Trump Gets Another Win — This One From The Job Market

Jobless Claims Numbers Surprise. Can The Good Times Last?

In a news week filled with tales of treason and Jeffrey Epstein, President Trump was able to collect a small but completely unrelated political victory. Thursday’s weekly unemployment claims report from the Department of Labor was not only good, it continued a trend of beating expectations.

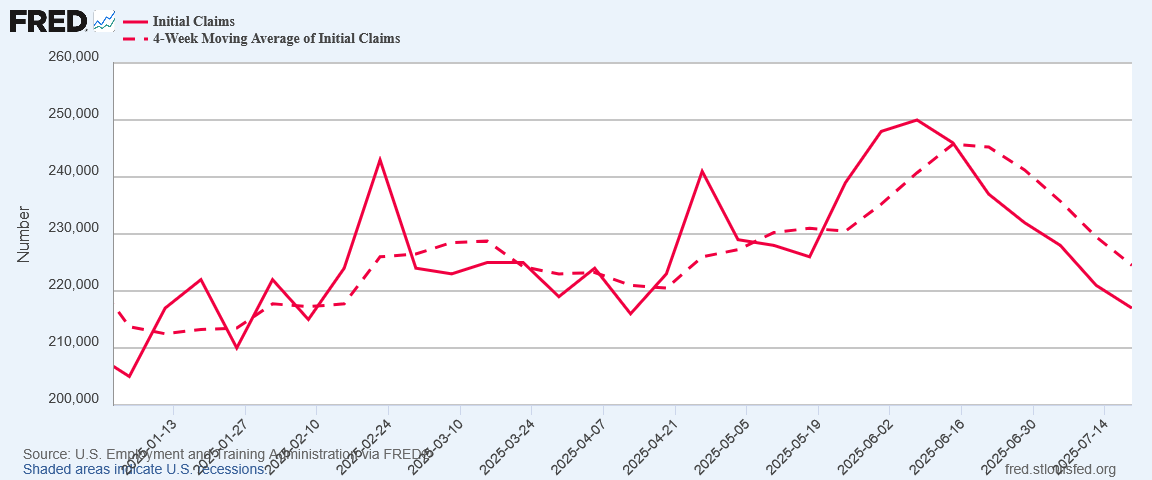

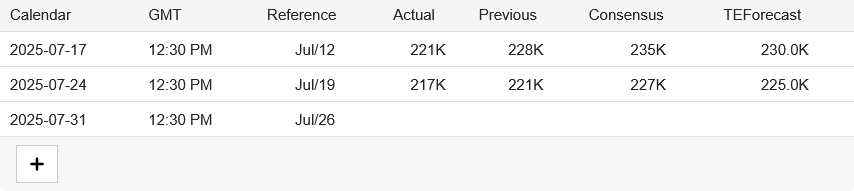

In the week ending July 19, the advance figure for seasonally adjusted initial claims was 217,000, a decrease of 4,000 from the previous week's unrevised level of 221,000. The 4-week moving average was 224,500, a decrease of 5,000 from the previous week's unrevised average of 229,500.

