Superficially, the May Personal Income and Outlays Report is scarcely newsworthy. The report confirms what we already knew—that consumer price inflation continued to rise in May, and the primary contributor to that inflation continued to be energy prices.

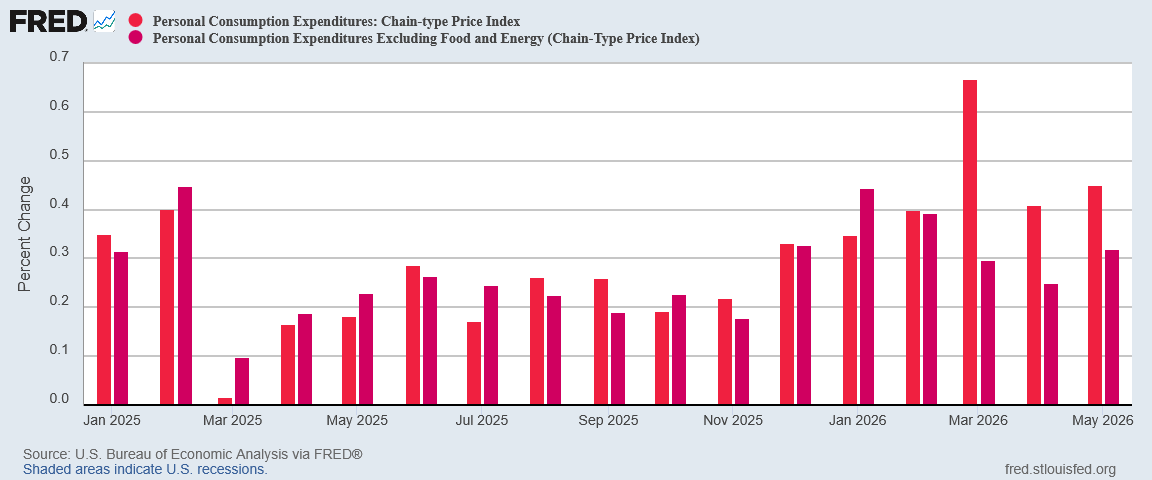

From the preceding month, the PCE price index for May increased 0.4 percent. Excluding food and energy, the PCE price index increased 0.3 percent.

