John Roberts' Tariff Ruling Is Simply Wrong

Roberts' Rambling Opinion Falls Apart Under Its Own Words

I am tempted to feel sorry for Speaker of the House Mike Johnson. In a rambling, disjointed, and fatally flawed ruling countermanding Trump’s Liberation Day tariffs, issued under authority of the International Emergency Economic Powers Act (IEEPA), Chief Justice John Roberts lobbed a Molotov cocktail of controversy into the current session of Congress. Now Johnson has to figure out what in the Nine Circles of Hell he is supposed to do with it.

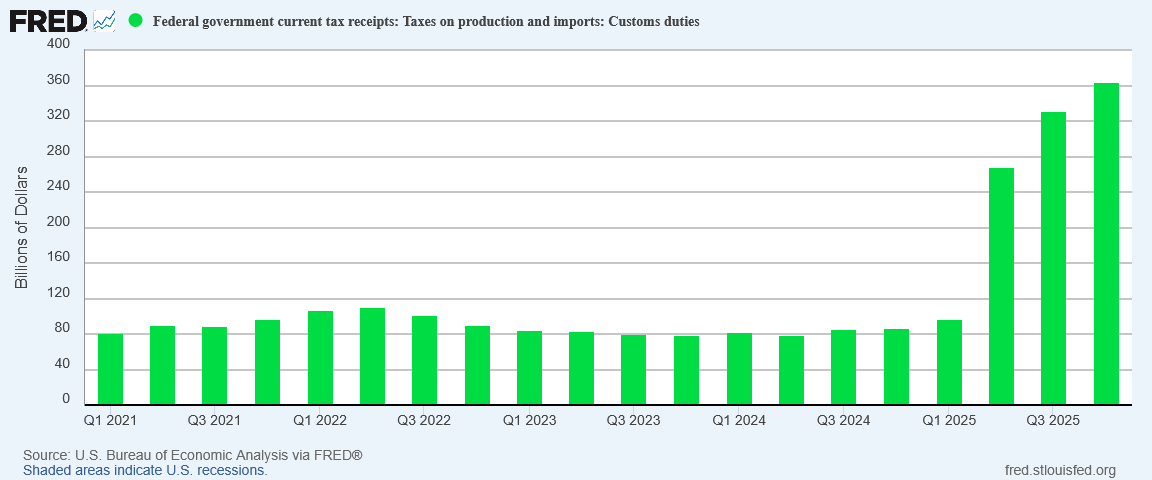

Speaker Johnson certainly has facts on his side: tariff revenue has soared into the stratosphere under President Trump.

Having facts on his side is quite a bit more than can be said for Roberts’ sketchy and contorted majority opinion. As dissenting Justices Thomas, Kavanaugh, and Alito elucidate, Roberts’ opinion is nothing but hogwash and horse hockey.

Chief Justice Roberts said Trump was wrong to secure this revenue for the United States.

Alas for Chief Justice Roberts, he is the one in the wrong. He is wrong in his opinion, he is wrong on the facts, and he is wrong on the law.

Is Roberts’ Opinion Even The Majority Opinion?

Assessing the Court’s 6-3 decision in the tariff case Learning Resources, Inc. v. Trump1 is challenging, because in addition to Roberts’ “majority” opinion there were concurring opinions produced by Justices Kagan, Jackson, Gorsuch, and Barrett, with dissenting opinions produced by Justices Thomas, Alito, and Kavanaugh.

There was a 6-3 vote on the case, but is there an actual majority opinion upon which future case law may be reliably built? The evidence strongly suggests there is not.

