While no one can accurately predict the full scope of the financial consequences of expelling Russia from SWIFT, the forex markets should give us broad visibility into the global economic shifts being imposed.

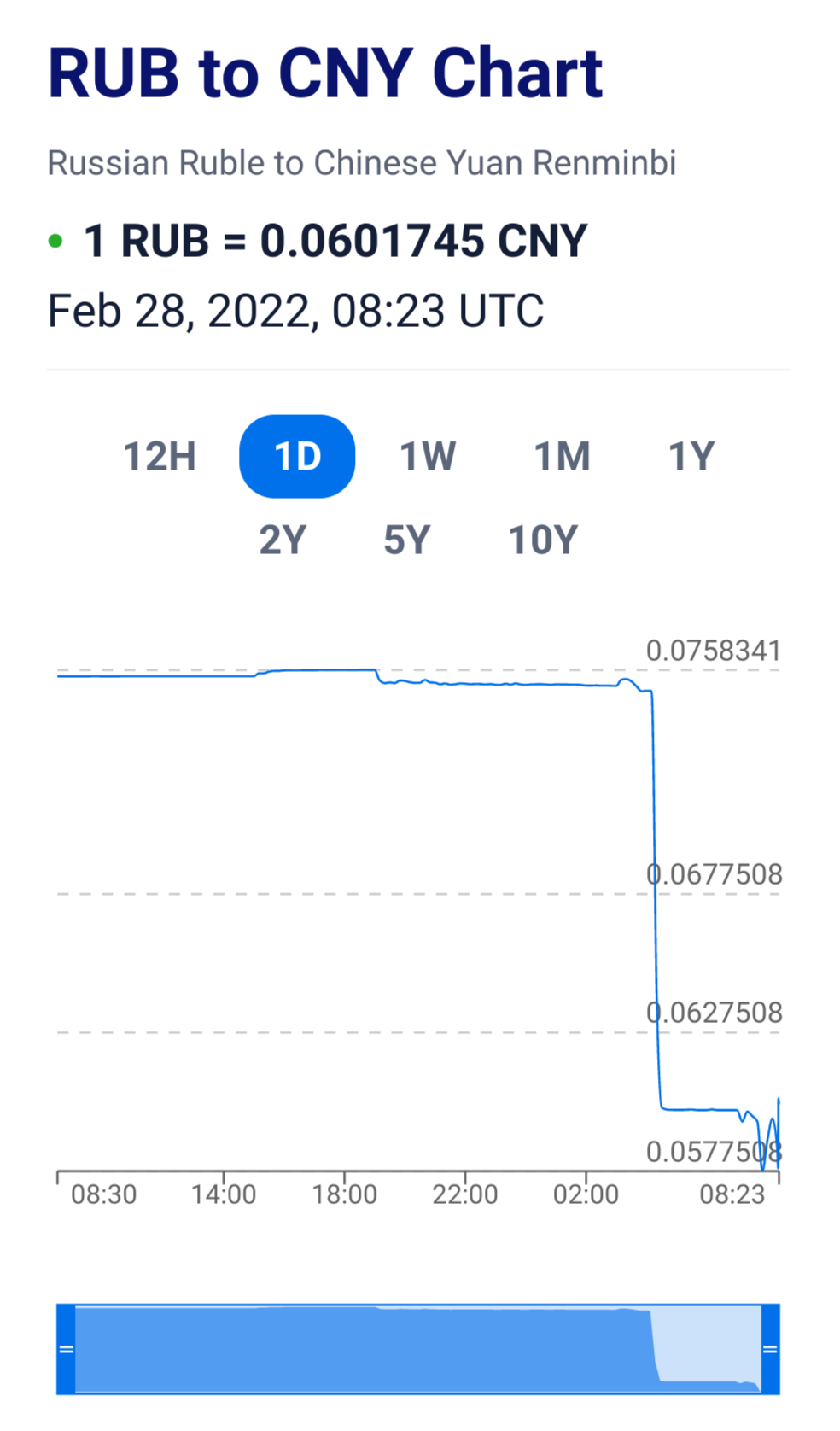

With that in mind, it is worth noting that the ruble is dropping like a stone against the Chinese yuan.

