June PPI: Producer Prices Ran Hot, Now Run Cold

Again We Must Ask: What Is The Producer Price Index Trying To Tell Us?

In a repeat of the June Consumer Price Index Summary, the June Producer Price Index Summary can also be summed up in a single word: deflation.

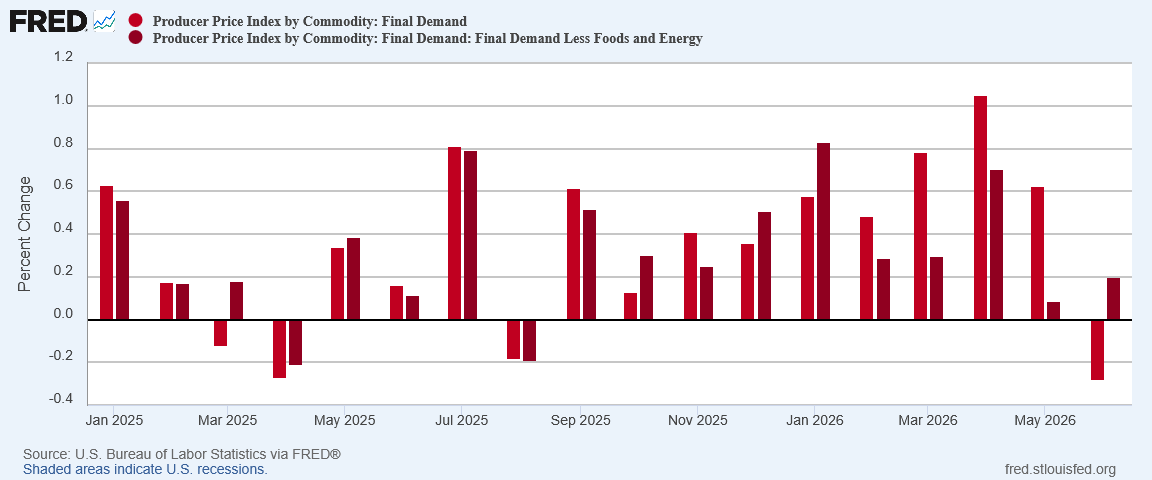

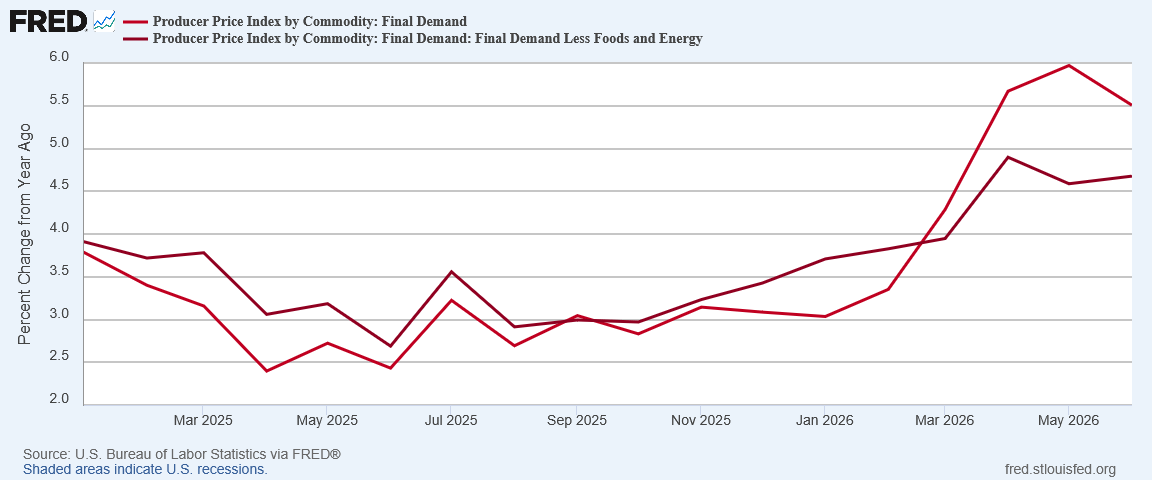

The Producer Price Index for final demand fell 0.3 percent in June, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices advanced 0.6 percent in May and 1.1 percent in April. (See table A.) On an unadjusted basis, the index for final demand increased 5.5 percent for the 12 months ended in June.

