really high, and the misery index was super high. Add them together, you get the misery index. And that’s not the case right now.

We actually have unemployment really close to longer run normal, and we have inflation that’s, you know, one percentage point above that. So calling that stagflation, it’s not, you know, I would reserve the term stagflation for stagflation, you know, a much more serious set of circumstances.

That is not the situation we’re in. What we have is some tension between the goals, and we’re trying to manage our way through it. It’s a very difficult situation, but it’s nothing like what they faced in the 1970s, and I reserve stagflation for that, the word for that period.

Maybe that’s just me.

“Stagflation”, in Powell’s mind, is when there is very high inflation and very high unemployment, producing a very high “misery index” figure.

Since the United States economy is arguably not facing super high inflation but for the inevitable price shocks heading our way from Operation Epic Fury, and since unemployment is theoretically not very high at all, stagflation is not a realistic scenario, according to Jay Powell.

Of course, Maria Capurro’s question was not about current conditions but about a future scenario. Powell appears to be saying that 1970s-style economic conditions are absolutely not in the cards, without actually saying much of anything. In that regard, it is a typical Jay Powell non-answer, where he throws out a bunch of words and hopes no one notices his evasiveness.

While markets were underwater anyway prior to Powell’s press conference, evasions such as the one he gave on stagflation did not help the markets at all, resulting in stocks declining further faster after he started speaking.

The biggest problem with his stagflation evasions comes when he mis-states the history of the term, and thus its actual meaning.

It’s a neat revisionist trick, confining stagflation to the 1970s, but the term did not arise during the 1970s, nor was it confined merely to descriptions of the brutal US economic conditions at that time.

The term “stagflation” was first attributed to Conservative Member of the British Parliament Iain Macleod, in a November 17, 1965 House of Commons Debate1.

I agree with the hon. Gentleman. It was. We now have the biggest gap between productivity and earnings of any time in modern economic history. Certainly history was being made. The index figure of industrial production at 133 for January—revised on the latest figures to, I think, 134; and for December it is down to 131—is certainly history. I can find no period—and I have checked this all the way back, with the possible exception of 1952—when in 13 years there was a year when the gap was so wide between what we should be doing and we were in fact doing.

We now have the worst of both worlds —not just inflation on the one side or stagnation on the other, but both of them together. We have a sort of “stagflation” situation and history in modern terms is indeed being made. There is another point behind the figures. As I say, production has fallen by 1 per cent. or ½per cent. while incomes have gone up, perhaps, by 8 per cent. This can result only in two things happening in the months ahead; either a considerable increase in our import bill to meet the increased consumer expenditure or a very real rise in our prices.

Macleod’s concern at the time was declining productivity in the UK at a time when incomes—and, by extension, prices—were going up.

Note that the rates he was describing—0.5-1pp drop in productivity against an 8pp increase in incomes—are not at the levels that would invite close comparisons to the 1970s in the United States. As Powell correctly noted in his non-answer to Maria Capurro, in the 1970s inflation was high while unemployment was also high.

However, the distinction between 1960s Great Britain and 1970s United States is fundamentally one of degree. Iain Macleod was describing an economic situation that was starting to get bad, whereas our looking back on the 1970s typically lands us in the late 1970s when the economic situation had already gone bad.

Just as we can have extreme or mild inflation, just as we can have extreme or mild deflation, we can have extreme or mild stagflation. The US economy in the 1970s is an example of extreme stagflation. 1960s Great Britain is an example of more moderate stagflation (which, we should remember, would get considerably worse in the years following the 1965 debate).

Powell might want to confine his use of the term “stagflation” to only the extreme scenarios, but history does not lend itself to such a narrow understanding of the term. Neither does a closer scrutiny of the forces underpinning the phenomenon.

If we go back to Macleod’s original formulation, an essential ingredient for stagflation is obviously rising inflation. We must take care to note, however, that direction and magnitude are two different dimensions of measurement. Whether inflation rises a little or a lot, what matters for stagflation is that it rises.

