Yesterday’s biggest non-news event on Wall Street was Federal Reserve Chairman Jerome Powell doing exactly what people expected of him—not a damn thing.

Specifically, Jay Powell and the Federal Open Market Committee (FOMC) opted not to lower the federal funds rate at the conclusion of their regular two-day meeting. This was exactly what Wall Street has been expecting for some time.

That Jay Powell did what Wall Street expected of him is not newsworthy. What warrants further consideration is that Powell did nothing on the federal funds rate because he does not know what he should do.

Remarkably, Jay Powell all but admitted he did not have a good read on the economy and Wall Street was okay with that!

Jay Powell’s indecisiveness is as good a reason as any to unpack some of the economic data which mystifies him. By applying a soupcon of analysis, perhaps we can see what Powell might be overlooking, and get the read on the US economy that appears to elude him.

Contents

Fed Stands Pat

As I had noted yesterday, the clear expectation on Wall Street was that the Federal Open Market Committee was going to let interest rates stand for at least another month.

When the FOMC made their public announcement yesterday afternoon, that is exactly what they chose to do.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In his usual post-meeting press briefing, Powell sought to explain in his opening remarks that the Fed’s uncertainty about the Trump Administration’s tariff policies was the principal driving force behind the the committee’s decision to stand pat on the federal funds rate.

The new Administration is in the process of implementing substantial policy changes in four distinct areas: trade, immigration, fiscal policy, and regulation. The tariff increases announced so far have been significantly larger than anticipated. All of these policies are still evolving, however, and their effects on the economy remain highly uncertain. As economic conditions evolve, we will continue to determine the appropriate stance of monetary policy based on the incoming data, the outlook, and the balance of risks.

If the large increases in tariffs that have been announced are sustained, they are likely to generate a rise in inflation, a slowdown in economic growth, and an increase in unemployment. The effects on inflation could be short-lived—reflecting a one-time shift in the price level. It is also possible that the inflationary effects could instead be more persistent. Avoiding that outcome will depend on the size of the tariff effects, on how long it takes for them to pass through fully into prices, and, ultimately, on keeping longer-term inflation expectations well anchored.

Yet while Powell and the FOMC are stymied by the unorthodox policies of the Trump Administration, Wall Street has for quite some time been dialing back the expectations of imminent recession.

We know this because not only have a number of Wall Street “experts” such as Ed Yardeni been reducing their recession forecasts, but last fall, the yield curve on US Treasuries finally came out of inversion. For the past couple of years, the shorter-term maturities have commanded higher yields than the longer-term maturities, a phenomenon long viewed as a recession warning signal as it indicates that markets are taking a dimmer view of the short-term outlook than the longer-term outlook.

That inversion ended last October.

President Trump’s disruptive policies have not altered the yield curve outlook. On that basis alone we have to take recession fears with a fairly large grain of salt. Wall Street is simply not channeling that sort of pessimism at the moment.

We received further confirmation of Powell’s confusion immediately after his opening remarks, when he fielded the very first question:

Steve Liesman, CNBC: Thank you, Mr. Chairman, for taking my question. A lot has happened since the last meeting. There's been tariffs put on, tariffs taken off. And meanwhile, there's a bill advancing in Congress. And I just wonder if I could press you on the last part of your statement. Are you any closer now to deciding which side of the mandate is going to need urgent care first?

Chair Powell: Well, so as we noted in our statement, post-meeting statement, we've judged that the risks to higher employment and higher inflation have both risen. And this, by the way, of course, is compared to March. So that's what we can say. I don't think we can say, you know, which way this will shake out. I think there's a great deal of uncertainty about—for example, where tariff policies are going to settle out, and also when they do settle out, what will be the implications for the economy for growth and for employment. I think it's too early to know that. So, I mean, ultimately, we think our policy rate is in a good place to stay as we await further clarity on tariffs and ultimately our implications for the economy.

Uncertainty would prove to be the dominant theme of the press briefing, even when Powell was asked why the Fed insisted on waiting still longer before making further reductions to the federal funds rate.

