Most economists and most Americans have a similar definition of recession: substantial job losses and mass layoffs, businesses shutting down, private sector activity slowing considerably, family budgets under immense strain. In sum: a broad-based weakening of our economy.

That is not what we're seeing right now when you look at the economy. Job creation is continuing, household finances remain strong, consumers are spending, and businesses are growing.

Household finances are, of course, hardly strong, as consumer price inflation is wreaking havoc with that most basic of household budget items, the grocery list, driving more American families to seek help from food banks and church food pantries.

Households struggling to put food on the table do not have “strong” finances by definition.

Yet even beyond this obvious flight of fancy, what about her assertion that jobs are being created? With the number of employed people in the US having declined since March, how credible is a claim of robust jobs marketplace?

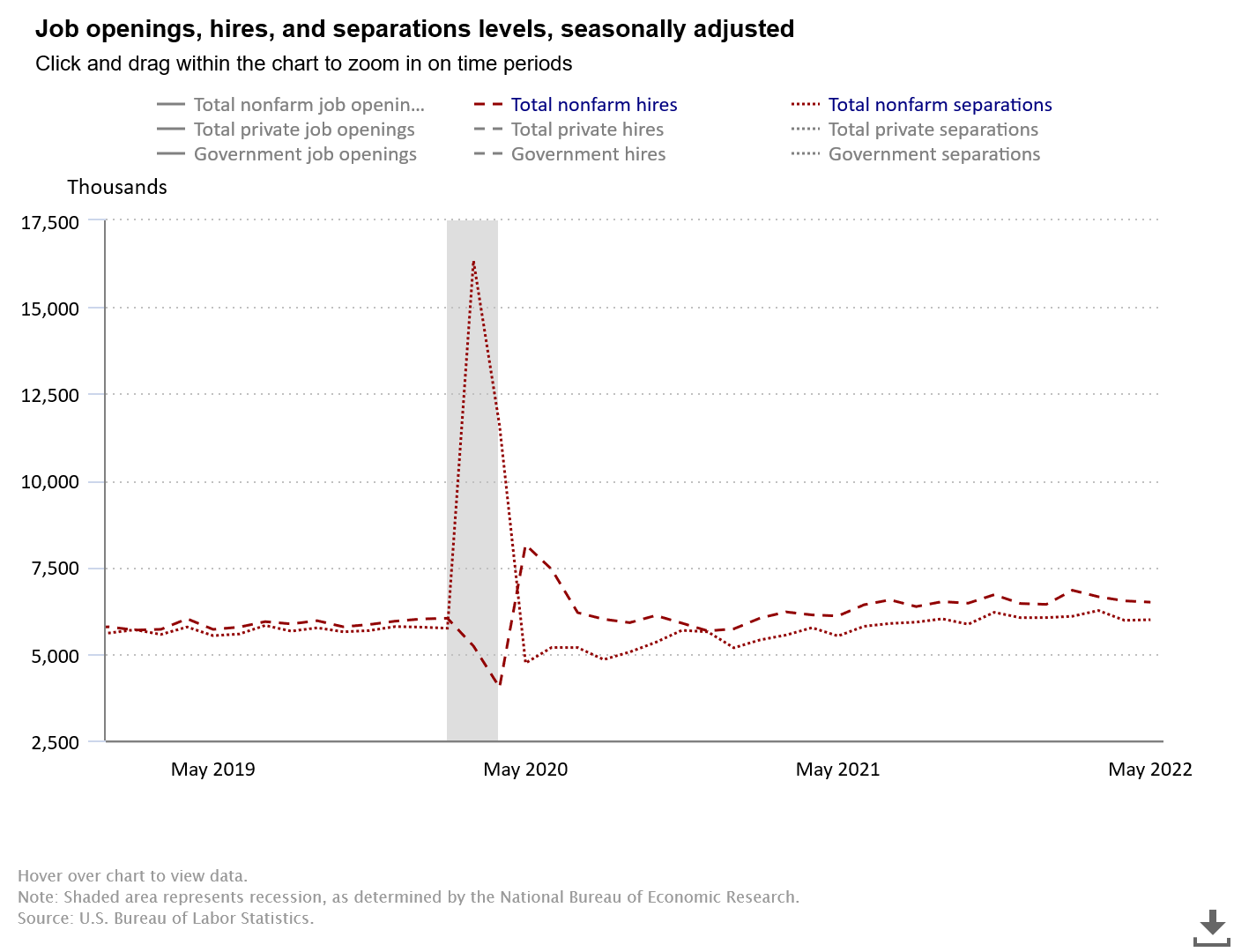

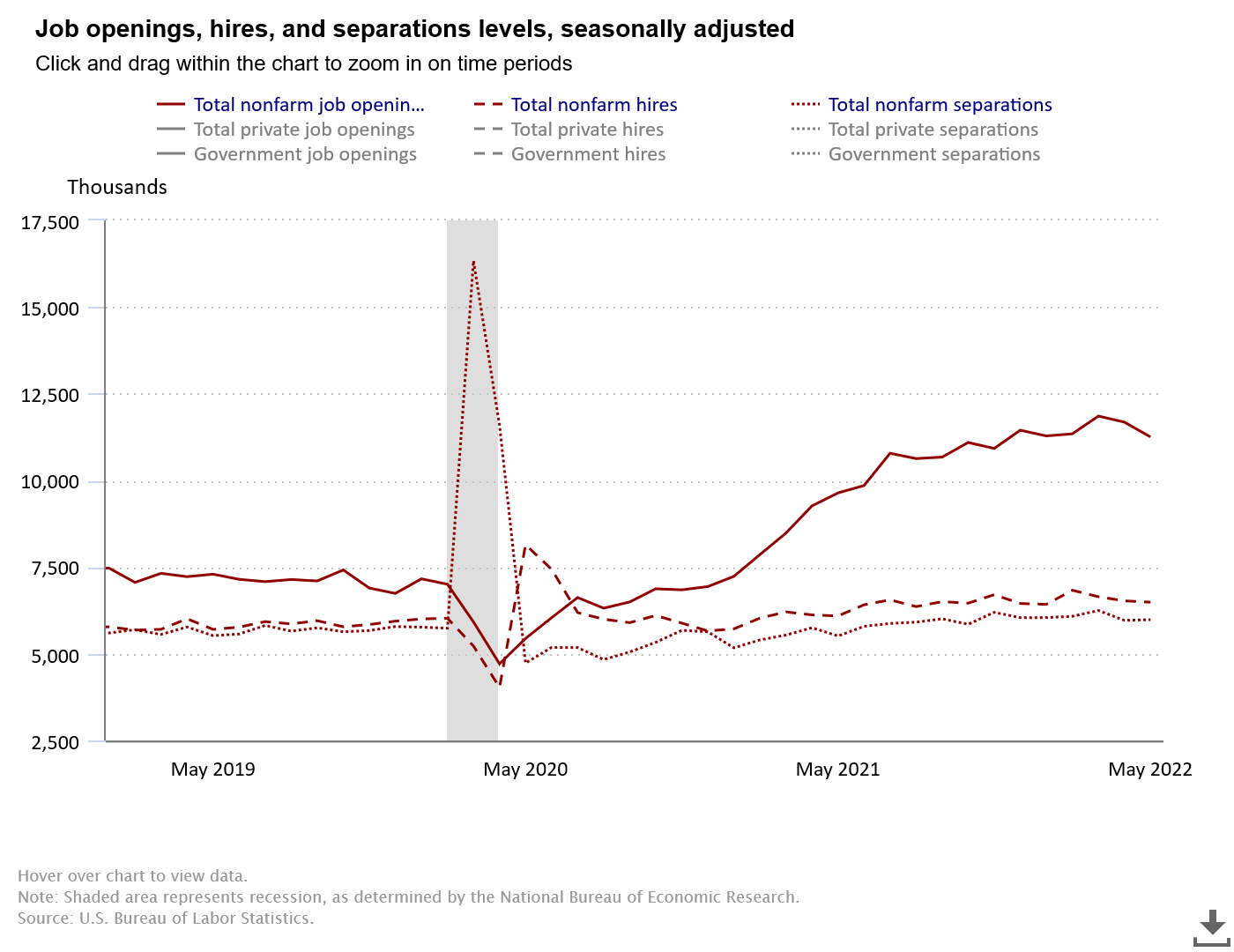

On the surface, the labor market certainly appears to be tight. As of the May Job Openings and Labor Turnover Survey, the number of unemployed workers in the US was approximately half of the number of job openings reported.