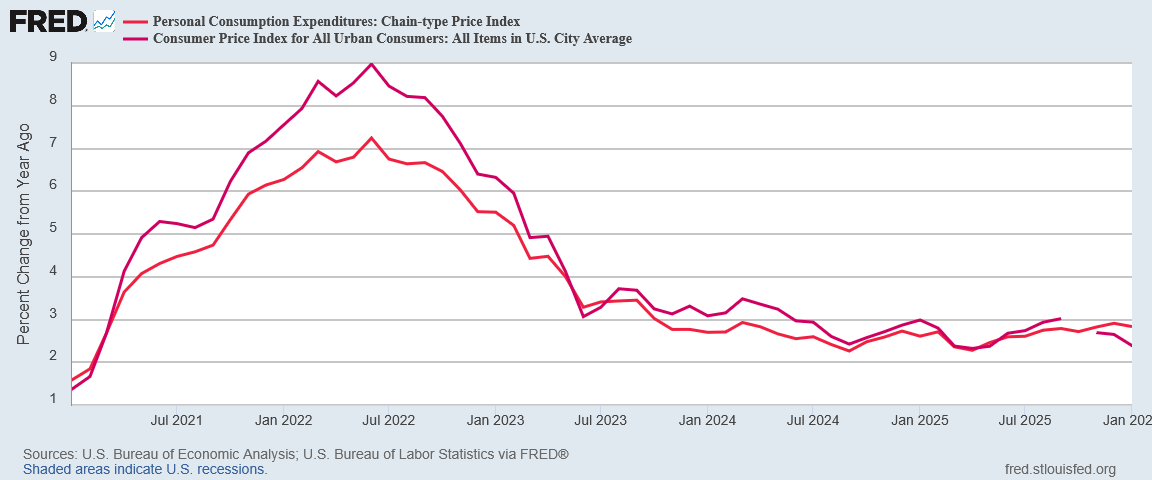

At first glance, we might dismiss inflation concerns. It is readily apparent that, relative to the 2022 hyperinflation cycle, we are not facing a serious rise in consumer price inflation at the moment.

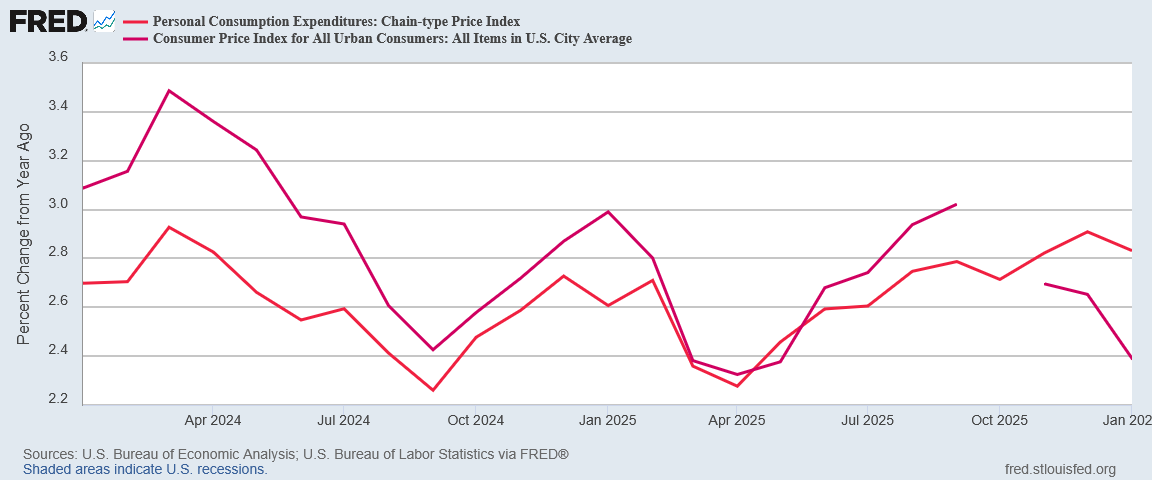

However, if we zero in on the last two years, we have to note that year on year inflation did start to trend up beginning in September of 2024.

The increase is hardly a dramatic rise, and the volatility in the data generates enough statistical noise to obscure any readily discernible trends in the month on month inflation metrics.

Not only have we not seen inflation rise much, but we have also seen headline CPI clearly decline since last summer. As I wrote about February’s CPI print, we are not seeing inflation getting appreciably hotter at the moment.

Corporate media pearl-clutching notwithstanding, once again the inflation report was notable for the absence of…well…inflation.

Why I am I now saying that inflation has risen? Because it has, albeit by an amount that is not necessarily significant and over a longer time frame than we usually consider when scrutinizing the monthly inflation data. More to the point, I am noting that, from a perspective of understanding stagflation, we have one of the predicates already established: rising inflation. We do not need to go farther than this and we should not go farther than this.

