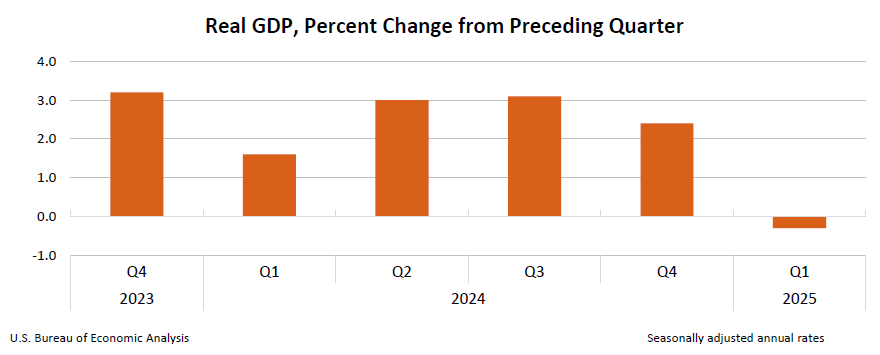

Real gross domestic product (GDP) decreased at an annual rate of 0.3 percent in the first quarter of 2025 (January, February, and March), according to the advance estimate released by the U.S. Bureau of Economic Analysis. In the fourth quarter of 2024, real GDP increased 2.4 percent.

If we stop reading at just that first sentence, then the headlines we see in corporate media about the advance estimate make perfect sense. Confirmation bias tells us that all is not well in the US economy, and that President Trump has made a complete mess of things.

And we would be wrong.

As I have said many times before, we should never stop with just the consideration of the top-level summary numbers, We should never be content with a narrative that does not delve more deeply into the economic numbers. We should never accept an analysis that does not explore the data in detail.

There is both good and bad in the economic data. There are reasons to smile and reasons to frown. We owe it to ourselves to look at all of those reasons. We must look at all of those reasons if we want to understand this nation’s economic circumstances.

Join a growing community that values truth over noise. Become a paid subscriber today!

Not Everything Shrank

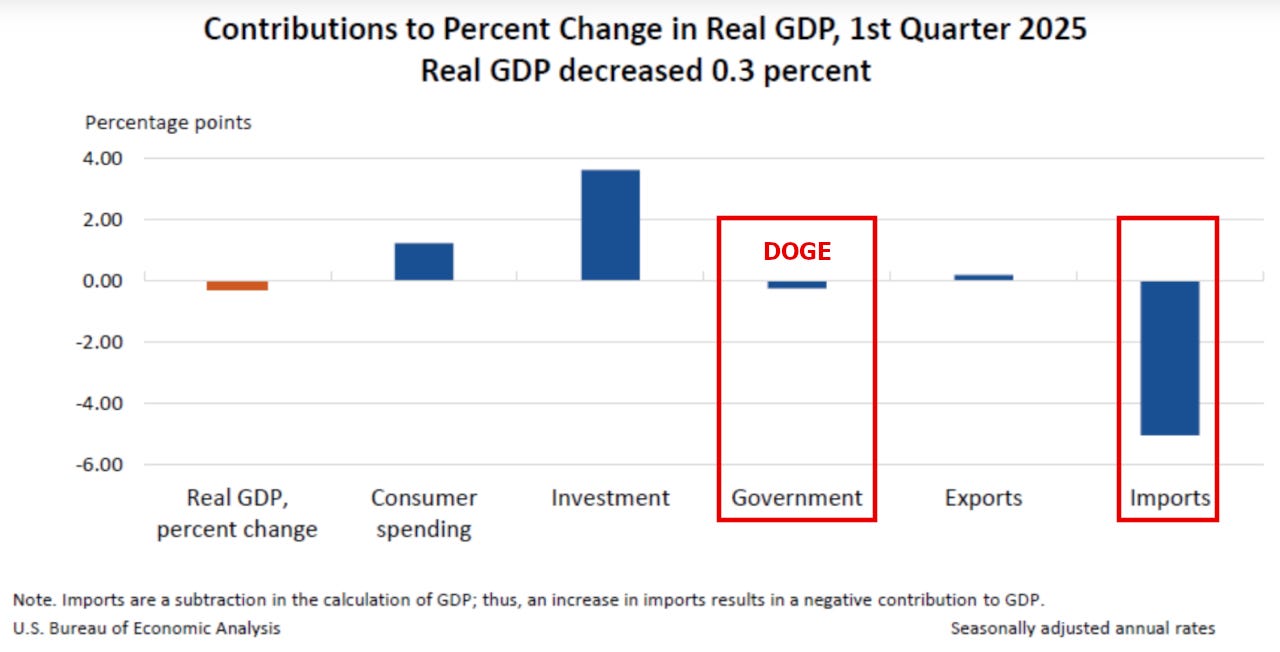

The first problem with looking at just the top level number is that not every part of the US economy contracted during the first quarter.