If China is Russia's new found trading partner, Beijing is reaping all the benefits.

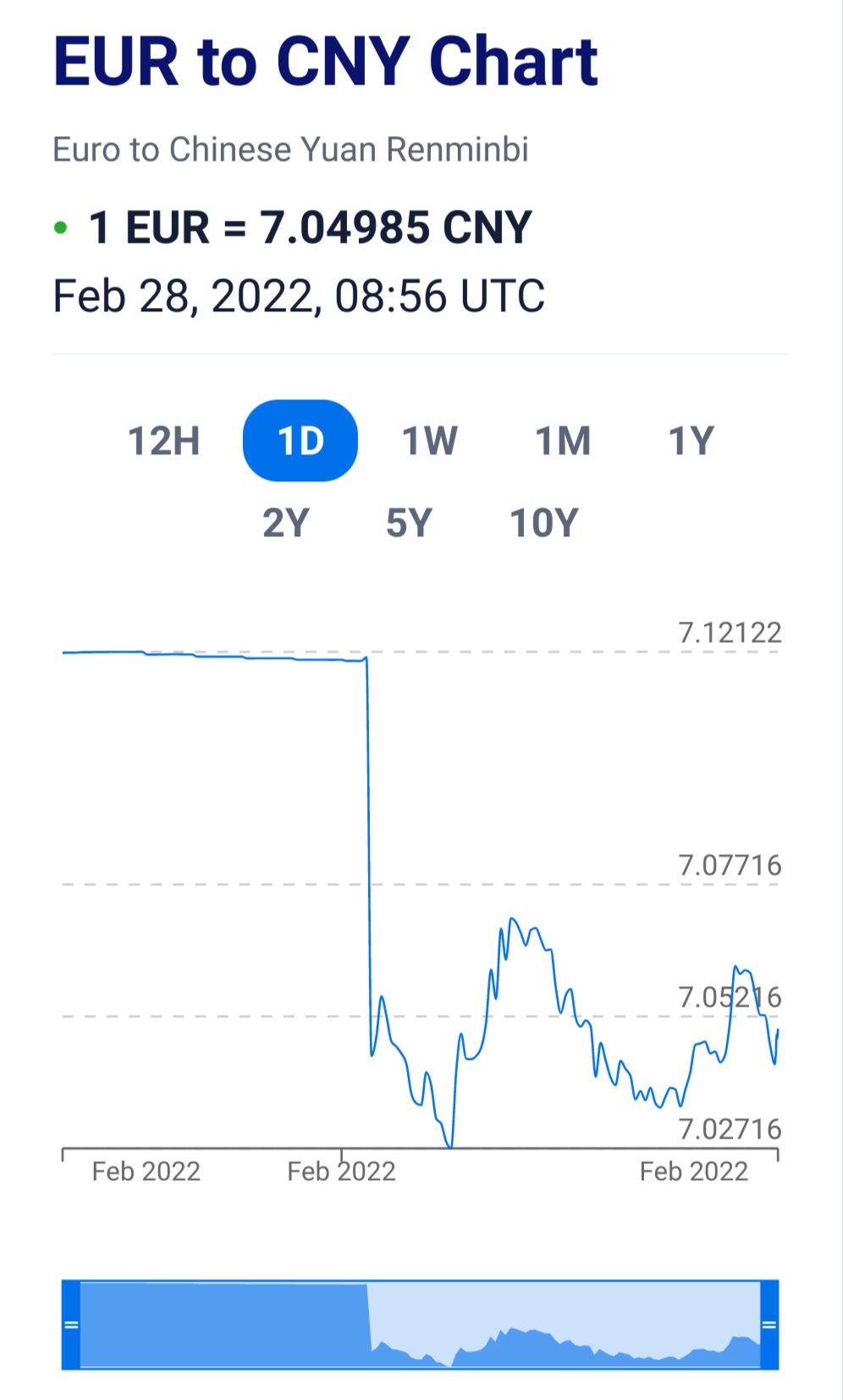

The dollar was up briefly against the yuan before trending down again.