Looking back at Macleod’s original stagflation formulation, the other predicate was falling productivity.

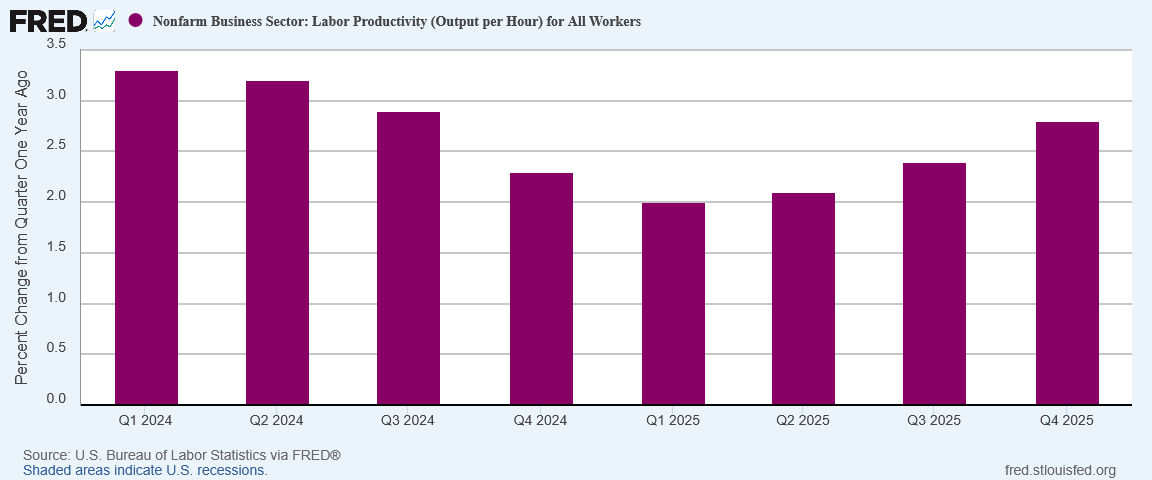

When we look at labor productivity growth in 2024 and 2025, we see that productivity slowed significantly in 2024.

Labor productivity has staged a recovery in 2025, but there is a clear softening of labor productivity growth over the past two years.

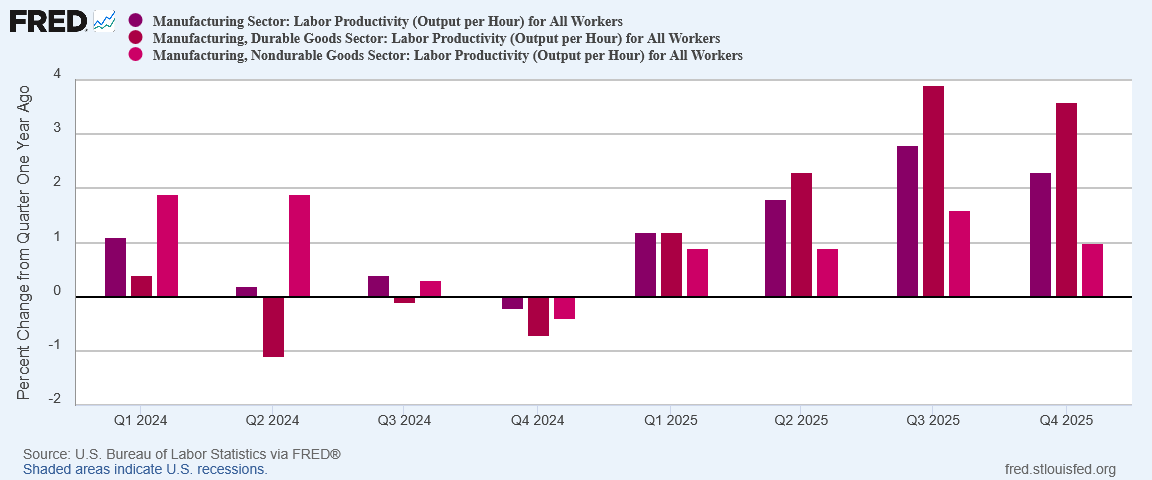

Manufacturing productivity tells an even worse tale for 2024, with outright productivity declines, before mounting a recovery in in 2025.