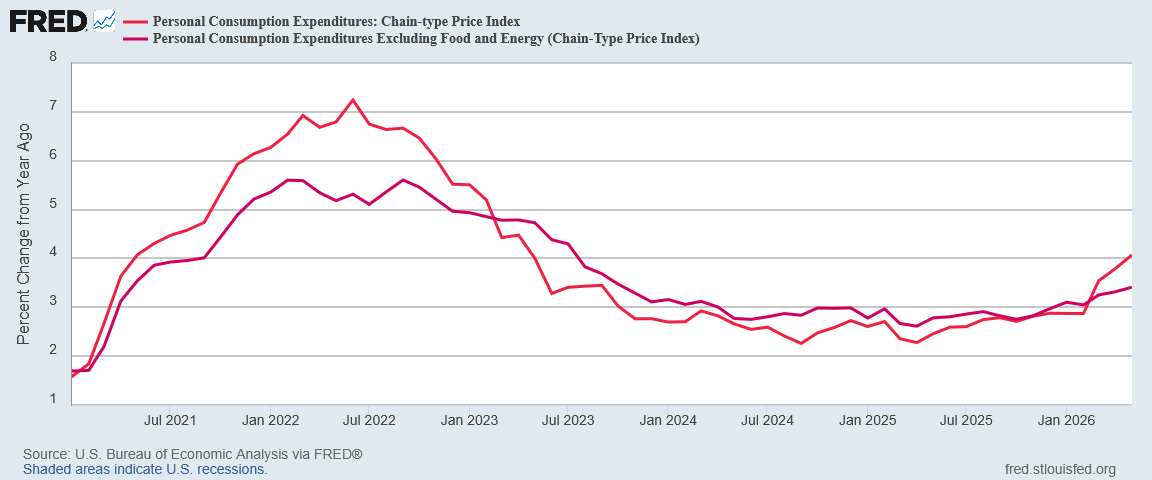

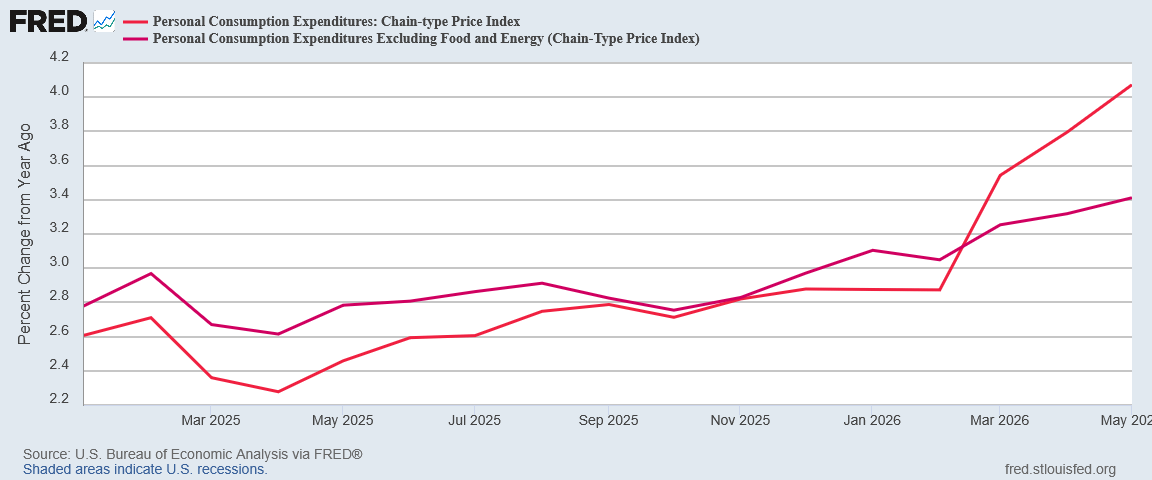

From the same month one year ago, the PCE price index for May increased 4.1 percent. Excluding food and energy, the PCE price index increased 3.4 percent from one year ago.

We know that prices are rising.

We even know why prices are rising: an oil price and supply shock after Iran illegally closed the Strait of Hormuz during the hopefully-ended war between the US and Iran.

What we do not know is how much more inflation are we likely to see. We also do not know how impactful renewed inflation will eventually be.

Corporate media continues to fret about inflation moving higher, and for the usual propaganda reasons. What corporate media overlooks is that there are signs this latest inflation cycle may have already run its course, and even more signs that the economy is not suffering as much as some have feared due to rising prices.

Inflation is rising, but is it also ending? Quite possibly, it is. At the very least, the risk of a stagflation crisis has diminished.

Headline Inflation Continues To Rise Faster Than Core

At 4.1% year on year, there is no denying that the PCE report shows inflation continuing to heat up in the US economy.

Yet it is also important to note that core inflation—consumer price inflation with food and energy prices stripped out—continued to increase at a significantly slower pace.

Even month on month, headline inflation is rising much faster than core inflation.

Not only is headline inflation outpacing core inflation, but the margin of increase has been greater over the past three months than at any time since the start of President Trump’s second term of office.

What is frequently overlooked in most media reporting on inflation is that core inflation has been moving steadily higher since last fall, while headline inflation’s recent rise is catalyzed mainly by energy prices.

That core inflation’s rise began last fall is particularly relevant given the obvious inflation impact of the oil supply shock which began in March, when Iran illegally closed off the Strait of Hormuz. While that oil supply shock presents significant risk of stagflation for most of the world’s economies, that risk has thus far largely not materialized in the US economy. The US is seeing primarily energy prices rise from the supply shock, but is not seeing significant contagion effect, where energy price inflation catalyzes additional price increases for other goods and services.

Corporate Media Obsessed With Interest Rates

The lack of a significant stagflation crisis in the US thus far has been almost entirely overlooked by corporate media. Instead, corporate media’s concerns about rising inflation have been revolving primarily around whether or not an increase in consumer price inflation will push the Federal Reserve to raise the federal funds rate. Even before the May inflation print came out, the main concern regarding the report was how it would be received by the Federal Reserve.