There are, however, anomalies within the jobs data that simply cannot be overlooked. Most importantly, the number of workers actually working has declined slightly since March—and declined both in terms of wage and salary workers as well as self-employed workers. Even the number of part time workers shrank.

Certainly the greater difficulty employers appear to have in filling job openings leads one to conclude there is a dearth of available workers. The ratio of monthly hires to announced job openings—the rate at which those openings notionally are being filled, in other words—has been declining steadily since 2020.

When roughly 40% of job openings go unfilled each month, that surely indicates there is a “tight” labor market…doesn’t it?

The Great Resignation

One aspect of the current jobs market that should not be ignored is the increase in the number of job quits among the monthly number of job separations. While formal layoffs have remained largely the same through May, the number of quits post-pandemic is noticeably higher than pre-pandemic in 2019.

This is the phenomenon many employment watchers have termed “The Great Resignation”. Workers are decidedly less satisfied with their jobs post-pandemic than pre-pandemic, and are expressing that dissatisfaction by leaving.

The wave of people leaving their jobs over the past few years is showing no signs of slowing down, and for many willingly choosing to quit, a massive reinvention of their ideal career is underway.

The number of employees who are considering quitting their jobs right now is around 40%, a number that hasn’t changed much in recent months.

That trend is surely encouraged when employers go to great lengths to hire needed staff, even to the extent of offering lucrative starting bonuses and wages—a trend which in Chicago has recently resulted in hospitality businesses ruthlessly poaching workers from each other.

While “recruiting” workers from fellow restaurateurs by flashing $100 bills and assuring lucrative pay is uncommon, the urgency to staff the Chicago hospitality industry has reached a fever pitch this summer, fomenting what some in the hospitality business are calling “a survival of the fittest” environment.

A labor environment where workers feel confident in leaving their current jobs would certainly seem to be an overall healthy one.

And Yet…Layoffs

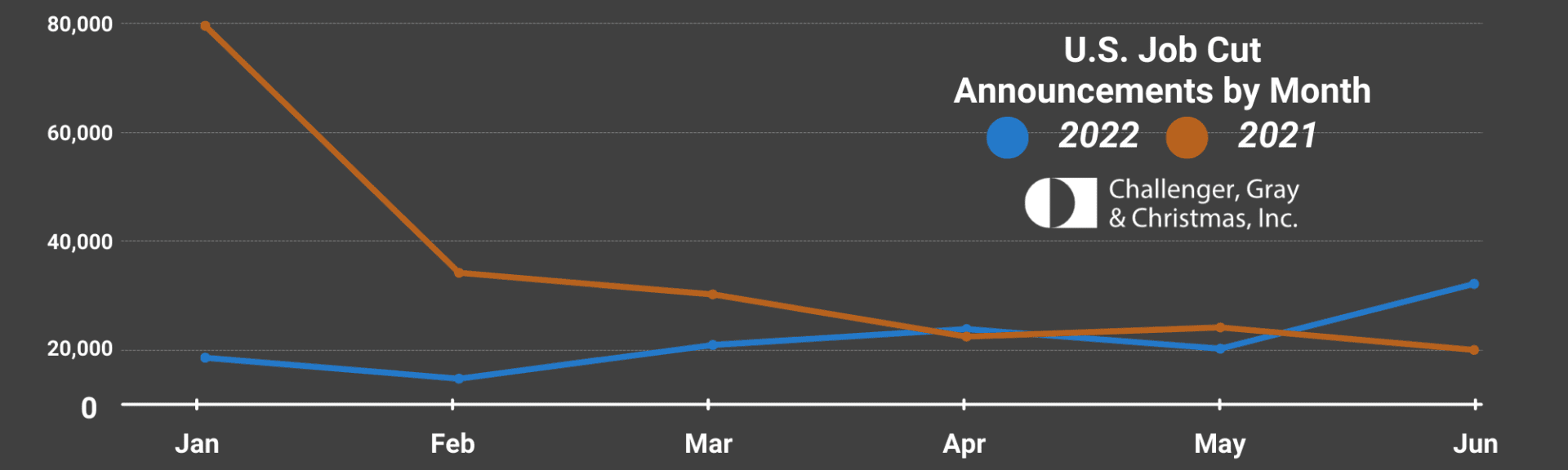

Still, the layoffs are happening, and appear to be increasing. The June Job Cuts Report by outplacement firm Challenger, Gray, and Christmas showed a dramatic surge in layoffs, both over May’s totals and last year’s.