Consumer spending grew in real terms.

Investment grew.

Exports grew.

What didn’t grow? Government spending.

Between a reduction in government spending and a surge in imports—imports are assessed as a reduction in overall GDP—the growth observed in other sectors was overwhelmed, and in the aggregate GDP has been calculated as having dropped 0.3pp from the fourth quarter of 2024.

We can quite plausibly say that the economy contracted in part because DOGE has been doing what was asked of them. Trimming back questionable government spending means trimming back government spending. By definition DOGE’s activities were always going to present as a reduction in overall GDP. Every reduction in government spending is also a reduction in GDP.

Nor do we have to guess why there was a surge in imports. President Trump has been talking about raising tariffs and taking other steps to address unfair trade practices since he was on the campaign trail last summer. President Trump has repeatedly threatened multiple nations with tariff hikes, and quite naturally importers front loaded as much of their overseas imports as they could in order to minimize their exposure to Trump’s tariffs as they become enacted.

The rush to import as much as possible ahead of the imposition of President Trump’s “Liberation Day” tariffs has unquestionably skewed net exports, and we can see just by looking at the BEA’s own charts that the import surge shows up in the GDP calculation as such a large negative number that it pulls down the entire GDP calculation.

If we set aside net exports, we are left with an economy that did manage to grow during the first quarter.

Readers will recall that I have long argued that the US economy is in a long-term “jobs recession”. The employment numbers have not done anything to change my mind on that point, but if we are focusing not on jobs but on value of goods and services produced, it is foolish to ignore the increase in at least some portions of that data. Weaknesses in employment do not erase observed strengths in output.

CNN wastes no time in taking President Trump to the proverbial woodshed.

The US economy just had its worst quarter since 2022 as President Donald Trump’s significant policy changes unnerved consumers and businesses.

Gross domestic product, which measures all the goods and services produced in the economy, registered at an annualized rate of -0.3% in the first quarter, the Commerce Department said Wednesday.

Ironically, even CNN can’t ignore the underlying detail, and thus has to contradict itself even within its own story.

The economy’s decline in the beginning of the year was driven by a wider trade deficit — a result of Americans front-running purchases to beat Trump’s tariffs — and cutbacks in government spending, according to a release. Imports skyrocketed from -1.9% in the fourth quarter to 41.3% in the first three months of the year. Meanwhile, exports registered at a 1.8% rate.

When imports exceed exports, that subtracts from GDP and that was by far the biggest drag on growth in the first quarter. The difference between imports and exports subtracted from GDP by the most on records going back to 1947.

This highlights the essential contradiction in the corporate media reporting on the BEA numbers. If a surge in imports is a net negative for the economy—if importing is a reduction in economic activity—then the front-loading behavior witnessed in the first quarter suggests that the tariffs will function to reduce imports. If tariffs are suppressing what is a net negative for the economy, the end results of tariffs arguably should be a net positive for the economy.

And CNN admits that if we exclude that difference between imports and exports from the overall economic assessment, we have positive GDP growth during the first quarter.

The U.S. economy contracted in the first three months of 2025, fueling recession fears at the start of President Donald Trump’s second term in office as he wages a potentially costly trade war.

Gross domestic product, a sum of all the goods and services produced from January through March, fell at a 0.3% annualized pace, according to a Commerce Department report Wednesday adjusted for seasonal factors and inflation. This was the first quarter of negative growth since Q1 of 2022.

Of course, CNBC also trips over the basic math surrounding exports, imports, and the presumed “contraction” of the American economy.