The monthly PCE report is the Federal Reserve’s preferred inflation gauge. New Fed Chairman Kevin Warsh has said the central bank is committed to bringing inflation back to its 2% target — a level it has failed to reach for the past five years. Wall Street now anticipates the Fed will raise its key interest rate at least once by year’s end in a bid to counteract the stronger price growth.

By making it more expensive to borrow money, the Fed slows overall economic activity and, with it, the pace of price increases.

“Thursday’s PCE is set to take on greater importance for markets, especially since Federal Reserve Chair Warsh was emphatic in last week’s meeting about the central bank’s desire to achieve price stability, and this PCE reading could affect the market’s rate hike expectations,” Rick Gardner, chief investment officer at North Carolina-based RGA Investments, said in a statement.

Corporate media reporting after the report was released kept focusing on a narrative of rising inflation means the Fed will likely raise interest rates later this year.

The report comes a little more than a week after the Fed and new Chairman Kevin Warsh delivered what markets widely viewed as a tough talk on rates and inflation.

Warsh in particular stressed the importance of price stability, with the Federal Open Market Committee adopting language in its post-meeting statement unequivocally stating that it would “deliver price stability” after missing its 2% inflation target for five years running. In addition, officials took off a previously indicated rate cut this year and indicated a likelihood of a hike.

Axios even regarded the US economy’s seeming resilience in the face of rising inflation as a negative, lamenting how consumers were not “cracking”, but were continuing to spend and consume despite rising prices.

Inflation is bad, we are told, not because of its impact on the prices consumers must pay for goods and services, but because of what it “forces” the Federal Reserve to do with respect to the federal funds rate. What the reporting never gets around to acknowledging is that the Fed is never obligated to raise or reduce the federal funds rate.

Perversely corporate media’s focus on the inflation reports potential impact on future Fed interest rate decisions highlights the importance of newly-minted Federal Reserve Chairman Kevin Warsh’ decision to curtail most of the Fed’s “forward guidance” following the latest Federal Open Market Committee decision to stand pat on the federal funds rate. Instead of examining how the economy is responding to rising prices, corporate media—and, presumably, Wall Street overall—is keeping one eye on the Federal Reserve, looking to the Fed for guidance on what the response “should be”.

If people harbored any lingering doubts that the Federal Reserve is exerting too much influence over financial decision-making in the broader US economy, how the media covers the official inflation reports does much to put those doubts to rest.

