Another month has come and gone, yet inflation not only lingers, but is trending ever higher.

The highlight of the July Personal Income and Outlays Report shows core inflation per the PCEPI increasing for the fourth straight month, even as headline inflation cooled significantly on the month.

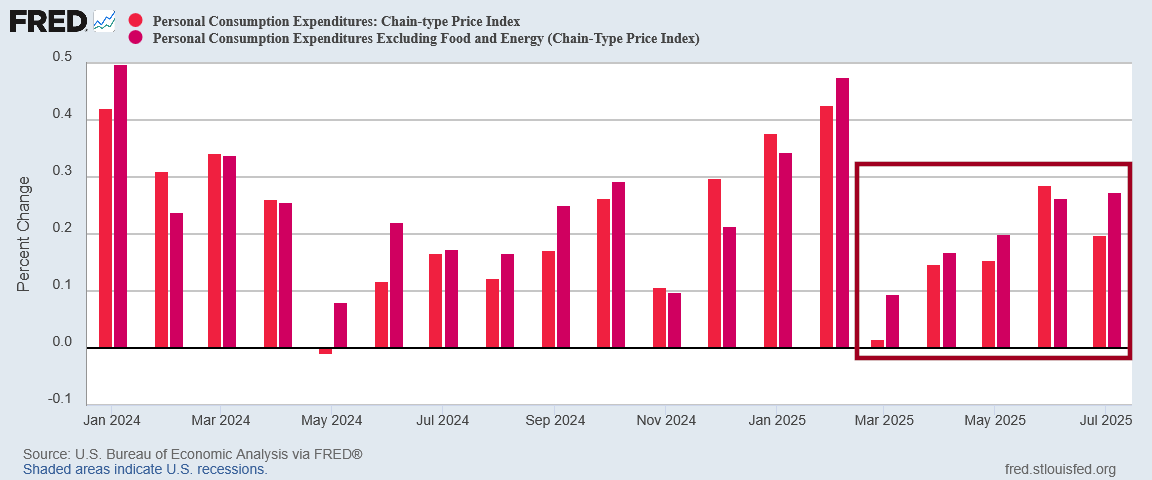

From the preceding month, the PCE price index for July increased 0.2 percent. Excluding food and energy, the PCE price index increased 0.3 percent.

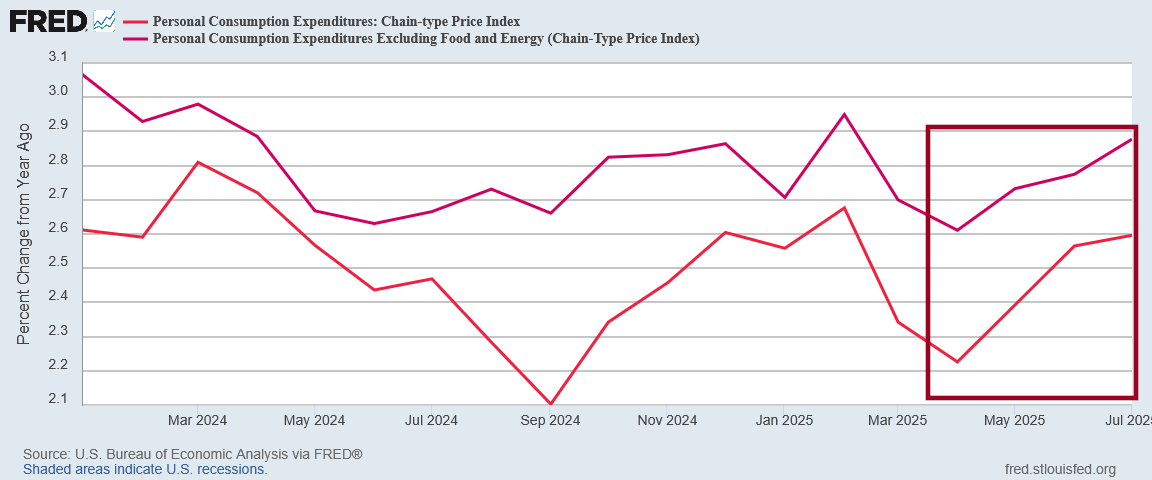

From the same month one year ago, the PCE price index for July increased 2.6 percent. Excluding food and energy, the PCE price index increased 2.9 percent from one year ago.

There is no disputing this inflationary trend: consumer price inflation is rising in this country, and it has been rising throughout President Trump’s nascent second term.

