June Jobs Reports: Labor Stumbles?

Overall Strong Jobs Data Cannot Conceal Continuing Weaknesses

The Independence Day holiday makes for a busy start to July, and the recent Supreme Court rulings have captured much attention. As a result, this month I am examining the ADP National Employment Report and the BLS Employment Situation Summary (ESS) together, rather than separately as I have been doing.

The common thread in both jobs reports: Job growth slowed in June. ADP reported 98,000 jobs created, down from 122,000 jobs in May.

The BLS jobs report showed an even greater cooling of labor markets, with job growth slowing to 57,000.

Both total nonfarm payroll employment (+57,000) and the unemployment rate (4.2 percent) changed little in June, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in professional and business services, social assistance, and health care. Leisure and hospitality lost jobs.

Both numbers were well below Wall Street as well as Trading Economics projections. Wall Street had anticipated ADP would report 113,000 jobs created in June.

Wall Street had similar expectations for the BLS jobs report at 110,000 jobs.

The job growth was there, just much less of it than was forecast.

Neither the ADP nor the BLS jobs reports are, on the surface, particularly bad jobs reports. Both reports are considerably cooler snapshots of US labor markets than we have seen in recent months.

While the headline numbers for both reports are not altogether bad numbers, when we delve into the details we quickly see that labor stumbled in June, with a number of sectors shedding jobs rather than adding them.

The June job reports are not altogether bad reports, but the strength of the overall jobs numbers cannot conceal the reality of continuing weaknesses within US labor markets.

We may not be backsliding into a jobs recession…yet. We are still very much at risk of a return to jobs recession, and without a lot of advance warning.

May JOLTS Was Right About Downward Revisions

One the more significant cautionary notes found in the May JOLTS data was the warning signal that the Employment Situation Summary may be about to experience significant downward revisions.

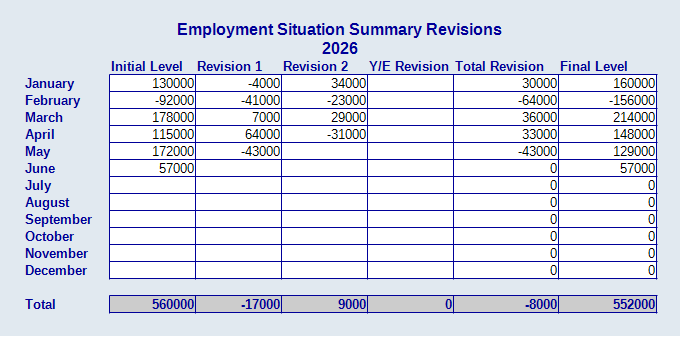

That warning signal proved to be prescient, for the June ESS had major downward revisions for both April and May.

The change in total nonfarm payroll employment for April was revised down by 31,000, from +179,000 to +148,000, and the change for May was revised down by 43,000, from +172,000 to +129,000. With these revisions, employment in April and May combined is 74,000 lower than previously reported.

This abrupt elimination of 74,000 previously reported jobs erased last month’s achievement of year to date job revisions printing positive.

Total year to date revisions to the jobs data is now down 8,000 jobs.

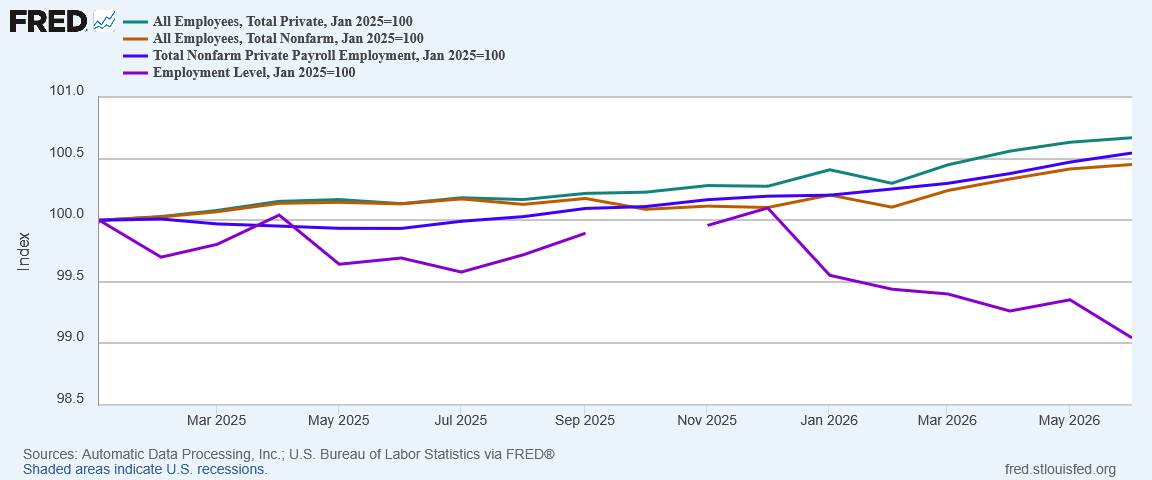

The June jobs report gives us another warning signal as well: signs that Lou Costello Labor Math is still lurking within the overall data set, as the Employment Level from the Household Survey once again broke with from the All Employees metrics within the Establishment Survey.

