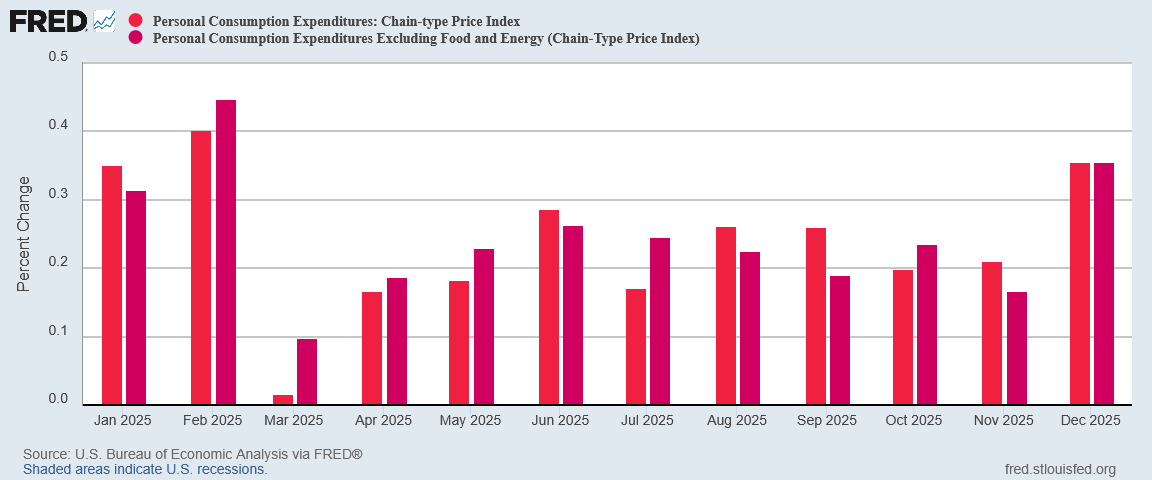

From the preceding month, the PCE price index for December increased 0.4 percent. Excluding food and energy, the PCE price index also increased 0.4 percent.

From the same month one year ago, the PCE price index for December increased 2.9 percent. Excluding food and energy, the PCE price index increased 3.0 percent from one year ago.

Corporate media, true to propagandistic form, seized on inflation’s rise, once more largely ignoring the underlying detail and the ramifications of that detail. Headline inflation rose, so naturally the corporate media headlines were that inflation rose.

Yet the price rises are not the real concern in the December report. There were also disquieting shifts in personal income and personal consumption, shifts which could signal not inflation, but deflation or stagflation.

The Personal Income and Outlays report does not sound any alarms on either inflation or deflation, but it does present a number of warning signals for both.

The report ends 2025 on a cautionary note, and opens 2026 with a return to skepticism rather than the surge of optimism we have seen recently.

Every article I publish takes time, care, and independence. A paid subscription fuels that work and shields it from outside pressure. If you’re able, join me today.