That is not good news for Donald Trump. Rising consumer inflation is certainly not good news for American consumers.

Yet the nature of the rise in consumer price inflation is also not good news for the Federal Reserve, as once again the inflation data refuses to validate Jay Powell’s stubbornly held thesis that President Trump’s tariffs would generate significant inflation—a thesis Powell continues to grasp tightly, as demonstrated by his remarks last week at the Fed's Jackson Hole gathering.

In what has become a perverse trend in recent inflation reports, the July PCE price data is not good news, but is also not disastrously bad news. The growth in consumer price inflation is noticeable, but not so noticeable as to touch off major alarms either on Wall Street or on Washington DC.

However, the July PCE price data is just bad enough to raise an even worse specter than inflation: stagflation—when inflationary forces and deflationary forces collide in a painful and prolonged fashion.

The July Personal Income and Outlays Report is once again a report that neither benefits nor satisfies anyone.

As the PCE data is compiled by the Bureau of Economic Analysis, it stands as an independent data set from the Bureau of Labor Statistics’ Consumer Price Index data. While the specific year on year and month on month inflation rates differ, both data sets show the same trends for 2025.

CPI Inflation Rates

There is no economic scenario where rising consumer prices are good for consumers. There is no economic scenario, therefore, where rising consumer prices are good for Americans. This is well understood, and is why rising inflation reports generally get a negative reception in the corporate media.

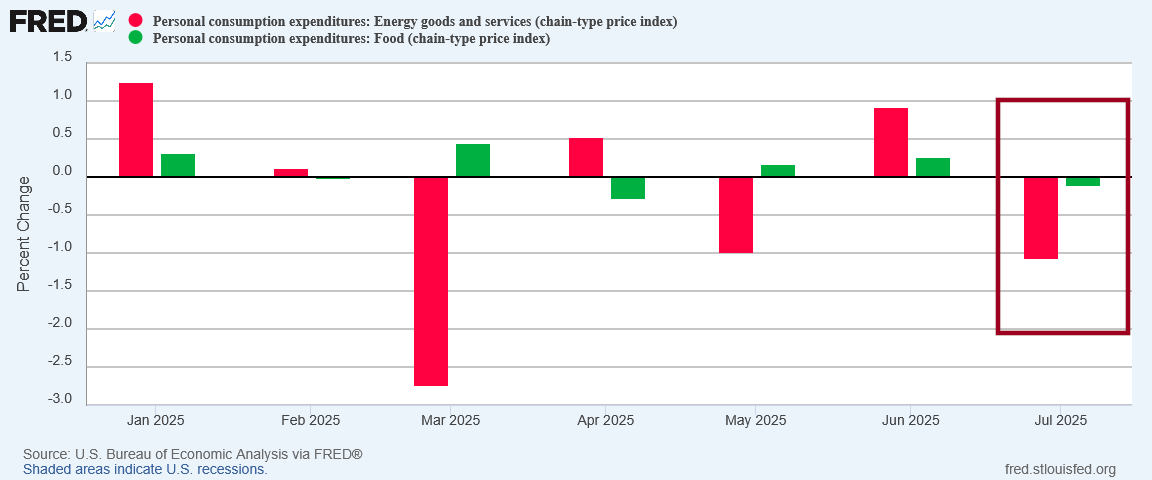

There were a few optimistic details, however. Energy and food prices—the differentiators between headline and core inflation—both declined month on month in July.

These areas of falling prices, however, were not enough to cool down core inflation, which was hot enough that energy and food price deflation had merely an incremental cooling influence on headline inflation.

While not good news, the inflation data was expected news, with the year on year inflation rate landing where Trading Economics reported both the Wall Street consensus projection for July and their own internal forecast.

Inflation is rising. Wall Street knows it. The Federal Reserve knows it. The BEA and the BLS know it. Main Street knows it.

The longer this trend continues the more of a problem it will become for everyone, We are still very far from the hyperinflation of 2022, but we are getting incrementally closer. That is a disturbing trend indeed.

Turning to inflation, higher tariffs have begun to push up prices in some categories of goods. Estimates based on the latest available data indicate that total PCE prices rose 2.6 percent over the 12 months ending in July. Excluding the volatile food and energy categories, core PCE prices rose 2.9 percent, above their level a year ago. Within core, prices of goods increased 1.1 percent over the past 12 months, a notable shift from the modest decline seen over the course of 2024.

