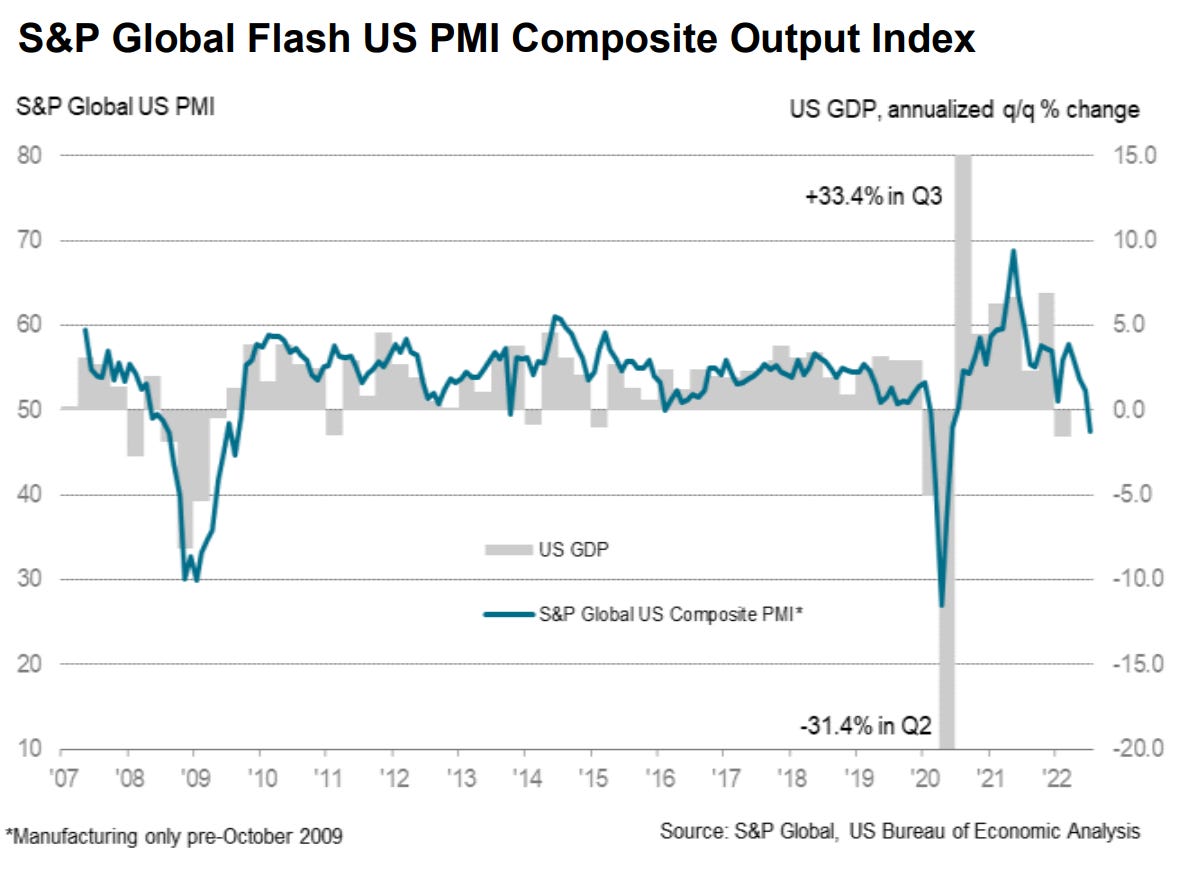

US private sector firms indicated the first contraction in business activity since June 2020 in July, according to latest ‘flash’ PMI™ data from S&P Global. The downturn in output signalled a further loss of momentum across the economy of a degree not seen outside of COVID-19 lockdowns since 2009. The downturn was led by a steep drop in service sector activity, though production at manufacturers also fell marginally, down for the first time in over two years.

Make no mistake, this is exactly what the Federal Reserve intends. I remind readers that Richmond Fed President Tom Barkin said this quiet part out loud back in June (emphasis mine):

Barring an unanticipated event, I see rising rates stabilizing any drift in inflation expectations and in so doing, increasing real interest rates and quieting demand. Companies will slow down their hiring. Revenge spending will settle. Savings will be held a little tighter. At the same time, supply chains will ease; you have to believe chips will get back into cars at some point. That means inflation should come down over time — but it will take time.

The Fed’s plan for curing toxic inflation is to poison the economy with high interest rates. It’s working.

“The way to crush the bourgeoisie is to grind them between the millstones of taxation and inflation.”

Vladimir Lenin