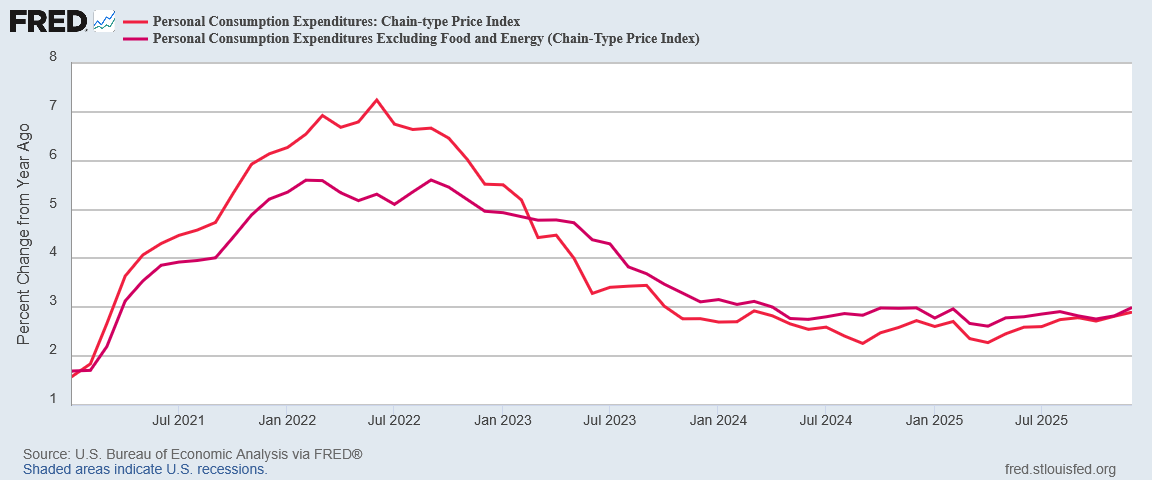

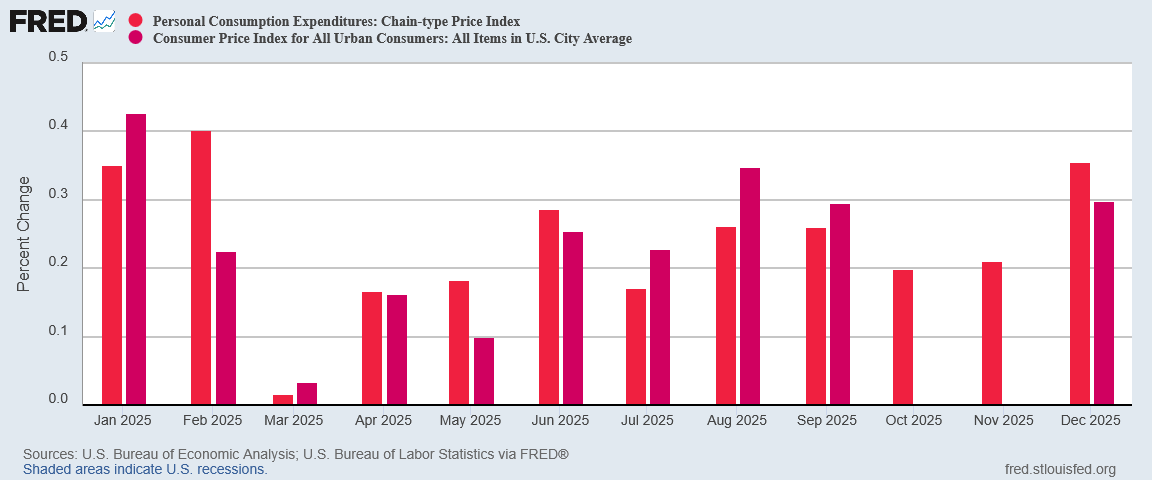

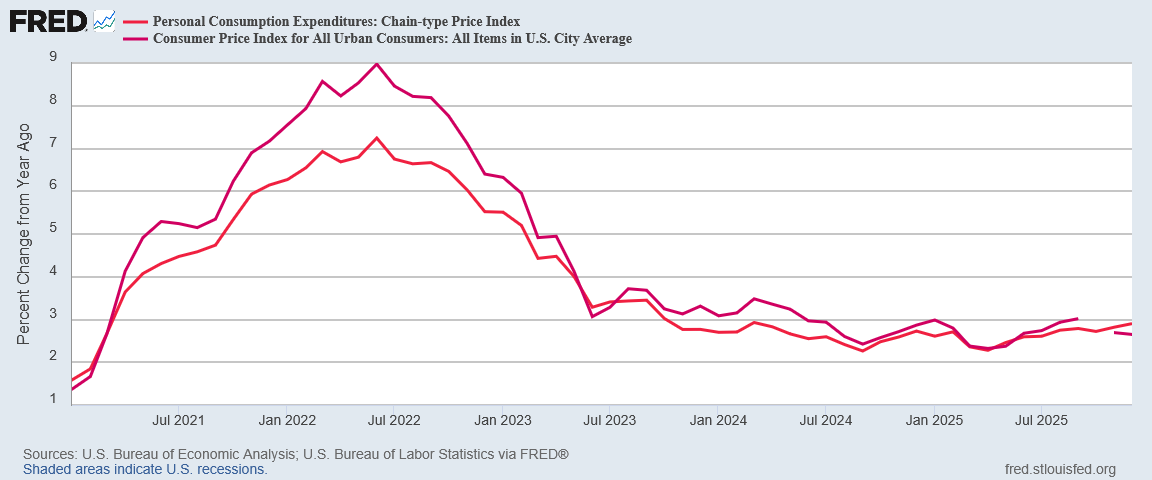

PCEPI Rises When CPI Fell

The PCE Price Index rose 2.9% year on year in December, and Core PCEPI rose 3%, the second consecutive year on year increase for both.