Courtney Brown, Axios: I guess, you know, we talked about some of the indications of potential layoffs, price hikes, an economic slowdown all being evident in the soft data. I'm curious why the Fed needs to wait for that to translate into hard data to, you know, make any type of monetary policy decision, especially if the hard data is not as timely or might be warped by tariff-related effects. Are you worried that the soft data might be some sort of false warning?

Chair Powell: No. I mean, it's-look, the late-look at the state of the economy. The labor market is solid. Inflation is low. We can afford to be patient as things unfold. There's no real cost to our waiting at this point. Also, the sense of-the sense of it is we're not sure what the right thing will be. You know, there should be some increase in inflation. There should be some increase in unemployment. Those call for different responses. And so until we know, potentially call for different responses. And so, you know, until we know more, we have the ability to wait and see. And it seems to be a pretty clear decision. Everyone on the committee supported waiting. And so that's why we're waiting.

Despite the Fed seeing elevated “risks” to employment, Powell believes it is better to stand and do nothing instead of attempting to be proactive.

Powell’s passivity reminds me of the Fed’s inaction in 2021 and 2022, when “transitory” inflation was allowed to take hold in the US economy. Standing by and doing nothing has not always worked out well for the Fed—or for the US economy.

Wall Street Was Happy

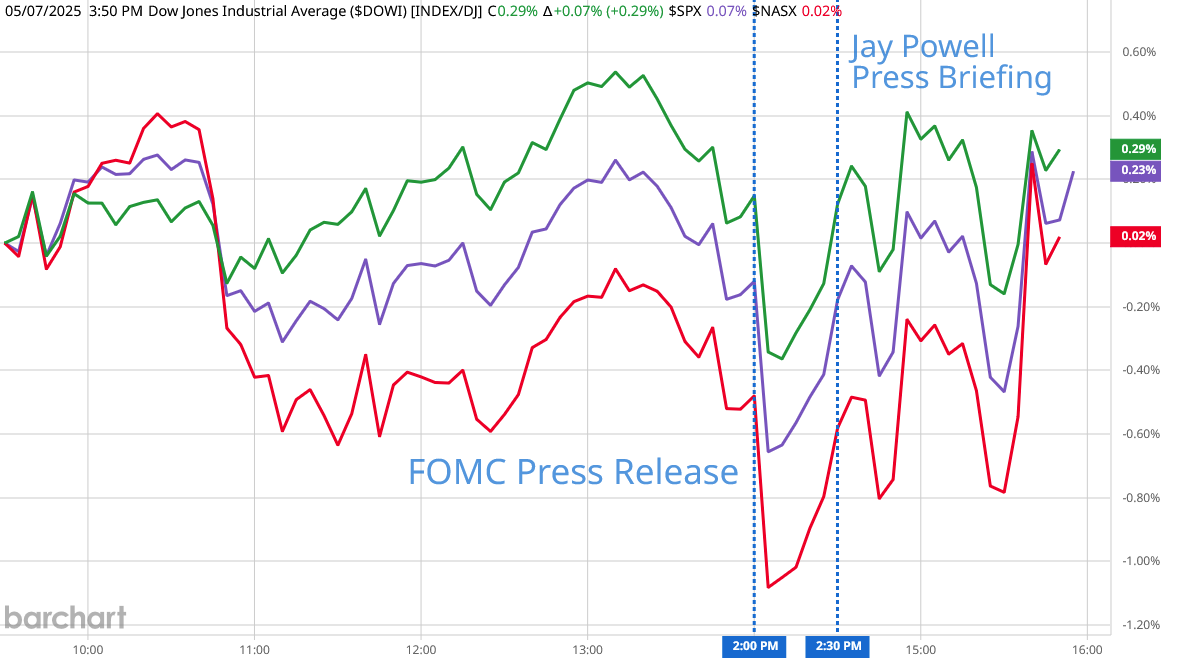

Whatever the reason for Powell’s inaction on interest rates, Wall Street was apparently satisfied that he met their expectations.

Despite dropping sharply when the FOMC press release first came out, during Powell’s presser Wall Street largely recovered to finish the day in positive territory.

In foreign exchange markets, the dollar rose against the dollar index throughout the press briefing.