Given that both the Household and Establishment Surveys are supposed to be measuring the same overall data—the American labor force—we should expect similar growth trends within both surveys. In June the Employment Level dipped again in a clear divergence from the All Employees trends.

When the two surveys are not reporting similar trends, we must be cautious about what to make of the data.

Sector Results Were Uneven

ADP’s Chief Economist Dr. Nela Richardson summed up the sector results for both the ADP and BLS data sets succinctly as a slowdown in job growth.

The pace of hiring is telling a story of both supply and demand. We know it’s taking people longer to find work, but there also are signs of labor supply constraints in certain industries. For now, the overall effect is a slowdown in job creation.

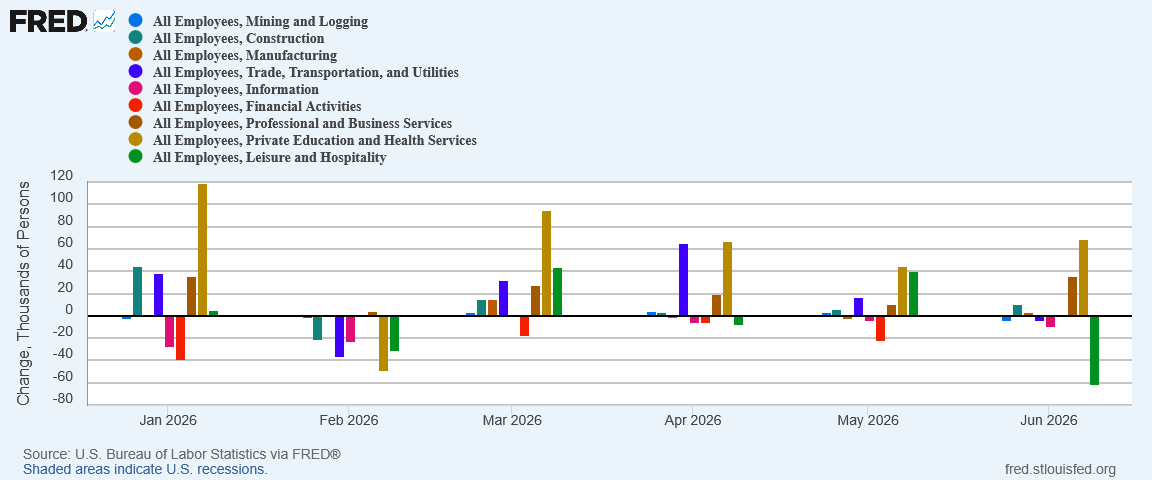

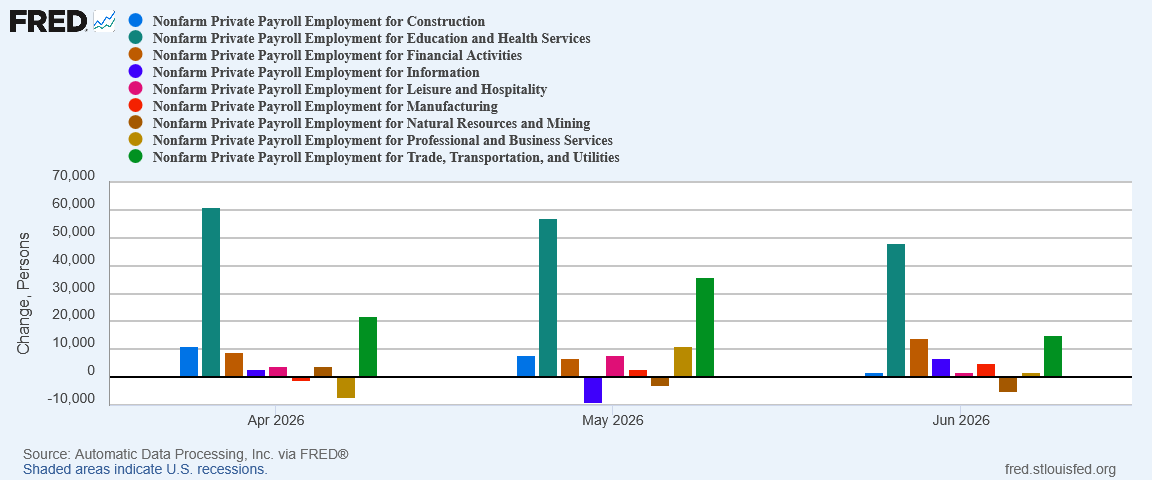

While the headline numbers were not bad—the ADP headline number would have been quite good were it not a climbdown from May’s much stronger figure—they obscure the weakness reemerging in several sectors. Several sectors lost jobs in June, according to the ESS.

ADP was more optimistic, although there is still a clear cooling trend in the data.