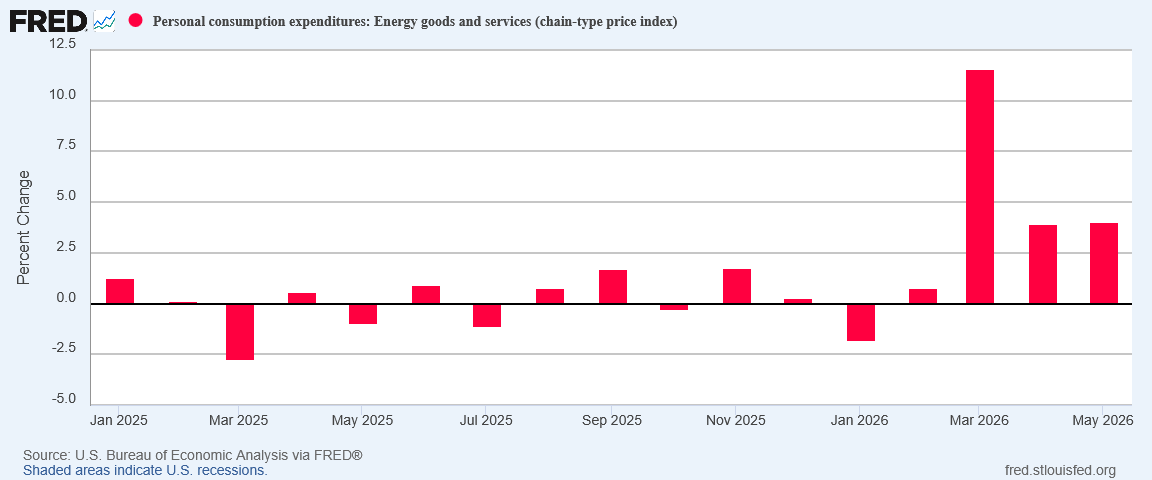

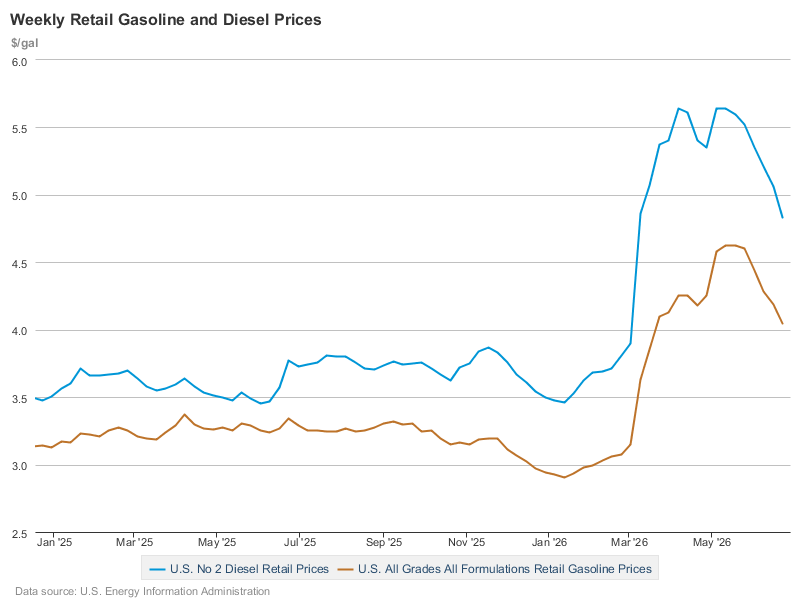

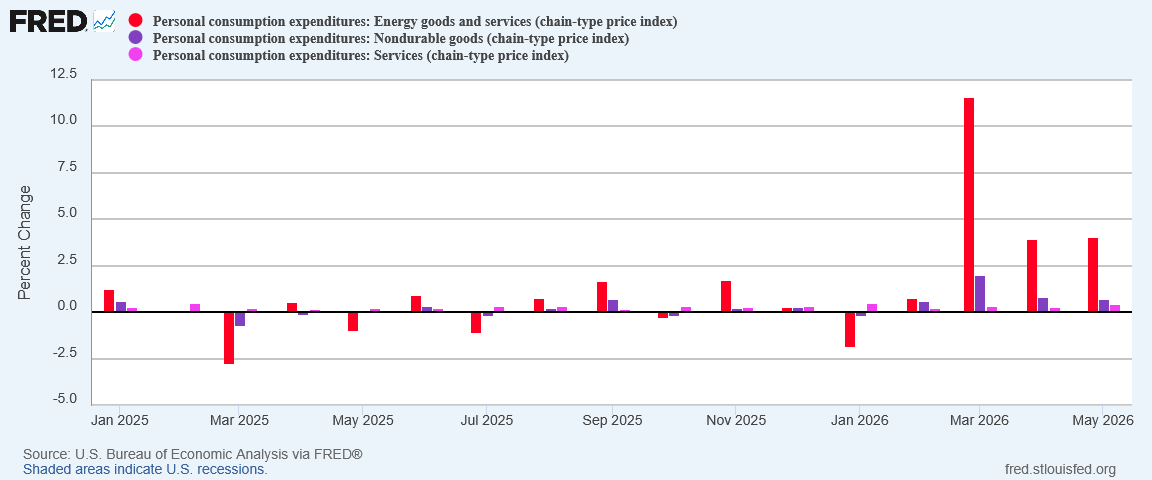

Energy Price Inflation Largely Unchanged

While energy price inflation remained the dominant component within overall consumer price inflation, month on month energy price inflation itself did not change much.

Oil supply disruptions from the Strait’s closure are continuing to exert pressure on energy prices in the US, but that pressure did not increase significantly in May.

If anything, it is remarkable that energy price inflation did not come down in May, given the decrease in gasoline and diesel prices throughout the month.

The persistence of energy price inflation in May is even more remarkable considering the decline in benchmark crude prices.

