Inflation Warnings From PPI, But It’s More Complicated Than Tariffs

What We Can Conclude From The Producer Price Index Data

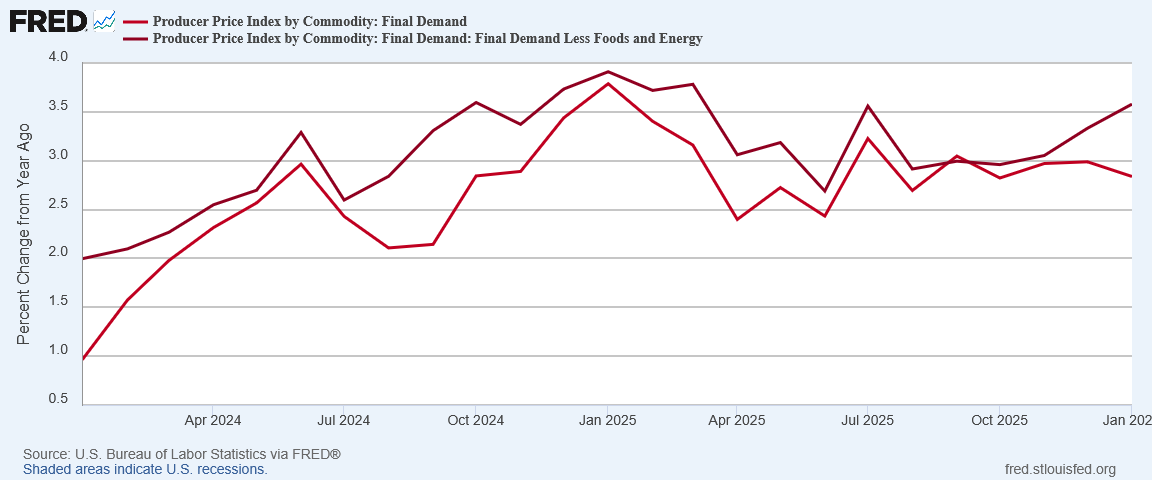

Wholesale prices once again are sending out inflation signals, with the January Producer Price Index printing a hotter than expected 2.9% year on year.

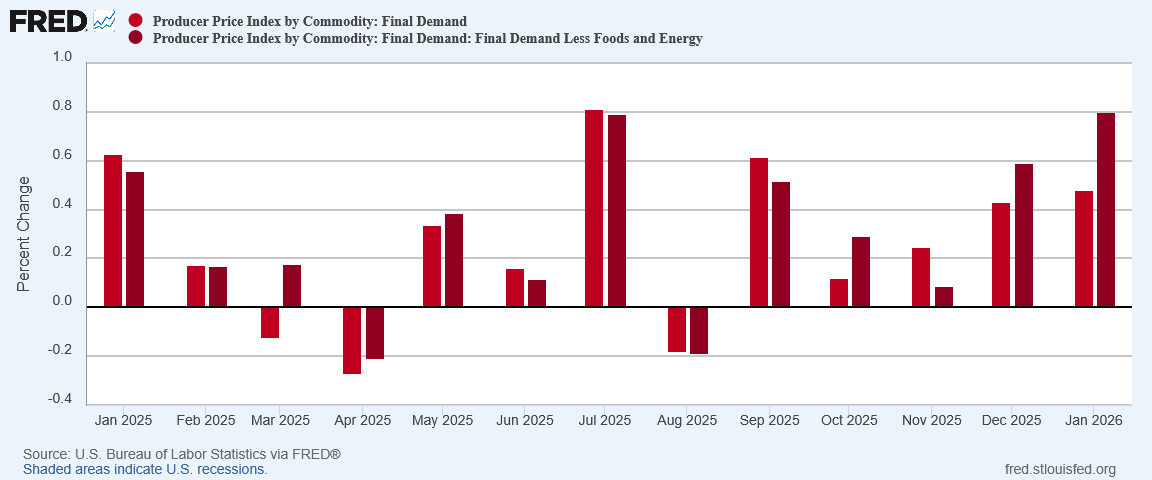

The Producer Price Index for final demand increased 0.5 percent in January, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices advanced 0.4 percent in December 2025 and 0.2 percent in November. (See table A.) On an unadjusted basis, the index for final demand rose 2.9 percent for the 12 months ended January 2026.

