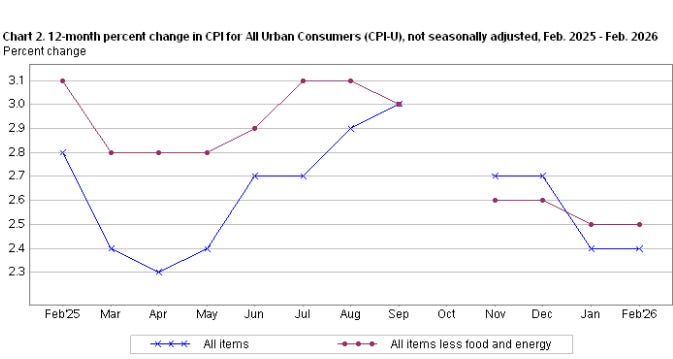

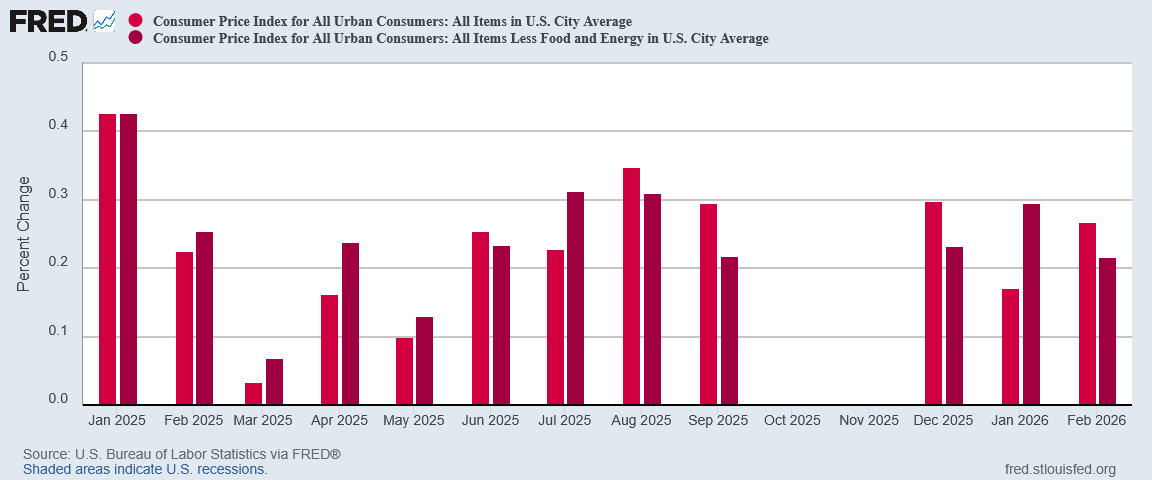

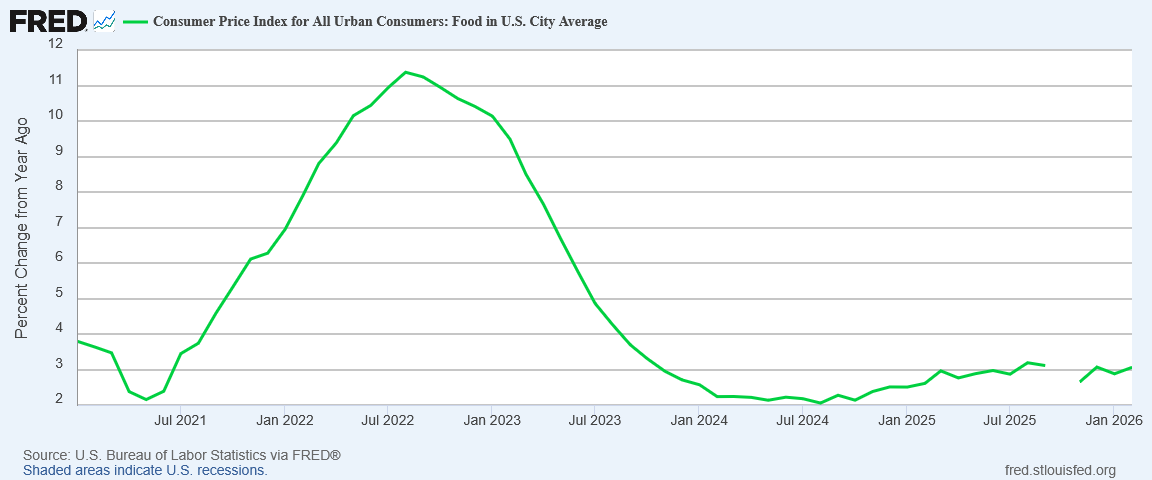

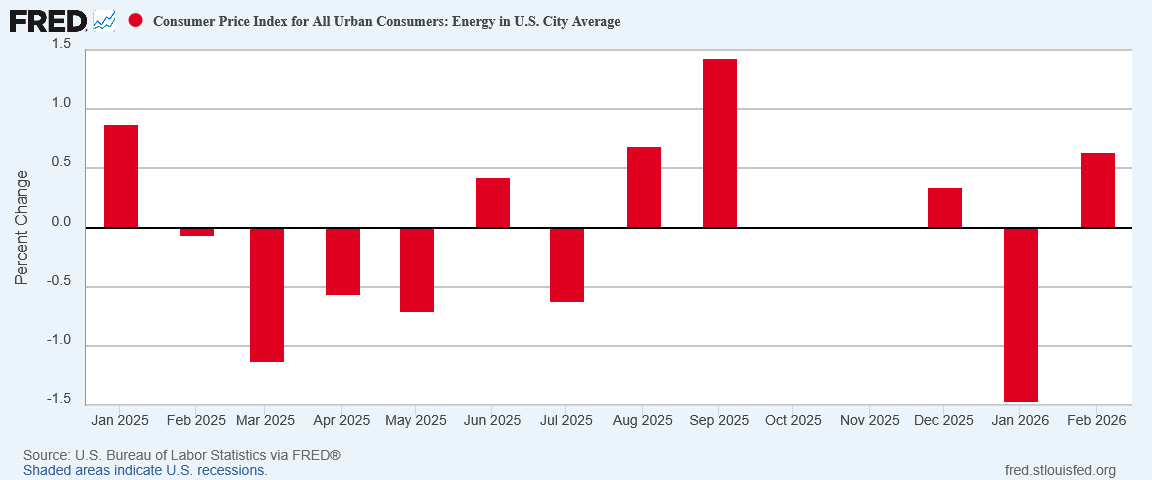

The all items index rose 2.4 percent for the 12 months ending February, the same increase as reported for the 12 months ending January. The all items less food and energy index rose 2.5 percent over the year, also the same increase as reported for the 12 months ending in January. The energy index increased 0.5 percent for the 12 months ending February. The food index increased 3.1 percent over the last year.

Naturally, the more egregious corporate media outlets such as Politico scoured the CPI data to find evidence of “surging” prices to justify their headlines.

Of course, “muh tariffs” once again bore much of the blame.

Once again, that narrative does not withstand even modest scrutiny, as is made plain when we unpack the data.

While President Trump Operation Epic Fury attacks on Iran are almost certain to produce a significant burst of inflation for March, February’s consumer price data is the calm before the coming storm. That’s a narrative that does withstand scrutiny, even when we unpack the data.

Every article I publish takes time, care, and independence. A paid subscription fuels that work and shields it from outside pressure. If you’re able, join me today.

Headline Inflation Did Not Change

Corporate media pearl-clutching notwithstanding, once again the inflation report was notable for the absence of…well…inflation.

Core inflation technically declined from 2.51% to 2.47% year on year. The BLS news release rounds to the nearest tenth of a percent, which means the 0.04pp shift for both headline and core inflation is not considered statistically significant.

Right away, that empirical reality discredits any narrative of prices “surging”.

Month on month, the change was the same: headline inflation rose 0.1pp, from 0.17% to 0.27% (reported by the BLS as 0.2% to 0.3%), while core inflation fell from 0.29% to 0.21%.

While inflation is still above the Fed’s holy grail level of 2% year on year, what inflation did not do in February is rise.

Still, the data we have is for February and not March, and predates the war with Iran. We will have hotter inflation in March, but for February we are still blessed with a conspicuous lack of overall inflation.