Indeed, the quality of the ruling itself is called into question rather ironically by Neil Gorsuch, one of the six justices voting to void President Trump’s tariffs. Intriguingly, Gorsuch’s concurrence2 suggests there may not even be a majority opinion on this case:

Not everyone sees it this way. Past critics of the major questions doctrine do not object to its application in this case, and they even join much of today’s principal opinion. But, they insist, they can reach the same result by employing only routine tools of statutory interpretation. Post, at 1 (Kagan, J., joined by Sotomayor and Jackson, JJ., concurring in part and concurring in judgment). Meanwhile, one colleague who joins the principal opinion in full suggests the major questions doctrine is nothing more than routine statutory interpretation. Post, at 1 (Barrett, J., concurring). Still others who have joined major questions decisions in the past dissent from today’s application of the doctrine. Post, at 1 (Kavanaugh, J., joined by Thomas and Alito, JJ., dissenting). Finally, seeking to sidestep the major questions doctrine altogether, one colleague submits that Congress may hand over to the President most of its powers, including the tariff power, without limit. Post, at 1–2 (Thomas, J., dissenting). It is an interesting turn of events. Each camp warrants a visit.

If Gorsuch’s assessment is accurate, then the six justices in the majority agree only partially with each other, and disagree partially with each other.

The concurrences authored by Kagan, Jackson, and Barrett certainly support that argument.

Perhaps more crucially, Gorsuch levels a significant and even lethal accusation against his concurring colleagues: bias.

Unpack that last claim first. My concurring colleagues contend that, as a matter of “straight-up statutory construction,” IEEPA does not grant the President the power to impose tariffs. Post, at 7. In doing so, they make thoughtful points about the statute’s text and context. But their approach today is difficult to square with how they have interpreted other statutes. Dissenting in past major questions cases, they have argued that broad statutory language granting powers to executive officials should be read for all it is worth. Yet, now, when it comes to IEEPA’s similarly broad language granting powers to the President, they take a more constrained approach.

Those last two sentences deserve particular emphasis and especial consideration. Gorsuch is saying plainly that the the Supreme Court is applying the law and case precedent differently in this case against President Trump than in previous cases.

That is not how the judicial doctrine of stare decisis3 operates. Stare decisis—Latin for “let the decision stand”—is a judicial principle dating back to medieval English Common Law which presumes that similar cases should be adjudicated similarly.

Under stare decisis, once a court has answered a question, the same question in other cases must elicit the same response from the same court or lower courts in that jurisdiction.

Per Justice Gorsuch, the Supreme Court has set that principle aside to adjudicate this case, and done so for the worst of all possible reasons: because Trump.

This is the point where Gorsuch’s concurrence leaves the United States: The Supreme Court reads the Constitution of the United States differently for President Trump than it did for President Biden.

Even corporate media has been obliged to acknowledge Gorsuch’s claims and the clear consequence that the Court issued the ruling it did because Trump.

A Supreme Court ruling made under the influence of Trump Derangement Syndrome is a ruling repugnant to the Constitution, to every premise and principle of the rule of law, and of simple common sense. On that basis alone this ruling is inoperable, null, and void.

Roberts’ Pretzel Logic Is Not Logical

The irony of Chief Justice Roberts’ rebuke of President Trump’s claims of sweeping and extravagant authority under the IEEPA is that he makes equally sweeping and extravagant claims to reject Trump’s authority.

Roberts begins his contorted reasoning by a simple but entirely unsupported statement reducing the Trump Administration’s arguments to exactly two words.

Based on two words separated by 16 others in Section 1702(a)(1)(B) of IEEPA—“regulate” and “importation”—the President asserts the independent power to impose tariffs on imports from any country, of any product, at any rate, for any amount of time. Those words cannot bear such weight.

This is the crux of Roberts’ ruling, that two words from the IEEPA do not mean what Donald Trump asserts them to mean.

Does Roberts’ claim stand up under scrutiny?

We begin by examining the text of the statute in question:

(a) In general

(1) At the times and to the extent specified in section 1701 of this title, the President may, under such regulations as he may prescribe, by means of instructions, licenses, or otherwise—

(B) investigate, block during the pendency of an investigation, regulate, direct and compel, nullify, void, prevent or prohibit, any acquisition, holding, withholding, use, transfer, withdrawal, transportation, importation or exportation of, or dealing in, or exercising any right, power, or privilege with respect to, or transactions involving, any property in which any foreign country or a national thereof has any interest by any person, or with respect to any property, subject to the jurisdiction of the United States;

According to Chief Justice Roberts, this is the sum total of the Administration argument.