Intriguingly, headline PCEPI has been trending up since last spring, while Core PCEPI has been primarily fluctuating and flirting with 3% year on year.

The lack of CPI data for October and November further complicates comparison between the two inflation metrics. Still, even year on year the PCEPI data is diverging from the CPI data somewhat.

While headline CPI has cooled year on year since last summer, headline PCEPI has not.

The differential is too small to be significant on its own, but the deviation extends back into last fall, and so bears ongoing scrutiny. The deviation may prove to be just statistical noise, or it may be a harbinger of something more relevant.

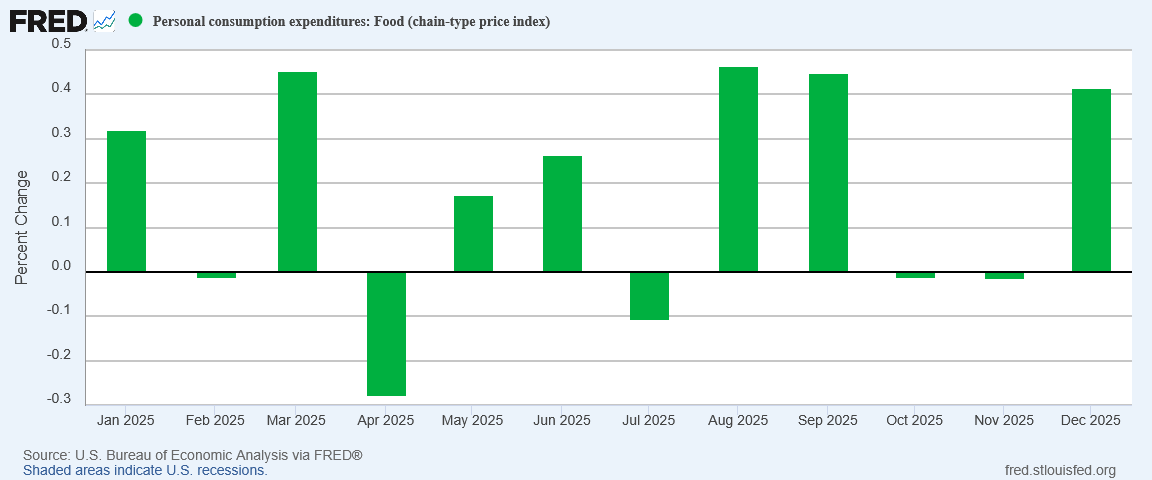

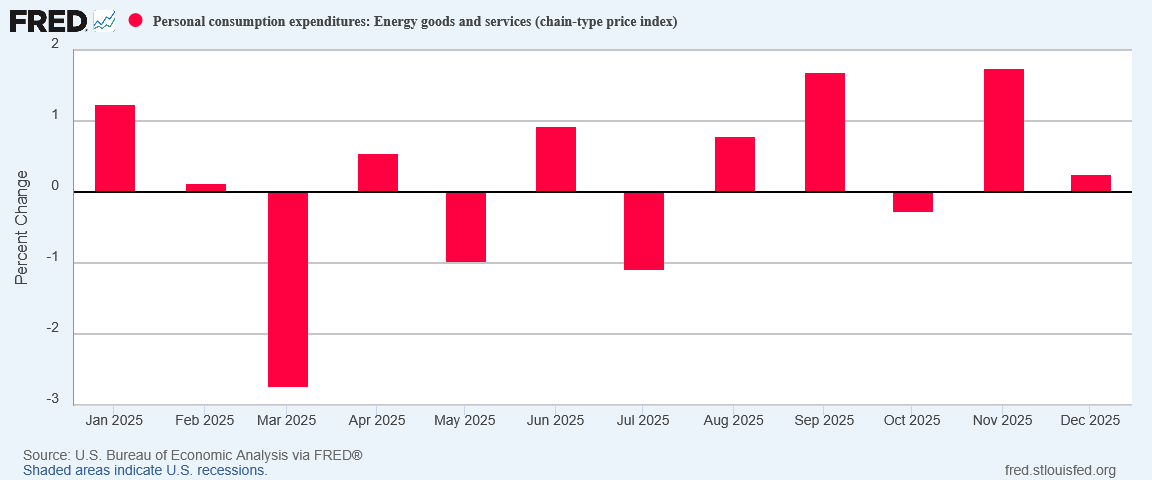

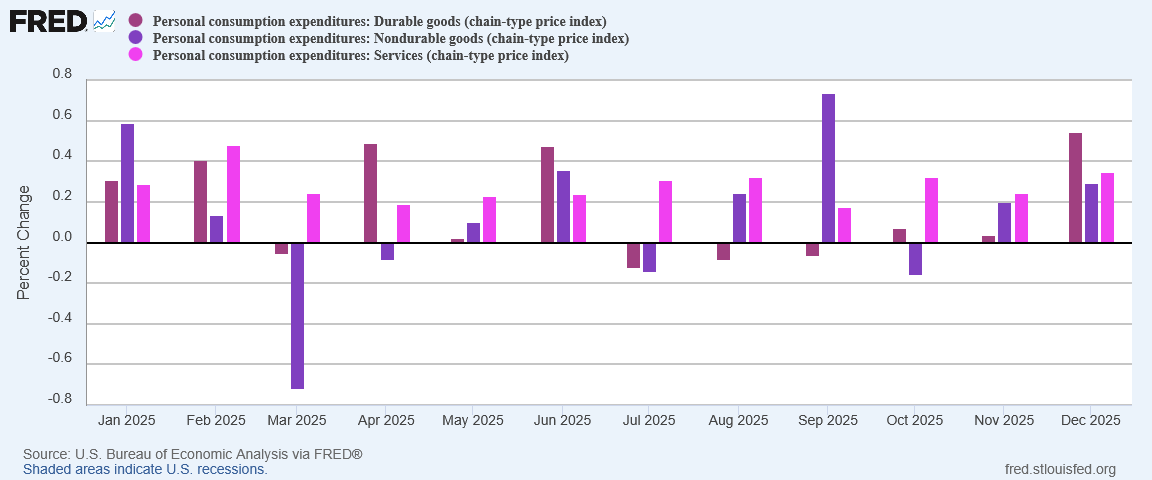

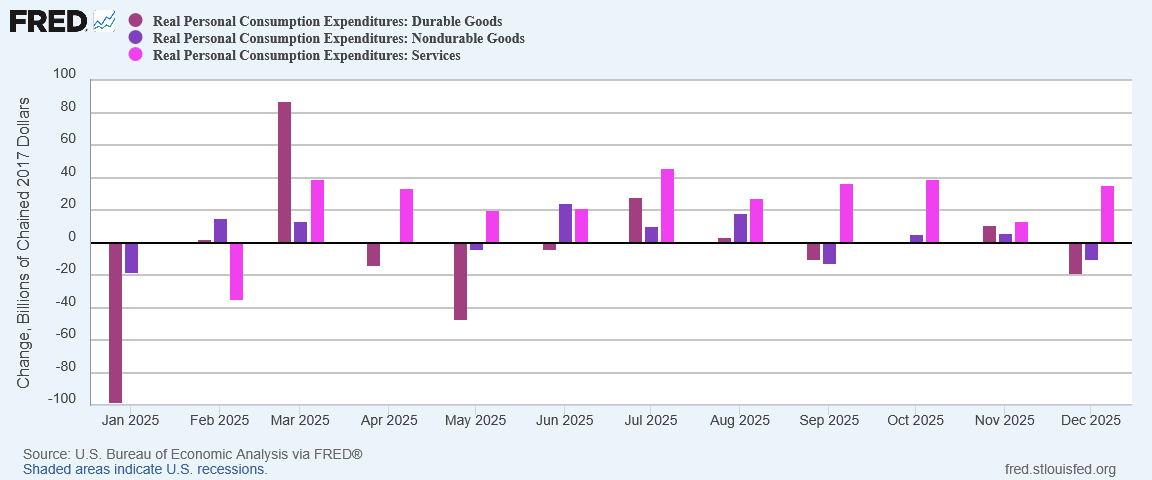

What is remarkable is that within the Core PCEPI, durable goods inflation surged, in a clear deviation from December’s CPI data, which saw durable goods in deflation.

Nondurable goods and services also printed higher in December. For the month the whole of Core PCEPI showed inflation heating up month on month.