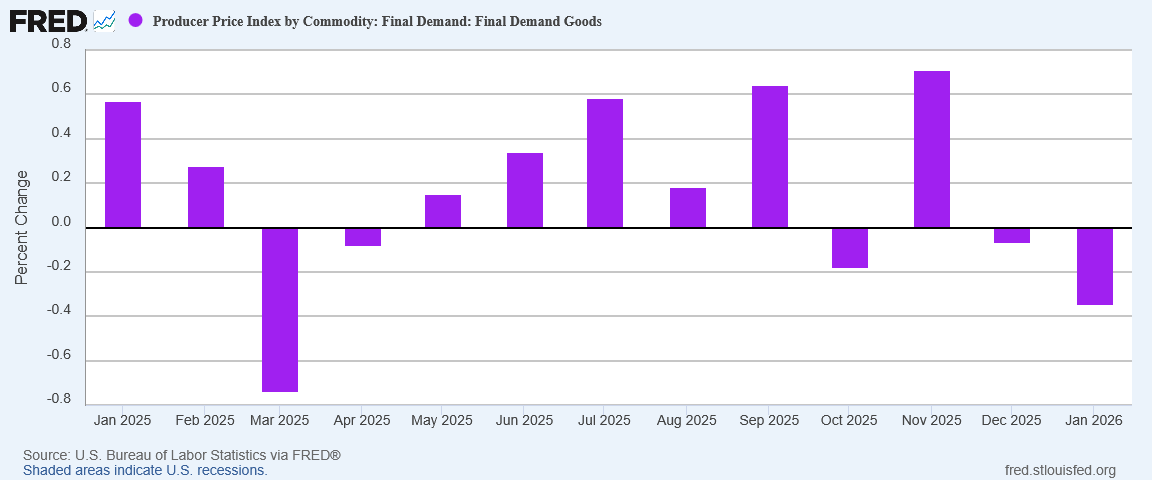

The January increase in prices for final demand can be traced to a 0.8-percent advance in the index for final demand services. In contrast, prices for final demand goods declined 0.3 percent.

Just as was the case for December, corporate media wasted no time in leaping to the ever-reliable “muh tariffs” narrative, this time by trying to actually parse the data.