But is it?

The Administration’s argument as elucidated in its formal responses is indeed grounded on a premise of authority to “regulate importation”.

Text, context, and history confirm that IEEPA’s phrase “regulate importation” includes tariffs, which have been recognized since the Founding as a traditional, well-established method to regulate imports. Plaintiffs concede that IEEPA authorizes a host of more aggressive actions not specifically enumerated in its text—including quotas, quality restrictions, and quarantines, VOS Br. 15; States Br. 23-24; Learning Br. 23, 35—but struggle to explain why tariffs alone should be excluded.

However, the Administration explicitly rejects a key component of Roberts’ core argument: It affirms Congressional oversight authority, which precludes the possibility of Presidential powers under the IEEPA ever being even notionally “independent.”

Plaintiffs invoke the major-questions doctrine, but it does not apply here. IEEPA addresses the most major of questions—international emergencies—by explicitly conferring major powers. A “practical understanding of legislative intent,” West Virginia v. EPA, 597 U.S. 697, 723 (2022), shows that Congress made a deliberate, “eyes-open” decision, 25-250 Pet. App. 66a, 112a, 123a (Taranto, J., dissenting), to equip the President in advance with the full range of tools he might need to address foreign emergencies. Recognizing that “it is impossible to foresee * * * the extent and variety of national exigencies” or the “variety of the means which may be necessary to satisfy them,” Loving v. United States, 517 U.S. 748, 767 (1996) (quoting The Federalist No. 23 (Hamilton)), Congress retained robust political oversight over the President’s exercise of those emergency powers.

However, even if we overlook Roberts’ clear factual error in his foundational reasoning, his reasoning extends further by differentiating between “regulation” and the imposition of tariffs, which he (correctly) points out is a part of the taxing authority of Congress.

The power to impose tariffs is “very clear[ly] . . . a branch of the taxing power.” Gibbons v. Ogden, 9 Wheat. 1, 201 (1824). “A tariff,” after all, “is a tax levied on imported goods and services.” Congressional Research Service (CRS), C. Casey, U. S. Tariff Policy: Overview 1 (2025). And tariffs “raise[ ] revenue,” West Lynn Creamery, Inc. v. Healy, 512 U.S. 186, 193 (1994)—the defining feature of a tax, United States v. Kahriger, 345 U.S. 22, 28, and n. 4 (1953); Sonzinsky v. United States, 300 U.S. 506, 514 (1937). Indeed, the Framers expected that the Government would for “a long time depend . . . chiefly on” tariffs for revenue. The Federalist No. 12, at 93 (A. Hamilton). Little wonder, then, that the First Congress’s first exercise of its taxing power (and its second enacted law, right after the one providing for the new officials to take an oath) was a tariff law. See Act of July 4, 1789, ch. 2, 1Stat. 24.

We will concede the obvious point, that Roberts cited the Constitution correctly on this point. Article 1 Section 8 Clause 1 of the Constitution explicitly mentions “Duties, Imposts, and Excises” alongside “Taxes” as a power of Congress.

However, even Roberts concedes the Trump Administration is not contesting the power of Congress to impose (and therefore rescind) tariffs, rendering Roberts’ reasoning on this point wholly non sequitur.

The Government thus concedes, as it must, that the President enjoys no inherent authority to impose tariffs during peacetime. Tr. of Oral Arg. 70–71. And it does not defend the challenged tariffs as an exercise of the President’s warmaking powers. The United States, after all, is not at war with every nation in the world. The Government instead relies exclusively on IEEPA. It reads the words “regulate” and “importation” to effect a sweeping delegation of Congress’s power to set tariff policy—authorizing the President to impose tariffs of unlimited amount and duration, on any product from any country. 50 U. S. C. §1702(a)(1)(B).

