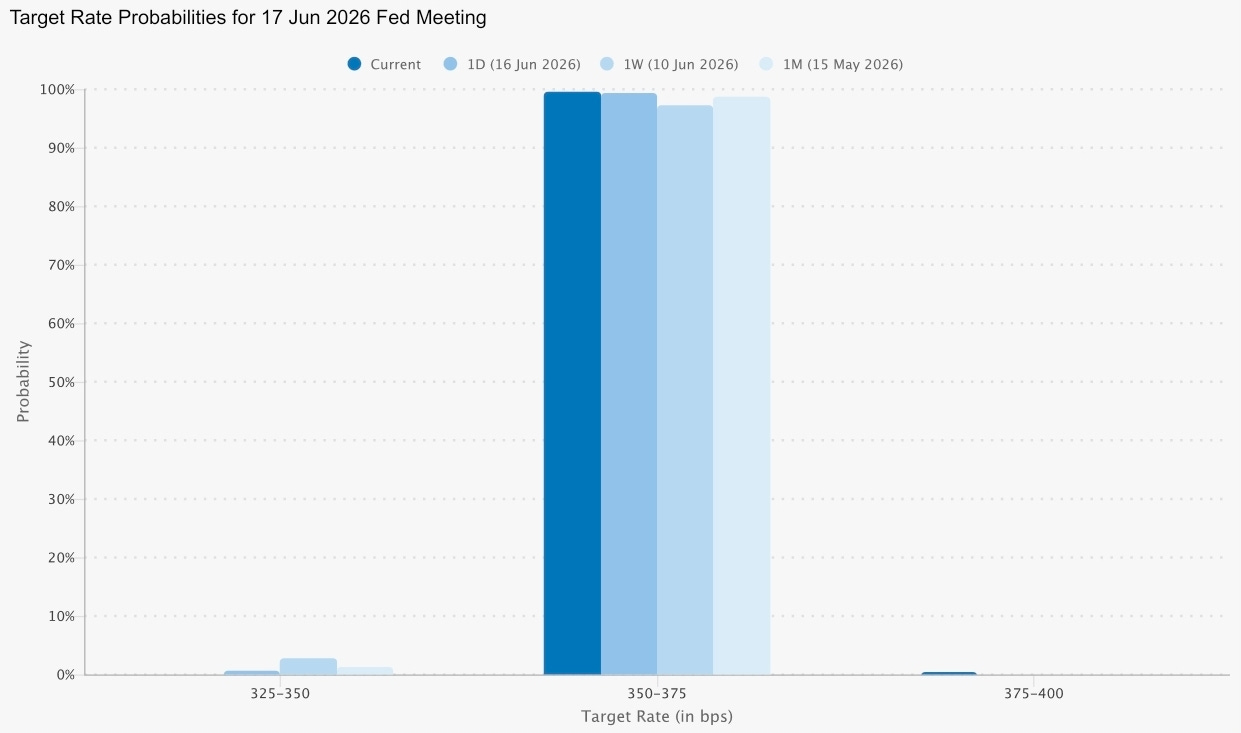

At first, the June announcement from the Federal Open Market Committee that there would be no change in the federal funds rate seemed right in line with Wall Street expectations.

The Committee decided to maintain the target range for the federal funds rate at 3-1/2 to 3-3/4 percent, in support of the Federal Reserve’s dual mandate. The Committee reaffirmed its policy of maintaining ample reserves in the banking system.

This was exactly what Wall Street had priced in weeks ago. On the rate announcement, Wall Street was not disappointed.

Then newly-minted Federal Reserve Chairman Kevin Warsh opened up his mouth, and it was that moment when the markets started heading south, dropping nearly 600 points over the course of the post-FOMC presser, a performance that surely had former Fed Chairman Jay “Too Little, Too Late” Powell downright jealous.

What did Kevin Warsh say that spooked the markets? Change. Kevin Warsh spoke of how he means to change how the Federal Reserve and the FOMC conduct monetary policy. The Kevin Warsh Federal Reserve will not be a continuation of the Jay Powell Federal Reserve.

That was enough to spook the markets and trigger a selloff in equities, while Treasury yields spiked.

Whisky Tango Foxtrot

Wall Street has for weeks presumed that the FOMC would stand pat on the federal funds rate, with CME Group’s FedWatch pricing tool putting the probability of no change very near 100%.

It is not hard to see the logic in this. With consumer price inflation heating up, and with producer prices signalling a few more months at least of higher inflation, traditional Fed thinking would lean towards either no change in the federal funds rate, or possibly a rate hike.

Blame Iran for closing the Strait of Hormuz. Blame President Trump for launching a war with Iran over their nuclear weapons program. Regardless of how one frames the oil price and supply shock emanating from the disruption of Persian Gulf oil flows, the reality remains the same: elevated energy price inflation, greater energy price volatility, and a finite capacity of leading industrial nations to buffer the shock with releases from strategic petroleum reserves.

All this has been known for some time, as has the Fed’s traditional policy playbook for such a scenario.

Yet the Fed caught Wall Street off guard even with the policy press release ahead of the post-FOMC press conference, as the first market hiccup of the day showed.