Not only did the dollar gain, but its gain was more rapid during the press briefing than it had been in the run-up to the FOMC press release

Even treasury yields rewarded Powell by moving lower on the day.

Given Powell’s predilection for saying things to spook the market, he received a surprising vote of confidence yesterday afternoon!

Main Street Not So Happy

If Wall Street is content with the status quo, Main Street—where the actual factories exist and where the actual jobs exist—is rather less optimistic about where the economy is headed.

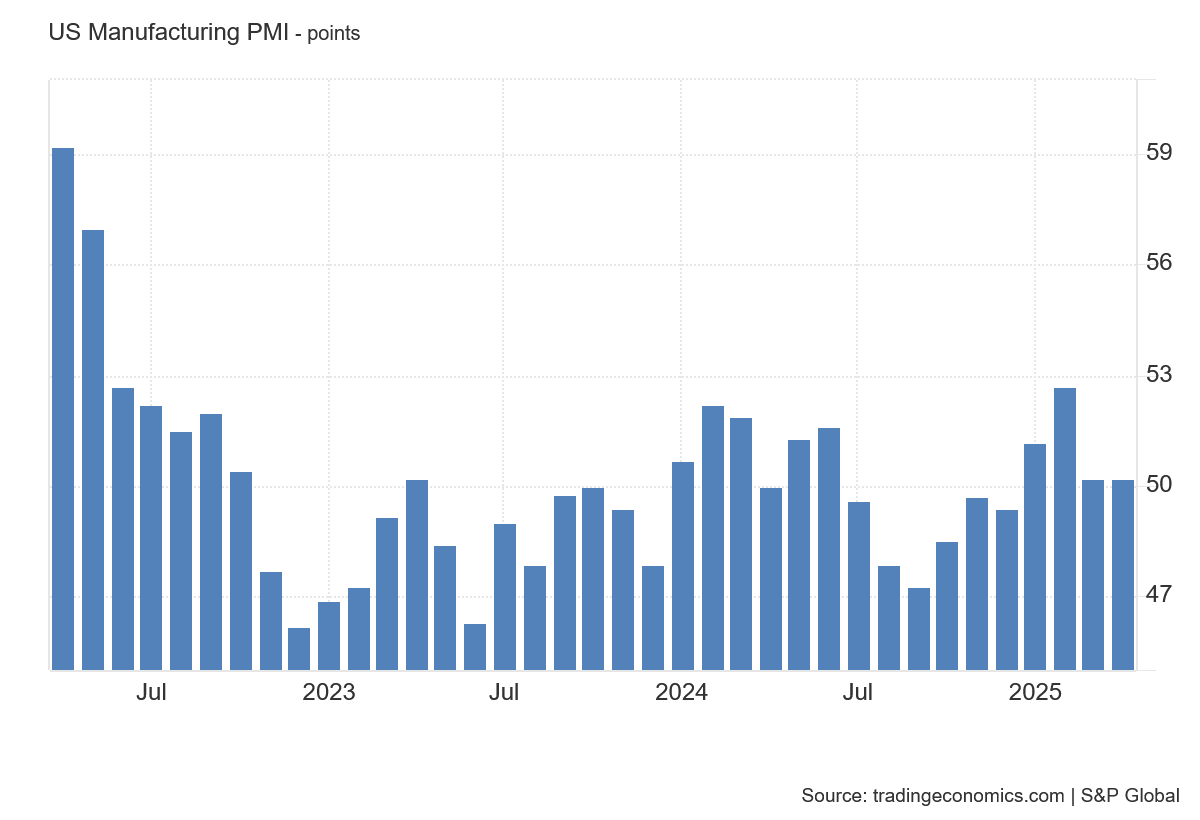

The Institute for Supply Management Manufacturing Purchasing Manager’s Index (PMI) printed contraction for April at 48.7, the second month of contraction in a row.

The S&P Global Manufacturing PMI was only slightly better, narrowly avoiding contraction with a 50.2 print.