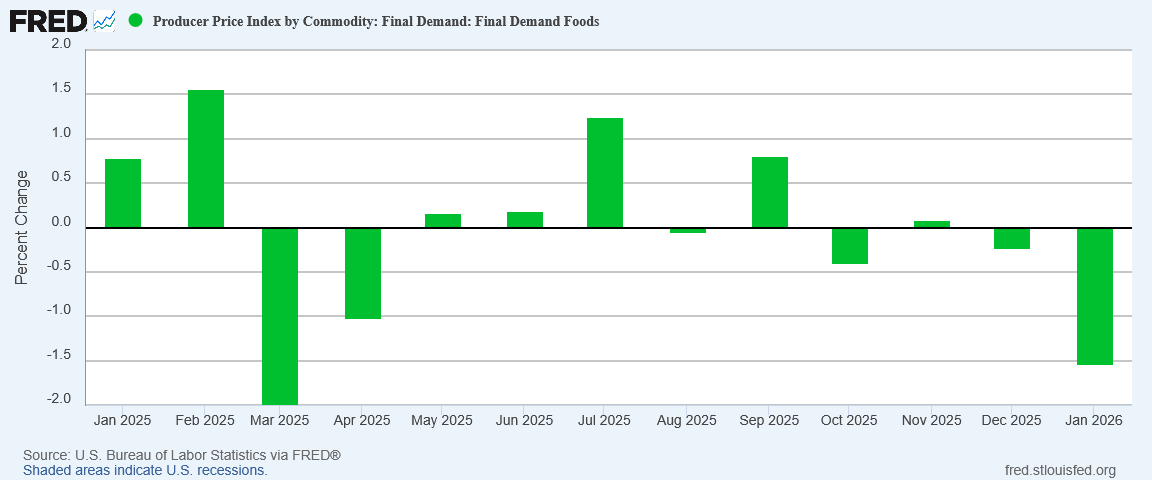

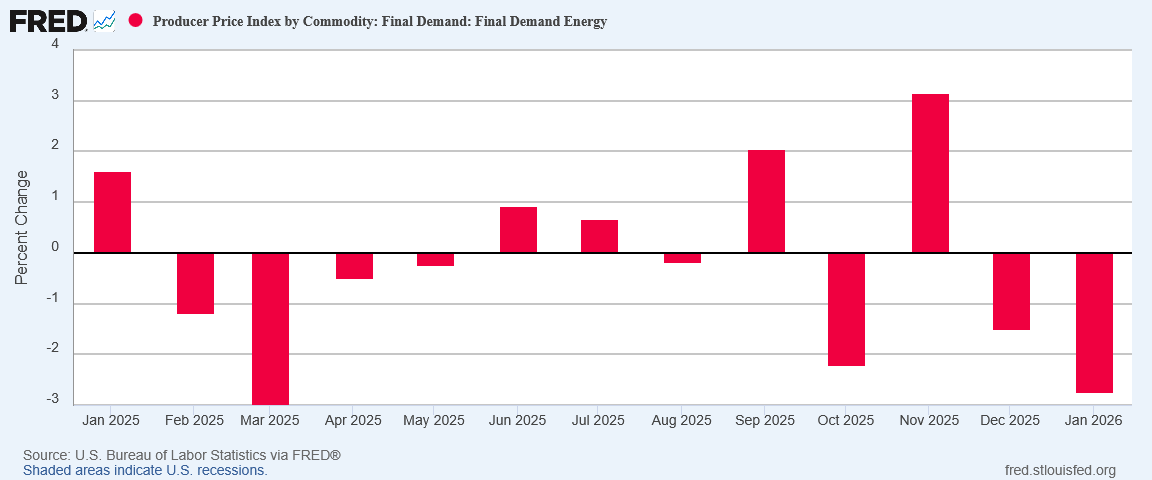

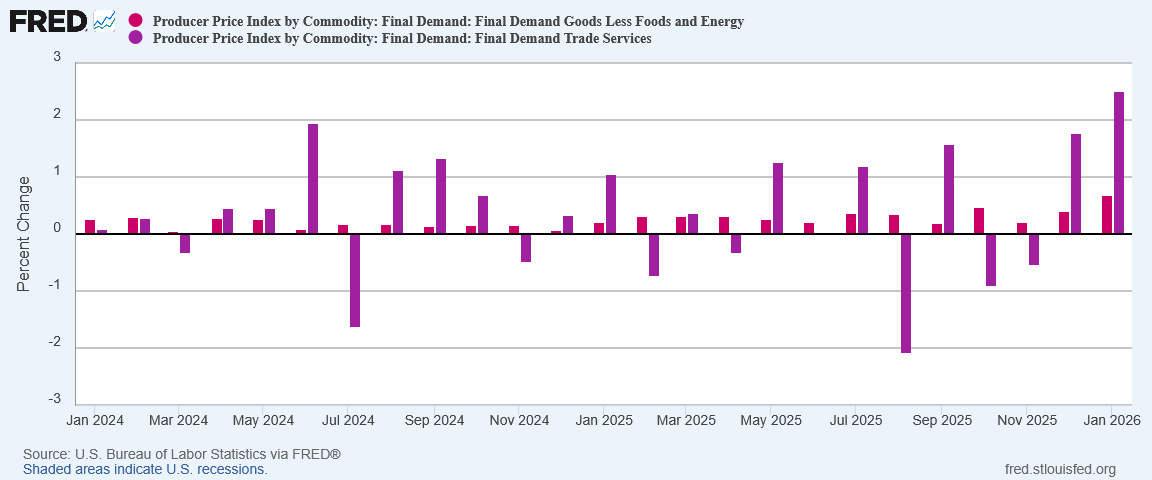

Gas and food prices tumbled during the month; however, those decreases were countered by a sharp increase in “trade services,” a category that measures profit margins for wholesalers and retailers.

Trade services can be highly volatile on a monthly basis and economists have closely watched this category during the past year as it could serve as a signal for whether businesses are absorbing the higher costs US importers are paying for tariffs.