Even with recovery, nondurable goods productivity is still softer at the end of 2025 than at the beginning of 2024.

For 2024 at least, we can say that the second of Macleod’s predicates for stagflation were met.

However, labor productivity is only one dimension to consider. In the 1970s, the dimension that captured everyone’s attention was the unemployment metric. If we expand our assessment of the labor aspect of stagflation to include joblessness, a much stronger case for seeing the second of Macleod's predicates for stagflation emerges in the current data.

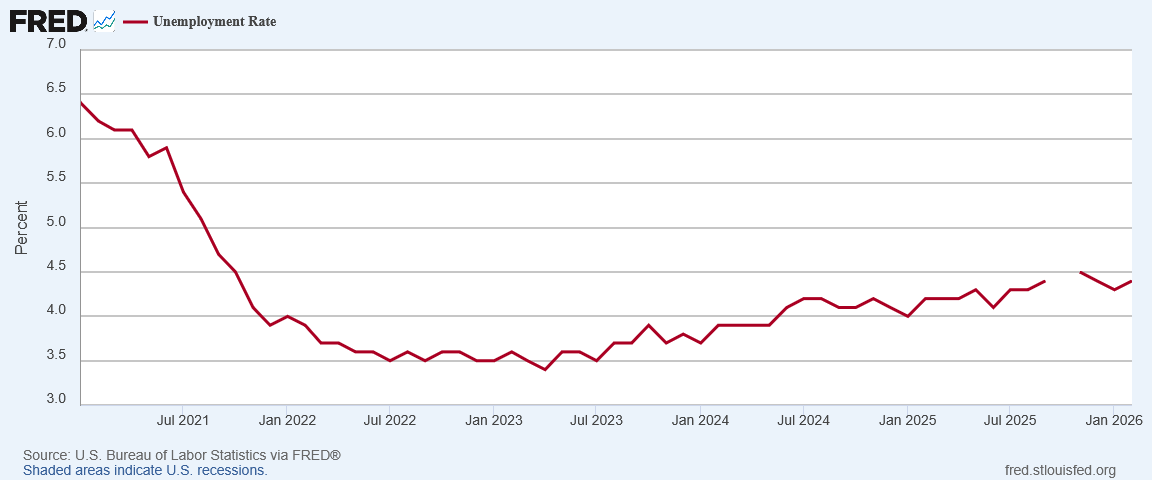

Here Powell hides behind a longstanding statistical sleight of hand regarding unemployment—not counting those technically not in the labor force as unemployed—to argue that unemployment is fairly low. On the surface, the unemployment rate now is certainly lower than it was in the 1970s and 1980s, when it was routinely above five percent and even flirted with double digits.

Nevertheless, while low relative to the rate as measured in the 1970s, the unemployment rate has been rising steadily since mid-2023.

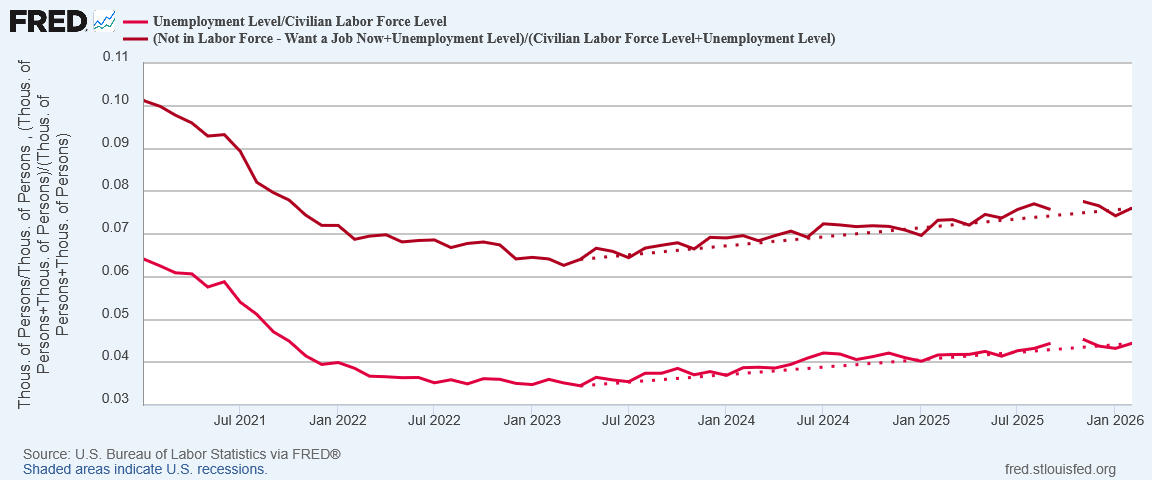

Moreover, if we address the BLS’ statistical manipulations regarding labor force participation by adding in the number of people technically not in the labor force but who want a job now, we find that current “real” unemployment rates are on par with what we saw during the 1970s.