After the broad price declines from the June CPI report, there is less surprise that the PPI print shows something similar. What is surprising, however, is that, unlike headline consumer price inflation, which had been cooling over the past couple of months after an initial spike in March, headline producer price inflation had not cooled.

In May PPI was running hot. In June PPI was running cold.

What should we make of this very large swing in producer prices?

Is this another signal that the mini-stagflation scenario of the past few months has ended even before it could get seriously underway?

Is this a signal that more deflation has yet to come? Possibly. If that is the case the collapse in price supports across the board could mean that a longer term deflationary trend has taken hold, and the United States is heading into another “lost decade” of minimal or no economic growth.

What is the Producer Price Index trying to tell us? That is an excellent question—lets peel back the layers of data to see if we can construct an excellent answer.

PPI Is Telling Us Prices Are Still Falling—Sort Of

Recognizing that the Producer Price Index broadly serves as a leading indicator for the Consumer Price Index, the most obvious signal we can see in the PPI data is that prices are still falling—sort of.

As the BLS press release noted, headline producer prices dropped 0.3% month on month in June.

However, core producer price inflation went up month on month, from 0.09% to 0.2%

Pulling back to look at producer price inflation year on year, the headline index eased to 5.5%, but core inflation rose from 4.6% to 4.7%.

Unlike consumer prices, producer prices did not fall across the board in June. Some goods and services are still seeing rising producer prices.

The headline PPI index suggests that we will not see significant inflationary pressure in the headline consumer price inflation data for at least the next month or so. With the core CPI print remaining constant year on year and the core PPI print moving up by 0.1pp, we may see some incremental increases in some core prices, even as prices overall trend down.

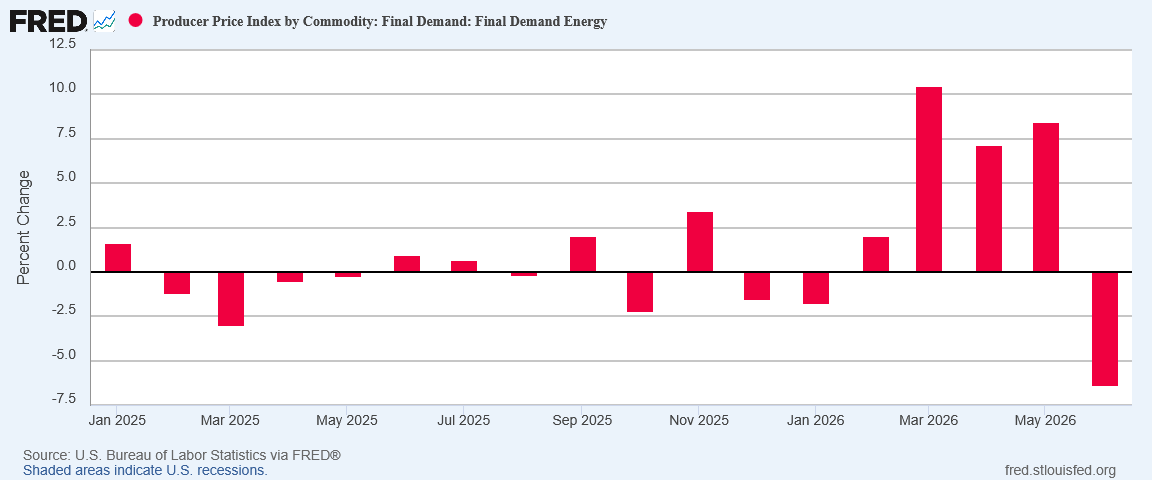

Energy Price Inflation Is Correcting Itself

In a repeat of the CPI data, the Producer Price Index for Energy dropped month on month by a fairly substantial 6.4%.

With oil prices having dropped throughout the month of June, this really should be no surprise at all.

Although the ceasefire with Iran is now over, declaring that ceasefire and reopening the Strait of Hormuz has proven hugely beneficial to energy prices in the near term.

If we go by just the data, the Producer Price Index for Energy is telling us that energy prices are still correcting, which would indicate we will see further energy price deflation in July within the CPI. However, we must buffer that thought with the reality that the price of oil is rising again, which will curtail whatever further price deflation the PPI appears to forecast for energy products.