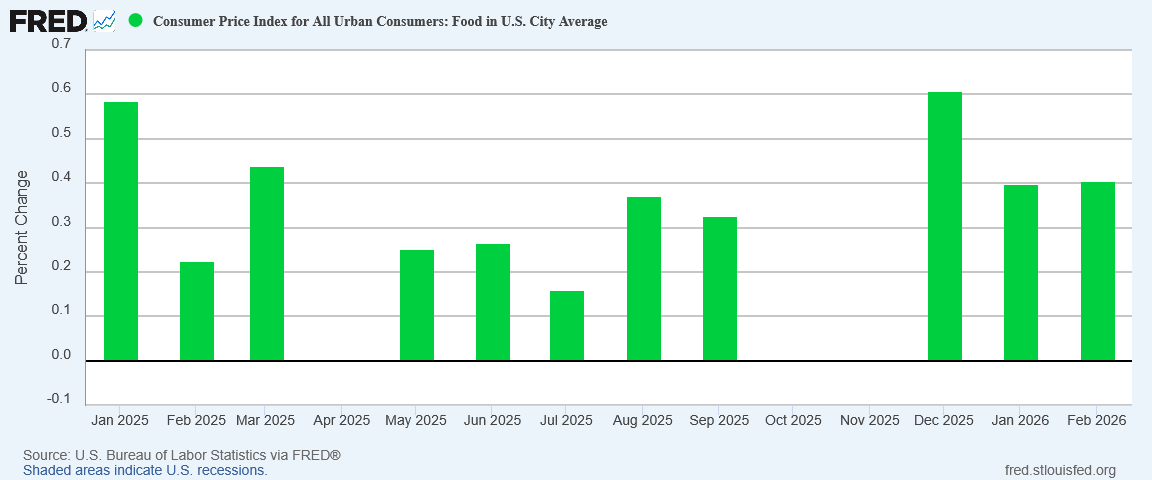

We do well to remember that food and energy prices are broken out from core consumer prices because they exhibit far greater volatility and much greater sensitivity to a variety of external factors.

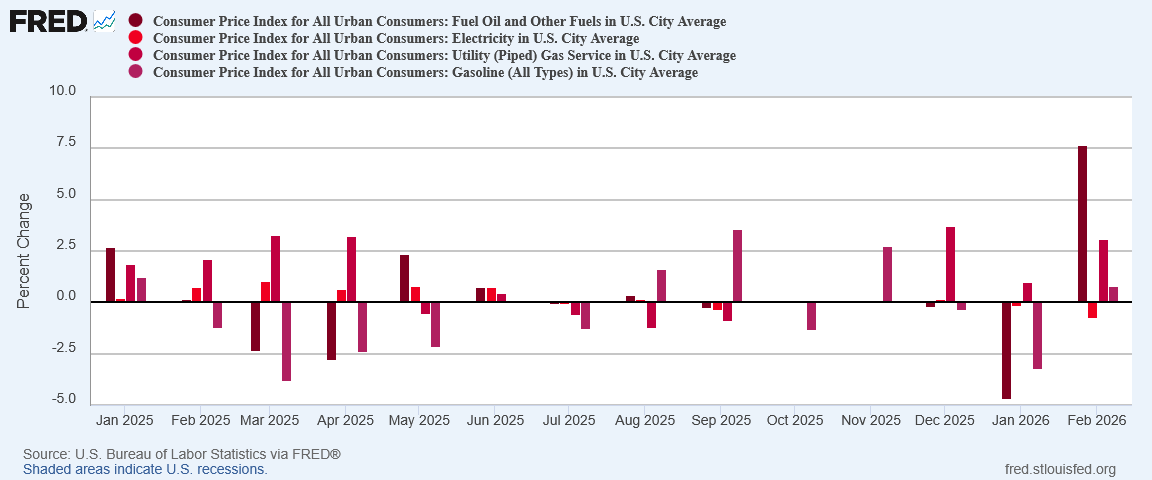

We should also note that the bulk of February’s hotter energy price inflation print was from a legitimate spike in fuel oil prices, even as other energy price components were relatively muted in their fluctuations.