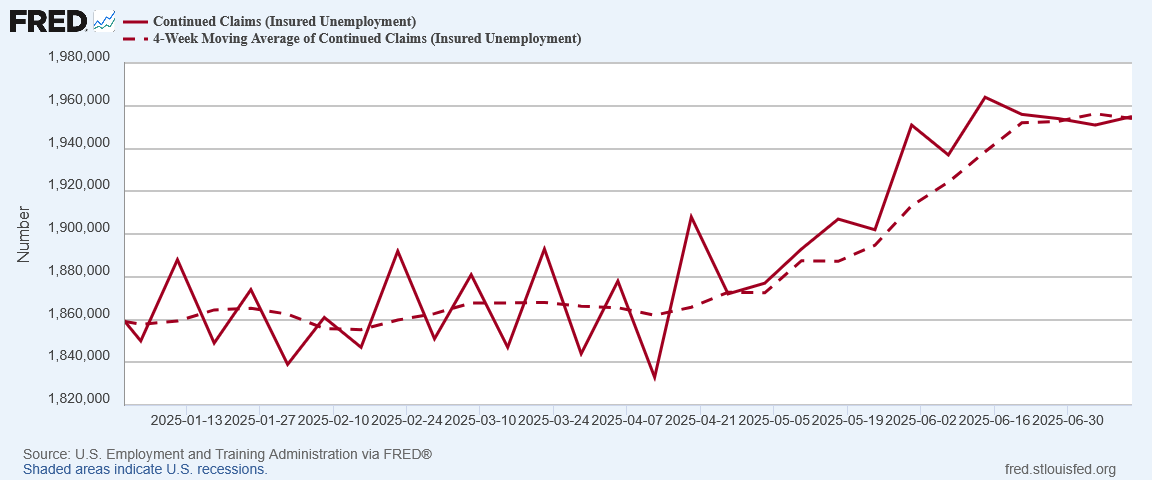

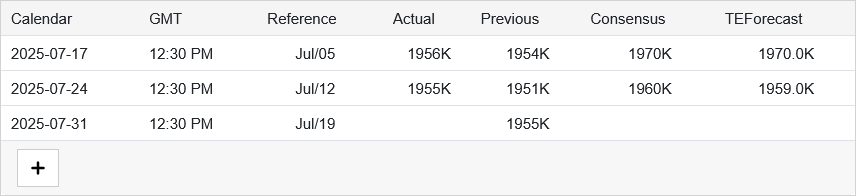

The advance seasonally adjusted insured unemployment rate was 1.3 percent for the week ending July 12, unchanged from the previous week's unrevised rate. The advance number for seasonally adjusted insured unemployment during the week ending July 12 was 1,955,000, an increase of 4,000 from the previous week's revised level. The previous week's level was revised down by 5,000 from 1,956,000 to 1,951,000. The 4-week moving average was 1,954,000, a decrease of 2,250 from the previous week's revised average. The previous week's average was revised down by 1,250 from 1,957,500 to 1,956,250.

There is no denying that this week’s unemployment claims data was a solid print, coming in ahead of expectations for at least the last six weeks in a row. It not only made for a Trump political win on the week, it was a clear economic win for US labor markets.

What made the numbers good?

For starters, the initial claims data charted its sixth straight week of decline, pushing initial claims to their lowest level in two months.

Additionally, not only did the number of initial claims continue to decline, they continued to beat market forecasts. As reported by Trading Economics, Wall Street projected initial claims at around 227,000, with the Trading Economics site itself forecasting 225,000.

At 217,000, the official claims number printed below forecasts by some 10,000 jobs.

The continuing claims data also turned in a nice set of numbers. While seasonally adjusted claims did rise, they did not rise so much as to prevent the 4-week moving average from printing a slight decline during the week.

As reported by Trading Economics, the continuing claims data also beat Wall Street’s expectations significantly.

Could the United States be about to finally break out of the jobs recession it has endured for nearly two years?

While that is certainly the hope, there are data points which remind us that it is still premature to claim “victory!” over the toxic US job markets.