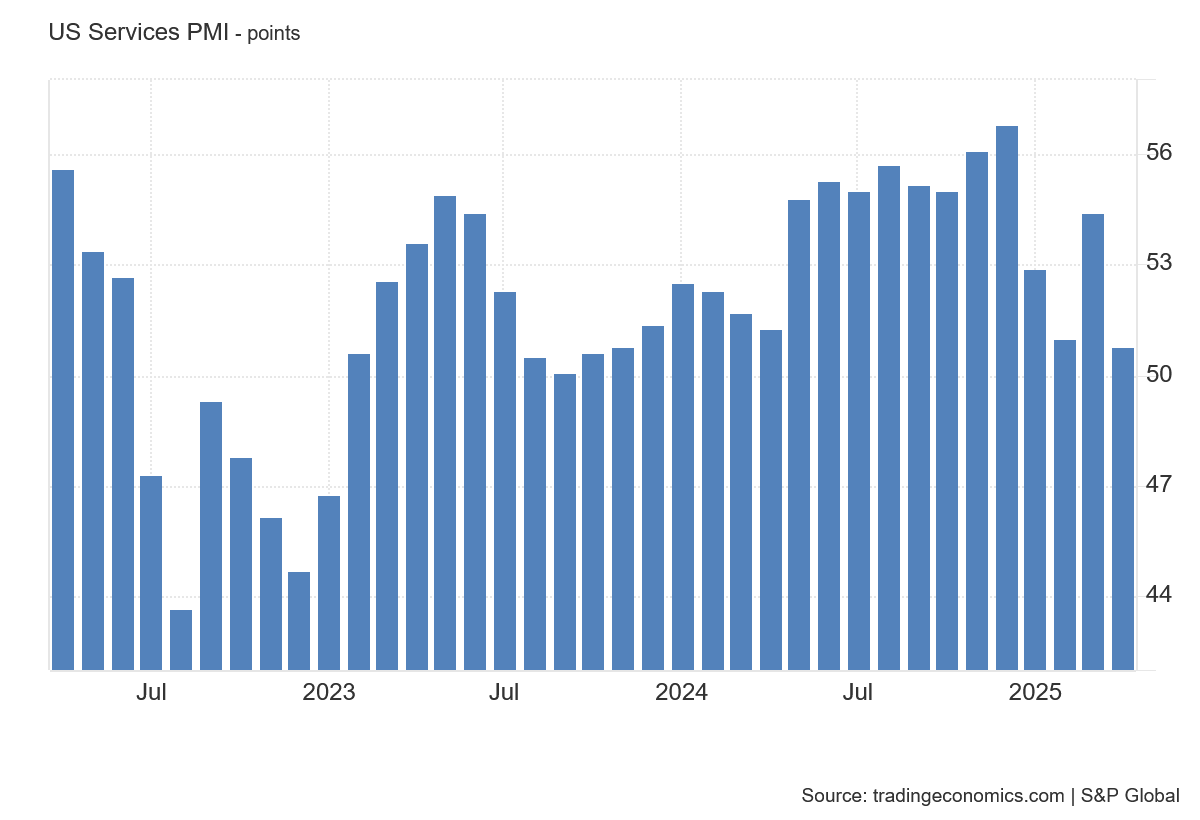

S&P Global’s Services PMI has likewise been softening in recent months. While it has been printing expansion, that expansion has still been declining.

