Switzerland Cuts Rates, UK Stands Pat

Is Wall Street Wrong About Coming Central Bank Rate Cuts?

Two significant central banks made divergent interest rate decisions last week.

The Bank of England opted to follow the Fed’s stance and hold its bank rate at 5.25%.

The Bank of England’s Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 20 March 2024, the MPC voted by a majority of 8–1 to maintain Bank Rate at 5.25%. One member preferred to reduce Bank Rate by 0.25 percentage points, to 5%.

Since the MPC’s previous meeting, market-implied paths for advanced economy policy rates have shifted up. In the United States and the euro area, inflationary pressures have continued to abate, though by slightly less than expected. Material risks remain, notably from developments in the Middle East including disruption to shipping through the Red Sea.

However, the Swiss National Bank made the surprise decision to trim its central bank rate by 25 basis points.

The Swiss National Bank is lowering the SNB policy rate by 0.25 percentage points to 1.5%. The change applies from tomorrow, 22 March 2024. Banks’ sight deposits held at the SNB will be remunerated at the SNB policy rate up to a certain threshold, and at 1.0% above this threshold. The SNB also remains willing to be active in the foreign exchange market as necessary.

The easing of monetary policy has been made possible because the fight against inflation over the past two and a half years has been effective. For some months now, inflation has been back below 2% and thus in the range the SNB equates with price stability. According to the new forecast, inflation is also likely to remain in this range over the next few years.

A Reuters poll of economists had forecast the SNB would also hold the line on rates at 1.75%. However, current inflation forecasts for Switzerland suggest that the rate cut is less remarkable than it might seem at first glance, and might not be the last one.

Following the announcement, analysts at Capital Economics said they expect two more SNB rate cuts over the course of this year, “with the Bank sounding more dovish and inflation likely to undershoot its forecasts.”

“We think inflation will come in even lower than the new SNB forecasts imply and remain around the current level of 1.2% before falling to below 1.0% next year. Accordingly, we forecast the SNB to cut rates at the September and December meetings taking the policy rate to 1%, where we think it will remain throughout 2025 and 2026,” Capital Economics analysts said in a note.

Have the central banks of the world concluded that the time for tightening policy and raising rates is over, and the question is when, how far, and how fast should rates be reduced? Is Switzerland an outlier or a precursor of the next market trend on interest rates?

While the BoE is holding the line on its central bank rate for now, unlike the Fed last week, BoE governor Andrew Bailey was sounding decidedly optimistic that rate cuts would be coming soon.

Andrew Bailey told the Financial Times that rate cuts were “in play” at future meetings of the BoE Monetary Policy Committee amid signs that tighter policy had quelled the risk of a wage-price spiral.

“It’s like the Sherlock Holmes dog that doesn’t bark. If the second-round effects don’t come through, that’s good because monetary policy has done its job,” he said.

“We have an increasingly positive story to tell on that,” Bailey added. “The global shocks are unwinding and we are not seeing a lot of sticky persistence [in inflation] coming through at the moment. That is the judgment we have to keep coming back to.”

This was far more direct an assessment of the economic environment than Fed Chairman Jay Powell was willing to give last week after the FOMC announcement, who could only muster up word salad nonsense.

And in terms of the timing, I said “fairly soon.” I wouldn’t want to try to be more specific than that. But you get the idea. The idea is—and this is in our—in our longer-run plans, that we may actually be able to get to a lower level, because we would avoid the kind of frictions that can happen. Liquidity is not evenly distributed in the system. And there can be times when in the aggregate reserves are ample or even abundant, but not in every part. And those parts where they’re not ample there can be stress. And that can cause you to prematurely stop the process to avoid the stress. And then it would be very hard to restart, we think. So something like that happened in ’19, perhaps.

So that’s what we’re doing. We’re looking at what would be a good time and what will be a good structure. And, you know, “fairly soon” is words that we use to mean fairly soon.

Certainly the Wall Street “experts” are pushing a narrative that the SNB decision marks an inflection point on global central bank policy, and that the future trend on central bank rates is going to be down.

“The writing is on the wall. It’s not whether central banks will cut rates but when,” said Stefan Gerlach, a former Irish central-bank official who is now chief economist at EFG Bank in Zurich. He expects major central banks to cut rates by as much as 2 percentage points over the next 18 months.