This is not an inflationary signal but a stagflationary one. People purchased fewer things in December (which is ironic given one would expect the Christmas holiday to push real consumption of goods higher).

With real consumption declining, it is difficult to project goods prices inflating much further. If there is diminishing impetus to buy now, higher prices are only going to depress consumption further, which will in turn create a dampening effect on any other inflationary pressures that might be in play.

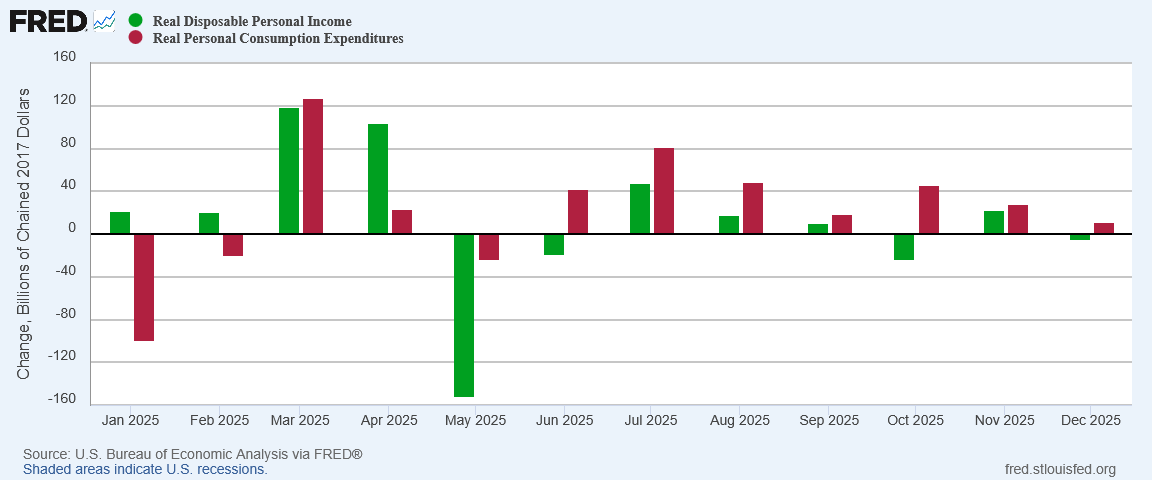

Consumption can only outpace income for so long before spending constraints emerge which limit consumption growth. Thus any future inflationary pressures are once again likely to be dampened by constrained consumption.

Most notably, however, is that real disposable income actually fell in December. Regardless of what wages and earnings have been doing in 2025, the amount of money people have to spend freely diminished in December.

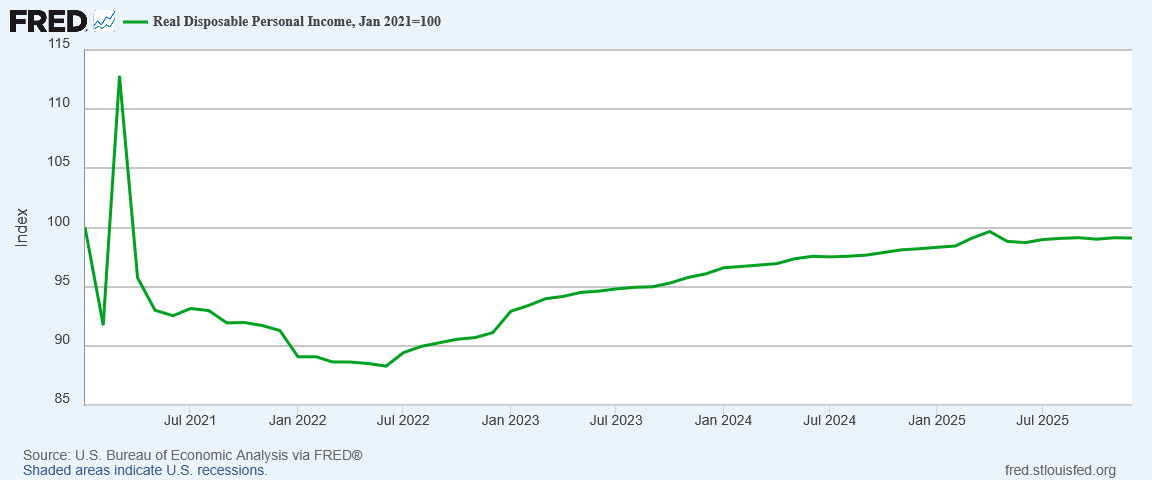

The reality of disposable incomes in the US is that it plateaued last spring and has not grown hardly at all since.