Powell presents the claim of tariffs pushing up prices as a factual statement, but even a cursory reading of his statement shows that he is committing the classical logical fallacy post hoc ergo propter hoc (“after this, therefore because of this”). One inference one can draw from Powell’s statement is that there are no other catalysts which might be driving prices up. Only Trump’s tariffs will serve as an explanation for price increases.

Trump Derangement Syndrome has apparently been elevated to the status of mainstream economic theory.

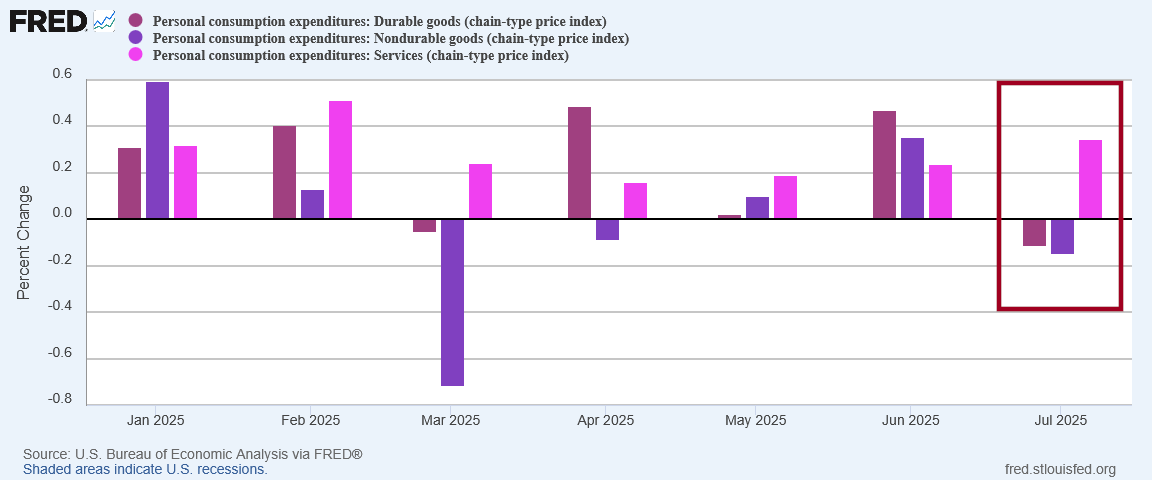

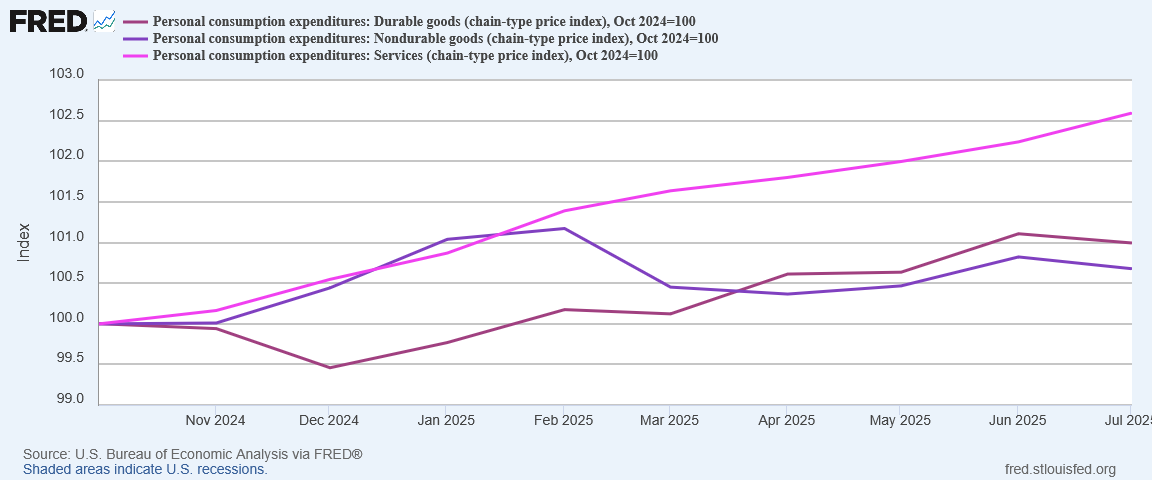

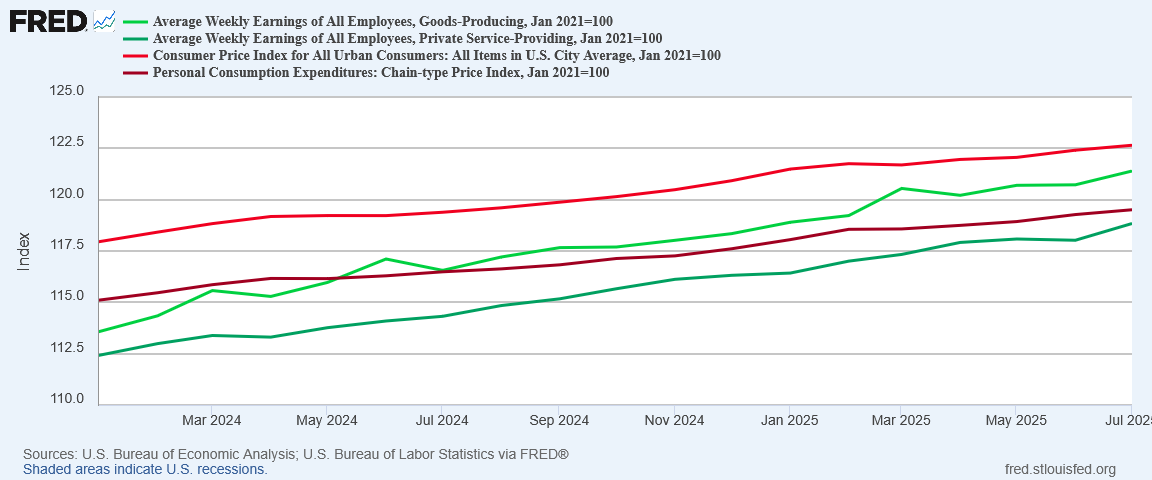