U.S.-based employers announced 32,517 cuts in June, a 58.8% increase from the 20,476 cuts announced in the same month last year. It is 57% higher than the 20,712 cuts announced in May, according to a report released Thursday from global outplacement and business and executive coaching firm Challenger, Gray & Christmas, Inc.

According to the data compiled by Crunchbase, more than 32,000 workers in the US tech sector have been laid off in mass job cuts, as of late July. "We've included both startups and publicly traded companies that are based in the US. We've also included companies based elsewhere that have a sizable team in the United States, such as Klarna," the analysis said.

While Secretary Yellen speaks of jobs being created, the tech industry is shedding jobs, cutting costs and staff to weather the deepening recession.

Once high-flying companies, with unprecedented valuations and growth-at-all-costs strategies, have started to scale back, as the economy appears to be heading for a slowdown. The efforts, which started in May, have resulted in massive layoffs at several firms, from startups to publicly traded companies worth billions of dollars.

Such reported trends serve to cast doubt on the government’s claims of job creation, a claim which is immediately made suspicious owing to the unusually high level of job openings coupled with the seeming inability to fill those openings.

Since the end of the 2020 recession, companies claim to be hiring large numbers of workers (job openings), yet the number of actual hires is not even on the same general trend. That is hardly a healthy indicator for the jobs market.

Beware The Lou Costello Labor Math

Readers will by now be familiar with my term for the odd government jobs counting methods which produces jobs growth without seeing a growth in overall employment: Lou Costello Labor Math. It was very much in evidence in January’s Employment Situation Report and it was tellingly on display last month as well.

The polite explanation for these massagings of the numbers is simply politics. The Biden Regime, like their predecessors in the White House, are perpetually loathe to admit any negativity in the American economy, and so have great incentive to make jobs numbers especially appear better than they are.

However, while the BLS can spin the top level numbers, the data underneath is much harder to disguise. If the Challenger Job Cuts Report for June is any guide, today’s JOLTS report will show a rise in layoffs, even if job quits do not shrink—which seems unlikely since the job quitting trend is by now a long-term one.

The true picture to be painted by the JOLTS report, as by the Employment Situation report due at the end of the week, will be that of a fundamentally broken labor market. A large number of jobs in the US are simply not considered “good jobs” by the workers who fill them—and who are as a result refusing to fill them. Meanwhile, the Fed is determined to prevent those jobs from being made any better—for the sake of fighting inflation, the Fed is Hell-bent on eliminating workers’ new-found market power to press for higher wages and better working conditions.

What we have is a toxic jobs outlook in this country, not a healthy one.

All Facts Matter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber. Alternatively, please consider leaving a tip through Ko-Fi. Thank you always for your support!

Louis Francis Cristillo (March 6, 1906 – March 3, 1959), professionally known as Lou Costello, was an American comedian and actor. He was best known for his double act with straight man Bud Abbott and their routine "Who's on First?".

The comedians, who teamed up in burlesque in 1936, were among the most popular and highest-paid entertainers in the world during World War II. During a national tour in 1942 they sold $85 million in war bonds in 35 days. By 1955, their popularity waned due to overexposure, and their film and television contracts lapsed. Their partnership ended in 1957.

Louis Francis Cristillo (March 6, 1906 – March 3, 1959), professionally known as Lou Costello, was an American comedian and actor. He was best known for his double act with straight man Bud Abbott and their routine "Who's on First?".

https://www.youtube.com/watch?v=kTcRRaXV-fg

The comedians, who teamed up in burlesque in 1936, were among the most popular and highest-paid entertainers in the world during World War II. During a national tour in 1942 they sold $85 million in war bonds in 35 days. By 1955, their popularity waned due to overexposure, and their film and television contracts lapsed. Their partnership ended in 1957.

--Wiki

So Peter, I have but a single question:

"Who's on first?"