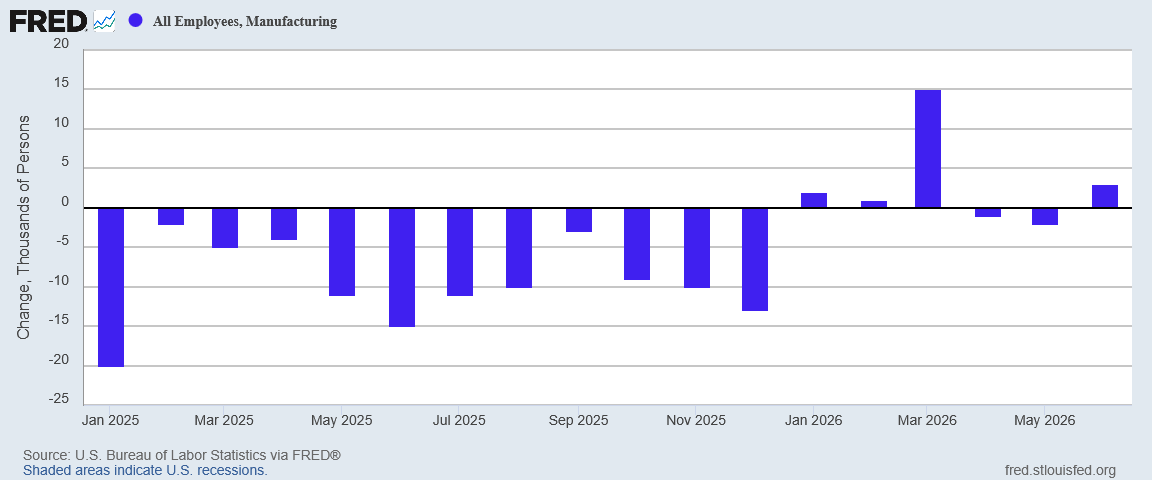

The BLS data for manufacturing was again one of the brighter spots in the ESS report. Although the downward revisions wiped out the past two months’ positive job numbers for the manufacturing sector, the June data still showed job growth for the sector.

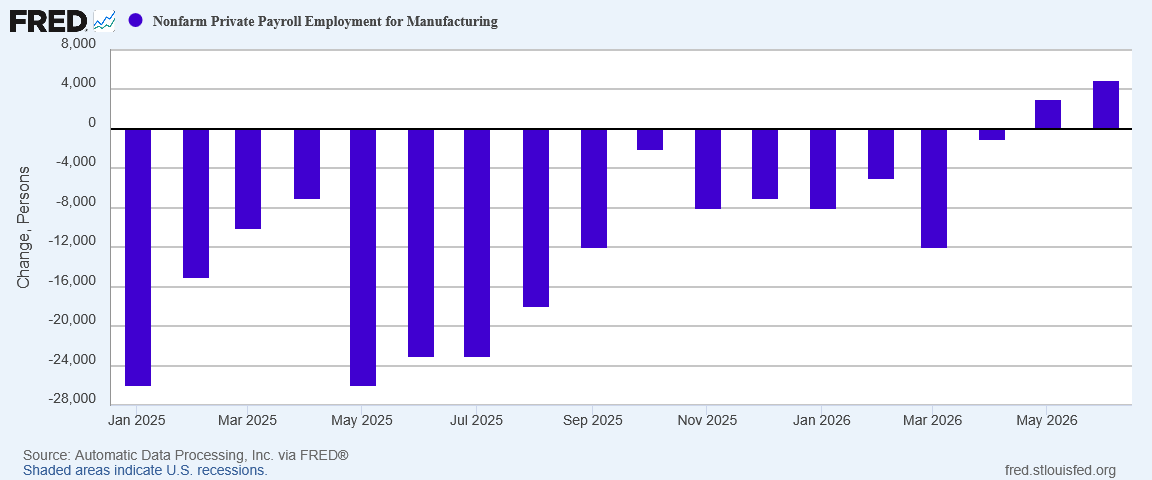

ADP showed manufacturing job growth gaining steam in June.

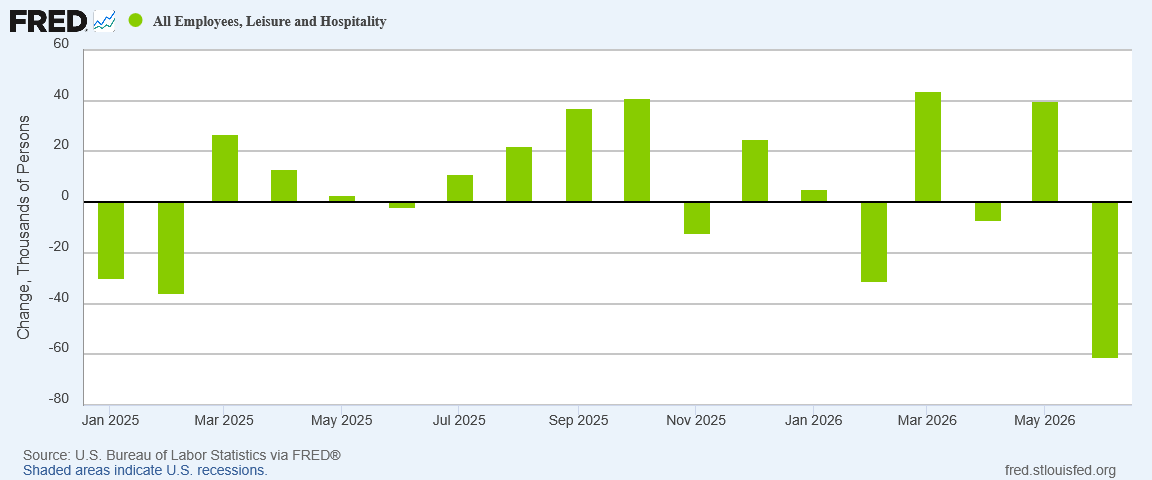

The ESS print shows Leisure as the worst performing sector in June, shedding a shocking 61,000 jobs.