That energy price inflation apparently has not fully captured all of the price decreases in May suggests that energy price inflation may be about to come down, particularly month on month.

Without continued energy price inflation, headline inflation cannot continue to rise at its current pace.

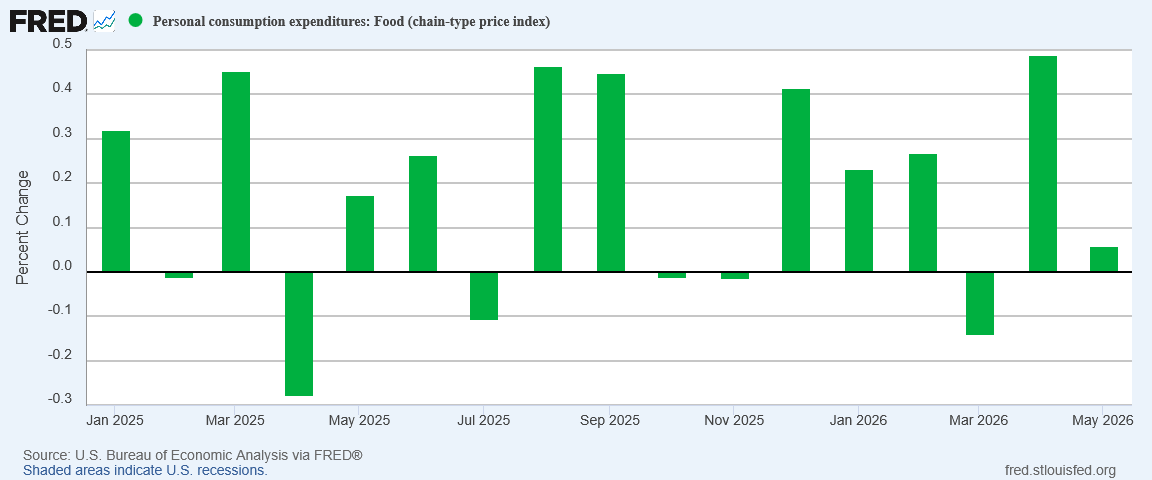

Food price inflation, the other inflation component outside of core inflation, certainly is not likely to push the headline index up the way energy prices have. After a significant month on month surge in April, food price inflation cooled way down in May.

While food price inflation had been rising since mid-2024, since last summer it has broadly stabilized.

Food prices are stripped out of core inflation calculations largely because of their greater volatility, just as with energy prices. Yet the fact that we are not seeing a dramatic inflation surge in food prices from the oil supply shock is the strongest signal we have that energy price inflation is not pushing up other prices, at least not yet.

For all the reporting of inflation heating up, the reality of May’s inflation report is that energy price inflation did not really change, and food price inflation actually fell.

Has the current inflation cycle already reached its peak? Food and energy prices suggest it may have.