Adding in people out of the labor force but who want a job now puts the February “real” unemployment rate at 7.6%—indisputably 1970s level unemployment.

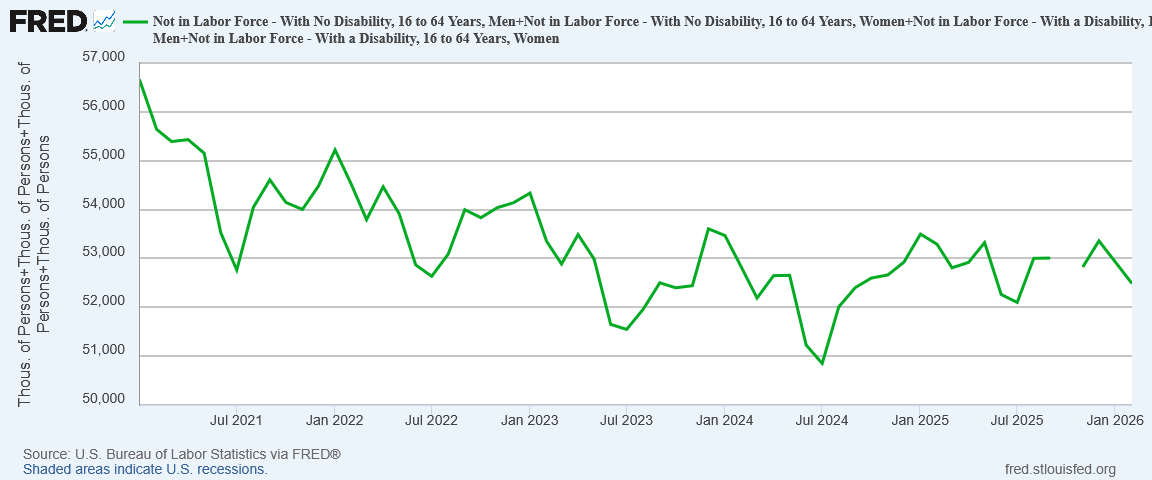

If we look more closely at those persons not in the labor force in general, we find their number has been increasing. Looking at those not in the labor force between the ages of 16 and 64, their number began increasing around July of 2024.

These are workers still in prime employment years, and they are apparently leaving the labor force altogether. A portion of these arguably should be counted as “unemployed” as they want a job now, but even without that consideration a growing number of “working age” people in this country are exiting the labor force.

While the rising inflation aspect of the stagflation formula risks being needlessly alarmist, the falling productivity/rising joblessness aspect is far more definitively met with the current data. In the absolute strictest of terms, both criteria are met within contemporary data sets. The crucial variance between the US today and both the US in the 1970s and the UK in the 1960s is the magnitude of the forces at work.

The only aspect of the present data which allows Powell to claim the current economic climate is not “stagflation” is the severity of the both the inflation and the joblessness. As we are not seeing “extreme stagflation”, Powell would say we are not seeing stagflation at all. That is both disingenuous and more than a little dishonest.

Conceptually, stagflation is when rising prices collide with low economic growth or even economic contraction2.

Stagflation combines stagnant economic growth, high unemployment, and persistent inflation.

Jay Powell himself last year articulated that the potential precursors to stagflation are lurking in the US economy3.

We have stressed that it will be very difficult to assess the likely economic effects of higher tariffs until there is greater certainty about the details, such as what will be tariffed, at what level and for what duration, and the extent of retaliation from our trading partners. While uncertainty remains elevated, it is now becoming clear that the tariff increases will be significantly larger than expected. The same is likely to be true of the economic effects, which will include higher inflation and slower growth.

Powell’s thesis at the time was that President Trump’s tariffs would result in higher inflation and slower growth—the textbook understanding of stagflation.