Lack of real disposable income growth suggests that deflation is a far greater concern than inflation at present.

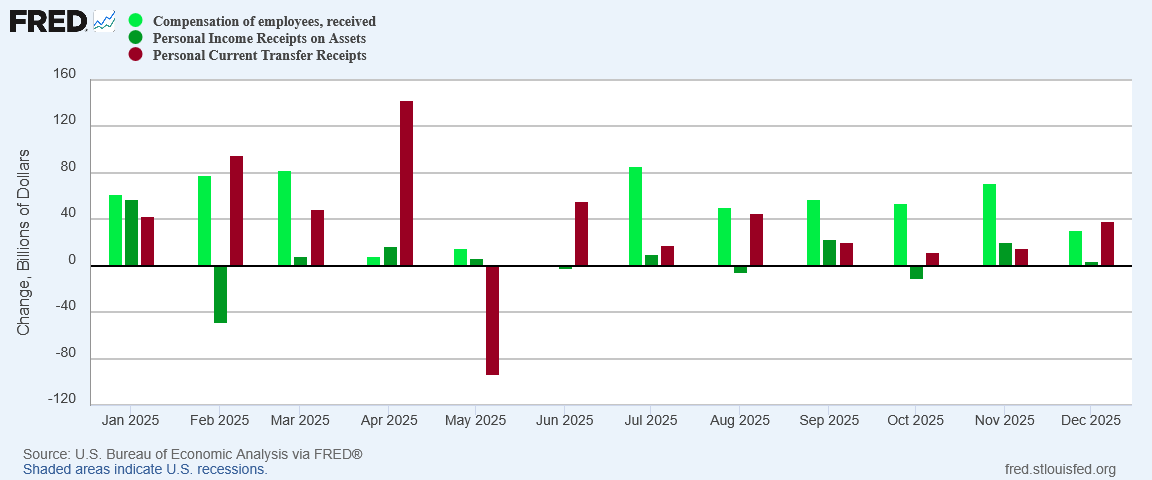

As a rule, the healthiest forms of personal income growth is in compensation and income generated directly from asset ownership. These represent actual additions to the overall economy, not merely shifting dollars around by government diktat. When transfer payments grow faster than compensation, the economy is becoming less productive overall. Should that trend continue the end result is deflation.