Alas for the Most Busted Name in Fake News, the ever-reliable “muh tariffs” is still ever-reliably wrong. Yes, prices are up, and yes there are even inflation signals in the PPI data. No, we cannot conclude from them that tariffs are to blame.

What can we conclude? Let us peel back the layers and find out!

More “Muh Tariffs” Nonsense

As a rule, one must be wary of news media headlines. Of necessity, headlines are meant to attract attention—and that includes mine. The impulse to “spice up” the narrative in the headline can be compelling, and it is an impulse corporate media rarely tries to resist, as CNN’s headline for its PPI write up demonstrates.

As noted above, CNN pointed to “trade services” and pretended that made the case for tariffs being the culprit.

However, when even the more finance-oriented Bloomberg declines to accentuate tariffs, we have to question the accuracy of the “muh tariffs” narrative.

Buried rather farther down in the Bloomberg story, there is even the concession that tariffs likely are not the culprit.

And while tariffs have put some upward pressure on consumer prices, companies largely haven’t hiked prices as much as economists once feared. Data out earlier this month showed a key gauge of inflation was fairly mild in January, defying concerns of a bigger jump.

I will reiterate what I said last month on this topic: “It’s complicated”.

Ultimately, the TLDR on what is driving factory gate inflation is almost always going to be “it’s complicated”.

Tariffs certainly can be a factor in pushing up prices, and are always an inflationary pressure on prices. Geopolitical tensions over Greenland, Venezuela, China, Ukraine and Iran can also be inflationary pressures. Political and non-tariff trade disputes can likewise be inflationary pressures.

There are simply too many forces pushing prices both up and down to say “inflation is due to this” or “inflation is due to that.”

Hyperbole may be a natural tendency for headlines, but that also means headlines should be distrusted as a general rule. (And yes, that includes the ones I use here on All Facts Matter)

PPI Is Printing Inflation Warnings

While skepticism over headlines is always warranted, the reality of the PPI data is that it is printing inflation warnings for January.

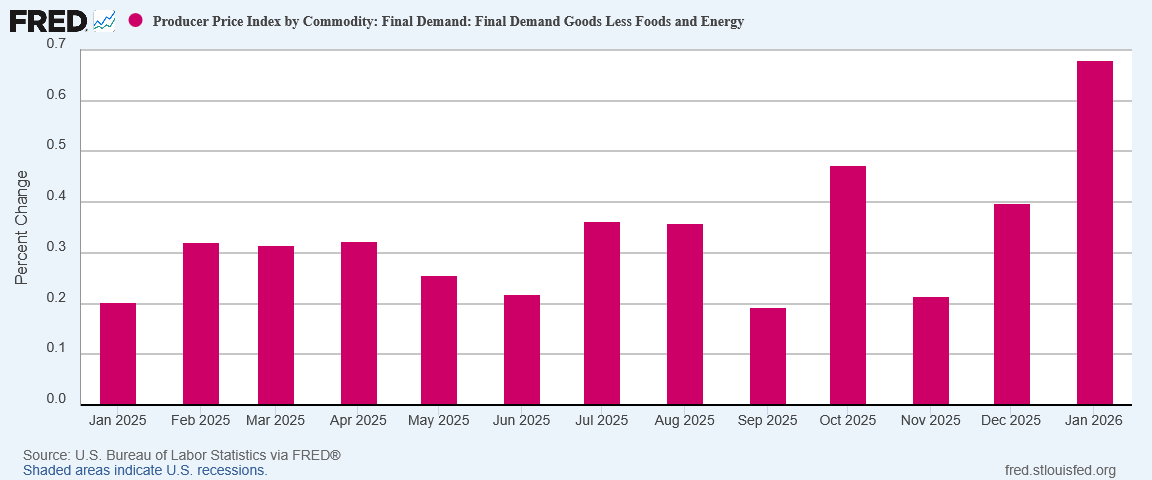

Although the headline factory gate inflation number actually declined year on year, from 3.0% to 2.9%, the core metric with food and energy left out actually rose.

Even month on month, the core inflation metric rose significantly higher than the headline figure for the second month in a row.

There is indisputably an inflation signal in the data.

However, that inflation signal is not across the board. For the second month in a row, food printed outright deflation.

