As with the first estimate, there were reasons to smile and there were reasons to frown.

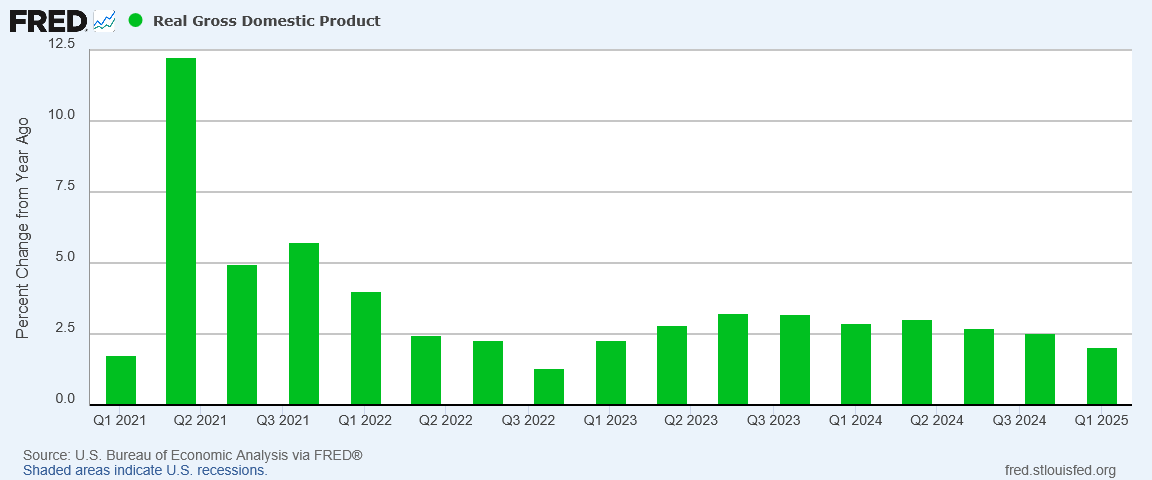

Real gross domestic product (GDP) decreased at an annual rate of 0.2 percent in the first quarter of 2025 (January, February, and March), according to the second estimate released by the U.S. Bureau of Economic Analysis. In the fourth quarter of 2024, real GDP increased 2.4 percent.

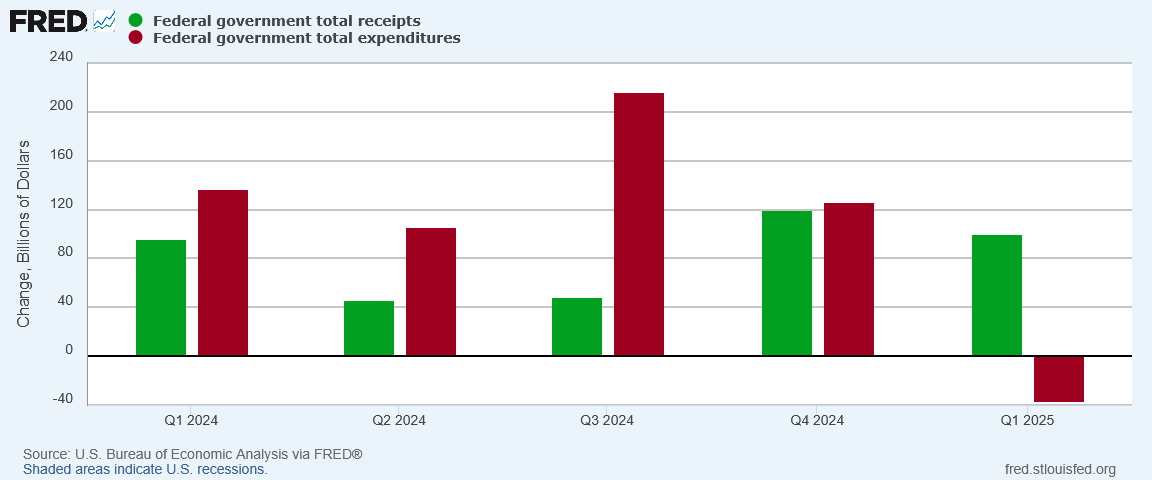

The decrease in real GDP in the first quarter primarily reflected an increase in imports, which are a subtraction in the calculation of GDP, and a decrease in government spending. These movements were partly offset by increases in investment, consumer spending, and exports.

Real GDP was revised up 0.1 percentage point from the advance estimate, reflecting an upward revision to investment that was partly offset by a downward revision to consumer spending.

In the second estimate, investment was found to have been larger than in the advance estimate. In direct consequence, the decline in real GDP was 0.1 percentage points less than originally thought.

The decline is still due entirely to a surge in imports, a reaction to the Trump Administration’s banging the tariff drum since the first day of Donald Trump’s Presidency.

Broadly speaking, the assessment of the US economy is still the same: there are still reasons to smile and there are still reasons to fround in the First Quarter GDP Estimate.

Sounds pretty good - especially in contrast to all of the doomsayers who screamed that Trump would ruin the economy! (Of course, he still might, if the tariffs don’t work as planned.)

Sounds pretty good - especially in contrast to all of the doomsayers who screamed that Trump would ruin the economy! (Of course, he still might, if the tariffs don’t work as planned.)

Thanks for the update, Peter. You’re the best!