While it is far too soon to tell if the price cap will have any meaningful impact on Russia’s war in Ukraine (so far, there is no indication either price cap has had any influence on Putin’s war aims in Ukraine), enough time has passed that we can begin to assess the market impacts of the cap, and their ramifications for Russia.

At least initially, European markets for refined products appear to have digested the imposition of the price cap rather successfully, all the while sustaining the price cap on Urals crude oil—the ultimate litmus test of the durability of the price caps, for if that cap cannot be sustained on Russia’s benchmark crude, a price cap cannot be sustained, period.

Certainly, the price caps have not drastically disrupted European oil product prices as of yet.

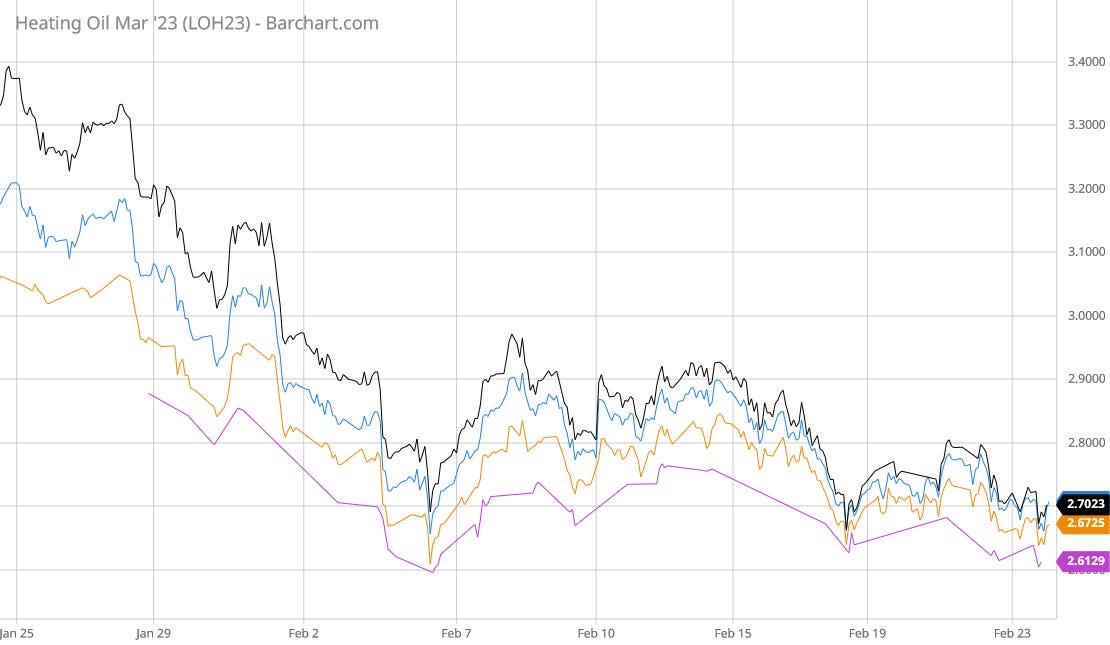

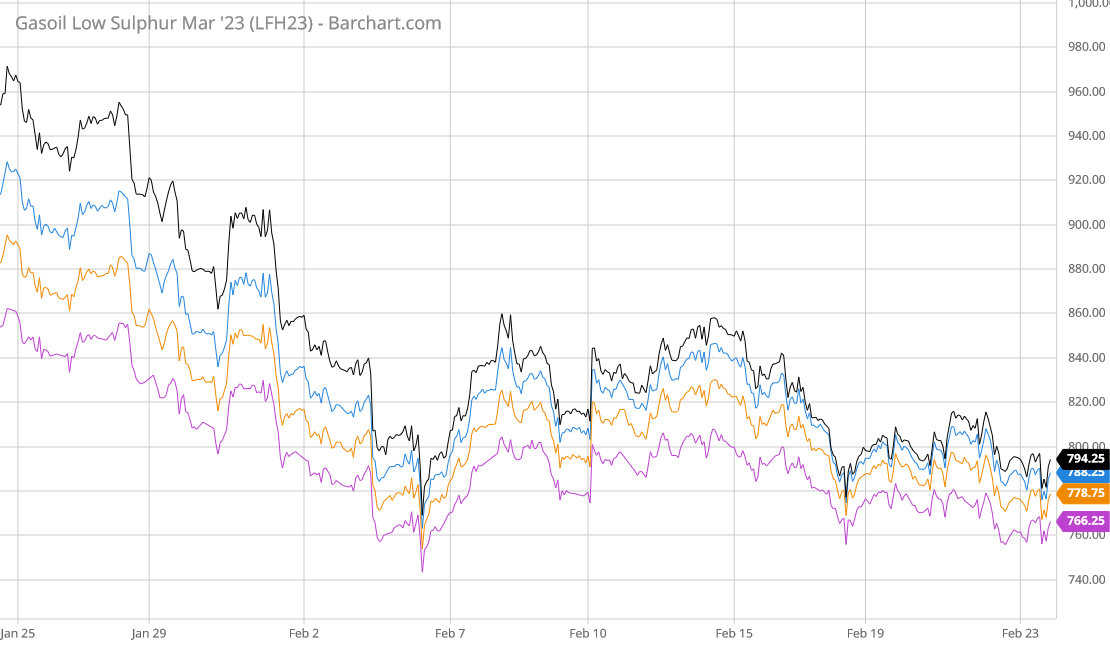

Fuel oil futures have followed a similar trajectory, just as before.

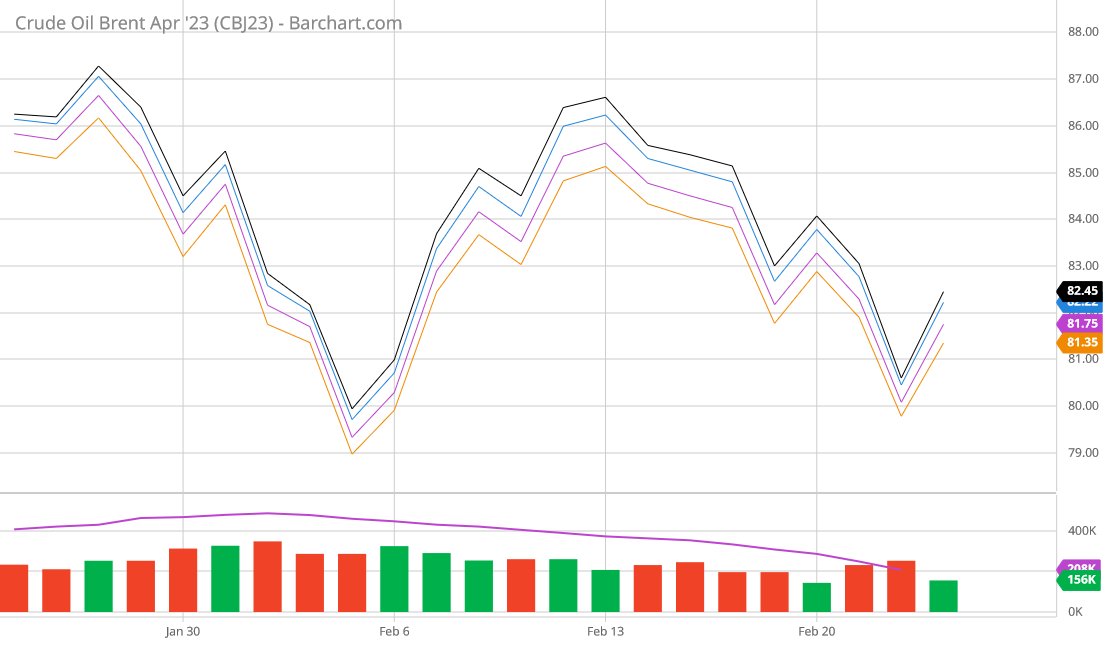

While the price for Brent crude surged somewhat both after the imposition of the cap and Russia’s announcement of production cuts, that price also has retreated.