Keep in mind that in recent months the PBOC has been seeking a weaker yuan against the dollar as part of their own internal monetary policy.

China has returned from its week-long holiday. While it is no secret that Beijing is easing (ever more aggressively, prompting fund managers to allocate capital to China at a time when the country is increasingly viewed as non-grata by both the left and right) to stabilize its slumping economy, just as the rest of the world is tightening, moments ago the PBOC underscored its commitment to keeping the yuan on a downward slope when it fixed the yuan at 6.3580. Compared to expectations of 6.3328, this was the weakest fixing on record!

Putin's war has completely derailed Beijing's currency manipulations. There is no way to know all the consequences of this, but is difficult to see Beijing being happy about this.

Interesting but China may not be as upset as you think. It seems clear China was forewarned about it and that it is likely the China and Russia actually discussed this on their February 4th meeting (perhaps even going so far as to ensure coordination that the whole thing kicked off AFTER the Olympics rather than during the Olympics as happened last time with Georgia in August 2008).

What also seems likely is that China is taking notes on this for their eventual operation to reunify Taiwan and the mainland under one government again (but this time it won't be a KMT government). We already had the editor of the Chinese state press agency (Xinhua) noting that China would be needing Russia's reciprocal "understanding and support when wrestling with America to solve the Taiwan issue once and for all,".

Through this China is gaining invaluable insight into how the West in general might react to an attack on Taiwan (sanctions, SWIFT expulsion, central Bank asset freezes, attempting to deliver weapons (including fighter aircraft, MANPADS and anti-armour missiles) to Taiwan, perhaps covertly sending their own armed forces as "volunteers" in a newly established Taiwan International Legion or something...perhaps even volunteer Fighter pilots to pilot those planes sent) and thus how to plan ahead to avoid the most serious consequences. Russia already did some of this. Unlike folks like Saddam Hussein or Gaddafi they had already located at least 50% on their central bank assets in countries that won't sanction them. They already diversified their foreign exchange holdings so that US dollars went from being 45% of the total in 2017 to around 16% in 2021. Chinese Yuan went from 2.3% in the same period to 13% (and recall the Yuan is fixed to the US dollar by the PBOC; and with China being the main trading partner for Russia and for most of the rest of the world and China having already established currency swap facilities with a number of countries these Yuan holding might have some value beyond just China). Russia already sold off most of their US treasuries a few years ago as well.

So China essentially gets to see the dress rehearsal of the MINIMAL Western response at the cost of temporary Yuan appreciation relative to the Rouble, Euro and US dollar. When this is all over what's to stop the PBOC from simply printing more Yuan to bring the exchange rates against EUR and USD back to what it was for them on Feb 23rd? It might not bring the exchange rate with RUB back to that level but what does that matter with the West cutting trade ties with Russia? Russia's demand for certain goods will simply shift from the West to China (and India and the domestic market where possible) and the price that is available from these non-western sources is the price that has to be paid if the goods and services are really needed. It isn't like a super-low exchange rate means that the goods won't be bought. After all look at Vietnam. Their dong is about 3,600 to 1 Yuan and around 23,000 to one USD but it doesn't stop them from having a trade deficit with China to the tune of $50 billion.

For China this is essentially the price of admission to see the dress rehearsal. It might as well be an investment.

Good points all. And long term China might well be the ultimate winner here.

Short term is looking like a different story.

The collapse of the ruble against the yuan is significant mainly because it indicates China is not doing much to help Russia. And one reason why might be because the euro and the dollar went south against the yuan. In the space of less than a week, Putin's war reversed at least three months of PBOC weakening of the yuan.

Nor is there yet any clear indication China is an immediate beneficiary of the turmoil. The Hang Seng is down over 4% since the invasion started, and Shanghai is treading water. Over the same time frame the Dow is treading water, with the Nasdaq and S&P500 posting gains.

Keep in mind that China is grappling with its own economic issues. Their real estate sector is still on PBOC life support. Their credit channels are clogged which makes monetary stimulus that much more difficult.