Coming the same week that Japan ended negative rates after more than a decade, Switzerland’s move signals a return to normality for central banks, Gerlach said. A series of economic shocks, from the 2008 global financial crisis to the pandemic, had triggered extreme and unconventional reactions that left monetary policy extremely loose in Japan and extremely tight in the U.S. Both sets of extreme policies look to be coming to an end.

Key in that narrative, of course, is the presumption that central banks have at last been able to take control on consumer price inflation. However, that is where the data becomes murky and the trends become imprecise.

On the one hand, it the Swiss decision to trim its central bank rate is not all that controversial. Switzerland itself has had a much milder experience with inflation than the rest of Europe as well as the United States.

Even Switzerland’s core inflation rate is better behaved, coming in 10 basis points below the Swiss headline inflation rate.

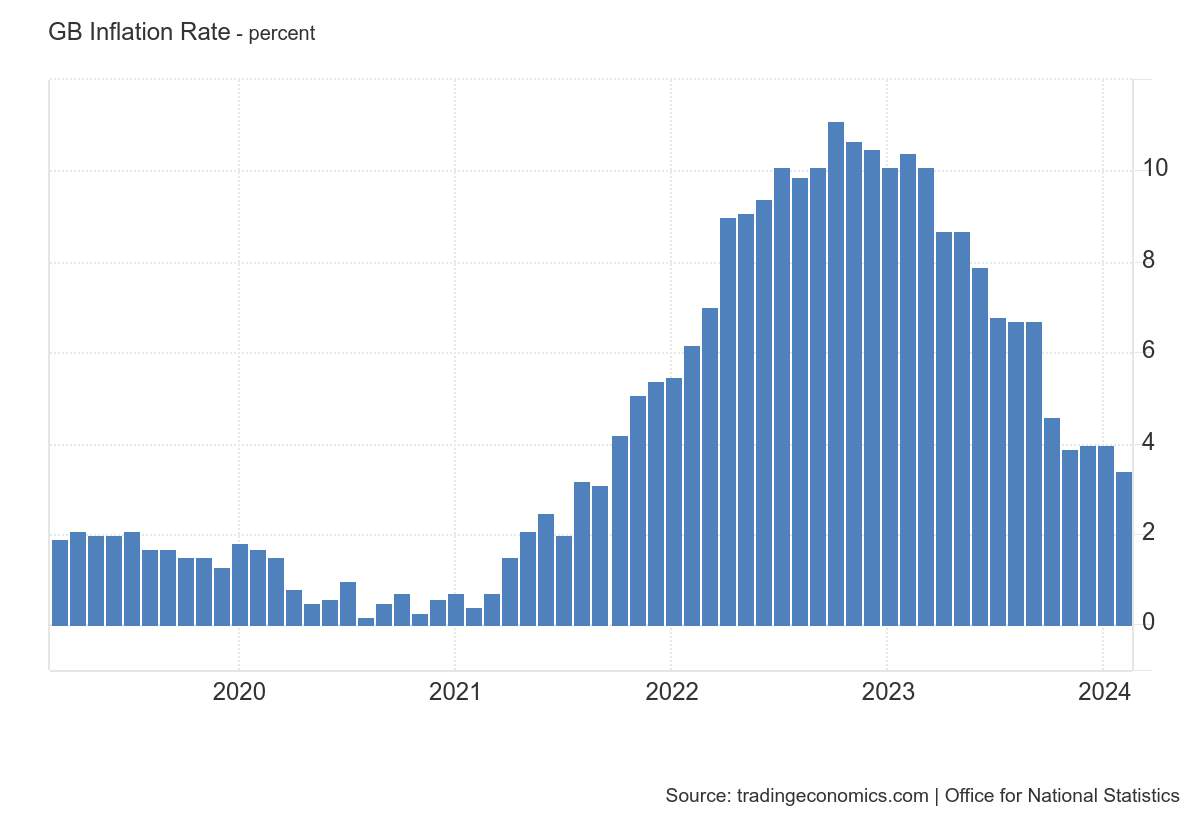

The United Kingdom, on the other hand, has endured much higher inflation, and still has much higher inflation than Switzerland.

Unlike Switzerland, and like the United States, the UK’s core inflation rate is a full percentage point higher than the headline inflation rate.