From the revised May figure of 40,000 jobs created, in June Leisure job growth suffered a 100,000-plus shift from job creation to job destruction.

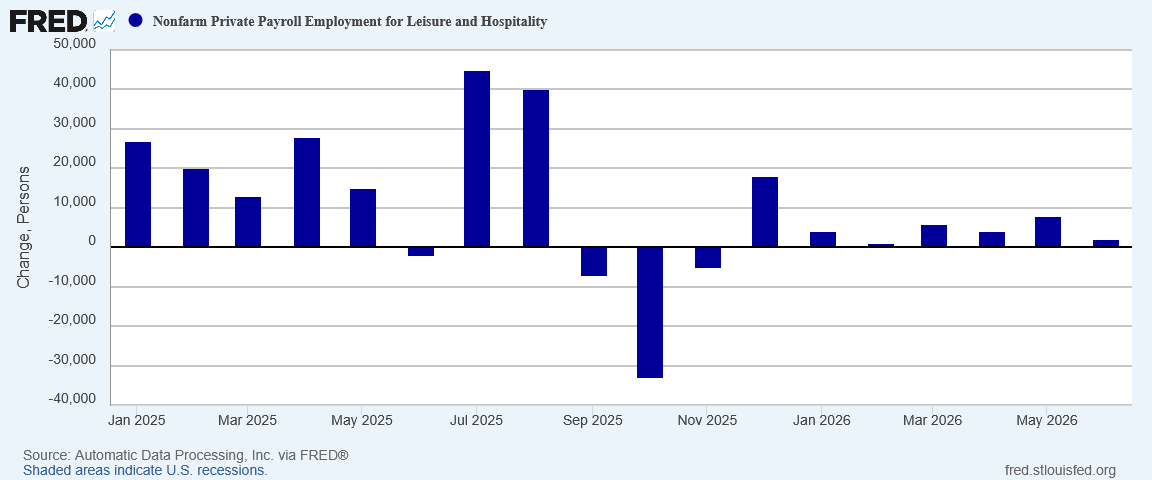

ADP tells a different, more muted, job growth story for the Leisure sector, printing job growth of 2,000 jobs in June.

Leisure job growth cooled in June, but it did not go into the deep freeze reported on the ESS.

The ESS and ADP reports also differed in jobs numbers for Information as well as Financials Services. In June ESS printed 0 job growth for Finance and 9,000 jobs lost for Information. ADP reported 14,000 jobs for Finance and 9,000 for Information.

One sector were the ESS and ADP data largely agree is Mining, which the ADP report prints as losing 5,000 jobs, and the ESS printing job loss of 4,000.

Both the ESS and the ADP reports show Healthcare returning to its status as the dominant sector for job growth, with the ESS printing 69,000 jobs in June and ADP printing 48,000 jobs.

Where the reports differ on Healthcare is ADP shows the job growth cooling in recent months, while the ESS report shows Healthcare having something of a rebound in June.

Overall, while both jobs report show job growth cooling in June, the ESS data is the more pessimistic not only in showing less job growth, but also in a cooling trend from peak job growth in March. The ADP data shows stronger job growth as well as job growth at a peak in May before cooling in June.

The one aspect of job creation for the US where the reports are clearly in agreement is that job growth for June was more uneven than was reported in April or May—although with revisions the Employment Situation Summary is proving to have been more uneven than originally reported, to the surprise of exactly no one (at least, no one who follows my work!).

The ESS in particular has snatched part of the employment rug out from under everyone’s feet, taking back a substantial portion of the glowing job growth narrative of the past two months. We still have job growth, we still have manufacturing job growth, but we have quite a bit less than we have been told in both April and May.