Wall Street’s comfort level with Kevin Warsh did not get any better during the press briefing itself, and by the end of the briefing the Dow had shed close to 600 points, with the S&P 500 and NASDAQ following close behind.

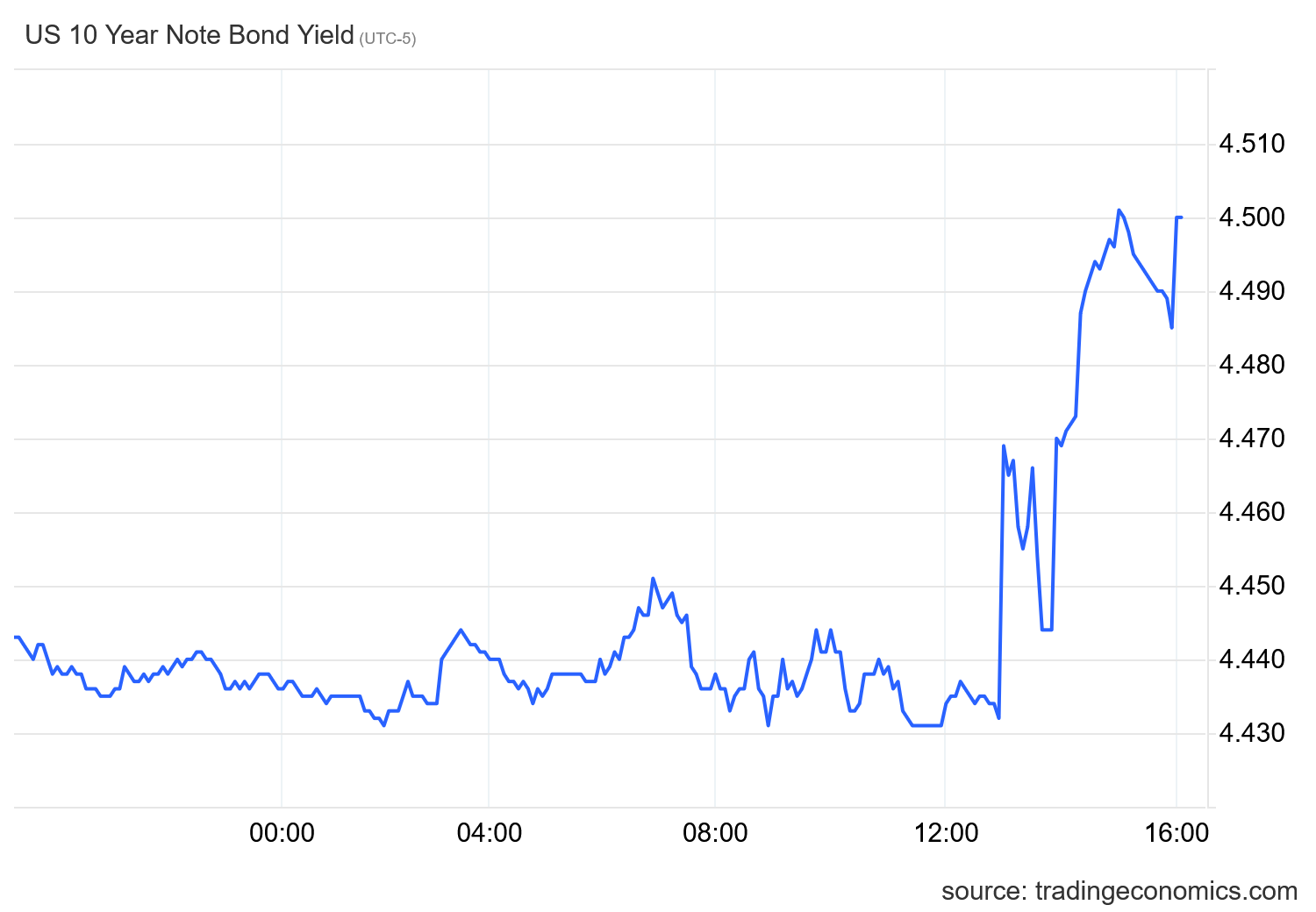

Treasury yields confirmed Wall Street’s shock and dismay, with the 10-Year Treasury jumping almost 10bps between the FOMC press release and the conclusion of the press briefing.

Even while meeting expectations on rates, the Kevin Warsh Federal Reserve succeeded in giving Wall Street a minor “Whisky Tango Foxtrot” moment.

What was the change that spooked Wall Street? While the rate decision was as expected, the tone of the announcement, as well as Warsh’s demeanor during the press conference, were noticeably different: more focused, more disciplined, and perhaps even more confident than had been the norm during Powell’s tenure as Fed Chair.

Less Fed Guidance, More Market Involvement

Warsh lost no time in signalling the start of a new era in Fed policy communications. The FOMC statement announcing the federal funds rate would remain unchanged was barely half a page.

April’s statement announcing the same policy decision was over a page in length.

Gone was the padding of reassurances that the FOMC really does mean to follow the data and get consumer price inflation down to 2% year on year. Gone was the fluff about what the data presumably showed.