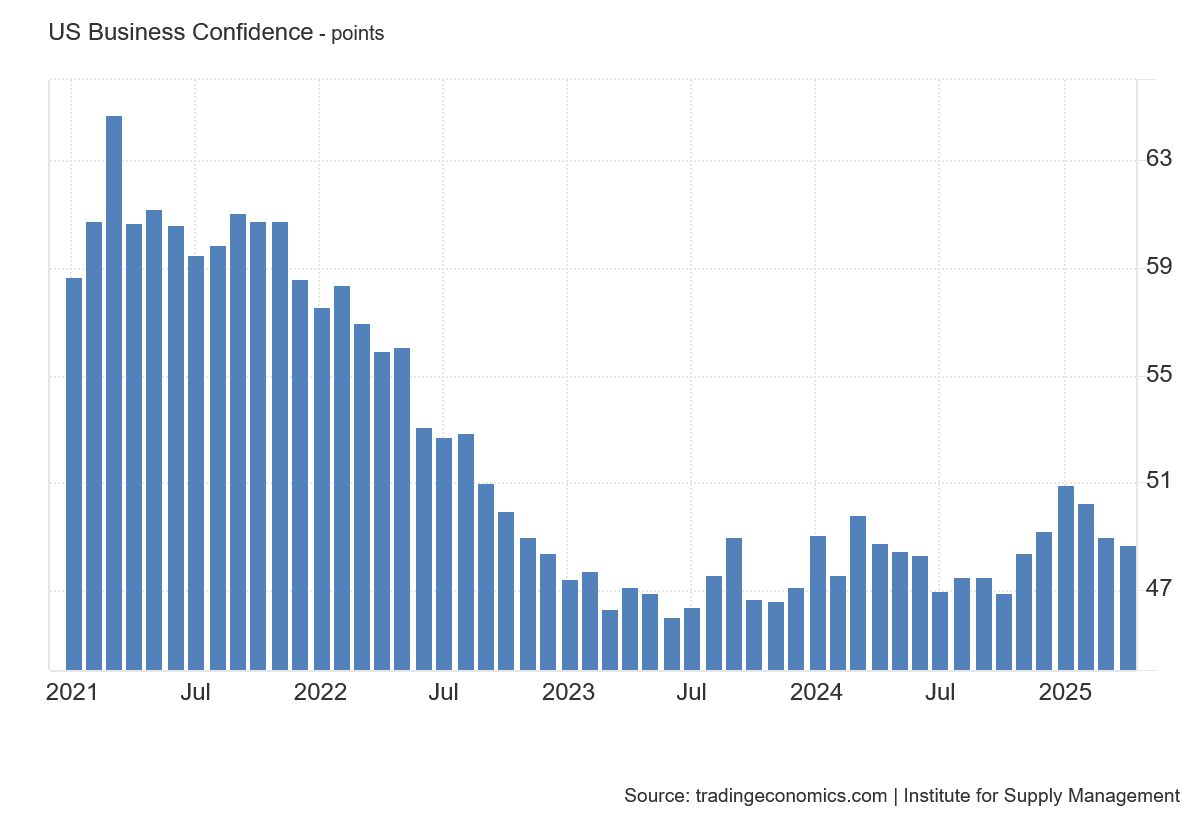

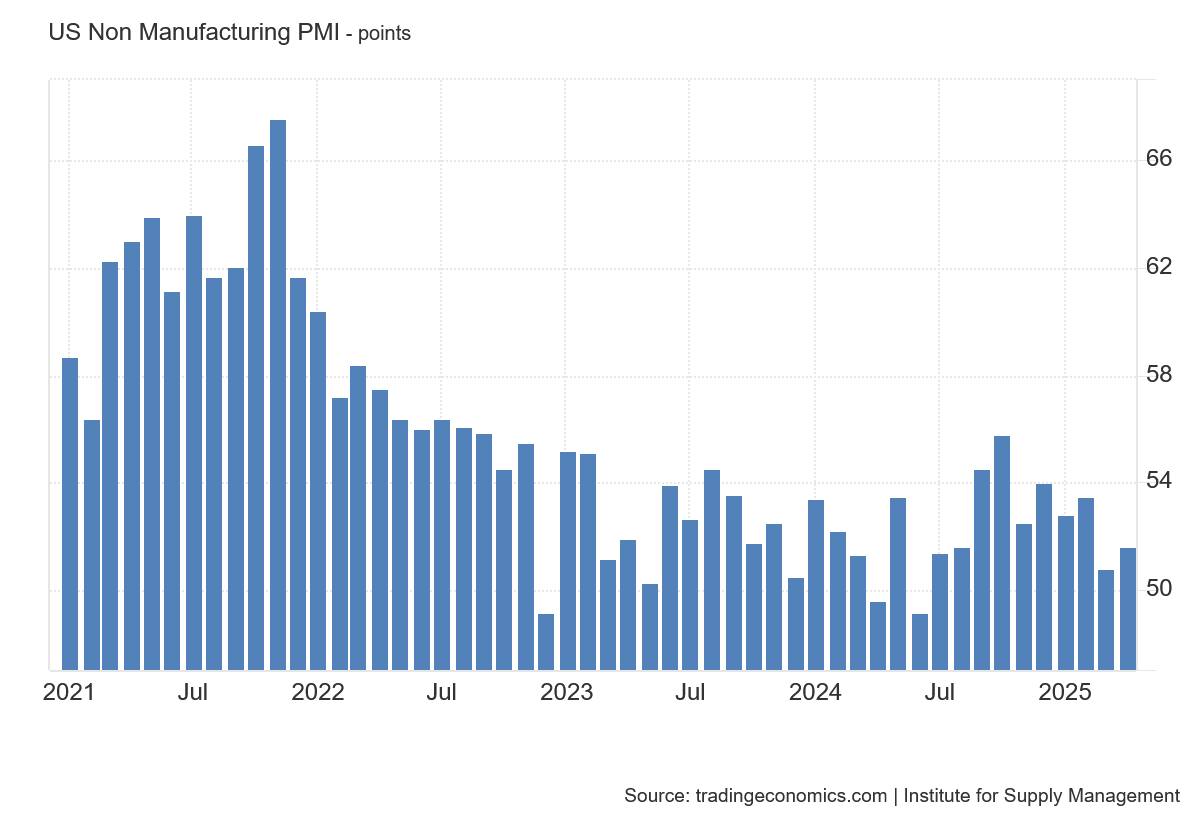

Even the ISM’s Services PMI has been showing signs of weakness in recent months.

While the S&P Global and ISM PMI data are apparently not on the Fed’s radar, they are still economic data points that Wall Street uses regularly to assess the ongoing state of the economy.

The S&P Global and ISM PMI data tell us the US economy is not altogether healthy and robust. Moreover, the economy has been getting somewhat worse over the past several months at least.

Manufacturing Signals Weakness

Nor is it simply the PMI data which is signalling that all is not well in the US economy.

The diffusion index from the Texas Manufacturing Outlook Survey printed an alarming -35.8 in April.

To say that manufacturing businesses in Texas have a negative perception of their business environment would be an understatement!

The outlook is not much better in New York.