Yet even in the UK, year on year headline and core inflation rates are coming down each month, just as in Switzerland, so it certainly appears reasonable that the SNB would feel comfortable in trimming rates, and it does not appear out of bounds that Andrew Bailey would talk positively about trimming rates as early as this summer.

At the same time, while year on year inflation is down in Switzerlanx, month on month inflation is rising, and rising sharply.

The trend is far less certain in the UK, where month on month inflation has been up and down from month to month recently.

Intriguingly, the wider Euro Area month on month inflation rate is reflective of what is being seen in the UK.

Switzerland, on the other hand, is showing a month on month inflation trend more similar to that of the United States.

Switzerland’s month on month producer prices are also showing an upward trend recently, first with a slowing deflation trend and finally flipping to outright inflation last month.

This again is more reflective of the United States than the Euro Area which is in Switzerland’s own back yard.

While Switzerland overall enjoys a much lower inflation rate than the UK, the US, or the wider Euro Area, at the same time it is seeing the same rising inflation trends that the United States is seeing, and which are confounding attempts by Wall Street to anticipate when the Federal Reserve will trim the federal funds rate.

The Wall Street narrative is certainly promoting the idea of central banks trimming interest rates sooner rather than later, even though the Federal Reserve in particular remains thoroughly confused on the matter—Jay Powell is blissfully unaware, or so it seems, that inflation is actually rising in the United States!

Powell’s ignorance of the data extends to simply being wrong about what the most current data shows, particularly as regards inflation:

Q: Thank you. A mic for me. Steve Liesman, CNBC.

Mr. Chairman, the projections show somewhat higher core inflation. They also show somewhat stronger growth. What should we infer from this notion that on average rates were kept the same this year but inflation is higher and growth is higher? Does it mean more tolerance for higher inflation and less of a willingness to slow the economy to achieve that target?

MR. POWELL: Well, it doesn’t—no, it doesn’t mean that. What it means is that, you know, we’ve seen incoming—as I pointed out in my opening remarks we did mark up our growth forecast and so have many other forecasters. So the economy is performing well, and the inflation data came in a little bit higher as a separate matter and I think that caused people to write up their inflation.

But, nonetheless, we continue to make good progress on bringing inflation down and so—

The problem with the assertion that the Fed is making progress on bringing inflation down is that for the past several months, month on month consumer price inflation per the CPI has been increasing.

It is an ironic counterpoint that Powell’s opposite number in the Bank of England is less muddled about inflation in the UK while the UK data is more muddled than in the United States.

Yet even in the UK, while there is not a clear trend of rising inflation, neither is there a clear trend of month on month deflation or even disinflation. If anything, inflation’s behavior in the UK as well as in the wider Euro Area is more typical of the bottom of a curve, which would suggest that inflation has reached a minimum and may soon begin to trend back up again.

While the corporate media and Wall Street narrative is a predictably optimistic assessment that Switzerland is the first among the major central banks to begin reducing central bank rates, the broader global inflationary outlook suggests that Switzerland may yet prove to be just an outlier. If inflation trends in the US continue to rise, and if inflation in the UK and the Euro Area has in fact reach a bottom, then the future outlook on inflation globally is for rising inflation in the near term, not disinflation.

Within the central bank logic of raising interest rates to choke off and corral inflation, renewed rising inflation is a recipe for holding interest rates higher for longer, not trimming them sooner rather than later—and renewed rising inflation is a far more supportable extrapolation of the current data than the Wall Street narrative of disinflation to drive rate cuts.

Is Wall Street poised to be dramatically wrong on interest rates yet again? The outcome is not certain, but that remains a very good possibility, perhaps even a probability.

I’m so disappointed in all of these central bankers such as Powell, who apparently does not do his own grocery shopping. If he had bought a loaf of bread three months ago and then bought one last week it would be immediately apparent - duh! - that prices continue to rise.

So I wonder to what extent these finance pros are taking seriously, and factoring into their decisions, possibilities such as deflation contagion from China, bank liquidity problems from the continued decline of commercial real estate, and the other looming economic problems you have warned about. Peter, do you see anything in their press releases that lead you to believe they are considering such problems in their decisions, or are they hopelessly clueless?

Peter, my iPad is dying, won’t charge - I’ll return in a few days....