Roberts is not restrained by this admission of the obvious, however, and then sets the stage for a Clintonian level of word parsing by deriding the IEEPA language as “ambiguous.”

We have long expressed “reluctan[ce] to read into ambiguous statutory text” extraordinary delegations of Congress’s powers.

Is the IEEPA text truly “ambiguous”? It might be if there were not prior statutory language already accepted by the Court, the Congress, and the country affirming substantially the same authorities being claimed by the Trump Administration.

Indeed, this is where Roberts’ rationale runs into severe problems, because the Liberation Day tariffs are not the first unilateral imposition of tariffs by a President. Most notably, and recalling Gorsuch’s claim of juridical bias in this case, we should ponder another President who quite recently asserted authority to regulate the importation of goods by means of tariffs: Joe Biden.

Why Was It Okay For Joe Biden To Unilaterally Raise Tariffs?

On May 14, 2024, Joe Biden promulgated a memorandum to the US Trade Representative directing that certain tariffs against China be increased.

Section1. Tariffs. (a) The Trade Representative shall maintain, as appropriate and consistent with this memorandum, the ad valorem rates of duty and lists of products subject to the two actions, taken under the section 301 investigation. To further encourage China to eliminate the acts, policies, and practices at issue, and to counteract the burden or restriction of these acts, policies, and practices, the Trade Representative shall modify the two actions to increase section 301 ad valorem rates of duty for the following products from China:

We should take note that Biden grounded this memorandum in authorities granted under the Trade Act of 19744. However, the text of the memorandum opinion is clear: Joe Biden (or at least Joe Biden’s Autopen) unilaterally raised tariffs on Chinese goods. There was no intervening act of Congress. Joe Biden apparently had authority to regulate importation of Chinese goods by means of tariffs, but Donald Trump does not have authority to regulate importation of goods by means of tariffs.

Going back further into the Biden era, we must also note Biden’s Proclamation 10403 on steel imports into the US.

This Proclamation is significant not just because it is an exmplar of Joe Biden unilaterally revamping tariffs. Perversely, it is predicated on an earlier Presidential Proclamation issued by none other than….wait for it….Donald Trump.

2. In Proclamation 9705 of March 8, 2018 (Adjusting Imports of Steel Into the United States), the President concurred in the Secretary’s finding that steel articles, as defined in clause 1 of Proclamation 9705, as amended by clause 8 of Proclamation 9711 of March 22, 2018 (Adjusting Imports of Steel Into the United States), are being imported into the United States in such quantities and under such circumstances as to threaten to impair the national security of the United States, and decided to adjust the imports of those steel articles by imposing a 25 percent ad valorem tariff on such articles imported from all countries except Canada and Mexico. The proclamation further stated that any country with which we have a security relationship is welcome to discuss with the United States alternative ways to address the threatened impairment of the national security caused by imports from that country, and noted that, should the United States and any such country arrive at a satisfactory alternative means to address the threat to the national security such that the President determines that imports from that country no longer threaten to impair the national security, the President may remove or modify the restriction on steel articles imports from that country and, if necessary, adjust the tariff as it applies to other countries, as the national security interests of the United States require.

Moreover, Joe Biden functionally affirmed Donald Trump’s earlier unilateral imposition of tariffs by amending rather than revoking or rescinding the Trump Proclamation:

Now, Therefore, I, Joseph R. Biden Jr., President of the United States of America, by the authority vested in me by the Constitution and the laws of the United States of America, including section 232 of the Trade Expansion Act of 1962, as amended, section 301 of title 3, United States Code, and section 604 of the Trade Act of 1974, as amended, do hereby proclaim as follows:

(1) Clause 2 of Proclamation 9705, as amended, is revised to read as follows:

“(2)(a) In order to establish certain modifications to the duty rate on imports of steel articles, subchapter III of chapter 99 of the HTSUS is modified as provided in the Annex to this proclamation and any subsequent proclamations regarding such steel articles.