Russia is at the moment adding to that burden. That's not exactly the stuff which bolsters good diplomatic relations.

The collapse of the ruble against the yuan is significant mainly because it indicates China is not doing much to help Russia"

But what you are suggesting would be a sign of China helping Russia is literally impossible so long as the Yuan is semi-fixed against the US dollar. It is the RUB rate against the US dollar that determines the Ruble/Yuan rate. The RUB/CNY rate doesn't exist in a vacuum. For the RUB to not be falling massively against the CNY then either the RUB must not be falling against the US dollar or else the CNY must be falling just as rapidly against the US dollar as the Rouble is (and for that the PBOC would have to be actively printing as much Yuan Reminbi as they possibly can AND setting a new rate to match to keep up with the Rouble's fall). While that might help Russia in terms of retaining the value of its own currency such a move (absent market forces somehow driving the CNY lower like say if the Yuan was free floating fully and China was also invading Taiwan and being sanctioned by the West), it would be rather curious on the part of the PBOC to be conducting Chinese monetary policy in reference to helping another country to the detriment of its own.

1) I think you're overstating the degree to which forex markets are linked. A simple review of the ruble, euro, and dollar against the yuan shows there is a considerable amount of variance among currencies.

2) the PBOC WANTS a weaker yuan. Mounting even a small defense of the ruble would not only buffer the ruble vs the yuan, but preventing dollar decline against the yuan would be a welcome consequence.

If I'm not mistaken the PBOC of China manages the Yuan exchange rate exclusively in reference to the USD within a 2% daily range. Therefore the ruble and euro rates against the Yuan would of course show considerable variance over time since both the ruble and euro are free floating currencies with respect to the US dollar (unlike the Yuan, though even here the Yuan is managed within a wider range than other currencies that have been fixed to the US dollar such as the Hong Kong Dollar, Singapore dollar or the Bahamian dollar). And indeed this is so. Over the past five years the USD/CNY rate has bounced around between about 6.3 and 7.15 Yuan per dollar (the least variance naturally since the USD is the reference currency), but about 7.3 and 8.3 Yuan per euro (more variance but not incredibly so given that the euro itself is broadly stable as a strong reserve currency) and has consistently appreciated (not bounced around) against the ruble from 8.6 rubles per Yuan to 12 rubles per Yuan before the current conflagration. Since the war it is now at 17 rubles per Yuan.

Interesting but China may not be as upset as you think. It seems clear China was forewarned about it and that it is likely the China and Russia actually discussed this on their February 4th meeting (perhaps even going so far as to ensure coordination that the whole thing kicked off AFTER the Olympics rather than during the Olympics as happened last time with Georgia in August 2008).

What also seems likely is that China is taking notes on this for their eventual operation to reunify Taiwan and the mainland under one government again (but this time it won't be a KMT government). We already had the editor of the Chinese state press agency (Xinhua) noting that China would be needing Russia's reciprocal "understanding and support when wrestling with America to solve the Taiwan issue once and for all,".

Through this China is gaining invaluable insight into how the West in general might react to an attack on Taiwan (sanctions, SWIFT expulsion, central Bank asset freezes, attempting to deliver weapons (including fighter aircraft, MANPADS and anti-armour missiles) to Taiwan, perhaps covertly sending their own armed forces as "volunteers" in a newly established Taiwan International Legion or something...perhaps even volunteer Fighter pilots to pilot those planes sent) and thus how to plan ahead to avoid the most serious consequences. Russia already did some of this. Unlike folks like Saddam Hussein or Gaddafi they had already located at least 50% on their central bank assets in countries that won't sanction them. They already diversified their foreign exchange holdings so that US dollars went from being 45% of the total in 2017 to around 16% in 2021. Chinese Yuan went from 2.3% in the same period to 13% (and recall the Yuan is fixed to the US dollar by the PBOC; and with China being the main trading partner for Russia and for most of the rest of the world and China having already established currency swap facilities with a number of countries these Yuan holding might have some value beyond just China). Russia already sold off most of their US treasuries a few years ago as well.