If tariffs are applied to goods and not services, they are a direct inflationary pressure on goods and not on services. We should expect to see a greater inflationary pressure on goods prices, yet since Donald Trump was elected last November, the greatest inflationary pressures have consistently been on services.

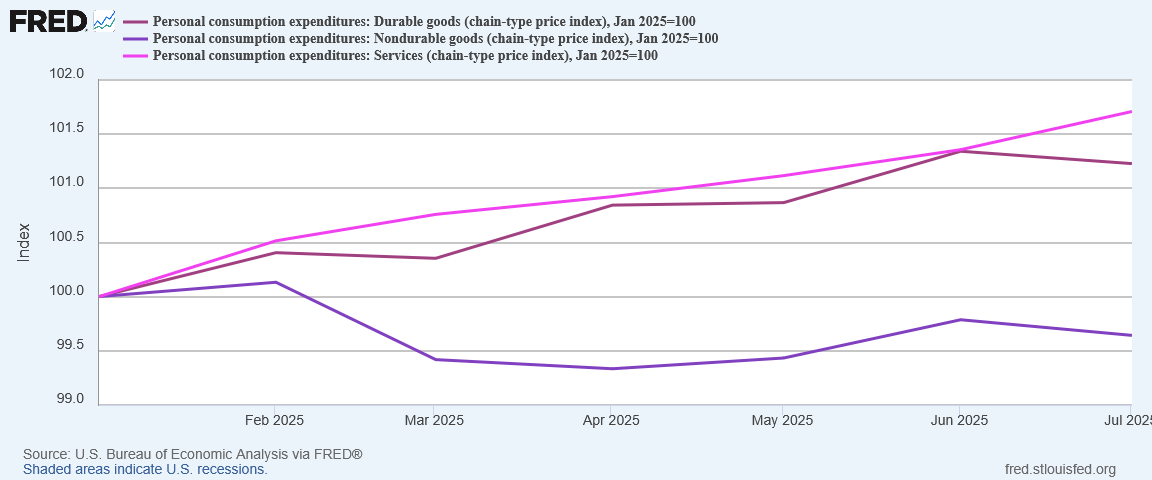

If we shift our referential time frame to when Donald Trump became President (i.e., January of this year), the inflationary pressure is still greatest on services.

This is the exact opposite of the price trend we should expect to see if tariffs are a primary culprit in consumer price inflation.

