There is no denying that the April Personal Income And Outlays Report was good news for the Trump Administration, as it heralded continued disinflation despite the ongoing hooplah over tariffs.

From the same month one year ago, the PCE price index for April increased 2.1 percent. Excluding food and energy, the PCE price index increased 2.5 percent from one year ago.

As I noted last week, the Cleveland Fed’s inflation nowcast was not optimistic enough in projecting ongoing disinflation for April.

Unlike many earlier reports, however, the April PCE report is relatively strong all the way through, as inflation simply has not yet appeared in the economy, despite the many predictions to the contrary.

Contents

Disinflation Continues

The headline numbers were unexpectedly good, with headline inflation coming in at 2.1% year on year, and core inflation printing at 2.5% year on year.

Month on month, the numbers ticked up from March, although not nearly as great as March’s drop from February.

After having trended up since late summer of last year, the drop in month on month inflation rates appears to be a permanent trend reversal. The price rises that were presenting as late as February are simply no longer present in the PCE Price Index as of April.

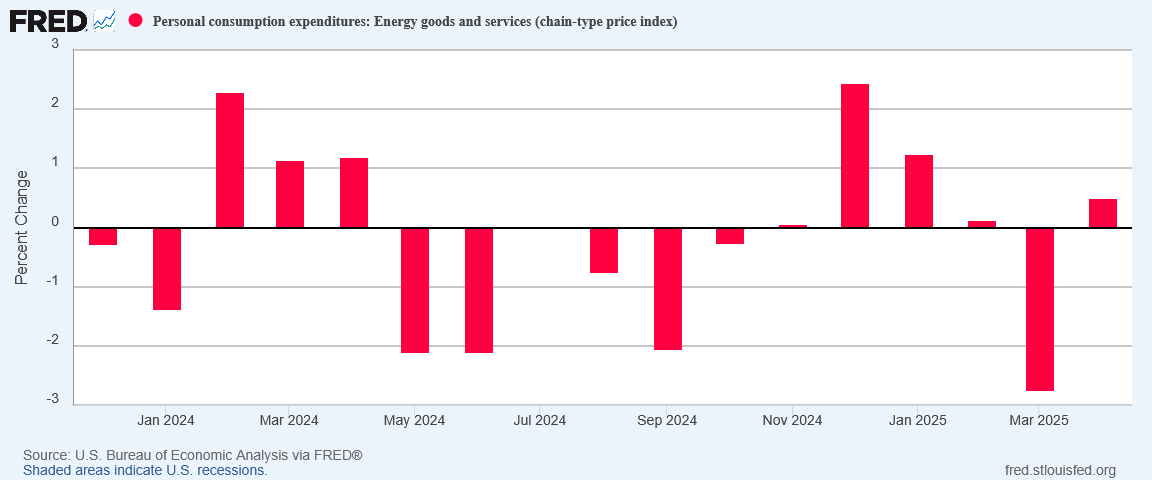

While energy price inflation returned month on month, the trend going back into December of last year is still very much a disinflationary one.

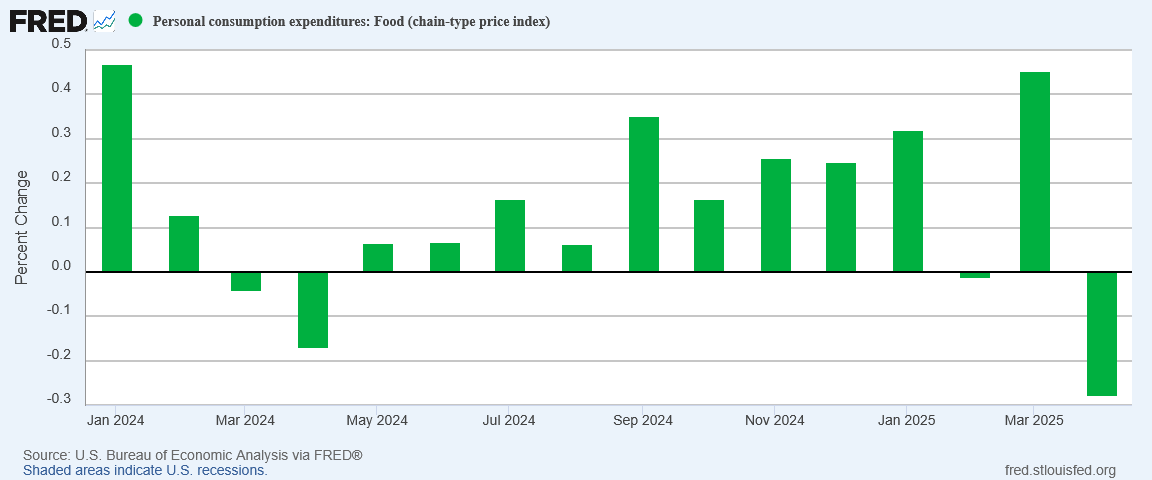

After spiking in March, food prices plunged 0.27pp in April.