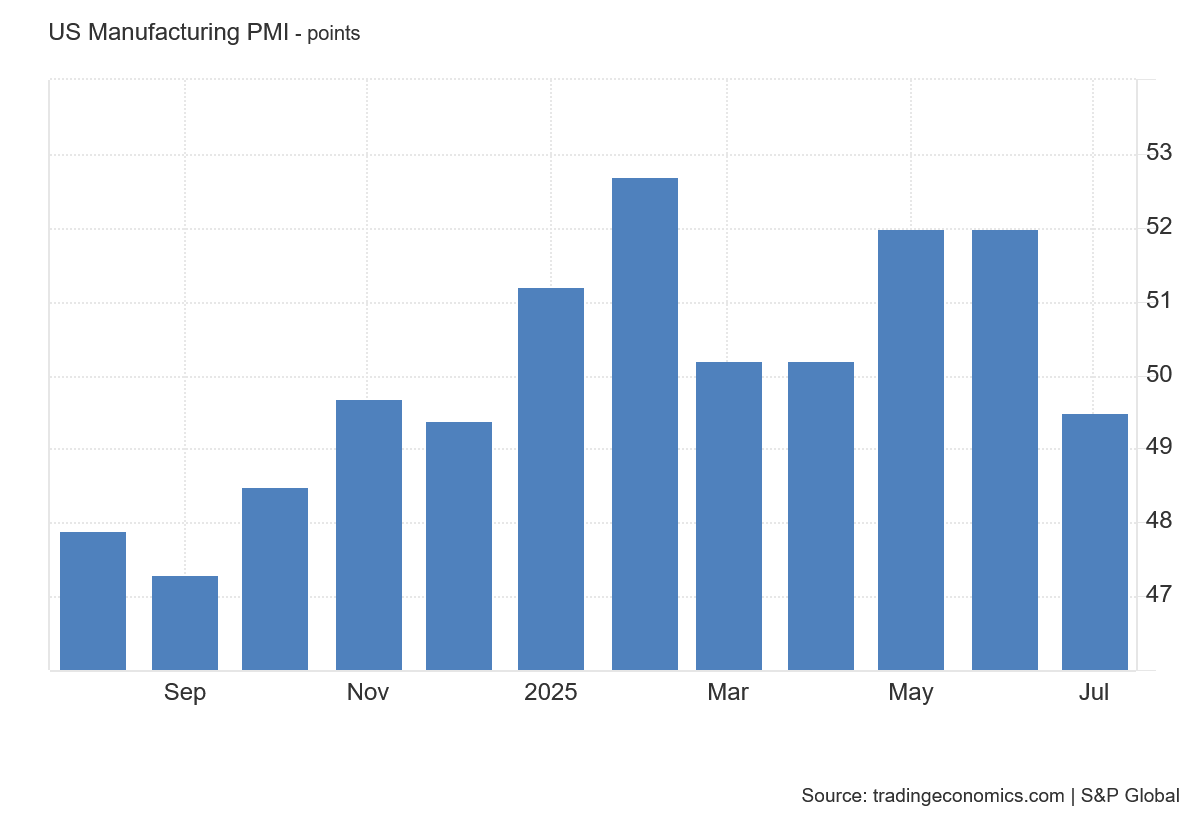

According to S&P Global’s July Manufacturing Purchasing Managers’ Index, manufacturing contracted significantly for the month.

At the same time, workers across several industries were informed they may soon be laid off.

Over the past several weeks, there have been 4,137 job cuts announced, according to media reports and Worker Adjustment and Retraining Notification (WARN) Act notices.

A contraction within manufacturing and notice of impending layoffs suggest that the weeks-long downward trend in initial claims may not last much longer.