In issuing Proclamation 10403, Joe Biden suspended steel tariffs on imports from a number of countries, including Mexico and Ukraine. While this is the reverse of imposing a tariff, setting a tariff to zero is the same exercise of tariff authority as imposing a tariff. Again, this is a unilateral wielding of tariff authority by Joe Biden, without any intervening legislation by Congress.

Biden unilaterally wielded tariff authority several times, including a further amendment of the Trump-era Proclamation 9705 with Proclamation 10771 on May 31, 2024, extending tariff suspensions in many cases into 2025.

Presidents may not have inherent tariff authority, but Joe Biden indisputably exercised tariff authority and that discomfited no-one, not even Chief Justice John Roberts.

Legal Precedent For IEEPA Tariff Authority?

Notably, Biden’s Proclamations 10771 and 10403, and Trump’s Proclamation 9705, reference the same law, section 232 of the Trade Expansion Act of 19625.

Consider the statutory language6 of the cited section:

(c) Adjustment of imports; determination by President; report to Congress; additional actions; publication in Federal Register

(1)(A) Within 90 days after receiving a report submitted under subsection (b)(3)(A) in which the Secretary finds that an article is being imported into the United States in such quantities or under such circumstances as to threaten to impair the national security, the President shall—

(i) determine whether the President concurs with the finding of the Secretary, and

(ii) if the President concurs, determine the nature and duration of the action that, in the judgment of the President, must be taken to adjust the imports of the article and its derivatives so that such imports will not threaten to impair the national security.

(B) If the President determines under subparagraph (A) to take action to adjust imports of an article and its derivatives, the President shall implement that action by no later than the date that is 15 days after the day on which the President determines to take action under subparagraph (A).

(2) By no later than the date that is 30 days after the date on which the President makes any determinations under paragraph (1), the President shall submit to the Congress a written statement of the reasons why the President has decided to take action, or refused to take action, under paragraph (1). Such statement shall be included in the report published under subsection (e).

(3) (A) If—

(i) the action taken by the President under paragraph (1) is the negotiation of an agreement which limits or restricts the importation into, or the exportation to, the United States of the article that threatens to impair national security, and

(ii) either—

(I) no such agreement is entered into before the date that is 180 days after the date on which the President makes the determination under paragraph (1)(A) to take such action, or

(II) such an agreement that has been entered into is not being carried out or is ineffective in eliminating the threat to the national security posed by imports of such article,

the President shall take such other actions as the President deems necessary to adjust the imports of such article so that such imports will not threaten to impair the national security. The President shall publish in the Federal Register notice of any additional actions being taken under this section by reason of this subparagraph.

(B) If—

(i) clauses (i) and (ii) of subparagraph (A) apply, and

(ii) the President determines not to take any additional actions under this subsection,

the President shall publish in the Federal Register such determination and the reasons on which such determination is based.

Note the word that is not present in this section: “duties” (governmentspeak for “tariffs”).

Indeed, the singular and plural forms of “duty” appear only once in the statutory language, and that is in subsection (a), which prohibits their elimination if so doing is deemed injurious to national security.

(a) Prohibition on decrease or elimination of duties or other import restrictions if such reduction or elimination would threaten to impair national security

No action shall be taken pursuant to section 1821(a) of this title or pursuant to section 1351 of this title to decrease or eliminate the duty or other import restrictions on any article if the President determines that such reduction or elimination would threaten to impair the national security.

Nowhere does this section of the US Code, which is cited in multiple Presidential proclamations by both Donald Trump and Joe Biden, say that the import regulation authority includes authority to levy tariffs. Yet this “ambiguous” text is not troubling to Roberts at all.