We may see some further energy price deflation in July, but with oil having risen over $12/bbl for West Texas Intermediate, we should expect energy price inflation to return.

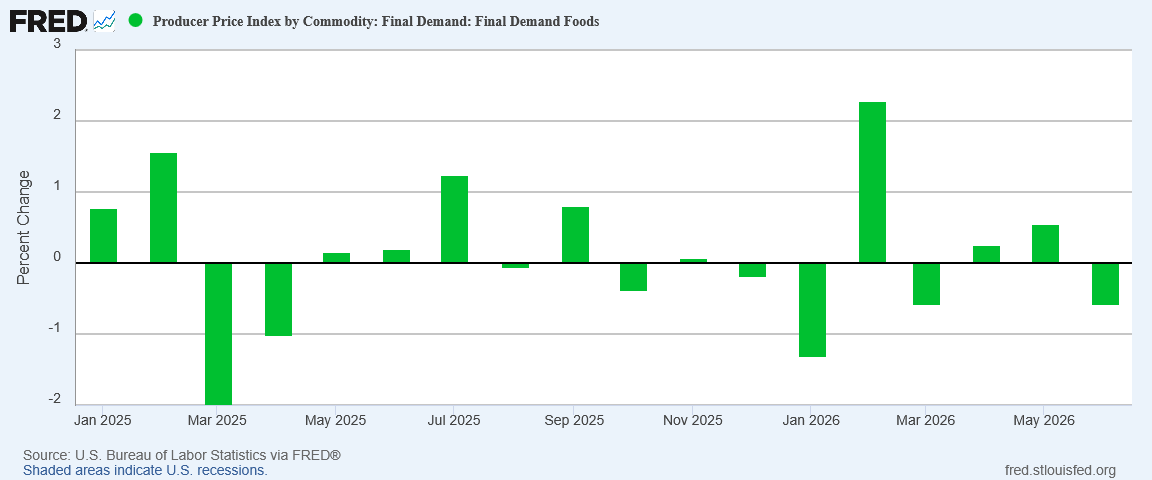

Food Prices Should Remain Stable

For food prices, the PPI report is quite at odds with the CPI report.

While the CPI data shows food price inflation heating up somewhat in June, the PPI data shows food prices in outright deflation, month on month.

This may be a stabilizing signal. If food prices are rising now, but are on track to fall again next month, overall food prices are neither trending up nor down.

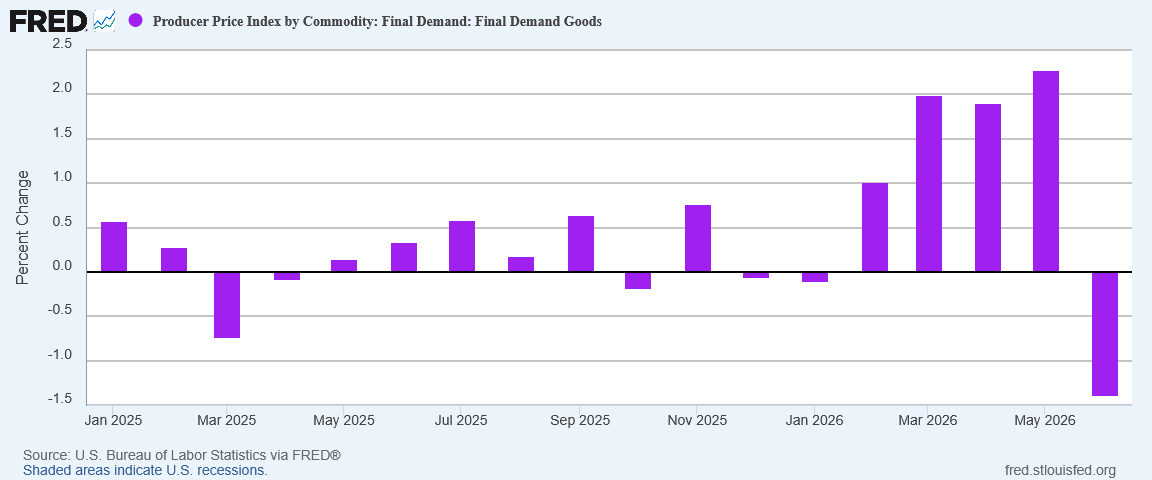

We could be seeing the same balancing act in other subindices. PPI for Goods, for example, saw producer price inflation heating up in April and May, only to drop significantly in March.