Notably, futures contracts for the next few months are also not showing any signs of upward pressure, suggesting that the markets are not feeling any pinch from the cap.

Furthermore, while the price Europeans are paying for gasoline and diesel fuel at the pump have risen since the first of the year, for most European countries those prices are well below peak prices set last summer, and in many countries those prices have even gone down in recent days.

Most crucially, however, the price for Urals crude remains below the price cap of $60/bbl.

While the refined products cap announcement and Russia’s production cuts announcement did generate momentary increases in the price for Urals crude, there has yet to be sustained pressure put on the price cap itself.

With Russian crude output reported has having declined slightly in January, down to 9.77 million barrels per day, according to the International Energy Agency’s February Oil Market Report, the market signs certainly appear to suggest the price caps are holding and that Russia’s oil revenues are being further constrained as a result of the caps.

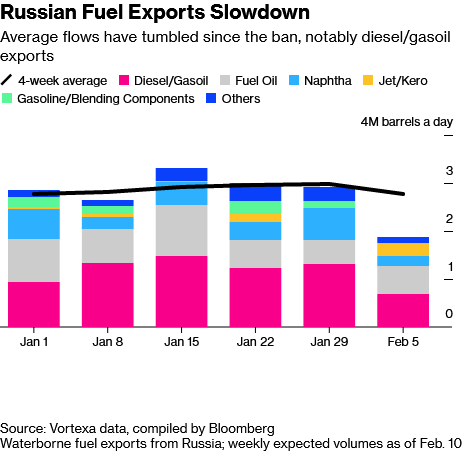

Flows of petroleum products ranging from diesel to jet fuel are set to tumble to about 1.9 million barrels a day in the week after the sanctions took effect, according to data from Vortexa Ltd. compiled by Bloomberg. That’s about 37% below average levels during the previous four weeks.

While it is easy to make too much of the coincidence, the possibility that Russia is curtailing production because it has nowhere to ship or store the oil cannot be dismissed out of hand.

"We feel that it is more likely that Russia is simply struggling to find buyers for its oil, particularly after the EU ban on Russian refined products came into force earlier this month," according to ING analysts Warren Patterson, the bank's head of commodities strategy, and Ewa Manthey, a commodities strategist.

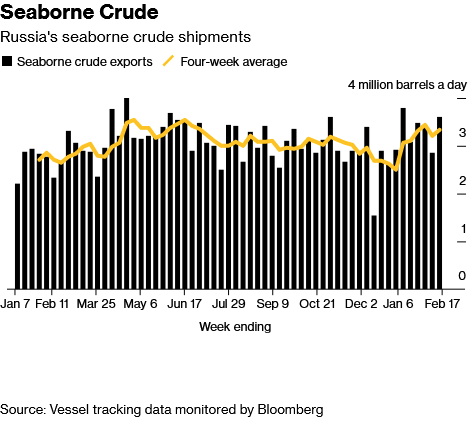

The country exported 3.6 million barrels a day from its ports in the seven days through Friday. That was a 26% hike in what are noisy weekly data. Flows climbed to multi-week highs from all its Baltic, Black Sea, Arctic and Pacific terminals. A less-volatile four-week average of exports also rose.

Based on tanker destinations, the vast majority of these shipments are heading to China and India.

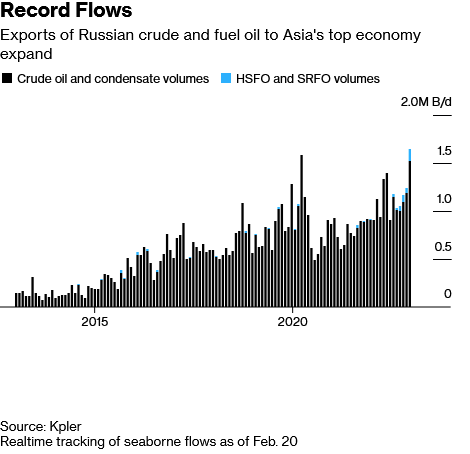

Russian exports of discounted crude and fuel oil to China have jumped to record levels as the re-opening of the world’s biggest energy importer gathers pace after the dismantling of Covid Zero.