As I have written on a number of occasions, however, the risks of stagflation have been lurking in the US economy for the past few years. Those risks did not emerge just because of President Trump nor because of the Liberation Day tariffs. While I dispute the contribution of Trump’s tariffs to those risks, I have never disputed the existence of those risks. Quite the contrary, I have been arguing the existence of those risks even when Powell and other “experts” denied them.

What makes stagflation challenging to comprehend—or to even grasp that it is occurring—is that it is a counterintuitive phenomenon.

Inflation—rising prices—is largely considered a sign of rampant economic activity. In Milton Friedman’s monetarist view of inflation, inflation rises when the velocity of money rises4.

This phenomenon of prices changing by more than the difference between the change in output and the change in money stock is often observed and is not special to these particular periods in India. The reason is not far to seek. When prices are going down, money becomes a more desirable way in which to hold assets; its value is increasing day by day; hence people have a strong tendency, if they expect the price decline to continue, to hold a larger fraction of their wealth in the form of money. On the other side of the picture, when prices are going up, money becomes a less desirable form in which to hold assets. In consequence, people tend to economise on their money balances; velocity tends to increase. How much velocity will change depends on whether the fall in prices or the rise in prices is anticipated. Generally, when inflation has started after a period of roughly stable prices, people initially do not expect prices to continue rising. They regard the price rise as temporary and expect prices to fall later on. In consequence, they have tended to increase their monetary holdings and the price rise has been less than the rise in the stock of money. Then as people gradually become wise to what is going on, they tend to re-adjust their holdings. Prices then rise more than in proportion to the stock of money. Eventually people come to expect roughly what is happening and prices rise in proportion to the stock of money.

Money velocity is simply the number of times money circulates through the economy. The more money is circulating, the higher the money velocity. The higher the money velocity, the more people are buying and consuming, and thus the more they tend to bid up prices for goods and services. Thus inflation is commonly apprehended as the consequence of runaway market activity.

However, factors such as falling productivity and rising joblessness are generally associated not with inflation but with its inverse5.

The inverse of inflation, of course, is deflation.

Strictly speaking, “deflation” is falling prices. Obviously, consumer prices are not going to rise and fall at the same time. However, one of the forces which can drive deflation is a drop in aggregate demand6. This intuitively makes sense: people buy less and prices come down.

If people are buying less, then by definition the consumption portion of an economy is contracting—or “deflating”.

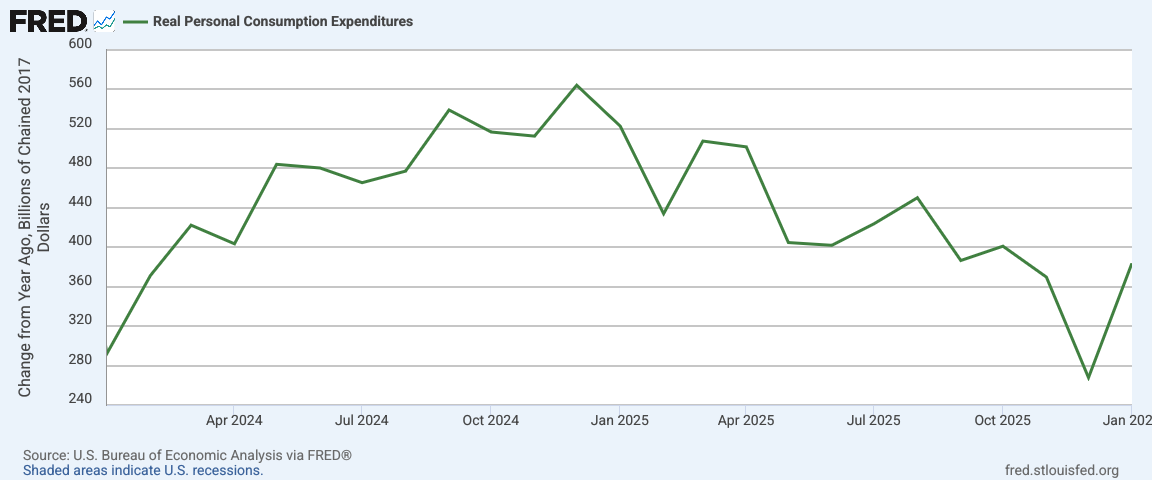

When we look at real personal consumption expenditures year on year since January 2024, there has been a clear drop in consumption.

A drop in consumption is indisputably a deflationary force, even though we are seeing rising inflation and not deflation in consumer prices overall.