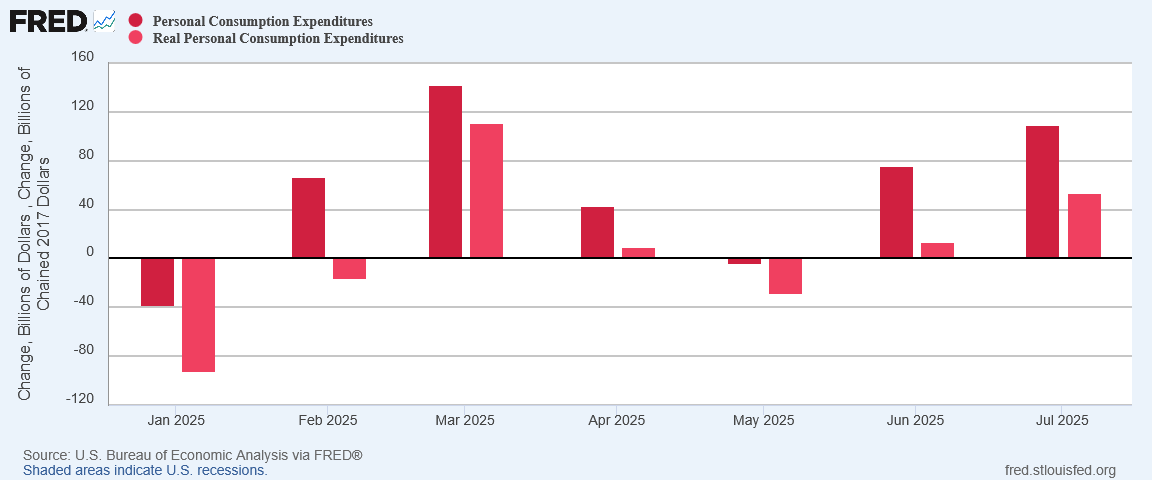

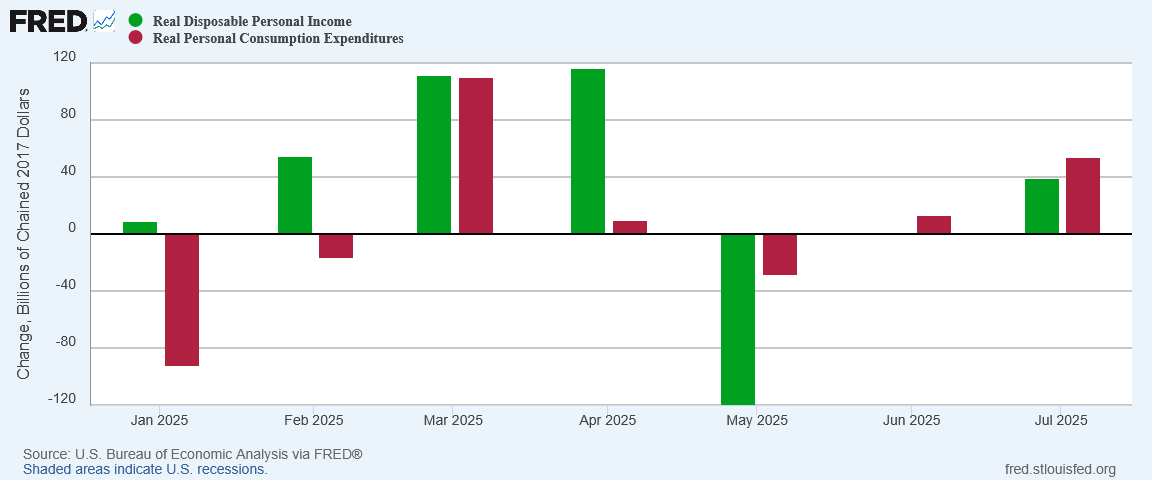

The argument that tariffs are responsible for recent price increases is further undermined by the reality that personal consumption expenditures (both nominal and real) have been rising during the same months that we have seen month on month consumer price inflation rising.

Increased spending in both nominal and real terms means demand has increased—if the nominal spending were solely due to inflation real spending would not increase, and might even decrease. Whenever there is rising demand for goods and services, prices for those goods and services is also going to rise. That much is economics 101.

People are clearly buying more, and not simply because they have more money to spend. Whenever people are buying more, that increased consumption is inherently the most probable primary catalyst for increased prices.

With a number of tariffs having been announced against a number of commodities such as copper, if tariffs were pushing prices higher we should be seeing a steady rising in commodity prices overall. We are not.