Overall flows last month were at the highest at any point since the invasion of Ukraine a year ago and surpassed a record set in April 2020, according to data intelligence firm Kpler. Exports of fuel oil surged to an all-time high.

India may be about to similarly exploit the price cap regime on refined products, as there are reports India may opt to import cheaper Russian fuel oil and export what it refines natively from imported Russian crude—which India, unlike Russia, can sell at market rates.

"Our people are exploring if we can source cheaper products from Russia," said a top executive at an Indian refiner. "If India can import so much crude, it can, of course, import products as well. But imports of products must make commercial sense. We are in the business to make money."

The executive added that the decision would be based on the discount, as well as the cost of insurance and freight. "Actual prices being quoted in the market are sometimes very different from the published information on prices and cracks. So, we will have to take a call based on what is being offered in the market," he said.

Perversely, these expanded purchases by India and China may prove to be the dynamic that sustains the price cap regime: Russian oil and potentially refined products are now more attractive in those markets because they are so much cheaper than the Brent benchmark. If this is the case, in effect the price cap becomes a massive hydrocarbon revenue transfer from Russia to China and India.

While this is perhaps not the impact that was envisioned for the price cap regimes, it does solidify that the price caps are achieving their stated goal of depriving Russia of hydrocarbon revenue even as Russian oil and refined products continue to flow.

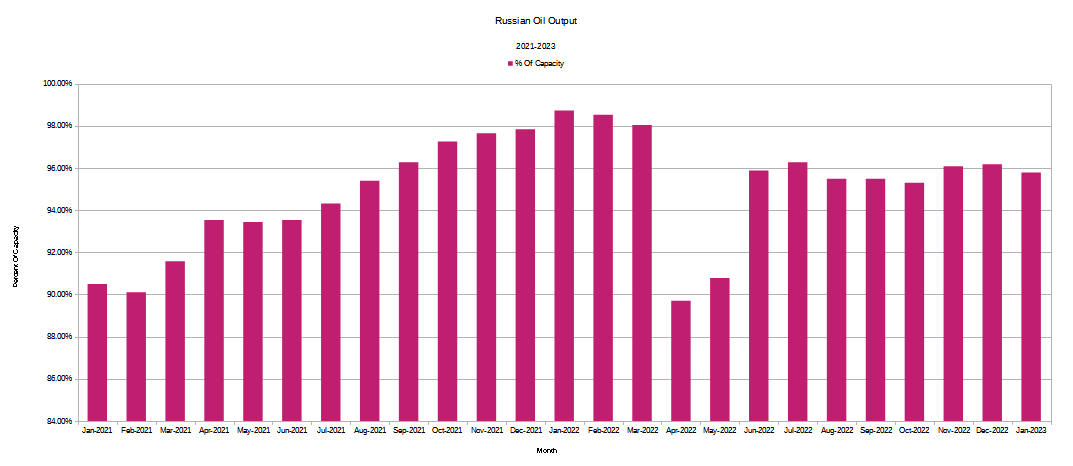

As regards Russia’s announcement of production cuts starting in March, this may be a continuation and possibly acceleration of an existing trend of declining Russian output. There have been signs that Russia has already been either trimming production or having production difficulties since before the crude oil cap was implemented.

Significantly, however, Russian production began to falter in February—before the invasion and attendant sanctions could have had an impact.

Russia is believed to have sustainable capacity of 10.2 million barrels per day, but has never achieved more than 98% of that amount, and, according to the IEA, is currently producing just over 95% of its sustainable capacity.