Remarkably, so did energy.

This is remarkable because January was a month when market oil prices—a major and obvious factor in energy prices—generally rose.

No matter what else happens with factory gate prices overall, we should definitely anticipate future energy price inflation in the PPI simply so that the PPI can absorb the inflationary impulse from rising oil prices.

Moving into the core price elements, for the second month in a row goods prices printed outright deflation.

While we can point to this as a rebuttal to the “muh tariffs” narrative, we need to do so carefully, because when we unpack the deflating food and energy prices, goods prices actually rose significantly month on month.

Wait, comes the question, if goods prices less food and energy are rising, why wouldn’t we ascribe it to tariffs?

The answer is to remember what I said at the top: “It’s complicated”. Tariffs are an indisputable inflationary pressure for both consumer and factory gate prices, by they are by no means the only such pressure. Just because core goods prices rose does not allow us to conclude that tariffs are to blame.

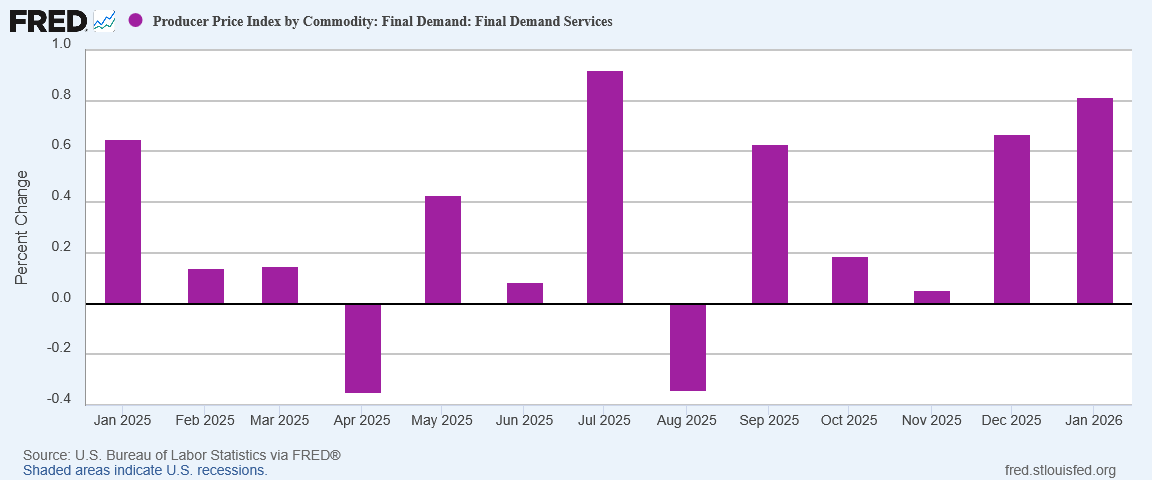

One complicating factor is that service price inflation has also been heating up.

Remember, services are not tariffed. If service prices are rising we are looking at inflationary pressure besides tariffs.