Indeed, imports soared 41.3% for the quarter, driven by a 50.9% increase in goods. Imports subtract from GDP, so the contraction in growth may not be viewed as negatively given the potential for the trend to reverse in subsequent quarters. Imports took more than 5 percentage points off the headline reading. Exports rose 1.8%.

“Maybe some of this negativity is due to a rush to bring in imports before the tariffs go up, but there is simply no way for policy advisors to sugar-coat this. Growth has simply vanished,” said Chris Rupkey, chief economist at Fwdbonds.

Yet even within CNBC’s own article, equating the surge of imports with a disappearance of growth is an irrational and illogical assertion on a good day. If the economy contracted 0.3%, and imports are a 5% reduction in the economy, then we again have an acknowledgement that, sans imports, there was economic growth.

When even the BEA’s own charts show economic growth outside of net exports, saying that “Growth has simply vanished” is an absurd thing to say. There has been some growth, albeit perhaps not at the levels Wall Street desired or hoped for.

A logistical consideration makes Wednesday’s report difficult to interpret: Imports subtract from the Commerce Department’s calculation of GDP, since they represent spending on foreign-made goods and services.

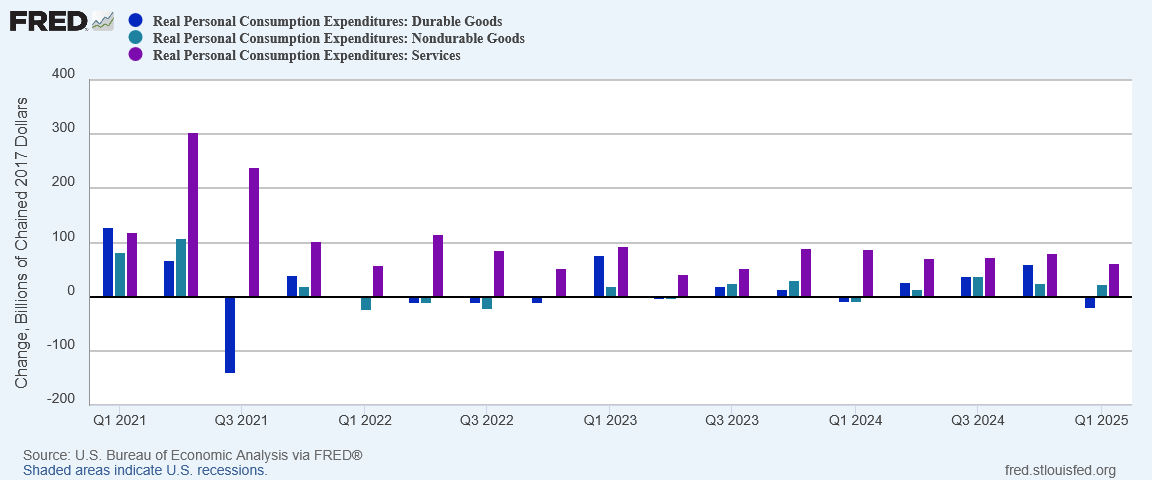

A measure of consumer and business spending that gauges underlying demand in the economy, final sales to private domestic purchasers, rose at a 3% annual rate.

Consumer spending rose at a 1.8% annual rate, slowing sharply from 4% in the final quarter of 2024. Consumers drive the U.S. economy.

Once again, but for imports, the economy grew overall in the first quarter, although not by as much as analysts would like.

What Did Grow

What did grow in the US economy during the first quarter?

For starters, investment, and especially nonresidential fixed investment.

If we delve further into non-residential fixed investment we see there was a large surge in equipment investment. Businesses plowed a lot of money into the tools to produce goods and deliver services.

Contrary to the assertions of corporate media, the increase in equipment investment is in addition to the growth in private inventories—which are goods held for resale.

During the first quarter, there was significant expansion in both equipment investment and private inventories.

It is a near certainty that much of this surge in both investment and private inventory build was the consequence of businesses attempting to front-run the Liberation Day tariffs. Purchases that would otherwise have been delayed were brought forward into the first quarter to avoid the tariff hikes.

Accordingly, we should expect in the second quarter to see a drop-off in both investment and private inventory builds. Front-running does not represent an increase in aggregate demand, merely an acceleration of when that demand is realized.

Note that exports were marginally negative in the fourth quarter of 2024, so the $11 billion increase in exports in the first quarter of 2025 is very much a welcome change—and is not something that can be considered to be front-running the tariffs, as these are goods America is shipping to the world.