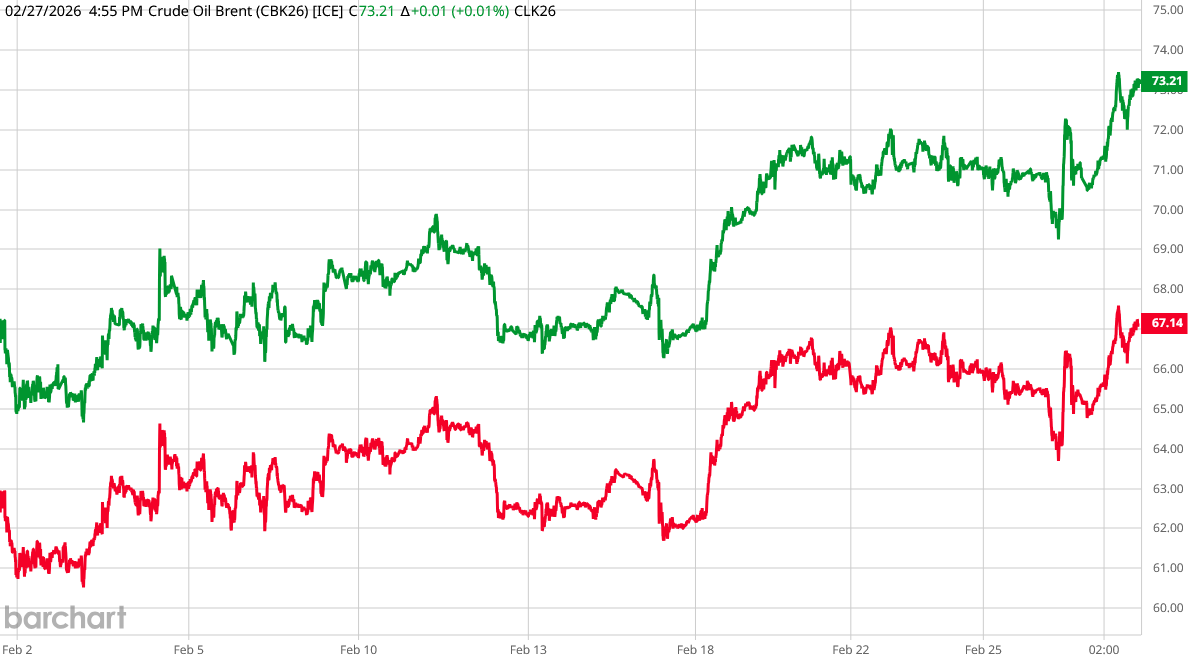

While it scarcely needs be said that energy price inflation is not desirable, March is going to be a month with severe energy price inflation. The surges in benchmark crude prices alone have made that all but inevitable. In March we should not be surprised to see every energy price component surging to the degree fuel oil did in February.

Still, with fuel oil being the only component with significant inflation for the month, we can fairly say that, overall, food and energy price inflation was relatively muted and even calm. Before war broke out, there was simply not a lot of either food or energy price inflation.