The Philadelphia Federal Reserve’s Manufacturing Business Outlook Survey found a business sentiment almost as negative as that in Texas.

When manufacturing businesses across the country share a negative outlook on business in general, it is difficult not to see that as a signal of gathering weakness within the manufacturing sectors of the economy overall. Regardless of the underlying cause for the negative sentiment, the end result is manufacturing businesses which do not have confidence in the future.

That’s a signal showing economic weakness that is difficult to ignore. Yet somehow Jay Powell managed to ignore it.

New Orders Promising

We should not conclude from the manufacturing surveys that all the data out there is negative. There are data points that signal economic strength.

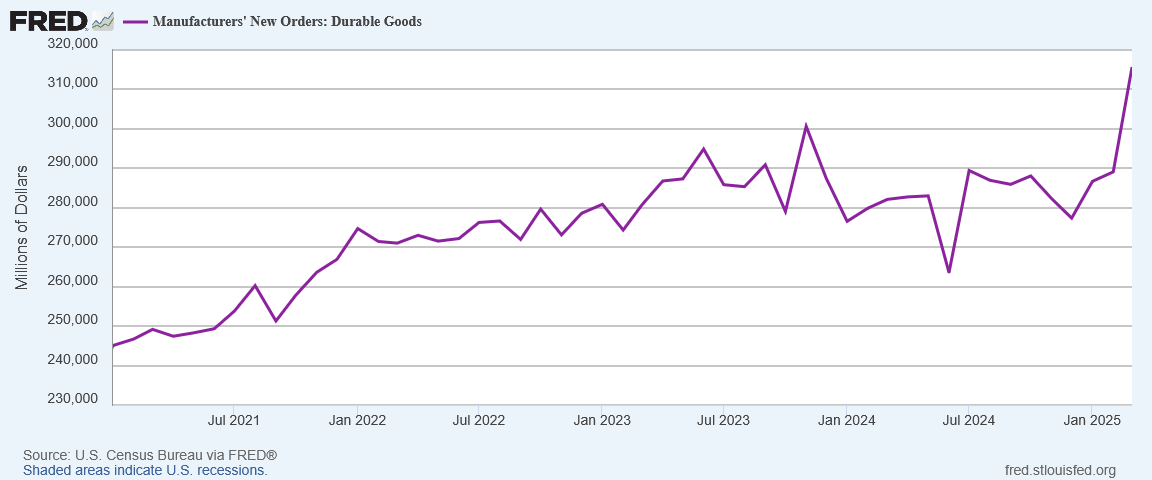

The rising dollar volume of manufacturing new orders is very much a welcome sign of manufacturing growth.