Not Every Price Rise Comes From Tariffs

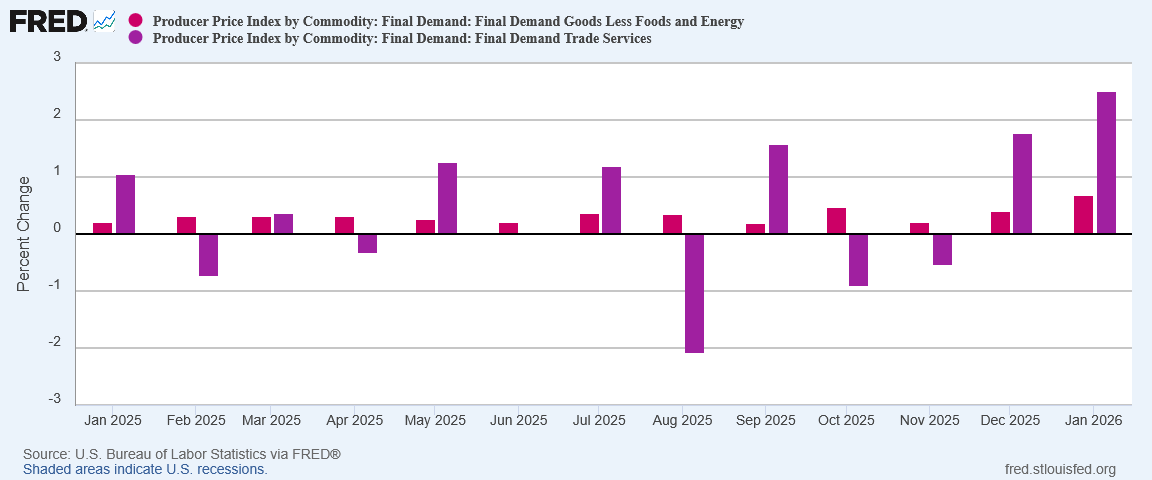

A second criticism comes from the canard of pointing to “trade services” as a potential indicator of tariff-driven inflation.

The first problem with that comes when we look at the behavior of trade service prices against core goods prices. Straight away we see that trade services are themselves particularly volatile.

Moreover, trade services were in outright deflation in August and again in October and November. The Liberation Day tariffs were announced in April. If tariffs were the culprit for the rise in trade service prices, we should not have seen trade service price deflation during the summer—but we did.

Additionally, trade service prices have a history of surging even without tariffs, which is easily seen when we expand the timeline to cover the past two years.

If tariffs are signaled by rising trade service prices, what catalyzed the surge in trade service price inflation during the summer of 2024? Donald Trump’s tariffs were not even proposed policy at that point.

Trade service prices are signalling hotter inflation, but their historic volatility does not permit us to look at them and consider the “muh tariffs” narrative proven.

Producer Price Inflation Is Not Consumer Price Inflation

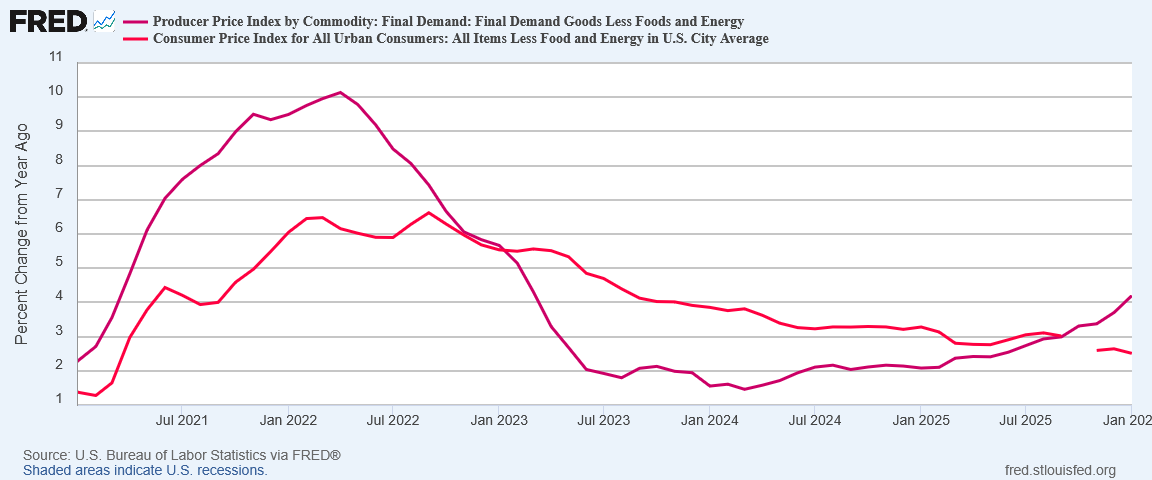

The most important reason to discount the “muh tariffs” narrative on inflation is that, despite the signals from the PPI, consumer price inflation remains notable chiefly for its absence.

What I noted last month about the quality of the PPI inflation signal remains very much the case, and even more so when we add the January data.