Turning to this Court’s precedents, the Government first relies on Federal Energy Administration v. Algonquin SNG, Inc., 426 U.S. 548 (1976). There, we held that Section 232(b) of the Trade Expansion Act of 1962, which allows the President to “adjust the imports” of particular goods to protect national security, includes the power to impose “license fees.” Id., at 561. But that holding bears little on the meaning of IEEPA. As a textual matter, Section 232(b) authorizes the President not only to “adjust . . . imports,” but (as the Government emphasized in Algonquin) to “take such action . . . as he deems necessary” to adjust the imports of a good. Brief for Petitioners 26 (emphasis in original) and Tr. of Oral Arg. 6–7, in Federal Energy Administration v. Algonquin SNG, Inc., O. T. 1975, No. 75–382. IEEPA does not contain such sweeping, discretion-conferring language. As for context, Section 232(a) states that “[n]o action shall be taken” to “decrease or eliminate” an existing “duty or other import restriction” if doing so would threaten national security. 19 U. S. C. §1862(a) (1970 ed.). This explicit reference to duties preceding Section 232(b) renders it natural for Section 232(b) itself to authorize duties. Thus, we decline to extend Algonquin’s expressly “limited” holding any further. 426 U. S., at 571.

I will invite readers to review the statutory language of the IEEPA mentioned above, and decide for themselves how “sweeping” and “discretion-conferring” that language is.

I will note that Roberts offers no elucidation of how the text of the IEEPA differs in substantive scope from the text of the Trade Expansion Act. He merely says “but that’s different.” Rational persons understand that extraordinary claims require extraordinary evidence, but Roberts offers no evidence to support this extraordinary claim. As a matter of simple logic, that is a major flaw in the reasoning his opinion constructs.

Despite Roberts demonstrably flawed logic, the reality cannot be avoided. President Trump during his first Administration wielded unilateral tariff authority, and Joe Biden when he was in office not only ratified Trump’s wielding of unilateral tariff authority but proceeded to wield it himself multiple times.

As Section 232 of the Trade Expansion Act of 1962 is permissible as a citation of tariff authority, despite not mentioning tariffs (actually “duties”) other than to restrict their diminution when there are national security implications, how is the IEEPA impermissible as a citation of tariff authority? On a strictly textual basis, the two statutes are similar in scope and function:

The IEEPA operates under declaration of national emergency, while Section 232 operates under conditions of national security.

Neither statute is limited to specific countries or global regions. The language in both is inherently global in nature.

Neither statute time delimits the imposition of any import regulation or restriction. The IEEPA authority endures so long as a declared national emergency endures, while Section 232 prevails so long as national security concerns are otherwise unmet.

If anything, a textual comparison of the statutes indicates they are both equally broad and equally “ambiguous”.

Justices Thomas, Kavanaugh, and Alito Call BS On John Roberts

While Justice Clarence Thomas’ dissenting opinion7 is worth reading in full, to appreciate how badly flawed Roberts majority opinion is we need only note Thomas’ first paragraph, where he flatly rejects Roberts’ opinion as factually false.

I join Justice Kavanaugh’s principal dissent in full. As he explains, the Court’s decision today cannot be justified as a matter of statutory interpretation. Congress authorized the President to “regulate . . . importation.” 50 U. S. C. §1702(a)(1)(B). Throughout American history, the authority to “regulate importation” has been understood to include the authority to impose duties on imports. Post, at 9–13, 22–29 (Kavanaugh, J., dissenting). The meaning of that phrase was beyond doubt by the time that Congress enacted this statute, shortly after President Nixon’s highly publicized duties on imports were upheld based on identical language. Post, at 14–22. The statute that the President relied on therefore authorized him to impose the duties on imports at issue in these cases. Justice Kavanaugh makes clear that the Court errs in concluding otherwise.

Even the usually reserved Justice Brett Kavanaugh, writing his own dissent8 (and joined by Justice Samuel Alito), was nonplussed by Roberts’ false and misleading presentation of US history and US law.