Even more disconcerting for Russia’s finances, its agreed-upon OPEC+ production target is actually 10.48 million barrels per day, which means Russia is only producing about 93% of what it can produce under the OPEC+ production regime.

Regardless of the reasons why, Russia is not producing as much crude oil as it once was, and is not producing anywhere near what it is permitted under OPEC+ quotas. If oil prices are not pushing upward even with reduced Russian output, it becomes far more likely the price caps will be sustained for a longer period than might have otherwise been believed.

Additionally, there are indications that Russia may be evading either the EU ban on imports of seaborne crude or refined products from Russia, or managing to evade the caps, through the use of a shadow fleet of ships that choose to operate outside mainstream shipping arrangements (meaning they do not get insurance or other financial services from the usual sources, and possibly do not get insurance at all).

There were now an estimated 600 vessels in a shadow fleet of ships helping Russia to keep flowing its refined oil – ships that need to be financed and insured outside of the major developed world markets. That leaves fewer vessels serving other oil exporters, which as a result has caused a spike in the price of carrying refined oil.

In addition, the EU banned Russian fuel imports from February 5th – the price caps apply to vessels with financial connections to the EU/G7/Australia, including insurance, carrying refined oil products to third-party countries. Prior to that the EU lifted its purchasing of refined products from elsewhere to ensure plentiful supply, which displaced some vessels in a restricted fleet.

Pricing data from Platts, a unit of S&P Global, suggest traders are garnering an unusually large margin on shipments of Urals crude sent from Russia’s ports in the Baltic region to India’s west coast, with delivery prices more than $20 a barrel higher than the purchase amounts.

Analysts at Goldman Sachs, in a Feb. 10 note to clients, said the effective price of Russian oil may be far higher than what’s often reported, and that might help explain why Russian oil production has remained resilient.

Exactly how this would work is indeterminate from the reporting, unless Russia is using a series of fronting entities which seemingly purchase Russian oil below the cap, then sell it at closer to actual market prices, with Russia managing to get some or all of the margin through a back channel.

Russia's federal budget showed a deficit of 1.776 trillion rubles in January according to preliminary data, which was 14 times the 125 billion ruble deficit in January last year and amounted to 60% of the total year plan for 2023 of 2.925 trillion rubles, the Finance Ministry said on its website.

Revenues in January were 1.356 trillion rubles, 35% less than revenues received a year earlier. Oil and gas revenues were 426 billion rubles, down 46% from January 2022. This is primarily due to a decrease in prices for Urals crude and a decrease in natural gas exports, the ministry said. Non-oil revenues were 931 billion rubles, down 28%, due primarily to a decrease in domestic VAT and income tax revenues.

The amount of false economic data Russia would be releasing to conceal any back-channel method of evading either the EU bans or the price caps is fairly substantial and would be quite the complex undertaking. While this doesn’t disprove Goldman’s speculation, it does greatly lower its probability of being accurate.

While the possibility that Russia has found a way to surreptitiously evade the caps cannot be wholly dismissed, the far more probable scenario is that the market data and Russia’s economic data are as they are, which would mean Russia is not evading the price caps, and is losing considerable oil revenues as a result. If Russia has not found a way to evade the price caps, then the market price data we have for Urals crude and other hydrocarbon prices suggest that, for now, the price caps are holding.

However, much still hinges on the overall state of global oil demand, and in particular how much additional demand will come in the near future from China as it struggles to restart its economy after Zero COVID. The refined products cap and Russia’s production cuts announcement did manage to move the price of Urals crude towards the price cap level of $60/bbl, which suggests there is an upper limit to how high oil prices can rise globally before the $60/bbl price cap gives way, and Urals crude commands a higher price.

For now, the price caps appear to be working, and Russia’s oil and hydrocarbon revenues appear to have been significantly curtailed. Whether that will continue to be the case will be an ongoing open question for the foreseeable future.

All Facts Matter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber. Alternatively, please consider leaving a tip through Ko-Fi. Thank you always for your support!