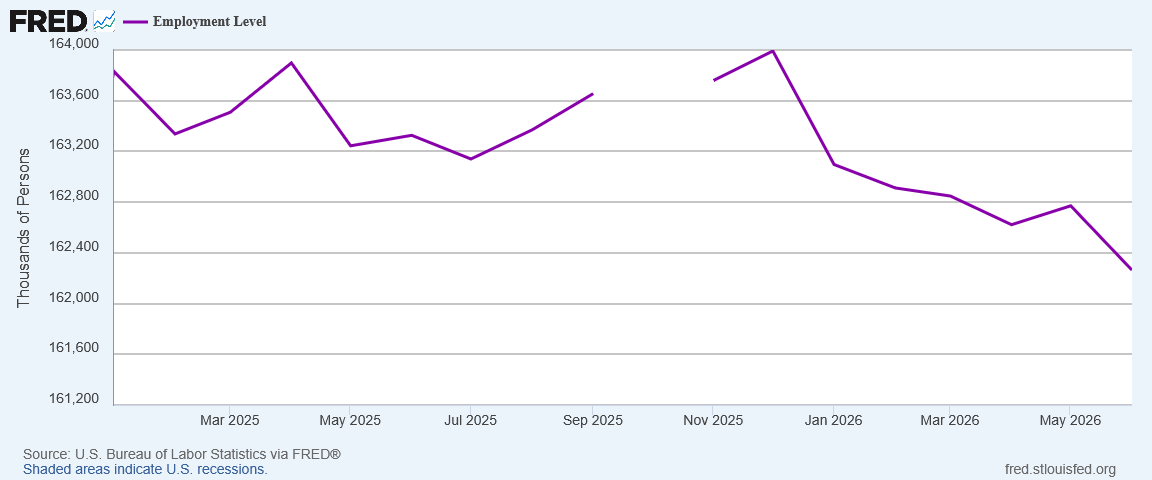

Employment Level Declined Again

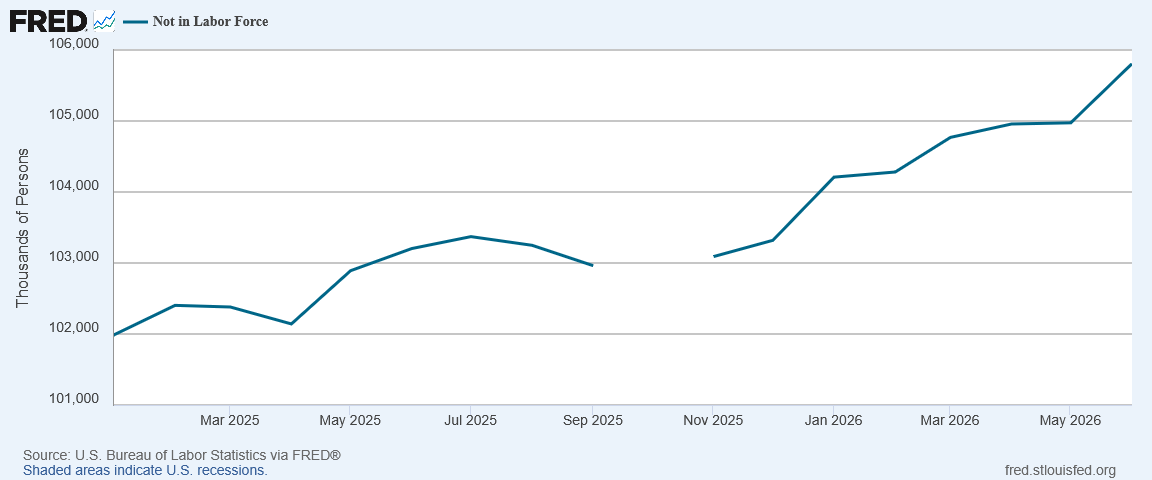

A major warning signal coming from the Employment Situation Summary is the decline in the overall Employment Level, which declined by some 507,000 individuals in June.

May apparently was a brief hiatus from a decline in overall employment from a December 2025 peak.

If we look at just the Employment Level data from the ESS’ Household Survey, we would see employment declining throughout 2026 to date, with only last month showing any respite from the contraction in the employed labor force.

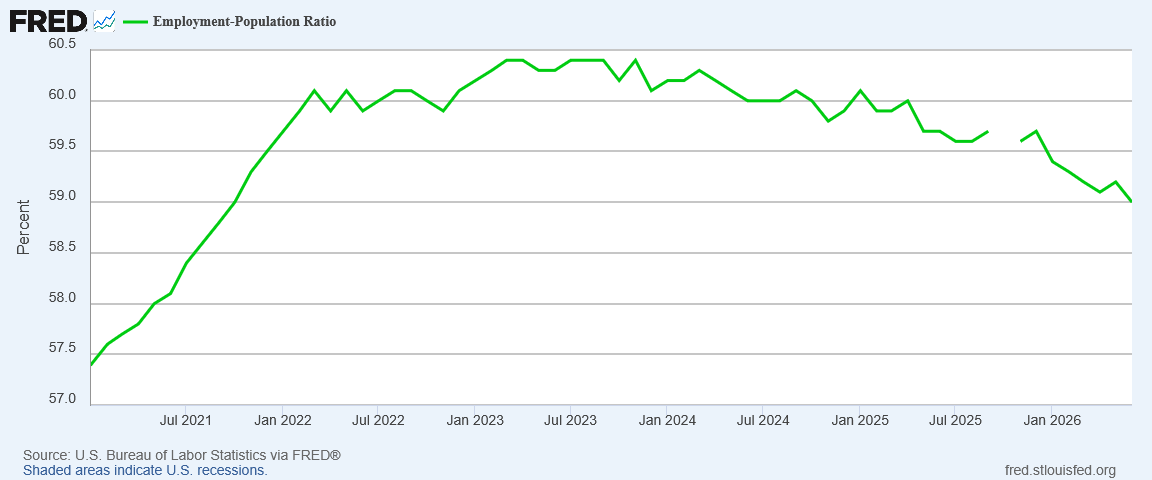

The Employment-Population Ratio shows a much longer-term decline, beginning back at the end of 2023.