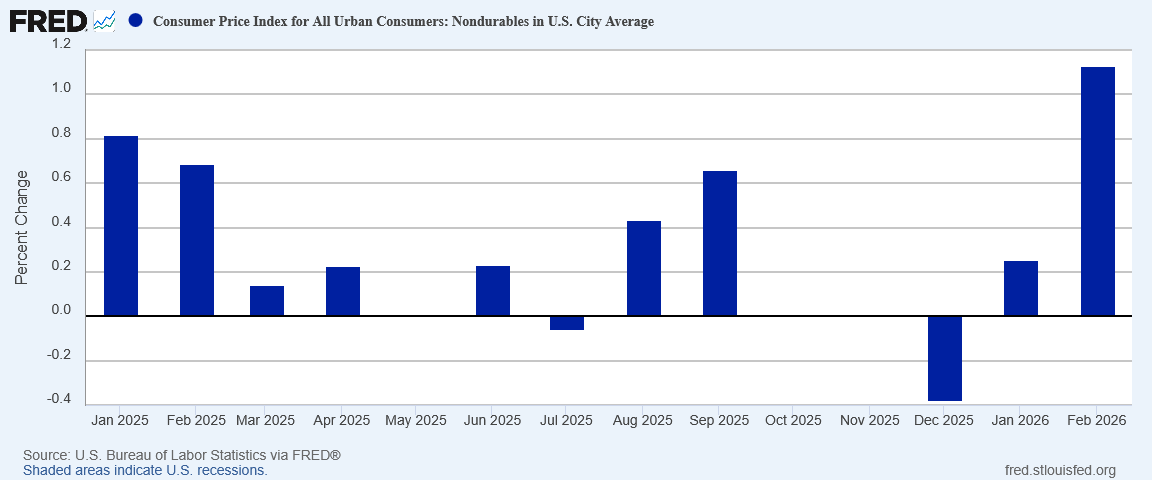

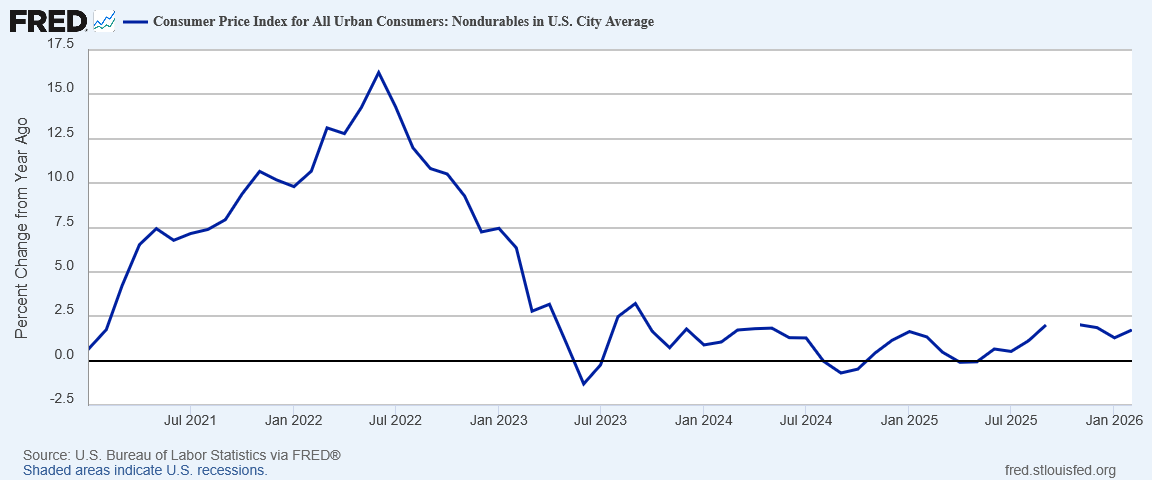

The irony of Politico making their headline about food and energy is that nondurable goods printed the hottest inflation of all for February, rising 1.1% month on month.