Even more encouraging is when we drill down into the new order data, we see similar strength for durable goods new orders.

Even consumer goods, which showed one of the weakest new order prints in April, at least remained constant on the month.

Manufacturing may be sour on the future, but rising new orders are definitely a reason to be hopeful about the present.

The Jobs Recession Is Real

No matter how hopeful we may be from rising dollar volumes of new manufacturing orders, however, we should not overlook the reality of the ongoing jobs recession in this country.

Manufacturing employment, which lost jobs in April, highlights the continued weakness evident in US labor markets.

A lack of manufacturing jobs is one reason the United States has seen rising unemployment since early 2023.

That lack of manufacturing jobs is equally a contributor to rising numbers of people who are forced to work part-time because they cannot find full-time employment.

When Powell speaks of a solid labor market in this country, it is clear he is ignoring much of the available detail on the labor market. Even the April Employment Situation Summary—notionally a “strong” jobs report—showed that the US is still not producing enough jobs given the size of the labor force.

The data shows the US economy is producing jobs. The data shows the US economy is not producing enough jobs.

Powell chooses to ignore this data.

Economy Is NOT Solid

Contrary to how Jay Powell presents the US economy, we have a wealth of data detailing numerous weaknesses within the economy.

We have PMI data indicating major sectors of the economy are in contraction.

We have survey data showing manufacturing businesses across the country are extremely pessimistic about the future.

We have shrinking manufacturing employment.

These are all signs the economy is not “in a solid position”.

The economy is not in a state of catastrophic collapse, but neither is it in a state of even rude health. That much is apparent even from just the few data points I have presented here.

Why Powell prefers to toss out nostrums about labor markets being solid and the economy being in a solid position, in the face of considerable data which shows the exact opposite to be true, is a mystery. Why he prefers to then contradict himself by rambling about “elevated risks”—risks which would not exist in a healthy economy by definition—is also mysterious.

Equally curious—and more disturbing—is Powell’s inability to state clearly why the FOMC felt that not lowering the federal funds rate was the right policy choice given the current data.

While the logic of tweaking the economy by manipulating the federal funds rate is dubious at best, within that policy the clear evidence of increasing economic weakness argues for action rather than inaction. A 25bps reduction in the federal funds rate might not produce an abundance of economic stimulus, but it certainly would also not produce an excess of consumer price inflation.

A 25bps reduction would have been a prudent and proactive choice by the Fed. It would have been the right choice by the Fed.

Even Powell’s “elevated risks” assertions would be better deployed defending a rate cut rather than a decision not to cut rates.

There is no logic to denying or minimizing the very real problems that have existed in the US economy for quite some time.

We have been in a jobs recession since November of 2023, and quite possibly earlier.

Manufacturing especially has not been doing well in this country.

We have economic sectors that are contracting rather than expanding.

Despite the data, Powell preferred to stand by and do nothing. Instead of looking at the economy unsparingly and realistically, Powell preferred to ignore crucial evidence and dissemble. Instead of defending in clear and coherent terms why the FOMC did not raise interest rates, Powell preferred to advance a confused and internally incoherent fairy tale about economic health and vitality.

Despite the data, Wall Street was pleased with Powell’s preferences.

Looking at the data we should not be pleased—not with Jerome Powell, and not with Wall Street.

“Looking at the data we should not be pleased—not with Jerome Powell, and not with Wall Street.”

I still have the sense that Trump might react. He is not going to be happy, and he’s a guy who takes bold actions. Peter, you are most likely right to say that Trump won’t fire Powell; you’ve given good reasons why that would be counterproductive. But Trump doesn’t like being stymied by others’ inactions. So I’m left wondering what Trump will do…