What remained was a simple statement of the policy decision and a few perfunctory sentences on inflation and job growth.

When Warsh began the press briefing a short time later, he wasted no time before announcing significant changes in how the Federal Reserve and the FOMC intended to communicate monetary policy, beginning with how the FOMC rate announcement was likely to be different going forward.

My Fed colleagues and I will be working in close collaboration to ask what changes might improve the conduct of monetary policy.

On that score, you might have already noticed something, a difference in today’s policy statement. It’s a bit shorter, a bit simpler, and it dispenses with some older language. That statement just gives you the facts as best we can judge it. Absent also is so-called forward guidance which we agreed was not well suited to the current policy conjuncture.

This afternoon you also received the usual summary of economic projections. It’s been the practice of this committee for participants to submit these projections and I have encouraged my colleagues to continue to do so. I, however, have refrained from offering any projections of my own, consistent with my long-held views on the SEP, at least as currently structured.

Without missing a beat, Warsh went on to announce a set of task forces to overhaul Federal Reserve communications practices and data management.

I’m appointing a task force in each of five areas that are central to the broad conduct of monetary policy: First, Fed Communications; Second, the Fed’s balance sheet; Third, our use and reliance on existing data sources; Fourth, productivity and jobs in an era of transformation; And last, the Fed’s inflation frameworks.

These subjects are timely, consequential, and in my view worthy of a fresh look. My colleagues and I discussed them with energy and purpose over the last couple of days.

For each of these independent task forces, I’m enlisting some of the very best minds, both inside and outside the economics profession. They will be supported by subject matter specialists from our superb Fed staff.

And they’ll have a straightforward charge: Start with first principles. Ask hard questions. Examine current practice. Consider alternatives. and ultimately propose next steps for policymaker consideration.

With short, succinct sentences in a crisp staccato delivery, Kevin Warsh made it clear that the Fed was going to be handling its brief differently going forward.

Perhaps the most notable point Warsh made during the press briefing was in his rationale for doing away with the previous Fed practice of giving “forward guidance”—a sense of where the Fed anticipated monetary policy going next. Fundamentally, Warsh wants to see the markets playing a greater role in driving interest rates than Federal Reserve policy.

Edward Lawrence with Fox Business. So if you don’t give a lot of ongoing forward guidance, won’t the markets have more volatility and shouldn’t Americans have more access into what you’re thinking going forward?

Kevin Warsh: So I think financial markets perform best when they react to incoming data. I think the financial markets work less efficiently when they ask a question, how will the Federal Reserve react to that incoming information? The more that markets are paying attention to what’s happening in the real economy, deciding what’s good data and what’s less good data, the more financial markets can price what they believe is the most likely and what are the tail risks. Financial market prices are probably the most important source of information to guide central bankers.

But when all the financial markets are doing is reflecting back what we’ve said then we’re taking the most important source of information and we’re being blind to it. I’d like us to create a system where those blinders come off where markets are following data that they efficiently think is reliable and they’ll come with better information through market prices to us we can make more informed decisions with ultimately the goal that I set at the outset, deliver on the price stability objective that Congress told us to do and that we better get in the business of doing.

Without directly criticizing his predecessor, Warsh made it clear that the policy of the Federal Reserve telling Wall Street where interest rates were going to go had the unhelpful consequence of turning Wall Street into little more than a policy echo chamber, where Wall Street was merely sending back at the Fed the outcomes the Fed said were desired through its forward guidance on interest rates.

Warsh wants Wall Street to do its own research, look at its own data, and drive its own conclusions on interest rates. In the short term this may mean greater volatility for both Treasuries and equities, but the end result will be Wall Street giving the Federal Reserve higher quality information on which to base future interest rate decisions.

Warsh quite plainly means to turn Wall Street from a consumer of economic data into a source for the Fed of economic data.

A New Day Has Dawned

Whether Kevin Warsh will turn out to be a good Federal Reserve Chairman or a poor one is a question we will see answered only gradually over the course of the next several months. One part of that answer has already been given, however, and that is how he intends to change the status quo at the Fed.

Warsh undoubtedly appeased the more hawkish Fed watchers by not pushing to lower the federal funds rate, even though President Trump has been consistently vocal about the need for exactly that. He will no doubt go up in the estimation of some if, some time during the summer, the FOMC elects to raise the federal funds rate by 25bps-50bps.

Warsh clearly unnerved much of Wall Street with his remarks. Without regard to how much independence Warsh intends to have from President Trump, he made it clear he will also be independent from Congress and Wall Street. He will steer monetary policy where he thinks it should go, and that may not be where Trump, Congress, or Wall Street think it should go.

A new day has dawned at the Federal Reserve, or so Kevin Warsh wants people to believe. If Warsh accomplishes his vision the Fed will provide less data but hopefully more information using higher quality data.

Whether that ends well for the Federal Reserve’s dual mandate of price stability and full employment is another question we will see answered only gradually over the course of the next several months.

This much is certain: the Federal Reserve will not be as it was.

He didn’t lower the federal funds rate as Trump wanted. Peter, do you get the sense that he still will be acceptable enough for Trump to consider him on Trump’s “side”?