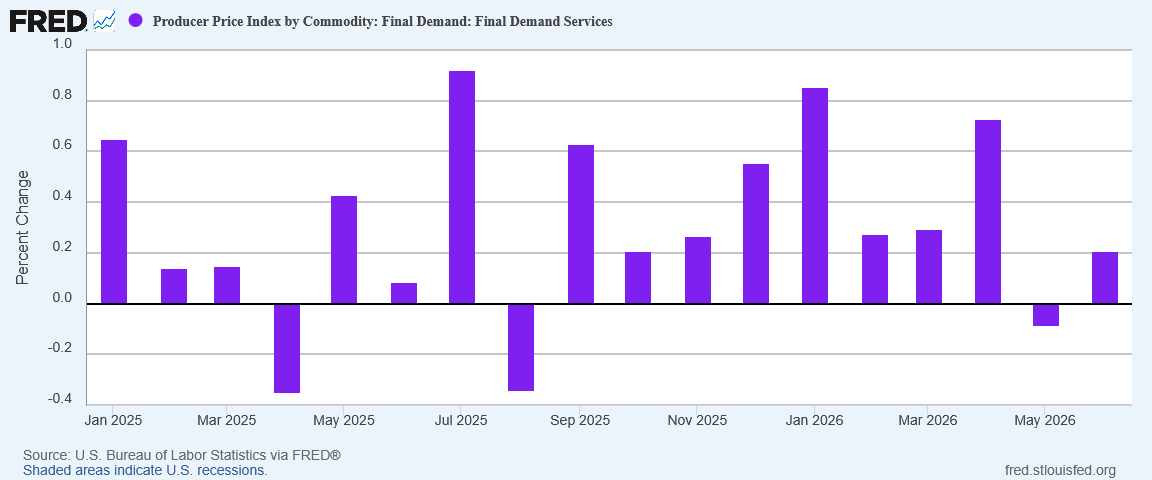

Services, on the other hand, actually rebounded into producer price inflation for June, after printing deflation in May.

Considering that core producer price inflation rose slightly in June, we may very well be seeing indications that core consumer price inflation will be moving up over the summer, even as energy prices continue to fall. What we are not seeing are signs of nascent hyperinflation.

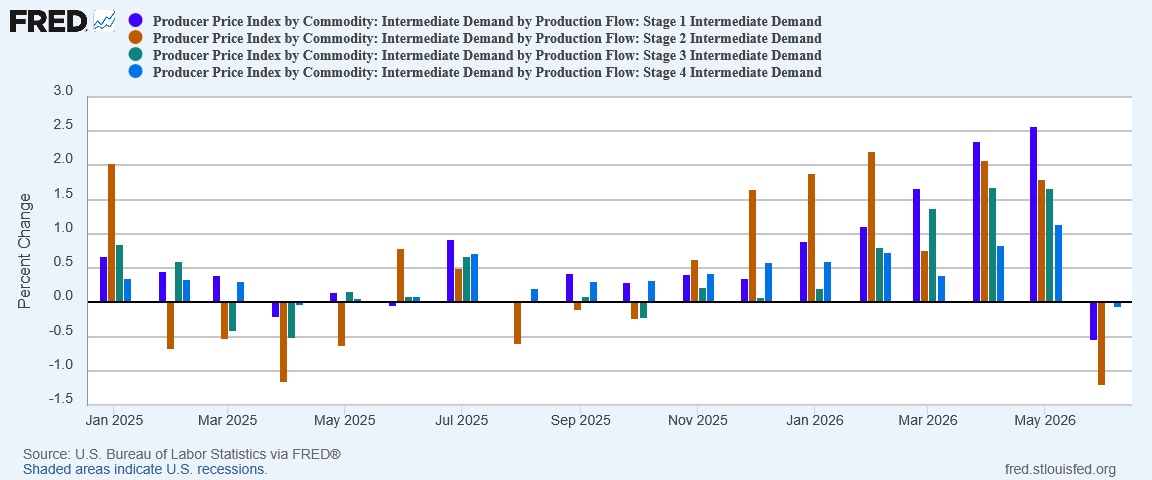

Intermediate Demand Is Cause For Concern

As a general rule, we tend to look at lower prices with a fair bit of enthusiasm. That is natural economic behavior—we always prefer to pay less.