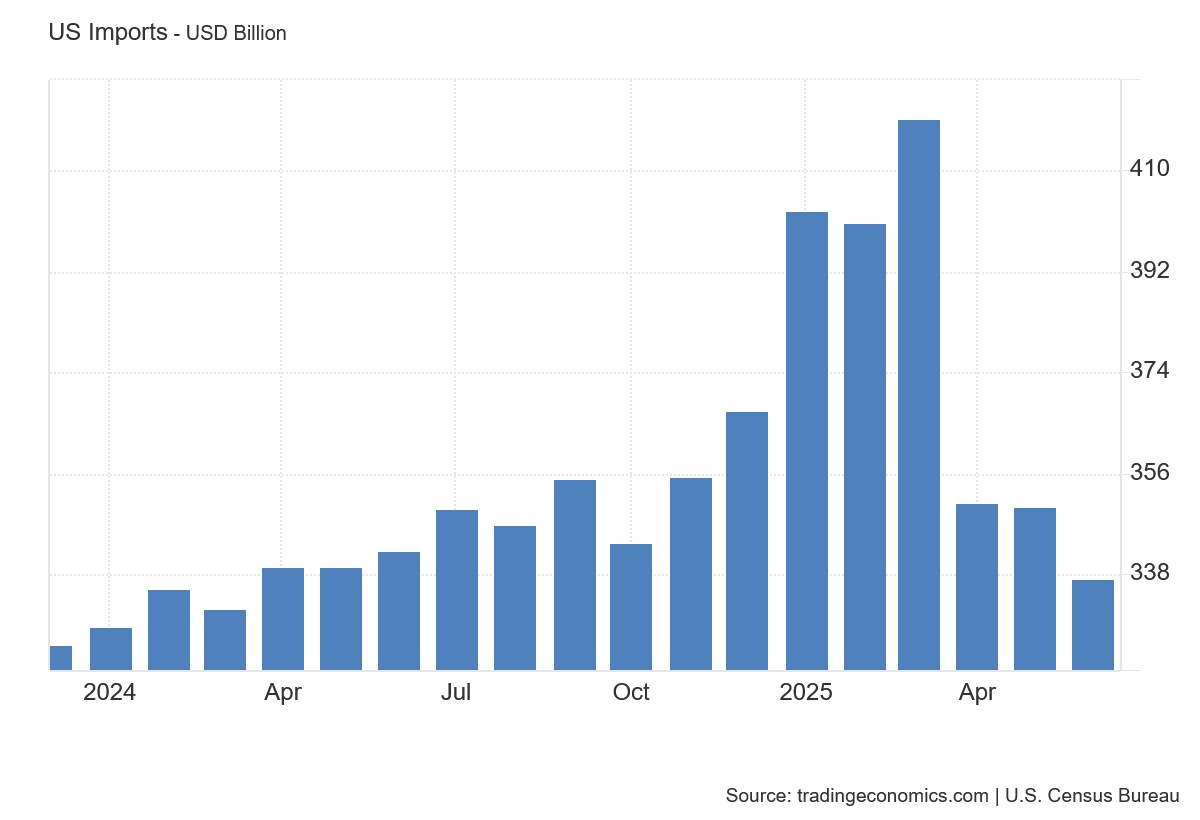

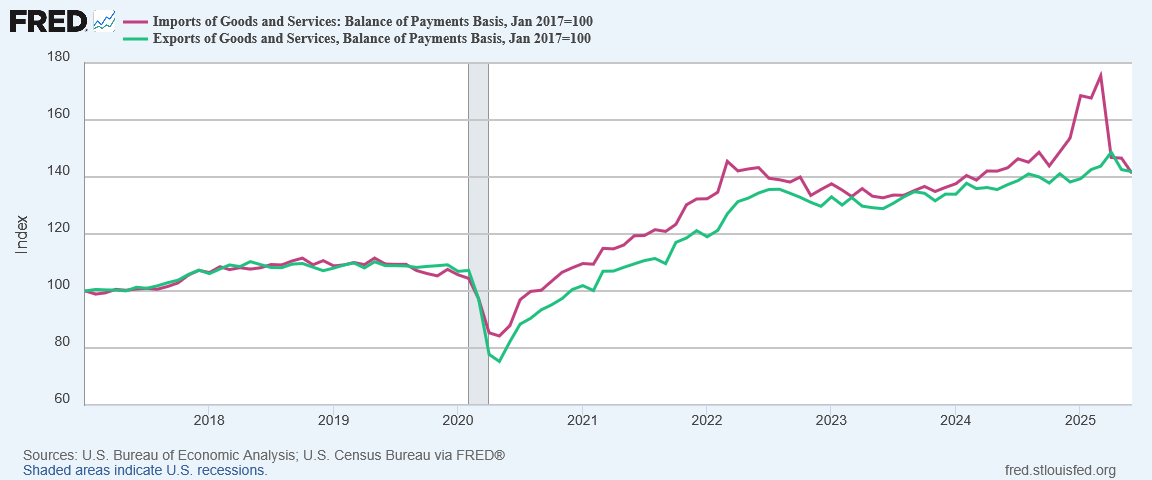

Jay Powell is arguably correct that President Trump’s tariff and trade agenda is having a transformative effect on global trade. The anticipation of the Liberation Day tariffs and their announcement arguably produced a “front-loading” phenomenon among imports, where US distributors and resellers accelerated import purchases they would otherwise space out across the year in order to avoid potential price hikes due to tariffs.

This front-loading phenomenon does not represent an increase in aggregate demand, however. Instead, overall demand for the year is simply shifted forward in time. Thus the surge in imports during the first quarter of the year is followed by a sharp drop in imports during the second.

However, the lack of significant consumer price inflation throughout the surge and the slump further discredits tariffs as a source of inflation. If tariffs were pushing prices up, we should have seen inflation far sooner than we have.

