The March Jobs Numbers Will Push The Fed To Hike Rates Again...But Should They?

A Second Look At Employment Figures And The Federal Funds Rate Is Warranted

After a full year of raising the federal funds rate, Jay Powell finds himself in an awkward situation: It hasn’t gone as planned.

Inflation has not obediently returned to a low 2% year on year.

Labor markets have not softened sufficiently.

Even interest rates overall have been notoriously rebellious since last November.

In the wake of the March Employment Situation Summary, the prevailing sentiment on Wall Street is that the jobs numbers are going to pressure the FOMC to raise the federal funds rate yet again.

The Federal Reserve has raised interest rates aggressively over the last year in a bid to slow inflation and the labor market.

Its efforts are still not quite feeding through to the data. Friday's March jobs report is the latest case in point.

With Friday's data, the Fed is likely to raise rates by another 0.25% next month. The Fed's forecasts published in March suggest that would mark the end of rate hikes for the Fed.

From the first increase in the federal funds rate in March 2022, one expectation of the Federal Reserve is that hiring would slow, unemployment would rise, employment would fall, and this would bring down inflation.

This strategy hinges on an assumption that there is a correlation to be made between the federal funds rate and overall rates of employment—but is that really the case? As with all strategies in any field of endeavor, the Federal Reserve’s rate-hike strategy only makes sense if the variables the Fed is watching respond as expected to increases in the federal funds rate, the one rate the Fed controls directly. If the variables do not response as expected, the strategy makes no sense at all.

What does the data say about the Fed’s strategy? Nothing good.

First, an important clarification of terms: As the quoted news article above illustrates, the common argot used to describe the Fed’s strategy is that the Fed “raises rates”, or “raises interest rates”. However, a quick examination of interest rates in the US over the past year suffices to disabuse us of that notion. When we look at Treasury yields over the past year, we see that they have actually declined since November, despite three increases in the federal funds rate over that same time period.

Corporate yields have also trended down in the face of repeated federal funds rate hikes.

Even junk debt yields have not responded as expected to increases in the federal funds rate.

A quick look at mortgage interest rates shows that, since November, the only rate the Federal Reserve has succeeded in raising is the federal funds rate.

The narrative that the Federal Reserve is “raising interest rates” is demonstrably false. Raising interest rates broadly is unquestionably the Fed’s intention, but it has had zero luck since last November in actually getting interest rates to rise. The Fed is unequivocally not raising interest rates.

Accordingly, if the Federal Reserve is going to have any discernible impact on employment, we cannot look reliably for a mechanism of action that goes through any benchmark yield to exert influence on labor markets. Since the Federal Reserve is not raising anything but the federal funds rate, we must look for a correlation between the federal funds rate and employment levels if the Fed’s strategy is to withstand scrutiny.

Within the data maintained by the St. Louis Federal Reserve as part of its FRED economic research data base there are four baseline indicators of employment in the United States:

From the Establishment Survey portion of the Employee Situation Summary we have "All Employees, Total Nonfarm” and “All Employees, Total Private.”

From data analyzed and presented by ADP, we have their metric of “Total Nonfarm Private”

From the Household Survey portion of the Employee Situation Summary, we have the “Employment Level”

For simplicity, I am looking at whole year intervals, with the exception of the current rate hike period, which is ongoing.

We divide the ADP metric by 1,000 to get the numbers to display properly, as the ADP metric presents the data in increments of individual people, while the Establishment and Household Survey metrics present the data in increments of thousands of individual. The resultant chart for employment levels since 2020 looks like this.

As we might expect, each metric reports different employment totals for the US economy. However, if we index each metric to the start of the period under examination—in this case, January, 2020—we can see how the trends for each metric go, including if the changes in relative magnitudes are broadly similar. Looking at the data since 2020, we can see that such is in fact the case.

If we overlay the Effective Federal Funds rate data and scale it on the right-hand Y-axis, we can see how employment has changed while the federal funds rate has moved upward.

If we zoom in on just 2022 and 2023 to date, the chart looks like this:

Thus we can immediately see the Fed’s dilemma: As the federal funds rate has increased, so has employment. There is no inverse correlation that can be easily seen here—and a decrease in employment as the federal funds rate rises is an inverse correlation1 by definition.

Inverse correlation is the relationship between two variables that change in opposite directions.

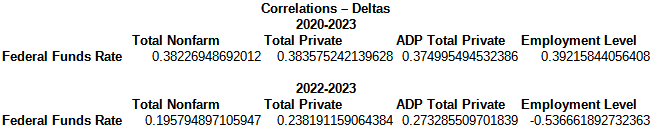

When we look at the correlation coefficients2, we see that the only inverse correlation is a somewhat weak relationship between the federal funds rate and the Employment Level from the Household Survey, and only when we look at the deltas, or changes, in the data from 2022 and 2023.

A case could be made that raising the federal funds rate has been a damper on growth in the Employment Level from the Household survey, but there is considerable room left for a variety of other forces to override the impact of changes to the federal funds rate. That the same inverse correlation is not seen for the other employment metrics also suggests that federal funds rate hikes have at most marginal restraining influences on labor growth.

For all other labor metrics, while the correlations are not strong, they also are not negative—there is no case whatsoever to be made that raising the federal funds rate has been a damper on any labor metric other than the Employment Level.

The statistical data confirms what we can see from direct inspection of the data—and what the corporate media has articulated as the Federal Reserve’s dilemma: raising the federal funds rate has not had appreciable impact on US labor markets.

Has it ever had appreciable impact? The data does not support that assumption either.