However, there are times when a price drop is a warning sign. The abrupt shift into deflation within the Producer Price Index for Intermediate Demand is one of those times.

Intermediate demand had been heating up since last fall—well before Operation Epic Fury and the war with Iran. Across the entire supply chain, for intermediate demand stages 1 through 4, in June rising prices were abruptly replaced with falling prices.

Is the drop in intermediate demand prices an outlier rather than a trend reversal? We won’t know that until we see next month’s data. As these shifts are month on month, we could easily be looking at a series of one-off price decreases.

We could also be looking at a signal of a slowing economy. If deflation continues within Intermediate Demand prices, we will definitely be looking at a slowing economy. Regardless of what prices do, the outcomes we do not want to see is a slowing economy or a recession.

Intermediate Demand prices suddenly losing altitude may be a recession warning, making the June drop a reason to be concerned.

War With Iran Still The Principal Factor

What seems certain is that the war with Iran, along with its potential for disrupting Persian Gulf oil flows, is going to have an outsized impact on prices for the next few months.

One reason is the uneven and somewhat problematic nature of traffic volumes through the Strait of Hormuz.

While President Trump insists the strategic waterway is open, and without tolls, traffic levels suggest the rest of the world is not entirely assured of the Strait’s safety. As the chairman of the Japan Foreign Trade Council Masahiro Okafuji said bluntly during a press conference, the Strait of Hormuz is “dangerous”.

There is an equally blunt rejoinder, however: the Strait may be dangerous, but avoiding it is costly.

Renewed re-routing of the shipping lanes around the Cape of Good Hope on Africa’s southern tip would hike transportation costs by over 30%, according to Okafuji, who is also chief executive at major Japanese trading house Itochu Corporation.

Following the re-escalation in regional hostilities in recent days, the Joint Maritime Information Center (JMIC) reaffirmed on Tuesday its regional threat level for the Strait of Hormuz at “severe”, which it had raised last week after the first signs emerged of the collapse of the U.S.-Iran ceasefire.

If the world’s freight carriers are doing all they can to avoid sending cargo vessels anywhere near the Persian Gulf, shipping costs are going to be rising for at least the next month or so.

If there should be another ceasefire, so that sailing through the Strait does not seem all that dangerous, we should see traffic levels through the Strait rebound again.

Even with another ceasefire, however, we are not likely to see traffic in the Strait return to the status quo ante right away. After the Memorandum of Understanding was signed, some ships began transiting the Strait once more, but the levels were not at all what they had been before the war with Iran. Signing a new MoU will not make ships any more eager to transit the Strait.

The economic reality is that the uncertainties of the war with Iran are equally uncertainties about prices and the global economy. As we cannot say with certainty how much longer the war with Iran will continue, we cannot say with certainty what is to become of traffic through the Strait of Hormuz. We cannot say with certainty if oil prices will trend back towards $100/bbl. We cannot say if Persian Gulf states will be able to reopen their oil fields or if production will have to be shut in.

If we cannot say with certainty what is likely to happen to fully one-fifth of the world’s oil supply, we cannot say with certainty what needs to happen with oil prices, as well as fuel prices and the prices of other refined petroleum products.

Last month’s ceasefire brought oil prices down by a very wide margin very abruptly. That lack of inflationary pressure has produced at least one month where prices drop because the anticipated supports for any given price or price level have moved lower.

However, the ceasefire is over. Iran is attacking other Persian Gulf states and the US is attacking Iran. The forces which brought oil prices down are already pushing them back up again.

What are we to make of the June Producer Price Index Summary? As with the Consumer Price Index Summary, the report is a one-off report of lower prices. Barring an outbreak of peace in the Middle East, we will not see a second drop in producer prices any time soon.

You are a treasure, Peter. Your superb analytical skills consistently give us the updated, accurate big picture. I so appreciate it!

One of the best campaign talking points a candidate can give is, “Prices have come down under our administration!” We can count on Trump-endorsed candidates to hype this. My question is, does the opposition have a valid argument that prices have come down regardless of Trump’s policies?