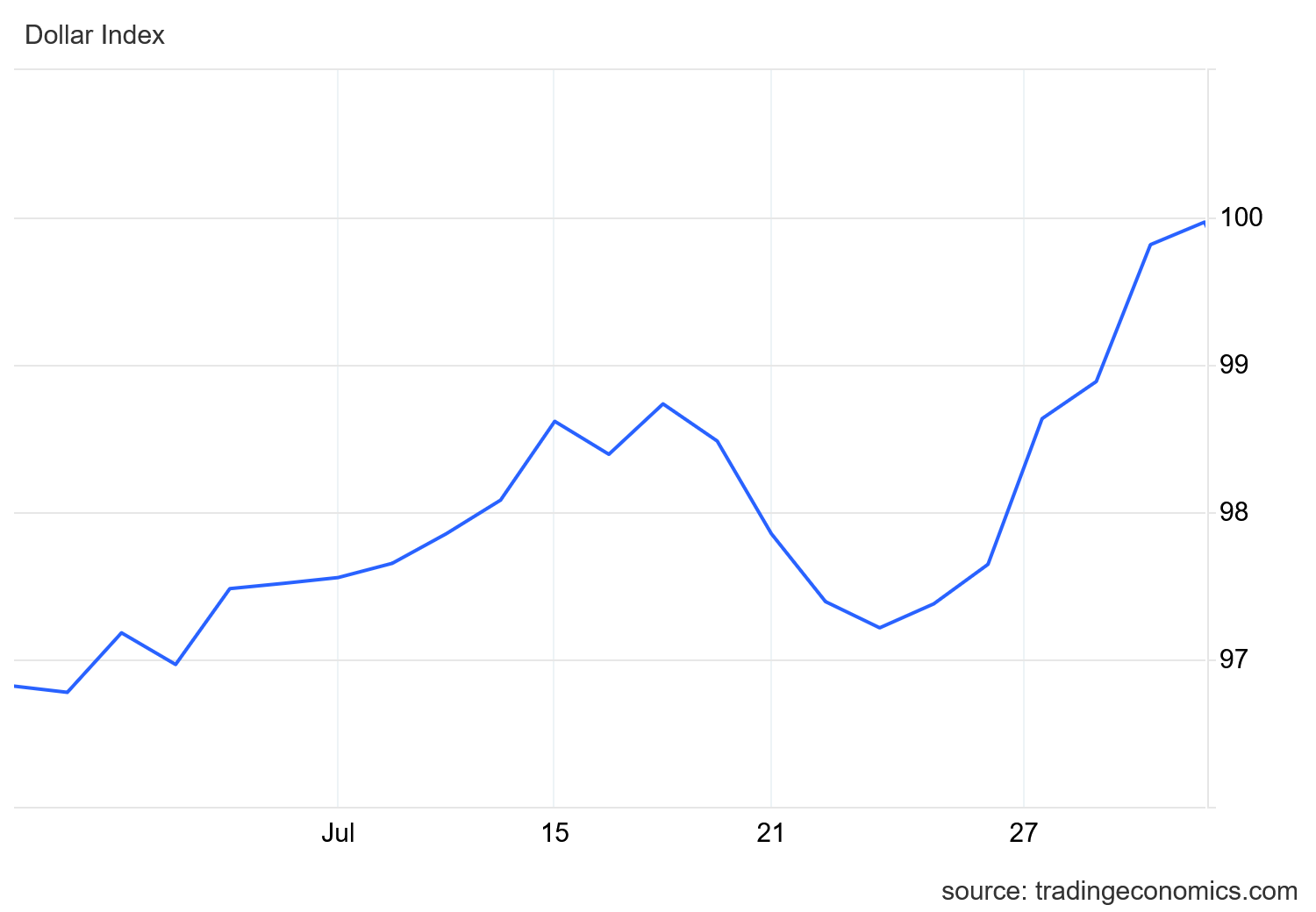

If tariffs were making US import markets less attractive globally, the dollar should not have strengthened during July—yet it did.

A strengthening dollar at a time of rising inflation is plausible when the inflation is driven by increased consumption—which we clearly have in the US economy.

At best, the PCE inflation data presents a mixed and even muddled view.

While the import surge in the first quarter has subsided and perhaps even produced a bit of an import slump, the longer-term trend for imports is still up. More intriguingly, however, is that President Trump once again has managed to grow US exports more than US imports, just as happened briefly during his first term of office.

While the inflation data does not lend itself very well to “gloom and doom” posturing on the state of the economy, it certainly does not portray an economy entering a “Golden Age” as President Trump has stated so many times.

Viewed in the context of other economic data, particularly jobs data, the inflation data suggests growing weakness in the US economy. While Trump’s tariffs and trade wars have not resulted in the high levels of inflation that have been so wrongly forecast by Wall Street and the Federal Reserve since before Trump took office, neither have they spurred sufficient domestic job growth and business growth to end the “jobs recession” that has been lingering in this country since 2023.

Moreover, if inflation continues to rise along with joblessness, we may be entering a period where “stagflation” becomes a disturbingly relevant consideration.

The lingering weaknesses in labor markets puts the Federal Reserve especially on the horns of a dilemma. On the one hand, the Fed’s TDS-infected insistence that Trump’s tariffs are producing inflation is a reason to keep the federal funds rate high. On the other, weak job gains undercuts the Fed’s claim that the economy is at full employment (it’s not).

That dilemma is not made any easier for the Fed by the latest PCE data. Despite the Fed’s insistence that recent inflation rises are due to Trump’s tariffs, the data simply does not bear that out. Either Jay Powell is not looking at the data, does not understand the data, or is simply lying whenever he opens his mouth (or all of the above).