So China essentially gets to see the dress rehearsal of the MINIMAL Western response at the cost of temporary Yuan appreciation relative to the Rouble, Euro and US dollar. When this is all over what's to stop the PBOC from simply printing more Yuan to bring the exchange rates against EUR and USD back to what it was for them on Feb 23rd? It might not bring the exchange rate with RUB back to that level but what does that matter with the West cutting trade ties with Russia? Russia's demand for certain goods will simply shift from the West to China (and India and the domestic market where possible) and the price that is available from these non-western sources is the price that has to be paid if the goods and services are really needed. It isn't like a super-low exchange rate means that the goods won't be bought. After all look at Vietnam. Their dong is about 3,600 to 1 Yuan and around 23,000 to one USD but it doesn't stop them from having a trade deficit with China to the tune of $50 billion.

For China this is essentially the price of admission to see the dress rehearsal. It might as well be an investment.

Good points all. And long term China might well be the ultimate winner here.

Short term is looking like a different story.

The collapse of the ruble against the yuan is significant mainly because it indicates China is not doing much to help Russia. And one reason why might be because the euro and the dollar went south against the yuan. In the space of less than a week, Putin's war reversed at least three months of PBOC weakening of the yuan.

Nor is there yet any clear indication China is an immediate beneficiary of the turmoil. The Hang Seng is down over 4% since the invasion started, and Shanghai is treading water. Over the same time frame the Dow is treading water, with the Nasdaq and S&P500 posting gains.

Keep in mind that China is grappling with its own economic issues. Their real estate sector is still on PBOC life support. Their credit channels are clogged which makes monetary stimulus that much more difficult.

Russia is at the moment adding to that burden. That's not exactly the stuff which bolsters good diplomatic relations.

"Short term is looking like a different story.

The collapse of the ruble against the yuan is significant mainly because it indicates China is not doing much to help Russia"

But what you are suggesting would be a sign of China helping Russia is literally impossible so long as the Yuan is semi-fixed against the US dollar. It is the RUB rate against the US dollar that determines the Ruble/Yuan rate. The RUB/CNY rate doesn't exist in a vacuum. For the RUB to not be falling massively against the CNY then either the RUB must not be falling against the US dollar or else the CNY must be falling just as rapidly against the US dollar as the Rouble is (and for that the PBOC would have to be actively printing as much Yuan Reminbi as they possibly can AND setting a new rate to match to keep up with the Rouble's fall). While that might help Russia in terms of retaining the value of its own currency such a move (absent market forces somehow driving the CNY lower like say if the Yuan was free floating fully and China was also invading Taiwan and being sanctioned by the West), it would be rather curious on the part of the PBOC to be conducting Chinese monetary policy in reference to helping another country to the detriment of its own.

Two points:

1) I think you're overstating the degree to which forex markets are linked. A simple review of the ruble, euro, and dollar against the yuan shows there is a considerable amount of variance among currencies.

2) the PBOC WANTS a weaker yuan. Mounting even a small defense of the ruble would not only buffer the ruble vs the yuan, but preventing dollar decline against the yuan would be a welcome consequence.

If I'm not mistaken the PBOC of China manages the Yuan exchange rate exclusively in reference to the USD within a 2% daily range. Therefore the ruble and euro rates against the Yuan would of course show considerable variance over time since both the ruble and euro are free floating currencies with respect to the US dollar (unlike the Yuan, though even here the Yuan is managed within a wider range than other currencies that have been fixed to the US dollar such as the Hong Kong Dollar, Singapore dollar or the Bahamian dollar). And indeed this is so. Over the past five years the USD/CNY rate has bounced around between about 6.3 and 7.15 Yuan per dollar (the least variance naturally since the USD is the reference currency), but about 7.3 and 8.3 Yuan per euro (more variance but not incredibly so given that the euro itself is broadly stable as a strong reserve currency) and has consistently appreciated (not bounced around) against the ruble from 8.6 rubles per Yuan to 12 rubles per Yuan before the current conflagration. Since the war it is now at 17 rubles per Yuan.