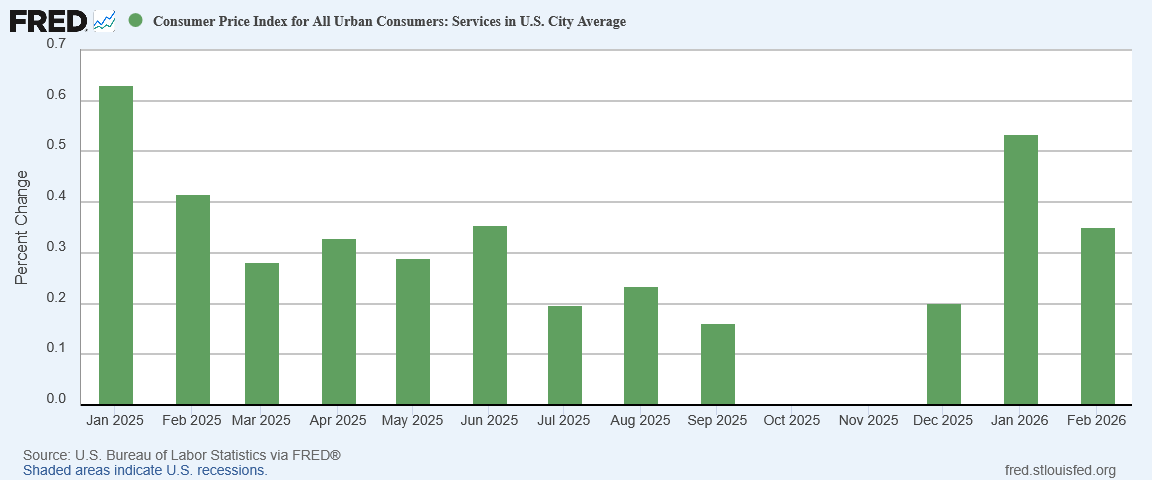

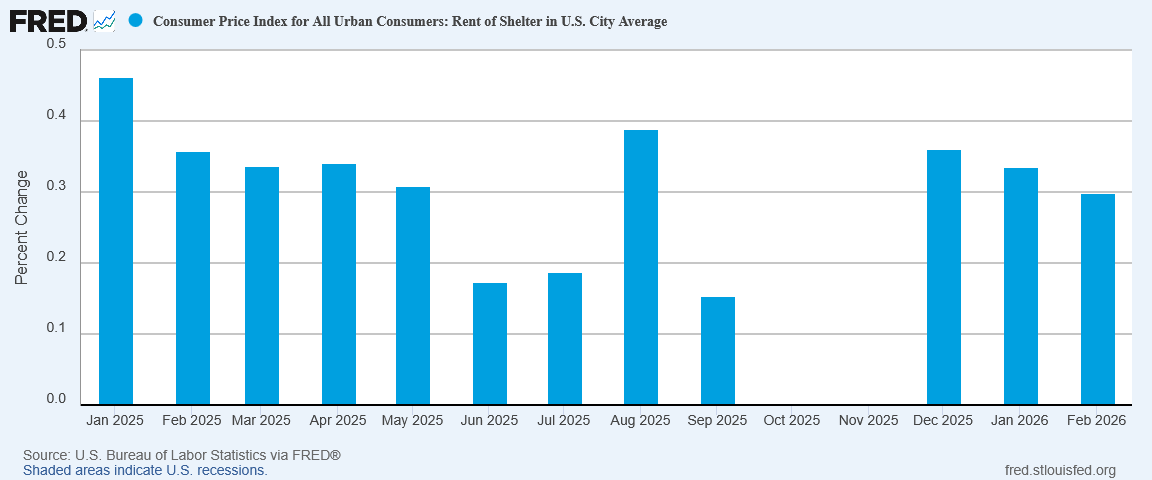

This marks the third consecutive month of disinflation for shelter pricing.