For all the reports of job growth in the ESS’ Establishment Survey data, the Household Survey continues to tell a tale of fewer and fewer people working over time, and a smaller segment of the population.

The Establishment Survey data might spin an optimistic narrative of job growth and jobs recovery within the US economy, but the Household Survey is challenging the jobs recovery narrative.

Declining Joblessness?

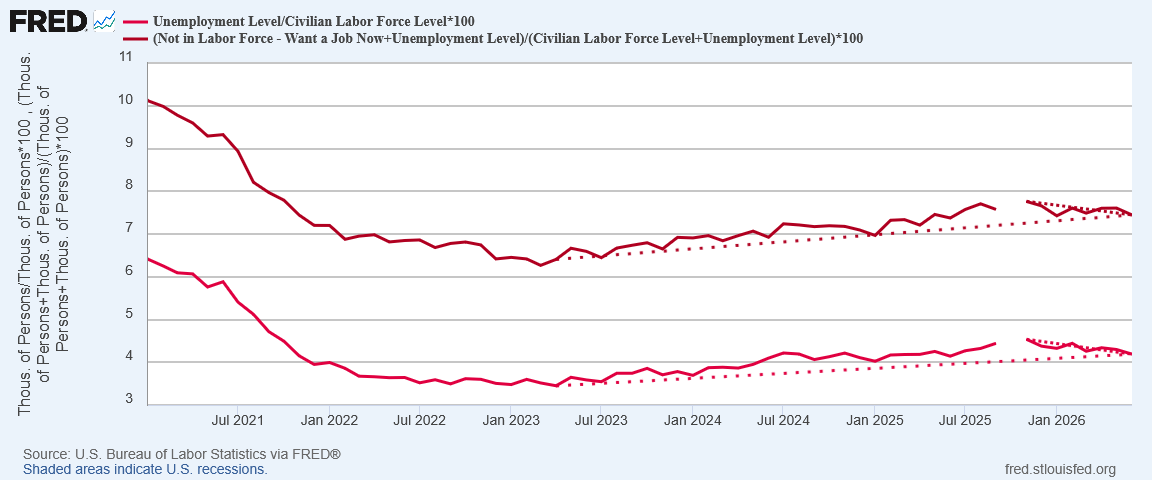

Despite the grim outlook on the nation’s overall employment level, unemployment actually dropped in June, in both the official and “real” unemployment rate metrics.

Both gauges of unemployment fell by approximately a tenth of a percentage point. The official unemployment rate fell from 4.3% to 4.2% in June. The real unemployment rate, still higher as I include with the unemployed people those not in the labor force but who want a job now in calculating that percentage, dropped a little bit more, from 7.61% to 7.45%.

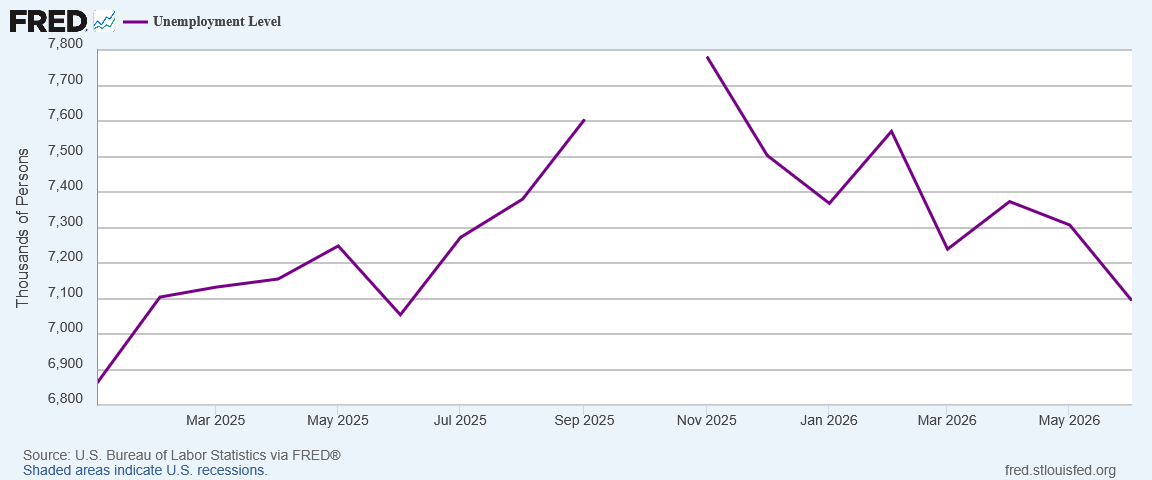

Looking at the reported numbers of unemployed individuals, official unemployment for June declined in this country by 213,000 people.