As stagflation occurs when we are seeing stagnant growth or even contraction in the economy while prices are rising, it necessarily occurs when we see both inflationary and deflationary forces exerting significant economic influence simultaneously. I frequently apply a shorthand description by saying that stagflation is when inflation and deflation occur together, but the crucial understanding here is that we are experiencing an economy subjected to oppositional stresses.

The US economy is quite literally being pulled in opposite directions, as it is arguably trying to expand and contract at the same time.

The combined magnitude of the oppositional forces might be dismissively mild in Powell’s view, but that the combined magnitude is not zero is on its own worth of note and should not be dismissed.

We are not seeing, at present, high inflation in the US economy. We are seeing rising inflation, but at an incremental level which is not at present cause for alarm on its own.

We have been seeing considerable signs of economic stagnation. I have been writing for months about the “jobs recession”. Even Moody’s Analytics Chief Economist Mark Zandi last December embraced the term in giving his stark assessment of the US economy.

The stark assessment comes as hiring has stalled, unemployment is rising—especially for the most vulnerable workers—and layoff announcements are piling up. To Zandi, the next stage is already visible: “If we actually do see layoffs pick up,” he told Fortune, “then it certainly would be a jobs recession.”

This is where Powell loses the narrative when it comes to stagflation.

No, we are not seeing stagflation at present, except in the most incremental and technical fashion. The oppositional forces are present and discernible, but they are not (yet) at a 1970s level of severity.

We are, however, seeing several indicators that a stagflation scenario is a real risk to the economy. A significant inflation shock coupled with the soft labor markets the United States has endured for the past few years could very easily translate into a stagflation scenario.

Bear in mind that a significant inflation shock is heading towards us and likely to hit very soon, as the war with Iran has sent oil prices soaring.

Soft labor markets and some very nasty oil price shocks are what gave us stagflation in the 1970s.

We have soft labor markets. We are about to have a very nasty oil price shock.

Will we have a repeat of 1970s stagflation?

At present, we do not know. We can safely forecast that there will be consumer price inflation in March, and possibly April and May as well as a result of the oil price rises that have happened since February 28. We cannot extrapolate with any accuracy how much consumer price inflation we will get.

We should not, however, ignore the possibilities for stagflation which are demonstrably lurking right now in the US economy.

The jobs recession is real. Soft labor markets have been the reality of the US economy since at least 2022.

The potential for a significant oil price shock is real. When we have news reports of Iran and Israel bombing Persian Gulf oil production facilities, that there will be an oil price shock in the very near future is practically a given.

Powell was wrong about stagflation. He was wrong to pretend there is no risk of stagflation. He was factually wrong about unemployment, just as he has been for years.

We are not experiencing significant stagflation at present. We are at far greater risk of significant stagflation than either Washington or Wall Street have the courage to admit.

Iain Macleod. Column 1165. "Economic Affairs". House of Commons Debate 17 November 1965. Hansard. Volume 720. Columns 1155–284.

Gratton, P. What Is Stagflation, What Causes It, and Why Is It Bad? 4 Feb. 2026, https://www.investopedia.com/terms/s/stagflation.asp.

Powell, J. Economic Outlook. 4 Apr. 2025, https://www.federalreserve.gov/newsevents/speech/powell20250404a.htm.

Friedman, M. “Inflation: Causes and Consequences. First Lecture.” Dollars and Deficits, Prentice Hall, 1968, pp. 21–46. Retrieved online from https://miltonfriedman.hoover.org/internal/media/dispatcher/271018/full

Picardo, E. Inflation and Unemployment: Understanding Their Relationship. 2 Mar. 2026, https://www.investopedia.com/articles/markets/081515/how-inflation-and-unemployment-are-related.asp.

The Investopedia Team. Understanding Deflation: Causes, Impact, and Economic Consequences. 17 Nov. 2025, https://www.investopedia.com/ask/answers/111414/what-causes-negative-inflation-or-deflation.asp.

A little off topic: the French Navy is also stopping unflagged Russian tankers. The U.S. is not alone.

https://news.usni.org/2026/03/23/french-navy-intercepts-suspected-russian-tanker-in-western-mediterranean

I’ve always found it admirable, Peter, that you have such good economic foresight yet you refrain from most speculation. What wise restraint! Not many analysts or pundits can do this. The result is you have long term credibility, and they don’t. Kudos!