Since my last article, the war with Iran has managed to become even more chaotic, and the fog surrounding that war has become thicker and more impenetrable.

Late last week, Iraq announced it was declaring “force majeure” for all oilfields developed and operated by foreign oil interests. That same day President Trump issued an ultimatum to the Khamenei regime: surrender now or Iran’s power plants woud be destroyed. Iran responded by threatening oil and natural gas production across the Persian Gulf region.

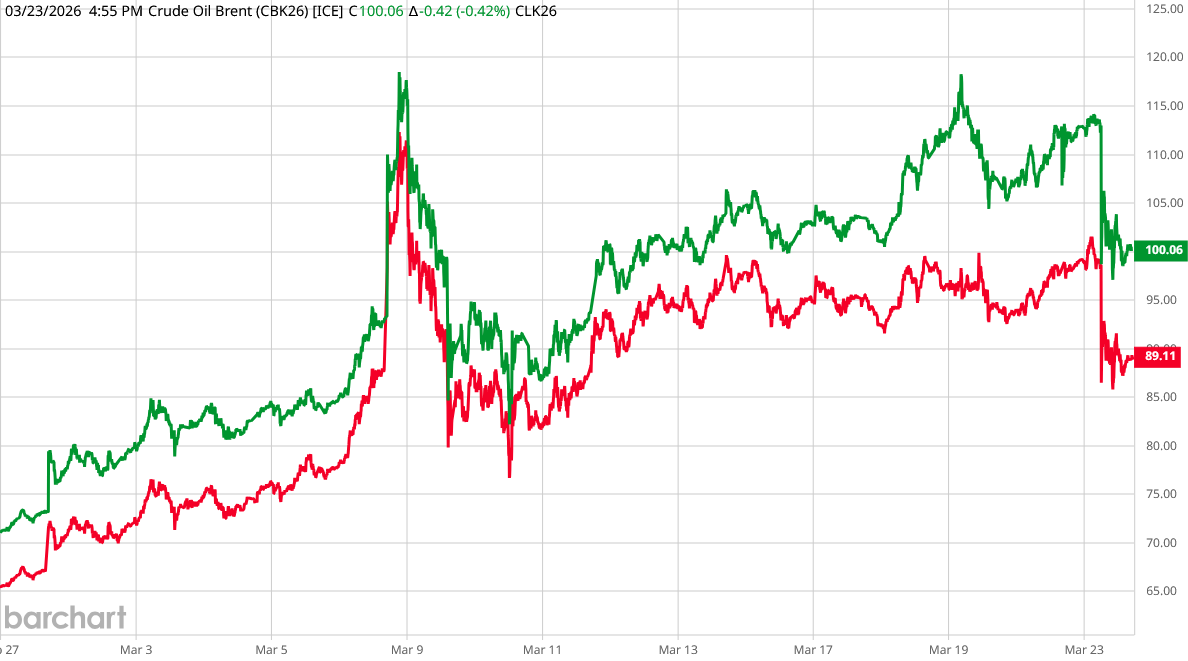

Oil, which had been stabilizing around $100/bbl for Brent Crude, soared yet again. Stock markets in turn dropped dramatically.

Yesterday morning came the news that President Trump and the Iranians were “talking”, leading Trump to postpone any deliberate targeting of the Iranian power grid.

Such has been the chaos of Operation Epic Fury over the past few days, whipsawing from the fallout of war, to major escalation, to possibly a chance for peace.

Do we know how this war will end? No, we do not. We cannot extrapolate with any certainty along any lines to project a final outcome. How this war ends is not merely unknown, it is completely unknowable.

Arab Oil Production At Risk

There was little doubt that the global economic fallout from this war was intensifying when the Iraqi Oil Ministry, in a letter dated March 17 and made public March 21, declared “force majeure” on all foreign-operated oil fields, ordering a complete halt to all production.

Iraq’s Oil Ministry sent a letter dated March 17, seen by Reuters, stating that navigation through the Strait of Hormuz has been severely affected by “unprecedented military activity,” causing storage capacity to reach its limits.

“The international partners were unable to nominate tankers to lift crude, preventing exports despite the state oil company SOMO being ready to load shipments,” the letter said.

“Based on the situation, the ministry ordered a full shutdown of production at affected concession areas, with no compensation arising from the measure under contract terms,” the letter noted.

Iraq’s oil output was promptly slashed by 70%, to 900,000 barrels per day.