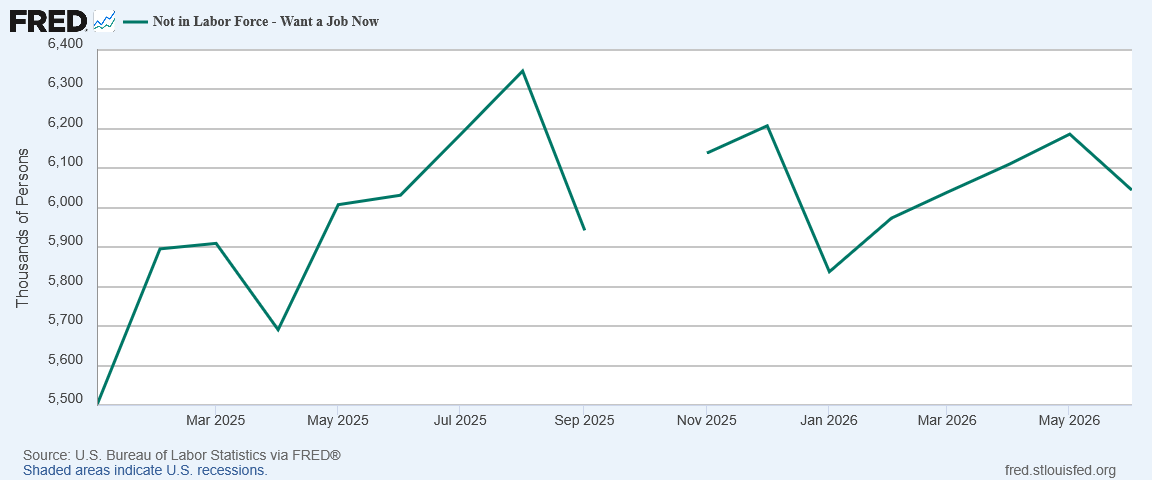

Even the number of people not in the labor force but who want a job now dropped in June by 142,000.

Paradoxically, even as the Household Survey shows fewer people working, it also shows fewer people not working but still looking for work.

However, while the cohorts of people not working but looking for work declined, the overall number of people not in the labor force rose in June, surging by 832,000.

These are curious trends, and disturbing trends. Taken as a whole they suggest that people who lose their jobs are, in increasing numbers, simply giving up on working.

That is not a healthy trend for any economy. Is the United States seeing a labor phenomenon similar to the “lying flat” trend among younger Chinese workers? The data tells us that may be exactly what is happening.

Wage Growth Disappoints Overall

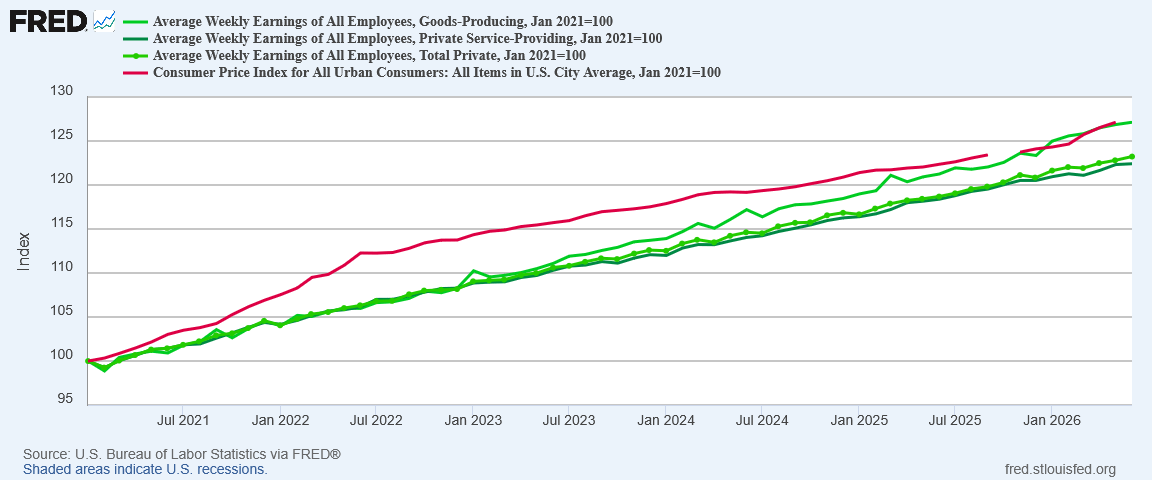

Paychecks proved another disappointment in the June ESS. While wage growth is still occurring, in June it appears to have continued the recent trend of losing ground to inflation once again.

We have yet to see the June CPI print, but unless it flatlines for the month, wage growth will still prove to have been less than inflation.

When wages can't keep up inflation becomes a major economic concern as well as a political one. With less money to spend relative to rising prices, workers’ overall consumption is restrained, and that means economic growth is constrained.

Since the start of Operation Epic Fury and the war with Iran, wages have not kept pace with inflation. That does not augur well for overall consumption in the second quarter. With less real income, people overall have less means for consumption, which will push down economic growth in this country.