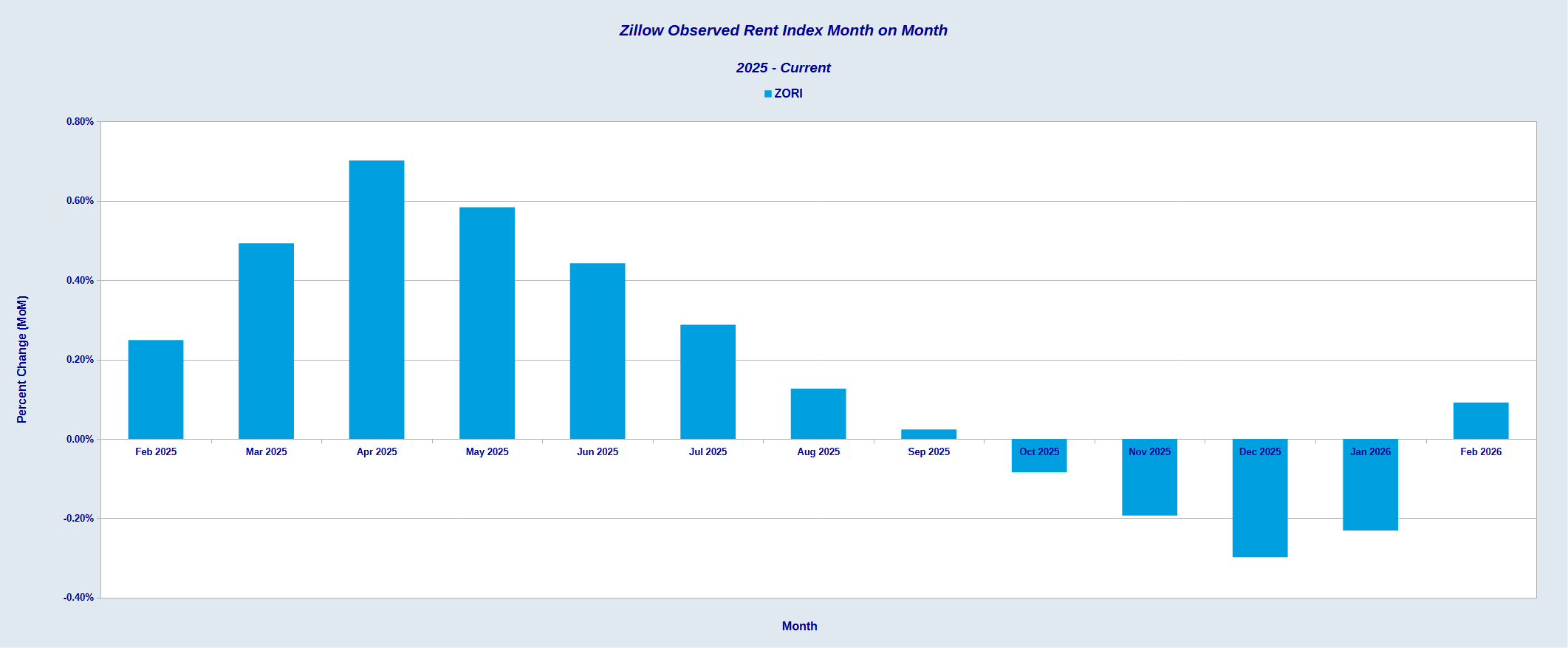

We should not expect that to remain the trend, however. The more forward looking Zillow Observed Rent Index charted an incremental uptick for shelter pricing, after printing deflation for the previous four month.

While nondurables posted a significant inflation bump month on month, the rest of core inflation performed exactly as expected. Across the board, inflation is simply not showing any significant sign of heating up.

Because corporate media is persisting with their “muh tariffs” balderdash, once again it must be pointed out that overall consumer behavior is still not reflecting any significant impact from tariffs.

Indexed, both the advanced estimate and the retail estimate showed the most significant uptick in sales was for building materials—a sign which may augur well for the construction sector in coming months.

Retail Sales Estimates Indexed

There simply is no support in the broad data for a significant inflationary effect attributable to President Trump’s tariffs.

Tariffs are an inflationary price pressure. That much is a given just by virtue of what a tariff is. However, that inflationary price pressure has not proven to be highly influential for consumer prices overall.

With the inflationary impulses seen in the Producer Price Index demonstrably not coming through to the Consumer Price Index, we must be skeptical about any individual inflationary impulse or price pressure percolating through the Consumer Price Index to print as higher inflation month on month or year on year.

Corporate media is clearly disappointed that prices have not risen outrageously in the year Donald Trump has been in the Oval Office.

Corporate media will undoubtedly take perverse pleasure in the hotter inflation print that is almost sure to come next month, as the impact of Operation Epic Fury on oil prices especially takes hold.

At the same time, we should be mindful that February is not March. The inflation that is sure to come has not yet arrived.

Tariffs have not been a primary inflation factor.