Iraq’s declaration underscores one of the logistical realities of oil production: oil wells depend on being able move the oil to someplace else. When oil shipments are disrupted, not only does oil not get to its intended destination, but the backlog can quickly extend back to the wellhead, as oil storage capacity is filled. When there is no more spare oil storage, oil producers have no choice but to shutter at least a portion of production capacity.

While Iraq’s force majeure declaration was the most dramatic, it was not the first disruption of oil production attributed to the war. Earlier last week it was reported that Saudi Arabia had reduced its oil output by 20% because of the war.

Middle East Gulf oil producers have had to shut vast volumes of production due to the blocking of the Strait of Hormuz, a narrow waterway between Iran and Oman, since the U.S. and Israel began airstrikes on Iran on February 28. Iran has said the world should prepare for oil prices at $200 a barrel.

It is one thing for oil tankers to be delayed on either side of the Strait of Hormuz. Such disruptions are, by their nature, temporary. All that is needed is a solution which can move tankers through the Strait.

It is quite another thing, however, when storage capacity at the oil terminals around the Persian Gulf is exhausted, and oil wells are obliged to stop pumping oil

While stopping the pumping process is fairly simple, restarting a stopped well is not nearly so straightforward. Once an oil well is shut down, a number of hurdles to restarting production tend to emerge, and will get worse the longer the well is shut in.

Some of those hurdles include precipitates such as paraffin, which can block the well itself. If the well is not filled with protective fluids, ground water and other external fluids can corrode and damage the well. There is even a risk of microbial contamination, necessitating particular care during well restart.

Iraq declaring “force majeure” over 70% of its oil production was tantamount to removing for the foreseeable future over 2 million barrels of oil output per day from global supply.

As I noted at the time of Iraq’s declaration, Iran’s asserting control over the Strait of Hormuz threatens Persian Gulf oil production in at least the near term:

An extended blockade of the Strait of Hormuz does not merely temporarily delay oil shipments. It threatens a long-term reduction in oil production capacity in the Persian Gulf, a reduction which will not be immediately eliminated once the blockade is even partially ended.

This is what Iran has done.

The near-term implications of Iran’s strategic decision regarding the Strait are nothing short of apocalyptic for the Persian Gulf. If Iran continues to retain control over the international waterway, Persian Gulf oil flows could stop altogether.

“48 Hours”

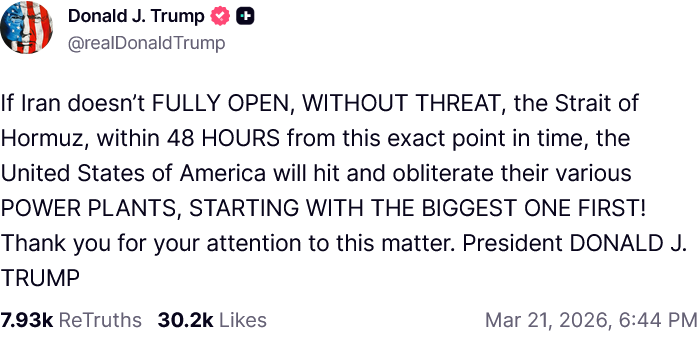

President Trump, faced with Iran continuing to threaten not only oil shipments from the Persian Gulf but oil production itself, responded in typical Trumpian fashion, escalating matters by issuing an ultimatum to Iran, posted via Truth Social: reopen the Strait of Hormuz in 48 hours or the US will begin bombing Iran’s power grid.

Iran responded in almost laconic fashion, with the Mehr news agency releasing a statement that said simply: “say good-bye to electricity.”

The outlet wrote, “Say goodbye to electricity,” and said that “with the smallest attack” on the Islamic Republic’s power infrastructure, “the entire region will fall into darkness.”

The statement was accompanied by a map showing the locations of major Arab power plants, highlighting how they were all within range of Iranian drones and missiles.

After Iraq’s force majeure announcement, and the earlier Saudi shuttering of its oil production, the apocalypse being threatened collectively by Iran and the US was more stress than oil markets were willing to tolerate. Brent Crude, which the week before had flirted with $120/bbl, surged towards that threshold again.

The timing of events was especially ironic, given that Federal Reserve Chairman Jay Powell had on Wednesday foolishly scoffed at the prospect that we might see a return of “stagflation”.

Even before the events of last weekend, it was clear that the war’s risks to the global economy were not insignificant.