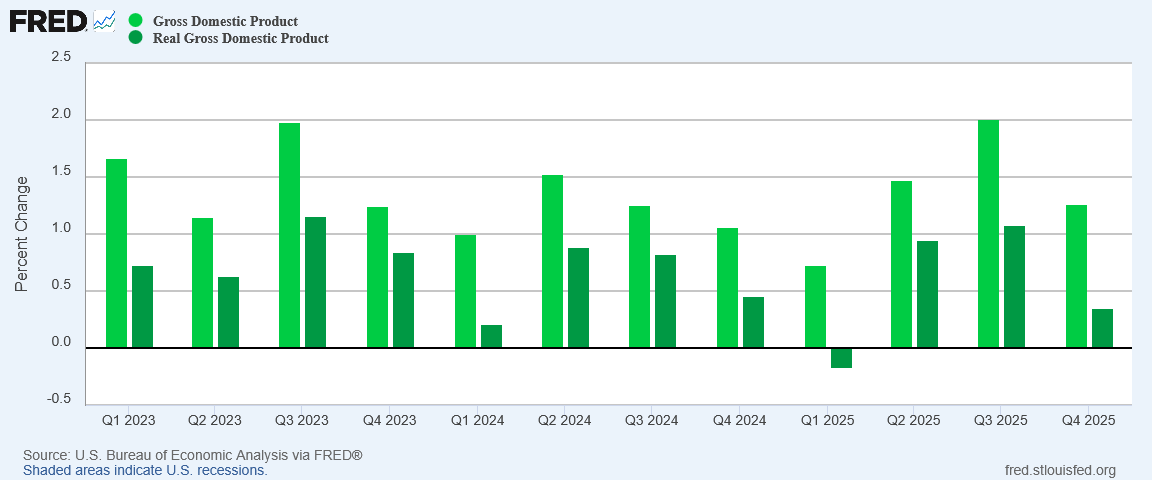

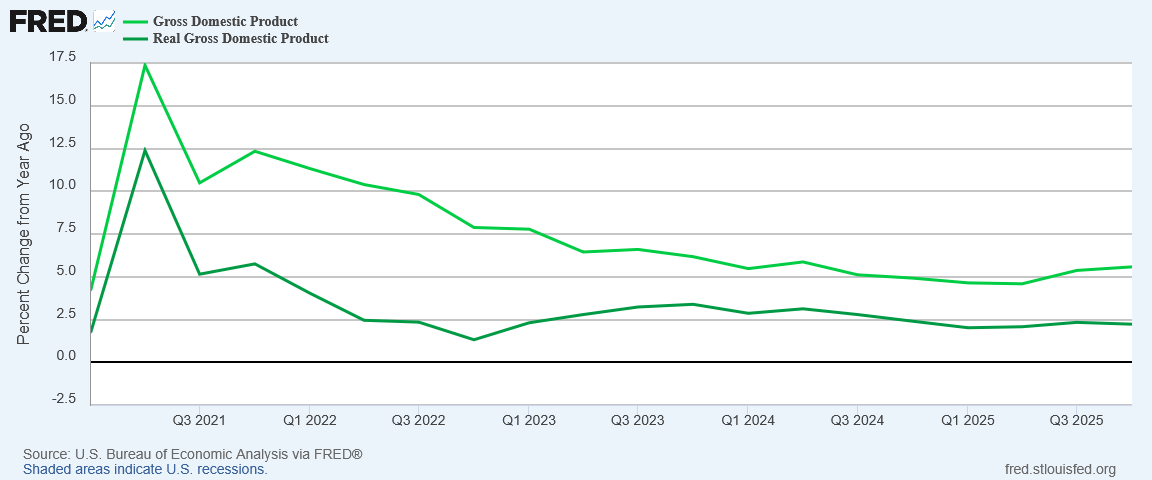

The concern is not merely that the economy slowed in the fourth quarter. The growth trend since 2021 has been one of slower and slower growth for both nominal GDP and Real GDP.

Some of that decline was to be expected, as 2021 was a rebound year from the COVID Pandemic Panic. However, that trend has continued, and while Real GDP staged something of a growth recovery in late 2022 and 2023, since late 2023 Real GDP growth has been slowing down.

When GDP growth is already slowing, the significance of deflationary and stagflationary signals in the economy increases dramatically.

We should not look at the December PCEPI inflation data as a sign that inflation is heating up and that price instability is returning. While the price rises are a cause for concern, and while the deviation between PCEPI and CPI definitely warrants further observation, at present even core inflation per the PCEPI is not trending significantly up year on year. Even month on month there was not a sustained upward trend for either headline or core inflation in the PCEPI data in 2025.

The data does not support any narrative that inflation is about to heat up overall going forward.

We should look at the lack of growth in real disposable income as a warning sign that the US economy may be slipping into stagflation. While the data shows that wages and earnings grew relative to inflation in 2025, the amount of income people are able to spend freely has not. Slowing compensation growth in December certainly does not help.

Without expanding real disposable income, increases in real consumption are inherently constrained. People have to have money before they can spend money as a general rule.

If there are constraints to consumption growth the potential for future growth in the economy overall are likewise constrained. Consumption is a major portion of the US economy, and if consumption is not growing the economy is not growing.

The Personal Income and Outlays Report reads as a cautionary tale. On the one hand we have an unwelcome rise in inflation. On the other hand we have continued lack of increase in disposable income. A continuation of either going forward is a problem for the economy, and a continuation of both would be alarming.

The report is encouraging in that inflation’s rise has so far been incremental. While the report does not confirm that “winter is coming” for inflation, it does not wholly discredit that narrative either.

The Personal Income and Outlays Report does not close out 2025 on a high note. The report opens 2026 with more skepticism and quite a bit less optimism.

That will be frustrating for those who want their narratives to be either good or bad, up or down, optimistic or pessimistic. For everyone else, the report means we cannot say at present whether the economy is heading up or down.

If this story gave you real value, help me keep going. All Facts Matter is powered by readers who believe facts should stand on their own. Your subscription makes that possible.

In an era where seemingly everyone is just pushing some narrative, I appreciate an accurate picture. Thanks, Peter!