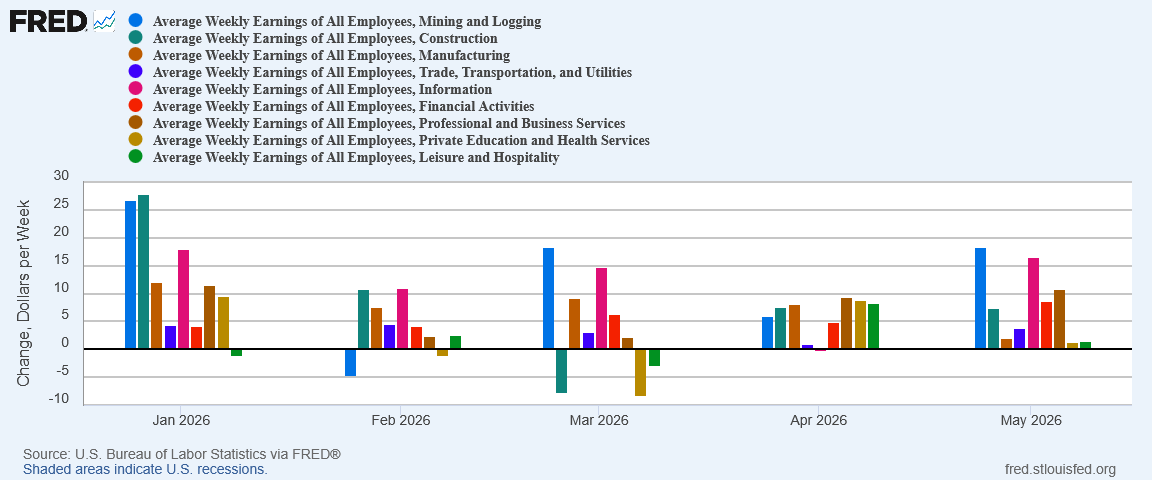

In another demonstration of how uneven the June jobs data is, the changes in nominal pay became more highly volatile during the month.

Curiously, or perhaps a reflection of the broader implications of shifting job growth numbers among sectors, the sectors who lost jobs showed the most wage gain, while the sectors showing job growth also printed slower wage growth.

Strictly speaking, wages are the “price” of labor. If labor demand is falling in a particular sector, as evidenced by job loss for the month, then we would expect to see slower wage growth as well.

In the real world, wages are a good deal less elastic. It is quite possible the shifts in wage growth are at least in some measure a direct consequence of May’s job growth numbers.

Continuing Jobs Recovery Or Slide Back Into Jobs Recession?

The overarching question surround the jobs data is whether or not we are seeing a continuing jobs recovery, or seeing labor markets in the US slipping back into recession?

While the June jobs data shows a slowdown in job growth, it still shows job growth. Relative to prior months, the June data still shows fairly robust jobs growth. Before March, an ESS jobs print of 57,000 jobs would have been unanimously viewed as a strong jobs report. We would have said the same thing about an ADP print of 98,000 jobs for the month.

Even after the robust job increases of April and May, both the ADP and ESS reports are still respectable reports showing in the aggregate respectable job growth.

Yet the data remains troubling. Any month where the Household Survey data diverges from the Establishment Survey data is a month where we must take all the data with an extra large grain of salt, as Lou Costello Labor Math means the overall numbers do not add up.

June was a month where the Household Survey diverged from the Establishment Survey. The numbers do not add up.

As robust as job growth numbers have been recently, wage growth remains a disappointment, as rising inflation is overwhelming increases in workers’ paychecks.

Are we seeing a continuing jobs recovery, or are we seeing labor markets in the US slipping back into recession?

On the strength of just the June data, it would be premature to call an end to the nascent jobs recovery we have seen over the past few months. The sector level numbers are in many sectors a disappointment, but other sectors did very well, more than compensating for job losses elsewhere. Wage growth is again a disappointment, but largely because of rising inflation pressures undercutting wage gains.

At the same time, the jobs data is warning us that all is far from well in US labor markets. The jobs data is telling us that the employed labor force is declining, and that workers as a percentage of the overall population are declining. The jobs data is indicating that if workers leave the labor force, they are giving up on working altogether.

Are workers choosing “lying flat” over searching for a job? That is certainly one interpretation of the data. If we see similar shifts among the civilian labor force and those no longer in it, we may have to pay particular attention to that interpretation.

The June jobs data shows cooler job growth than in May, by a wide margin. On just about every metric, June was a worse month for jobs than May.

The June jobs numbers are technically “not bad”, but the June jobs reports make it clear that labor stumbled. That’s never a good shift in the narrative, and if the numbers do not move back in the direction of more robust job growth over the coming months, it could mean that the jobs recovery is already petering out, and a jobs recession is coming back into the picture.

A return to jobs recession is of course a bad thing, and that would make the June jobs reports bad reports. We are not there yet, but we have moved away from where we can say the reports are unambiguously good reports.

Labor stumbled in June. Hopefully labor stumbles only in June.

You’re ahead of the pack as usual, finding the troubling data. At least manufacturing looks good, and that is a large part of the engine of our economy. But the large drop in leisure-related jobs indicates that people have less disposable income to spend on having fun. Not good.

Peter, the small gift I ordered for you nearly five weeks ago is still ambling about the country. For the past week it’s been mired in a California Post Office facility, where apparently the potheads who work there are too stoned to find San Antonio on a map. Sigh. Well, it won’t get to you by the Fourth of July, but it should still show up someday. I’ve added a small ko-fi tip as compensation for the delay. The gifts are in appreciation of your consistent and eloquent work to promote the true ideals of America - thank you, thank you, excellent Patriot!