Soft labor markets and some very nasty oil price shocks are what gave us stagflation in the 1970s.

We have soft labor markets. We are about to have a very nasty oil price shock.

Will we have a repeat of 1970s stagflation?

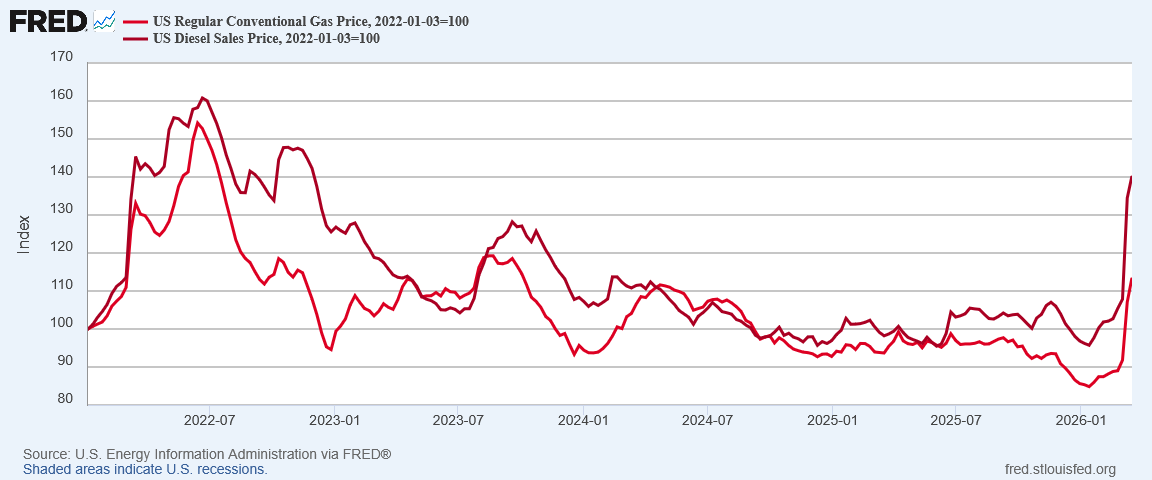

The surge in gas prices which has already occurred alone make for a severe price shock, potentially enough to usher in a stagflationary episode.

Wall Street looked at the potential energy crisis looming as a result of US and Iranian brinksmanship and accelerated its downward trend.

While it continues to be true that, as I have said previously, the US and Israel have for all intents and purposes won the war militarily, and have destroyed nearly every military target of significance in Iran, having an oil price shock of ever increasing magnitude bearing down on the global economy is not an outcome anyone would be able to sell as winning in a geopolitical sense.

Was President Trump on the verge of having won every battle with the Iranians—if the non-stop bombing can indeed be called a “battle”—only to lose the war itself?

Over the weekend, that was far from a radical or fringe interpretation of events.

“We’re Talking”

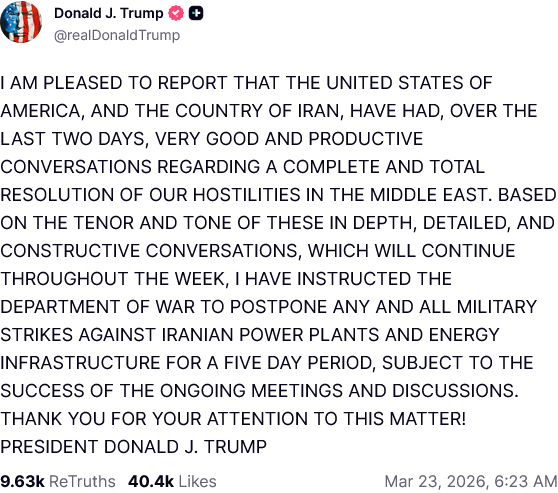

Yesterday morning, President Trump managed to flip the script yet again, posting on Truth Social that he had extended his ultimatum by five days, as a result of “productive” talks with Iran over ending the war.

And just like that, the price of oil dropped like a stone.

The optimism was infectious, as equities surged.

Apparently, there is no good news quite so pleasing to hear as an announcement that the Apocalypse is being postponed.

Never one to be satisfied with a linear narrative and an obvious geopolitical plus, Iran has reacted to Trump’s announcement by calling it a fabrication, denying that any talks were taking place.

Foreign Ministry spokesman Esmaeil Baghaei insisted Iran’s positions had not changed regarding the Strait of Hormuz.