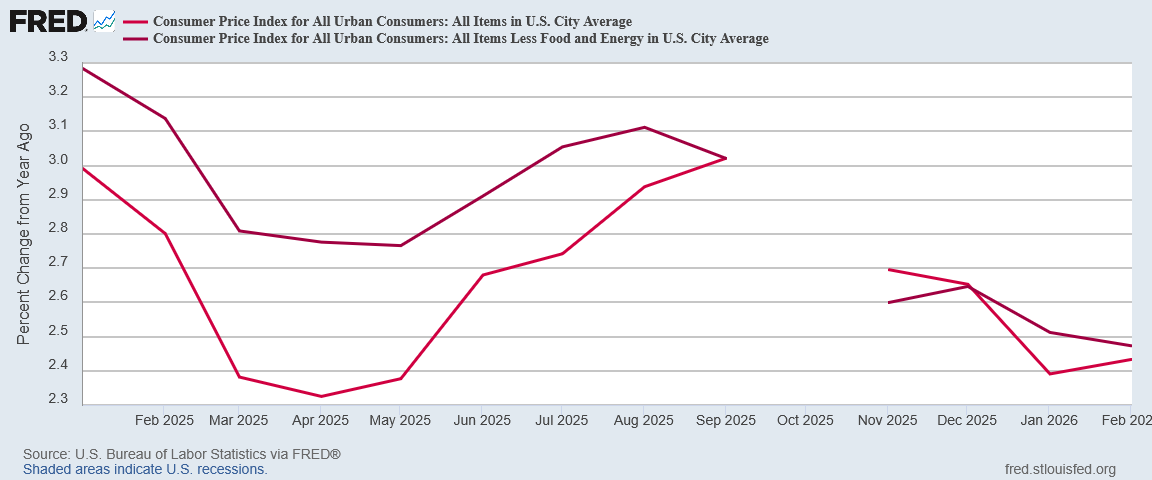

Year on year, inflation has been cooling steadily since August, and while the war with Iran is sure to break that trend, it surely says something about the state of consumer price inflation that it took a war to break the disinflationary trend.

While in theory PPI signals may take a couple of months to materialize, the prevailing presumption among most corporate media is that the PPI is a leading indicator for the CPI. By all accounts, the inflation print we saw in the PPI last month should have been reflected in the CPI data this month. Thus far, the inflation data has not transmitted an inflation impulse from the PPI to the CPI.

As the apocryphal Einstein quote goes, “in theory, theory and reality are the same. In reality, theory and reality are different.”

In theory, tariffs are a primary contributor to consumer price inflation.

In theory, inflation surges in the PPI show up in the CPI in the following month or two.

In reality, tariffs have not had significant impact on consumer price inflation.

In reality, the inflation impulses in the PPI have not percolated through to the CPI.

No matter what theory says will happen, when reality does not show that happening, reality triumphs over theory. It must and it will, every time.

No matter how much corporate media says “muh tariffs” will produce inflation, when reality does not show inflation, the “muh tariffs” narrative stands discredited and debunked. It must and it will, every time.

The reality of consumer price inflation is that, despite all the fear-mongering and pearl-clutching of corporate media, President Trump’s policies have not produced significant consumer price inflation. His tariffs and trade policies will produce their network effects, but broad consumer price inflation has not numbered among them.

The war in Iran is sure to produce a significant uptick in consumer price inflation. Given the lack of inflation to date under Donald Trump, the war in Iran is sure to be the only reason we see a significant uptick in consumer price inflation in March.

That likelihood by itself stands as a backhanded tribute to Donald Trump’s economic policies thus far. War is the only one of President Trump’s policies that is likely to produce notable inflation. All of Trump’s other policies have proven to be anything but inflationary.

Corporate media will not be pleased it took a war to bring back inflation into the US economy. Most consumers will be quite pleased—and should be.

If this story gave you real value, help me keep going. All Facts Matter is powered by readers who believe facts should stand on their own. Your subscription makes that possible.

“No matter how much corporate media says “muh tariffs” will produce inflation, when reality does not show inflation, the “muh tariffs” narrative stands discredited and debunked. It must and it will, every time.”

Corporate media continues to destroy its own credibility. Every sane person knows that an adult must admit when he is wrong, or his judgment loses credibility. Corporate media now deserves to fail!

Another explanation for the uptick in energy and petroleum prices in February is Winter Storm Fern. The dramatic surge in electric power consumption as well as heating fuels drove prices up during the prolonged cold weather.

“No matter how much corporate media says “muh tariffs” will produce inflation, when reality does not show inflation, the “muh tariffs” narrative stands discredited and debunked. It must and it will, every time.”

Corporate media continues to destroy its own credibility. Every sane person knows that an adult must admit when he is wrong, or his judgment loses credibility. Corporate media now deserves to fail!

Another explanation for the uptick in energy and petroleum prices in February is Winter Storm Fern. The dramatic surge in electric power consumption as well as heating fuels drove prices up during the prolonged cold weather.