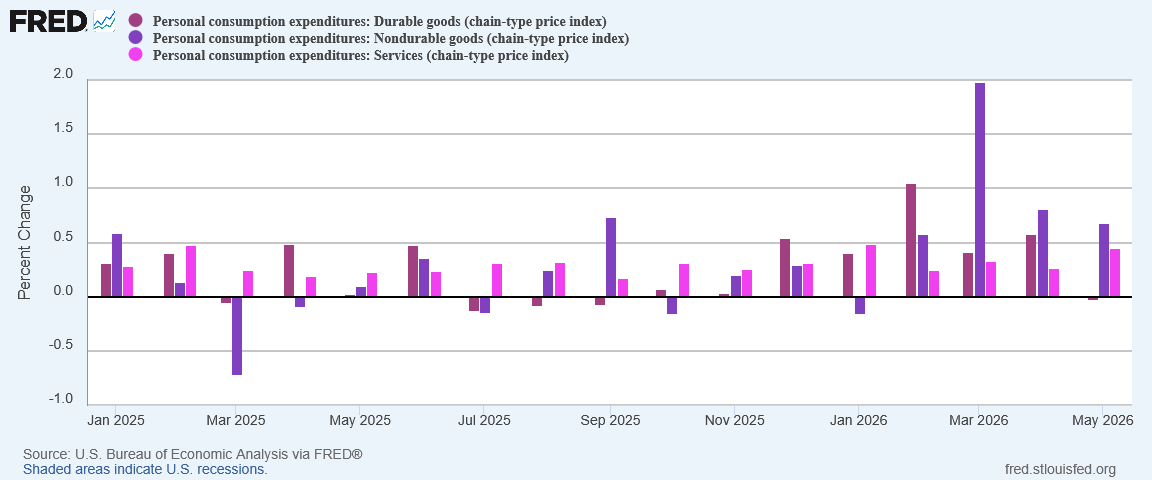

Durable Goods In Deflation For May

A further signal that inflation may have already peaked comes from durable and non-durable goods prices in May.

Durable goods prices actually fell in May, and non-durable goods showed price disinflation, despite the continued pressure from energy prices. Service price inflation rose month on month, but is still below its recent January 2026 peak.

That non-durable goods inflation eased in May suggests that, outside of energy prices, non-durable goods might very well have been in deflation for May as well. Certainly when energy price inflation is put next to non-durable goods inflation, we can see that energy prices are the dominant factor in non-durable goods inflation.

Just as with the earlier CPI report, the PCE report is showing considerable energy price inflation, but not much additional inflation.

If energy price inflation eases next month or the month after, there is simply not much inflation in other areas to sustain the current headline inflation rates. If energy price inflation tips back into outright deflation, as it did for most of 2023 through mid-2025, headline inflation will ease dramatically.

AI: The One Contrarian Signal

If we look at just the broad pricing data, we could easily conclude that this latest inflation cycle has already reached its peak and that, barring a major change such as renewed hostilities with Iran, consumer price inflation is poised to cool significantly. We would be remiss not to acknowledge that could very easily prove to be the case.

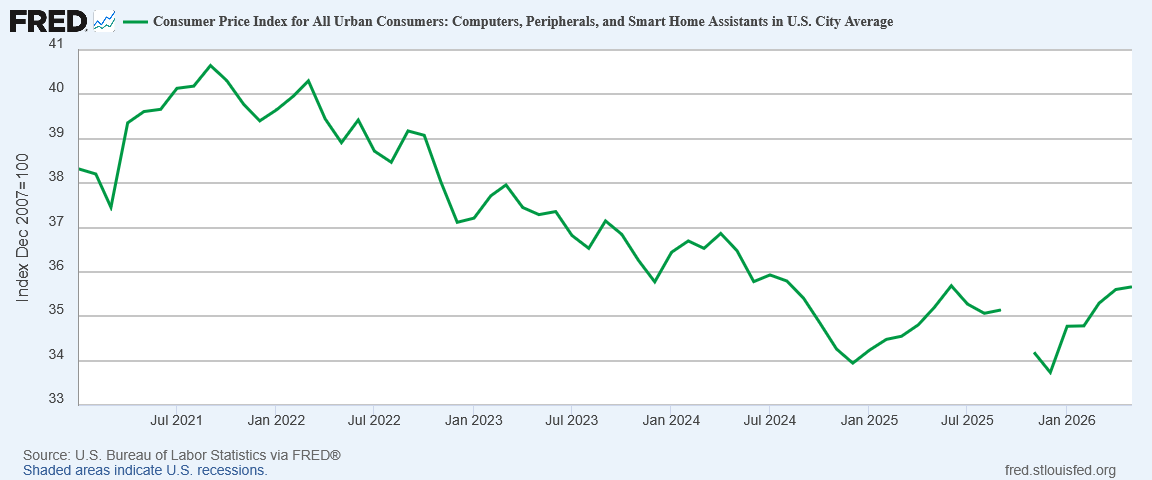

Yet we should note that energy is not the only source of inflationary pressure in the US economy. One area that is exerting increasing pressure is computer technology.

With events in the Middle East dominating headlines worldwide, little attention was given last week to outgoing Apple Computer CEO Tim Cook’s warning that the tech giant was about to raise prices across the board.

“Unfortunately, price increases are unavoidable,” he said. “We’re doing our best to mitigate the huge increases that are being passed to us, and we’ve been trying to shield our customers from the increases, but the situation has become unsustainable.”