In comments shared by the state news agency IRNA, Baghaei said: “Messages have been received from some friendly countries regarding the US’s request for negotiations to end the war.”

Iran responded by giving warnings about “the dire consequences of any attack on Iran’s vital infrastructure”, Baghaei said.

Iranian parliament Speaker Mohammad Bagher Ghalibaf, believed to be the person engaging with US Special Envoy Steve Witkoff, was similarly emphatic:

There is, of course, no way to independently verify the claims on either side, especially regarding which side made the first diplomatic overture. Both sides would clearly benefit from a peaceful resolution of this war—or at least a ceasefire—and yet both sides have powerful political reasons for not being perceived to be the one who backed down before the other.

What we know is that President Trump has issued a five-day delay, presumably in order to give peace a chance.

What we know is that Wall Street was quite relieved to hear that the Trump Administration were talking.

What we know is that Wall Street investors prefer a narrative of President Trump looking to “do a deal” with Iran over one of Donald Trump threatening to eradicate Iran’s vital infrastructures. For the moment, at least, President Trump has given them that narrative.

Check Your Assumptions

Wall Street is frequently a useful bellwether for gauging how various geopolitical events are being received. Movements in oil prices tell us how investors assess the risks of oil supply dislocations as a result of the war. Movements in equities are a useful proxy for gauging investor sentiment—and, by extension, public sentiment—surrounding the war with Iran (or any other major event).

Wall Street responses are by no means a measure of information accuracy, but they do provide context for the media narratives by which the details surrounding the war are presented.

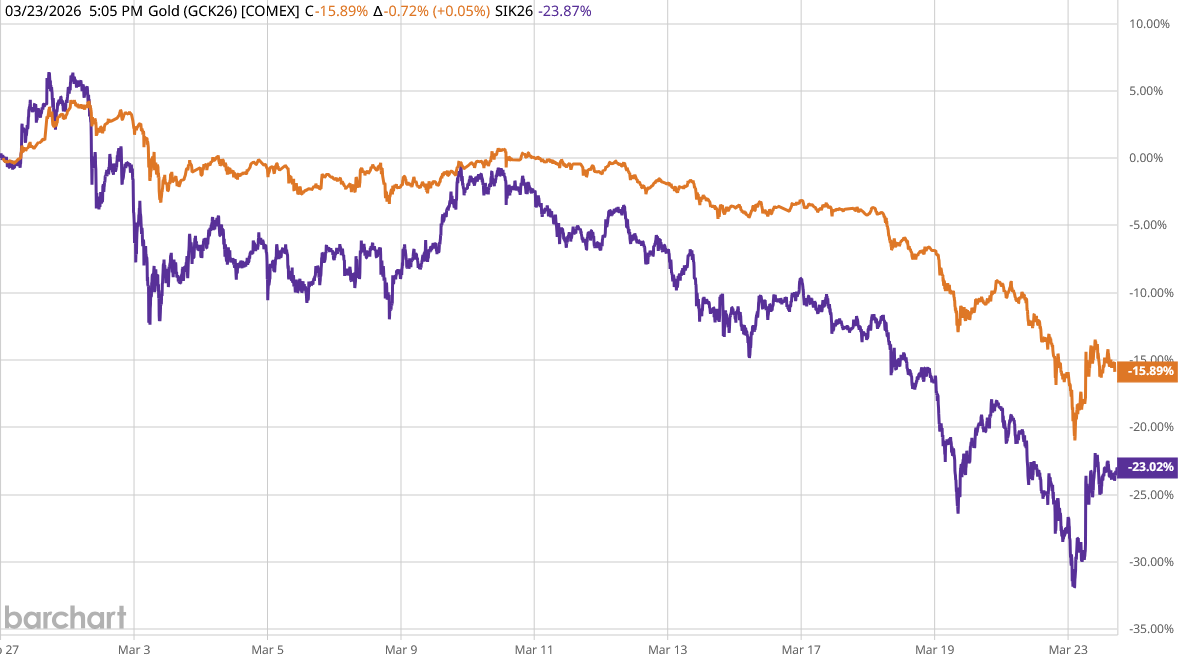

Ironically, the one asset class which has not performed well during the entire war is one we would expect to be doing extremely well: gold and precious metals.

Gold has long been considered as a hedge against inflation and geopolitical risk. Especially when war breaks out, we typically expect the price of gold to rise, as it did during the opening stretch of Russia’s invasion of Ukraine.