Since early in U. S. history, Congress has regularly authorized the President to impose tariffs on imports of foreign goods. Presidents have often used that authority to obtain leverage with foreign nations, help American manufacturers and workers compete on a more level playing field, and generate revenue for the United States. Numerous laws such as the Trade Expansion Act of 1962 and the Trade Act of 1974 continue to authorize the President to place tariffs on foreign imports in a variety of circumstances, and Presidents have often done so. In recent years, Presidents George W. Bush, Obama, and Biden have all imposed tariffs on foreign imports under those statutory authorities.

As the Biden-era Proclamations I have quoted here demonstrate, the wielding of unilateral tariff authority by a President is neither unprecedented nor, prior to the Liberation Day tariffs, particularly controversial. Roberts’ claims in this regard are simply not true.

Even worse, Roberts’ dismissal of the IEEPA text as “ambiguous” while defending the equally “ambiguous” text of the Trade Act of 1962 is disingenuous to the point of dishonest. The argument lacks credibility because it lacks factual foundation. Both the IEEPA and the Trade Act of 1962 are textually similar and grounded in similar situations, national emergency vs national security threat.

The reality of legislation such as the Trade Act of 1962 is that these statutes obviate the need for particular language within the IEEPA to establish tariff authority for the President. As the President already enjoys broad tariff authority because of similar legislation, for the purposes of the IEEPA tariff authority must be presumed, not rejected.

Yes, the Constitution delineates taxation and regulation of foreign commerce as separate powers of Congress, but the realities of both exercising and delegating these powers inextricably link them together. Where the one goes the other quickly follows.

Those realities collapse Roberts’ reasoning entirely, and leave his majority opinion in a decidedly awkward place for a Supreme Court opinion: repugnant to the Constitution.

As a matter of law and Supreme Court precedent, we should regard the Roberts ruling as void, and with no legal effect. Roberts got the law wrong, and that disqualifies his opinion from enjoying either credibility or legal validity.

The Liberation Day tariffs remain legal. The Liberation Day tariffs remain Constitutional. Roberts rambling nonsense cannot and should not be understood to change that reality.

Learning Resources, Inc. v. Trump, 607 U.S. ___ (2026)

Learning Resources, Inc. v. Trump, 607 U.S. ___ (2026) (Gorsuch, J., concurring)

"stare decisis." A Law Dictionary, Adapted to the Constitution and Laws of the United States. By John Bouvier.. 1856. 21 Feb. 2026 https://legal-dictionary.thefreedictionary.com/stare+decisis

Learning Resources, Inc. v. Trump, 607 U.S. ___ (2026) (Thomas, J., dissenting)

Learning Resources, Inc. v. Trump, 607 U.S. ___ (2026) (Kavanaugh, J., dissenting)

Bravo, Peter, for once again shining with your astoundingly good legal mind!

So, we’ve got several Supreme Court Justices with Trump Derangement Syndrome. What’s the solution, besides waiting for them to die off?

I'm not an American. From where I sit the problem hinges on whether there is an Emergency or not. If there really is an emergency, then an executive may need to ignore or circumvent the normal rule of law just to get what is needed done in an urgent fashion. If there is no emergency, then the declaration of one is tyrranical, and sets the dangerous precedence of "Declaring an Emergency" to be the first act of all Presidents. The court seems a reasonable enough place for deciding whether a state of Emergency existed at all. And since Justice Kavanaugh's dissenting opinion listed exactly how the executive could continue to get the tariffs it wants without the IEEPA, this looks like a win for everybody from over here.

It also looks, from over here, that the real emergency is that the Congress is no longer doing its job of legislating, and is leaving things that should be a matter of law to be done through regulations written by unelected bureacrats. That's a different, but no less potent source of tyrrany. But I have no clue what it is in the American system of checks and balances that is supposed to discipline a rogue or ineffectual Congress. Can the Supreme Court order that Congress sit down and at least attempt to legislate on a matter? or what?