Based on Powell’s Jackson Hole address, he has not yet figured out what to do to resolve both rising inflation and rising joblessness. He may not fully comprehend what is happening with either one. With the next FOMC meeting coming up in just over two weeks, he is running out of time to decide if he can stomach yielding to President Trump by trimming the federal funds rate.

The inflation data is clear on this much: this has not been a good summer for the US economy. Barring a significant shift in underlying dynamics, the US economy is not shaping up to have a very good fall and winter either.

President Trump wants everyone to believe that the US economy is healthy and getting healthier. The reality is more in the opposite vein, of an economy that sick and getting sicker.

That is not an economic message anyone wants to take away from the Personal Income and Outlays report. That’s not a message President Trump will like. That’s not a message Wall Street will like. That’s not a message Jay Powell will like. That’s not a message Main Street will like.

It is the message the report has to deliver. The US economy is not healthy. It is hurting, and it is likely to continue to hurt for a while yet.

Thank you once again for factual data and sound analysis, Peter. Apparently, this latest info will only serve to make Americans less trusting of anyone’s narrative. Maybe it will also cause people to turn their attention to other matters, because it’s “meh”. In the largest picture, do you see anything looming on the immediate horizon - such as China’s economic problems, or Europe’s - that could soon push us into a sharp economic turn?

Thank you once again for factual data and sound analysis, Peter. Apparently, this latest info will only serve to make Americans less trusting of anyone’s narrative. Maybe it will also cause people to turn their attention to other matters, because it’s “meh”. In the largest picture, do you see anything looming on the immediate horizon - such as China’s economic problems, or Europe’s - that could soon push us into a sharp economic turn?

Everything is definitely more expensive every time I get out.....