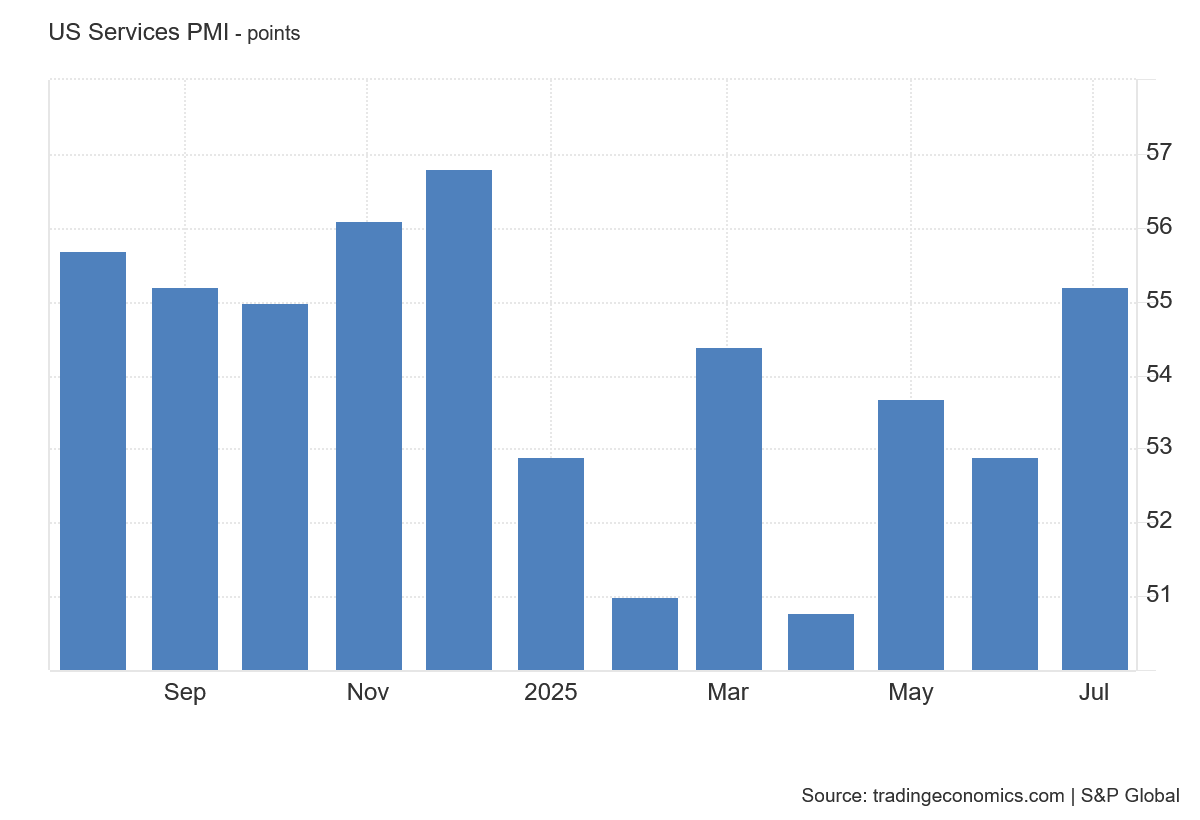

Despite the red flags surrounding manufacturing, S&P Global’s Services Purchasing Manager’s Index rose in July.

While the future for US labor markets remains eternally problematic, the positive unemployment claims data gives reason to hope that June’s Job Opening and Labor Turnover Summary (JOLTS), which is due out next Tuesday, might offer up some good employment news.

This week’s unemployment numbers are good, and while there is reason to suspect the numbers will not remain good, we still do well to acknowledge the good data while it lasts.

If the trends in initial jobless claims continue, we may yet break out of the “jobs recession”. We are not there yet, but job markets took a small step in that direction this past week—and that’s a good thing.

We will have a much better insight in to the numbers when employment by industry segment numbers are posted.

I suspect construction employment will increase. Summer's here, outdoor site work is ramping up in the northern 1/2 of the country. Also, owners may want to complete work before prices increase due to inflationary pressures, real or percieved.

I’m thinking there will be a few trends in the coming months:

Manufacturing jobs will continue to decline, because of lingering effects from the Biden administration, until - several months, or a year-plus from now - they start to increase, as tariffs drive jobs creation to the U.S.;

The jobs situation overall will continue to improve, as ICE and self-deportations lead to more openings for workers and increased wages;

The new AI industries - IF they pan out anywhere close to the hype - lead to an economic boom similar to the one in the 1990s after the invention of the World Wide Web.

BUT all of this could fizzle if Trump’s plans are sabotaged, or a new major crisis (WW3, the San Andreas fault line cracking in a 9.3 earthquake, etc.) upends everything. Most worrying to me is this new, delusional mindset of young Democratic Socialists in the governing bodies of our cities. Their deranged laws and ordinances could undermine every economic plan of the Trump administration, and are a real threat to civilization!

So the future picture is still up in the air - as always. It’s wonderful to have your factual analysis, Peter, to give us first glimpses and understandings. Thank you!