However, after a fleeting “flight-to-safety” moment at the very beginning, as Wall Street sentiment on the war has soured, gold as well as silver prices have dropped.

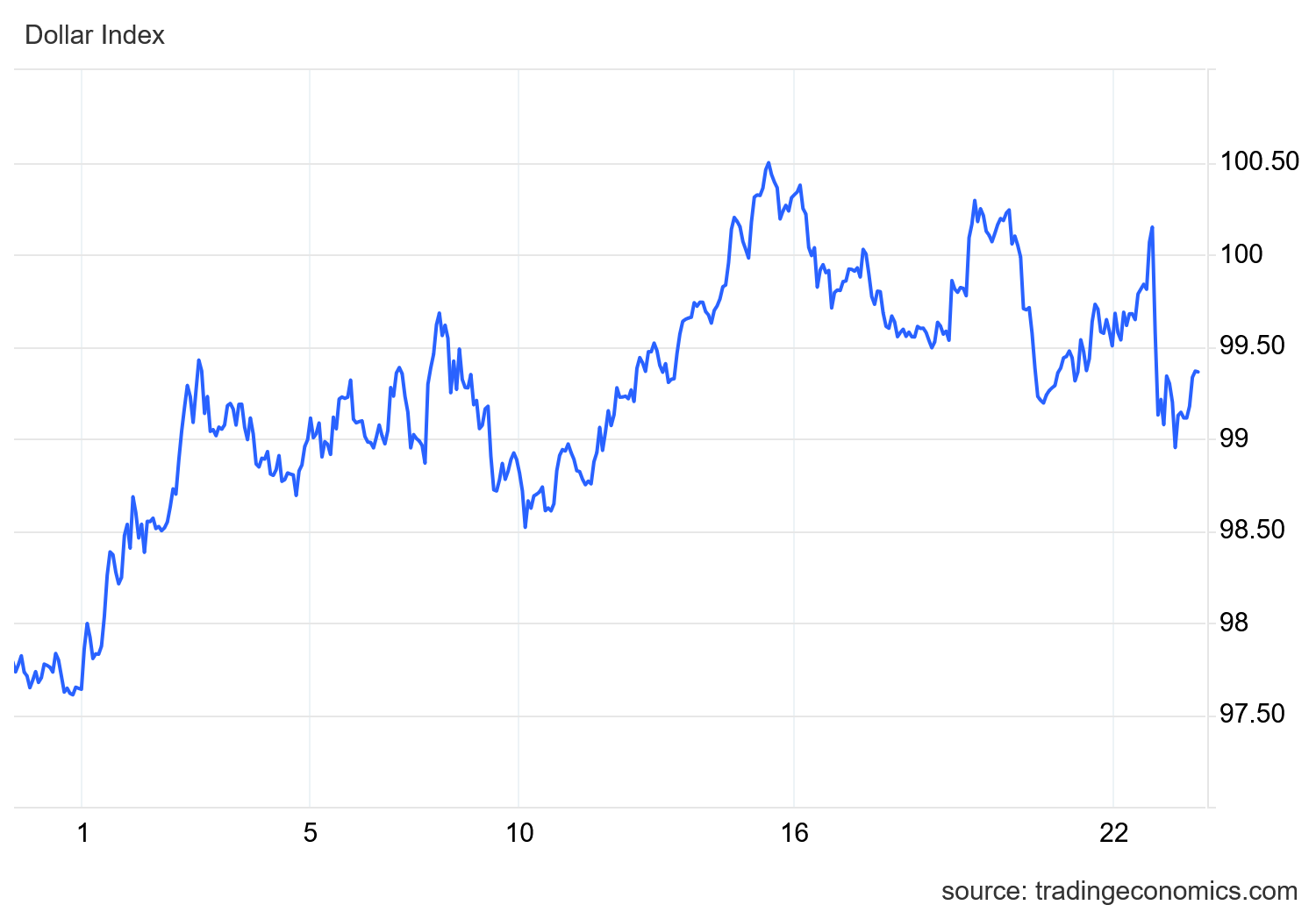

What has been the preferred “flight-to-safety” investment as the war with Iran has unfolded? Suprisingly, it has been dollars. On forex markets the Dollar Index has been climbing steadily since the start of Operation Epic Fury.

It is worth noting that forex investors responded to Trump announcing “productive” talks with Iran yesterday morning by dumping dollars. Peace prospects apparently do not contribute to the strength of the dollar.