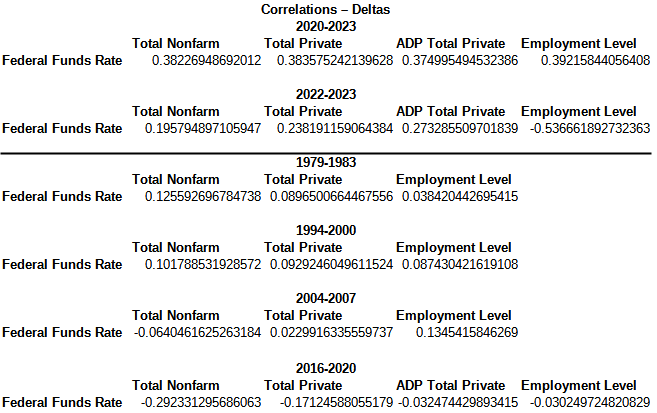

Including the current rate hike period, there have been five periods since the Volker Recession where the Federal Reserve has embarked on an extended strategy of raising the federal funds rate: 1979-1983, 1994-2000, 2004-2007, and 2016-2019.

As we have employment data for all of those periods as well as the federal funds rate, we can compare the behavior of the labor metrics from those periods to the changes in the federal funds rate to see if there is any negative correlation to be found.

When we look at the indices for the employment metrics from 1979-1983 vs the federal funds rate, there is no clear correlation (note: the ADP data only dates back to 2010, and so is only available for the 2016-2019 interval as well as the current interval). To the extent we can see any correlation, it appears to be positive all the way around.

Remember, we need to see a strong inverse correlation at some point to validate the Fed’s rate hike strategy as a means to curtail labor growth in the US. In 1979-1983 data extract, visually we cannot see such an inverse correlation.

In the 1994-2000 interval, the correlation is clearly positive.

It is clearly positive again in the 2004-2007 interval.

2016-2019 is a bit less clear—which while it doesn’t show emphatically that the correlation is positive or negative, it does illustrate that the correlation is not that strong, which leaves the door open for other influences to override changes to the federal funds rate.

In fact, when we calculate the correlation coefficients for all these intervals, we see that the 2016-2019 interval has a negative, or inverse, correlation for every labor metric, but is a weak correlation.

2004-2007 shows a weak negative correlation for the Total Nonfarm metric from the Establishment survey, but for every other data sampling, we have weak positive correlations between changes in the federal funds rate and changes to employment levels.

None of this lends any validation towards the Fed’s rate hike strategy as a means of curtailing employment in the US. Other economic forces have room to exert a far greater and even overriding influence on labor metrics in the United States.

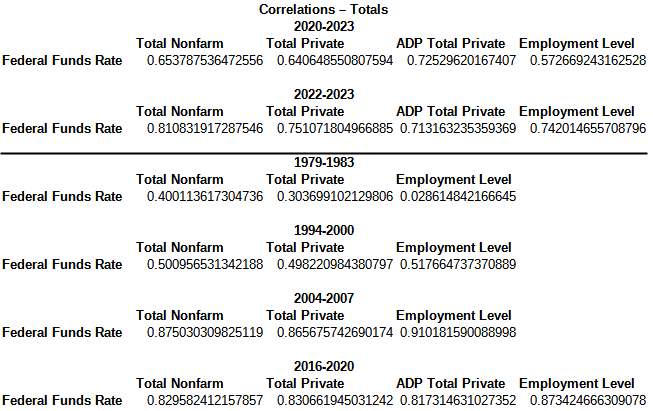

If we look at the correlations between employment levels and the federal funds rate itself during these same intervals, we see somewhat stronger positive correlations—but no inverse correlations.

Without inverse correlations, there can be no justification for presuming that raising the federal funds rate will restrain labor growth or reduce employment levels. Without inverse correlations, the strategy is indefensible on its face.

The historical data simply is not providing any support to the Federal Reserve’s rate hike strategy for restraining labor markets. Not only is the Fed’s rate hike strategy not raising interest rates, there is no historical basis to presume there is a reliable correlation between federal funds rate hikes and changes in the various measures of employment in the US. Raising interest rates cannot be said to reliably diminish labor growth or reduce employment levels. The requisite inverse correlations simply are not there. The one interval which is the exception to this the correlations are too weak to reliably produce the “cooling off” effect the Federal Reserve is seeking currently.

In theory, the Fed’s strategy is simple and straightforward: raise the federal funds rate, which pushes up interest rates overall, which constrains credit, consumer spending, and labor growth—and which will ultimately push the economy into recession, thereby bringing down consumer price inflation.

In reality, the Fed’s strategy has proven simply ineffective. Raising the federal funds rate is not pushing interest rates up and is not constraining labor growth, at least not at sufficient magnitude to produce the desired economic contraction. Whether raising the federal funds rate initially was the best strategy at the time is no longer relevant. What is relevant is that the continuation of the strategy is not producing the necessary effects, including a substantial decrease in inflation—each month, the decline in consumer price inflation has been marginal for the most part.

The Fed cannot reliably push interest rates up by raising the federal funds rate.

The Fed cannot reliably reduce employment or employment growth by raising the federal funds rate.

The Fed has not produced meaningful reductions in consumer price inflation by raising the federal funds rate.

At some point the Fed needs to admit the obvious: their chosen strategy, on which they have hung all their inflation-reducing hopes, is failing. A strategy which is not working is no strategy at all—and that’s what the Fed is giving us: no strategy at all.

The Investopedia Team. “Positive Correlation vs. Inverse Correlation: What’s the Difference?”, Investopedia. 4 Mar. 2022, https://www.investopedia.com/ask/answers/040915/what-difference-between-positive-correlation-and-inverse-correlation.asp.

Correlation coefficients were all calculated using the statistical functions of LibreOffice Calc 7.4.0.3 (x64).