It is also growth, the very thing CNBC claimed did not exist in the first quarter.

While we can and should question the amount of growth that took place in various parts of the economy, we cannot say there was no growth at all. That simply is not an accurate assessment of the economy.

What Didn’t Grow

We should not presume that the economy is growing across the board and all is well. That would be equally inaccurate and dishonest.

We can broadly attribute the drop in federal spending to the work of Elon Musk and DOGE.

We should also remember that because government spending is included in the GDP calculations, any wholesale reduction in government spending is going to show up as a reduction in GDP itself. There is no way to trim out-of-control government spending and not have it negatively impact the GDP numbers quarter on quarter.

We broadly consider trimming wasteful and inefficient spending as a net positive, and so even though the reduction in government spending is also a reduction in GDP, it would not be entirely out of bounds to characterize that as a “good” reduction in GDP.

Still, these are reductions in GDP, and these are reductions in overall economic activity. While there are valid interpretations of these reductions that are fairly benign, we cannot avoid the reality that they are reductions.

Getting Defensive

Was corporate media wrong? Did the economy actually expand in the first quarter rather than contract?

By the numbers, no. Corporate media was not wrong.

By the numbers, when all the parts of the economy are aggregated together, there was a reduction in GDP of 0.3pp quarter on quarter.

All the detail numbers I have mentioned here are part of what gets aggregated together to arrive at that 0.3pp reduction in GDP, and if we are not challenging the accuracy of these detail numbers we do not have a solid basis for challenging the top-level aggregate number.

Taken together, the US economy may be said to have contracted by 0.3pp in the first quarter of 2025.

At the same time, there are significant parts of the economy that are still showing themselves to be relatively healthy and robust. It is a positive economic sign that exports increased in the first quarter despite global concern over President Trump’s tariff policies. It is a positive economic sign that businesses felt the prudent and proactive response to the possibility of tariffs was to accelerate equipment investment into the first quarter, rather than to cancel that investment altogether.

The investment might be accelerated, and that acceleration will have consequences in the second quarter especially, but the investment is still on the books. That’s not a bad thing.

While the economy did contract by 0.3pp in the first quarter, we are better served by viewing the data as signs of an economy that is getting defensive.

Businesses are stockpiling inventory in an effort to buffer likely cost effects of the Liberation Day tariffs.

At the same time, businesses are plowing additional money into equipment investment, which implies efforts to expand domestic production capacities. Even if that equipment investment involves initially purchasing items from overseas, if domestic production capacity is expanded, then the future economic output will be increased. That is the ideal for all investment—to push the production boundaries outward.

Is the contraction a cause for concern about the future of the US economy? Absolutely. The magnitude of inventory stockpiling itself should be alarming. That could prove to be an overreaction in the face of the Liberation Day tariffs, or it could be an indication that the tariffs are about to go very wrong for the US economy.

The Trump Administration is undeniably committed to the narrative that the tariffs will produce good results for the economy, but we should not conflate those good intentions with what will be the eventual outcomes. We do not yet know how the tariffs will play out for the US economy. The concerns driving the inventory builds are hardly baseless, even if they should prove to be exaggerated.

Still, the economic news is not all bad. There is growth, and there are even areas of possible economic strength. If the Trump Administration’s trade negotiations prove successful the economy could quite easily rebound from a relatively minor contraction to enjoy several quarters of growth and expansion.

That is the best case scenario for the economy but it is no less probable at this point than the worst case. It might even prove to be more probable.

The corporate media is, once again, going out of its way to exaggerate the negatives and downplay the positives within the US economy. Their rabid anti-Trump bias corrupts all of their thinking even on issues that should be politically neutral, such as the economy.

The prudent response is not to get caught up in what corporate media says, or what Wall Street analysts think.

Look to the data to understand the condition of the economy, and watch the trends within the data to get a sense of where things are headed.

Ignore the corporate media headlines. Whatever details they may actually get right, it is already certain the headlines will be wrong.

Join a growing community that values truth over noise. Become a paid subscriber today!

Great analysis. Something msm sorely lacks/omits/hides/purposely misleads (take your pick).

Can you send a copy of this to Jessica Tarlov? Please and thank you.