These counterintuitive asset movements in response to evolutions in the war lend a vital perspective to assessing events as they unfold, as they are a constant reminder to check assumptions and question narratives. We do not expect gold to lose value during a geopolitical crisis, and during a war especially. We do not expect the dollar to become an attractive forex play when the United States decides to start a war. Yet these things have happened.

Whatever cherished assumptions and narratives people think are true about the Middle East as well as Donald Trump, people do well to check those underlying assumptions and question those prevailing narratives.

Nobody Knows

The challenge of chaos and confusion is that they make any sort of rational extrapolation of current events impossible. While we can assess probable outcomes if certain shifts are maintained, we can have no confidence that any shift will be maintained. Events just of the past few days have demonstrated just how fluid things continue to be within this war.

Will there be a peace deal struck between the Trump Administration and the Khamenei regime in Tehran? Nobody knows.

Are there actual talks taking place between members of the Khamenei regime and the Trump Administration? Nobody knows—certainly nobody outside of the Administration or the regime.

Will this war end in a geopolitical victory for Donald Trump, a defeat, or a stalemate? Nobody knows. There are simply too many unknowns (both known and unknown) to allow us to assess with any degree of confidence how they will get resolved. We do know that partisan assessments have already decided that President Trump has already either won or lost this war (depending on the political orientation of the one doing the assessing), but that sort of goal-seeking exercise sheds no real light on how much geopolitical influence Donald Trump and the United States might have gained or lost as a result of this war.

Will Iran’s moves compel the Arab states to move closer to the US and Israel, or to Iran? Nobody knows. Much hinges on whether the Arab states in the Persian Gulf region determine the dangers threatening their countries are more the handiwork of President Trump or of the Iranian regime.

If President Trump emerges from this war with a clear geopolitical win, it is reasonable to assess that perceptions of American strength and dominance worldwide will increase. Yet what if the outcome is not a clear geopolitical win? Will American strength be seen as diminished?

If the mullahs in Tehran survive this war and remain in control of Iran, is that enough for them to claim victory? It certainly seems likely they will at least make the claim, although the credibility of that claim is likely to be at least problematic.

If the mullahs in Tehran remain in control, does that mean the war has ended in a draw? Certainly that is a tempting conclusion to reach.

Will there be a popular uprising in Iran that topples the Khamenei regime? President Trump called for one in his very first address after the start of Operation Epic Fury, and there is little doubt that he would like to see the Iranian people dismantle the regime. However, as of this writing, no insurgency has erupted within Iran.

Could the bombings end, the kinetic operations cease, and there be a space of some months before a popular insurgency displaces the Khamenei regime? We cannot know if that would happen, although is certainly one possible scenario. If during the summer months the Khamenei regime were overthrown, President Trump would arguably deserve at least some credit for crafting an opportunity for the Iranian people to rise up.

Yet we also cannot dismiss the possibility that the mullahs remain in charge, and that there is no insurgency. We cannot dismiss the possibility that such an outcome may diminish Donald Trump’s overall political capital, both domestically and globally.

Virtually every conceivable scenario for what happens next in this war remains very much on the table. Virtually every conceivable scenario could be what happens next in this war.

Which of those scenarios will we see unfold? Nobody knows.

This is a smart and balanced assessment of where things stand, Peter. You’re right, there are too many variables and too many unknowns for anyone to be able to make predictions. The truisms that come to mind are “a chain is only as strong as its weakest link” and “war is a game of chicken” - but we have insufficient knowledge to guess where the weakest link is in this whole situation, or who is panicked enough to chicken out and swerve.

That leads me to ponder what Trump has up his sleeve in his gambit of a five-day pause. Is he maneuvering new troops, ships, and supplies to the region, and needs time for them to arrive? Are the Kurds bringing in arms to supply a civilian uprising? We’ll find out in five days, but Peter, if you hear any plausible speculations from military experts, please pass them along. I thank you again for all you do!

⛪🎶🕊️ Grace and peace to you Amigo,

https://claude.ai/public/artifacts/d4bf54e9-9f82-479c-a6e4-f04f9d81147e

Most Holy Theotokos save us! 🌐📖🔥🪽

Nine Months until Nativity 🌳 Luke One 🔔

.......Salvation becomes 🩸 InCarne! 🧵🪡

⚓ Semper Fortis and pray as if one of your own children was manning the walls of the Polis today!