Yesterday, the warning became reality, when Apple announced price hikes across a broad range of products, citing pricing pressures from surging memory and chip prices.

“We have never seen a component price increase this much, this quickly,” Apple said in a statement. “We have shielded our customers from these increases so far, but we have now reached a point where we need to begin raising prices on a number of products, including today’s increases for iPad and Mac.”

Apple hiked the price of MacBook Air with 512 gigabytes of storage rose to $1,299 from $1,099, while the MacBook Pro with 1 terabyte of storage rose to $1,999 from $1,699, according to updated prices on its website. The iPad Air with 128 gigabytes of storage rose from $599 to $749, among other changes.

Prices for computer hardware had been on the decline for years up until last year, when prices rebounded during the spring before easing back down later in the year.

Since January, hardware prices have repeated their early-2025 surge. Whether they will ease back down in the fall remains as yet unknown.

Driving much of the surge in hardware prices is the runaway interest in artificial intelligence, along with the building of data centers to meet that growing demand. As one would expect, the surge in computer hardware demand is producing a surge in prices.

With so much demand, prices are rising for many of the things that go into the AI build-out. And because those things are used for more than just AI, those price increases are spilling over into the broader economy.

Memory and storage chips, for example, are used in a broad array of consumer-electronics products that includes everything from videogame consoles to cars. Nintendo, Microsoft and Sony have all raised prices on devices. Higher price tags are coming to Apple products, too, according to Chief Executive Tim Cook, who told The Wall Street Journal that the jump in costs was unlike anything he had seen “in any area in over 40 years.”

According to Tim Cook and Apple, there is already contagion effect at work with chip and memory prices pushing up Apple prices.

Will AI fuel a renewed hyperinflation cycle? That is extremely unlikely. While data center buildouts can and will have impacts on local economies, the surge in component and overall tech prices has not resulted in a sustained inflation pressure across the broader economy. Despite a price surge in tech prices that is now months old, durable goods still went into deflation for May, while non-durable goods showed notable price disinflation.

At the same time, we must recall that core price inflation was trending higher long before Operation Epic Fury and the closure of the Strait of Hormuz. There are clearly inflation pressures at work on the US economy besides energy.

Is Artificial Intelligence one of these inflation pressures? If we take Tim Cook’s warning last week seriously, yes, it is. Against a rising number of inflation signals suggesting inflation is close to being done heating up, computer tech prices stand out as a notable contrarian signal.

Is Stagflation Still Possible?

When Iran first closed the Strait of Hormuz, I noted that, given the softness that had been the prevailing trend in US labor markets, stagflation from the oil shock from the Strait’s closure was a real possibility. Given the “fugly” jobs report we had in February, a stagflation crisis was a very real risk for the US economy at that time.

Since that time, we have had three months of good jobs numbers, including back-to-back revisions to the upside. The soft jobs markets of February have morphed into robust and recovering job markets for May.

With stronger job markets and softer core inflation, at present the risks of a 1970s-style stagflation crisis in the US are greatly diminished. The risks here in the US are apparently less than in the EU, given the European Central Bank’s recent decision to raise interest rates, in contrast to the Fed’s decision to stand pat on interest rates.

That does not mean the risks are non-existent. Some of the members of the Federal Open Market Committee have indicated the Fed may raise the federal funds rate at least once during the remainder of the year.

If American jobs markets soften again, the potential for stagflation will return.

If consumer price inflation surges such as it did in March, the potential for stagflation will return.

If both happen at the same time, the potential for stagflation not only returns, but moves from a possibility to a probability.

At present, jobs markets are not softening and inflation is not surging, but if the last few months are testament to anything it is the capacity of even broad economic metrics to shift dramatically from one month to the next.

Stagflation is still very possible, but unless there is a significant shift in either jobs or prices for June, stagflation is for now not very probable.

Overall, this is a pretty good picture for Republicans going into the midterm elections. No opponent can point to anything catastrophic, such as gas prices doubling or stagflation settling in.

But I am surprised to hear talk of needing to raise the federal funds rate. Trump wants it lowered. Peter, do you think Warsh would actually raise it, and before the midterms?