The only notable exception to the month on month disinflationary trend was in durable goods, which saw prices rise dramatically, even as nondurable goods continued March’s deflationary trend.

Overall, the price elements in the PCE Price Index either fell or slowed dramatically in their rise during April—indisputably good news for consumers, particularly in the face of the negative press over the Liberation Day tariffs.

DOGE And Tariffs Having Impact?

We should not presume that the tariffs have not been a factor. They have, and so has Trump’s iconoclastic Department Of Government Efficiency, or DOGE.

Perhaps the most visible impact of DOGE has been in stabilizing various government transfer (welfare) payments.

In March and April, while the size of transfer payments did not fall, they especially did not rise. Given the tendency of transfer payments to run on autopilot through most administrations, that the Trump Administration has succeeded in halting their rise for at least a couple of months is a decided win for the Administration and for the likely catalyst to the spending freeze, DOGE.

The impact of the Liberation Day Tariffs comes in as a network effect from March’s surge in personal consumption expenditures.

The March spike represented a front-loading of a lot of consumer demand, almost certainly because of consumer fear about possible tariff-driven price increases.

However, front-loading of demand does not increase aggregate demand, but merely shifts it in time. Thus the March consumption surge becomes a tapering off in consumption for April.

This particularly evident in consumption expenditures for durable and non-durable goods, which shrank in April.

Even service spending growth slowed in April

Will This Continue?

While lack of inflation in any given month is welcome, the significance of inflation itself is always in the longer term trend.

Are prices going to rise or fall as we move into the summer?

While much depends still on the outcome of various trade talks and tariff threats, when we look at a lot of the cost drivers for inflation we do not see significant inflationary forces building at this time.

Oil prices have been trending down since Liberation Day.

Even retail gasoline prices are trending down, with both AAA and Gas Buddy charting price declines extending into May.

The broad energy price declines are part of an overall drop among input prices.

Even if we focus on the commodity indices themselves, we still see broad decline since Liberation Day.

Most remarkably, import prices have not trended up at all since April of 2024.

While we should never say there is no possibility of inflation rising over the near term, at present there are few of the predicate forces needed to push prices up. Until that changes, the likelihood of an uptick in inflation is low.

Inflation Not Returning (Yet)

We should note that, at present, the Liberation Day Tariffs have largely not taken effect yet. Their impact on prices thus far has largely been an anticipatory reaction to their announcement.

Whether we would see significant inflation return should the tariffs be enforced in full and across the board remains very much an open question. With trade talks between the Trump Administration and most trading partners still ongoing, there are no clear predictions which can be made regarding the ultimate impact of the tariffs.

Clearly, as corporate media has been constantly reminding us, if the tariffs are applied in full we could see substantial price increases, along with substantial disruptions to the flow of consumer goods.

However, a curious side effect of the media’s constant pearl-clutching over the tariffs very likely has been to spook consumers, potentially magnifying the drop in consumer demand after March’s exercise in front-loading demand. An overall drop in consumer demand is going to push prices down regardless of what the tariffs have or have not done yet.

Corporate media may very well have helped President Trump beat inflation for a second month simply by being their usual Trump-deranged selves!

Irony abounds.

If the tariffs result in good trade deals, which would mean that most of the reciprocal tariffs would not be applied, the final inflationary impact from the tariffs will be largely mitigated by improved trade. Even if the tariffs ultimately are applied, the longer they hang out there as a future possibility, the more opportunity businesses have to find alternative sourcing for various products, thus sidestepping at least some of the tariffs.

We should not presume that inflation has been completely conquered by the Trump Administration. It hasn’t, and it won’t be. Inflation does not get conquered, it merely does not get made worse by the incumbent Presidential administration.

However, until many of the ongoing macroeconomic trends change, President Trump can look forward to ongoing disinflation for the next few months at least.

That will be a clear political win for President Trump, and a clear economic win for the American consumer.

Thanks for giving us some good news (food prices are down!) and for answering in advance all of my nitpicking little questions, Peter. You are so good at this!

I find it particularly hilarious that corporate media may have, once again, shot themselves in the foot while going after Orange Man Bad. Every time Trump gets another win he becomes empowered to soldier on with his revolutionary changes. MAGA!