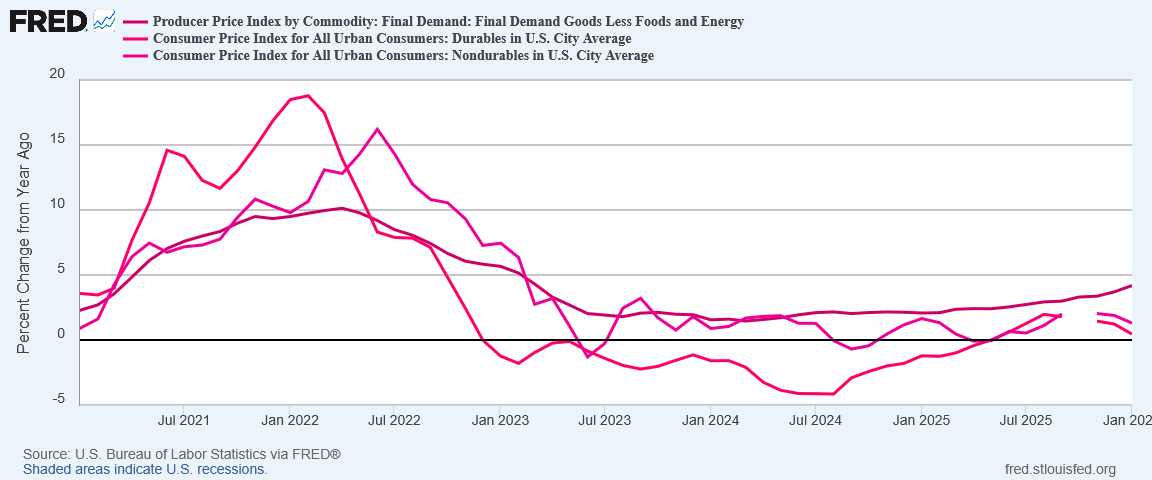

While there was a correlation between year on year consumer price inflation and factory gate inflation for goods immediately after the COVID Pandemic Panic and during the 2022 hyperinflation cycle, after 2022 there has been more divergence, with consumer prices dipping into deflation year on year while producer prices stabilizing and then trending up.

In January, the Producer Price Index year on year deviated even more from the CPI for both durable and non-durable goods.

While the historical presumption has been that the Producer Price Index acts as a leading indicator for the Consumer Price Index, that presumption is challenged considerably by the post-COVID data, and in particular by the behavior of both indices after the 2022 hyperinflation cycle.

The unalterable reality of consumer prices is that if they are not rising, tariffs cannot be contributing to consumer price inflation. It is mathematically impossible for it to be otherwise.

The unalterable reality of both indices is that, year on year, while core producer price inflation has been rising, core consumer price inflation has not.

Even with the disruption in CPI data from the Silly Schumer Shutdown, we are still presented with data which completely contradicts the presumption that the PPI is a leading indicator for the CPI.

Inflation, But Not From Tariffs

What we are seeing in factory gate prices is inflationary pressures which are quite demonstrably not being passed on to the customer.

There are two broad hypotheses we can propose for this phenomenon:

Suppliers are compelled to acknowledge that previous profit margins have included a measure of economic rents, which market conditions are forcing suppliers to now surrender by absorbing cost increases.

Suppliers are anticipating that the current inflationary pressures are actually transitory and will subside again. Maintaining current prices is therefore a defensive measure to preserve market share.

Neither scenario makes tariffs a principal driver of consumer price inflation. We cannot hypothesize that suppliers will view Trump’s tariffs as transitory because Trump’s tariffs from his first term were not transitory. One of the major criticisms of the recent Supreme Court ruling on the Liberation Day tariffs is that Joe Biden doubled down on Trump’s first term tariffs—hardly a rejection of the premise that Presidents can invoke tariffs.

This is why we must remember that every exploration of the contribution of specific inflationary pressures towards overall inflation is always going to be complicated. There is never a situation where a single inflationary pressure operates in isolation. The pressures which drive prices up and the pressures which drive prices down always are acting against each other.

No matter what data we examine, we are always compelled to recognize that the relationship between inflationary pressures and inflation is not a linear relationship but a differential one. Overall inflation for both producer and consumer prices is always going to be the resolution of all such pressures.

At present, even for producer prices, tariffs are just not a primary pressure pushing up prices. The data simply does not get us there.

Your insights and reasoning are endlessly impressive, Peter. And you can out-argue anyone on the planet.

The great news for a Monday morning is that prices of food and energy are down. I’ll take it!