Between Jay Powell promising pain and suffering for the US economy and Xi Jinping unable to stave off pain and suffering for the Chinese economy, the other day we get this little tidbit from Russia: Vladimir Putin has ordered the Russian military be expanded by 137,000, to 1.15 million men.

President Vladimir Putin ordered the expansion of the Russian military Thursday as Moscow struggles to fulfill its objectives in Ukraine six months after the invasion of its pro-Western neighbor.

As part of the changes, the total number of military and civilian staff in the Russian Armed Forces will increase from 1.9 million to nearly 2.04 million.

The increase will only come from adding new soldiers — not new civilian employees — meaning that the total number of soldiers will rise by 137,000 to 1.15 million.

This expansion is of course noteworthy because of Russia’s ongoing war with Ukraine. While many will look at this expansion as a commentary on how well that war is going (or not going) for Russia, my own intrigue stems from the economic ramifications: Bolstering the military by 137,000 troops is not a small increase in military—and therefore government—spending.

How well positioned is Russia’s economy to support a larger military? After 6 months of war and sanctions, how easy will it be for Russia to pay for these additional troops?

Given the disruptions the Russo-Ukrainian War has caused and continues to cause worldwide, a fresh examination of the data1 coming out of Russia is in order.

Russia’s Stock Market Has Not Prospered Since The War Began

While Russia has not collapsed the way sanctions advocates might have hoped at the outset of the war, it would be quite the exaggeration to suggest that Russia has prospered since invading Ukraine. Certainly, the Russian stock market, the MOEX, has languished in the doldrums since the invasion, after first crashing from record heights.

The market’s rise has been completely derailed, as the clear upward trend before the invasion of Ukraine has been supplanted by a downward trend, indicating a stagnant-to-contracting domestic stock market.

More significantly, Russia’s energy companies have not enjoyed good outcomes for their stocks. Gazprom, for example, has seen its stock drop in value to a level below where it was throughout all of 2022.

In particular, Gazprom stock has not recovered following a June crash in value after the company canceled its quarterly dividend. Rosneft and Lukoil have likewise suffered extreme drops in market value since the start of the war and have yet to recover.

Given that Russia has often been described as an “energy superpower”, such lackluster market performances by its leading energy companies can hardly be seen as a sign of robust economic health.

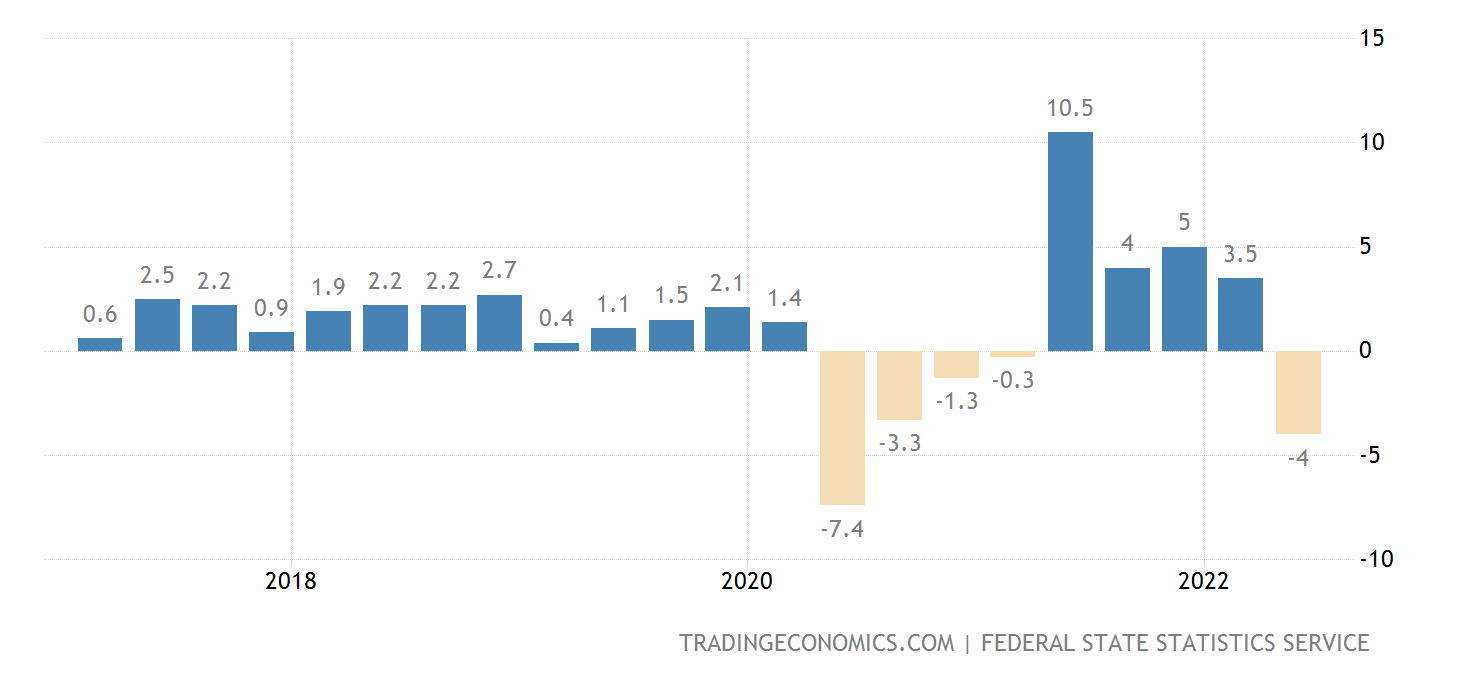

GDP Shed 4% Last Quarter

After expanding 3.5% in the first quarter of 2022, in the second quarter Russia’s economy shrank at a 4% annualized rate.

That drop is rather surprising given that Russia’s manufacturing sector has largely avoided contraction in recent months.

Paradoxically, Russian industrial production has declined in recent months, although that trend did ease significantly in July.

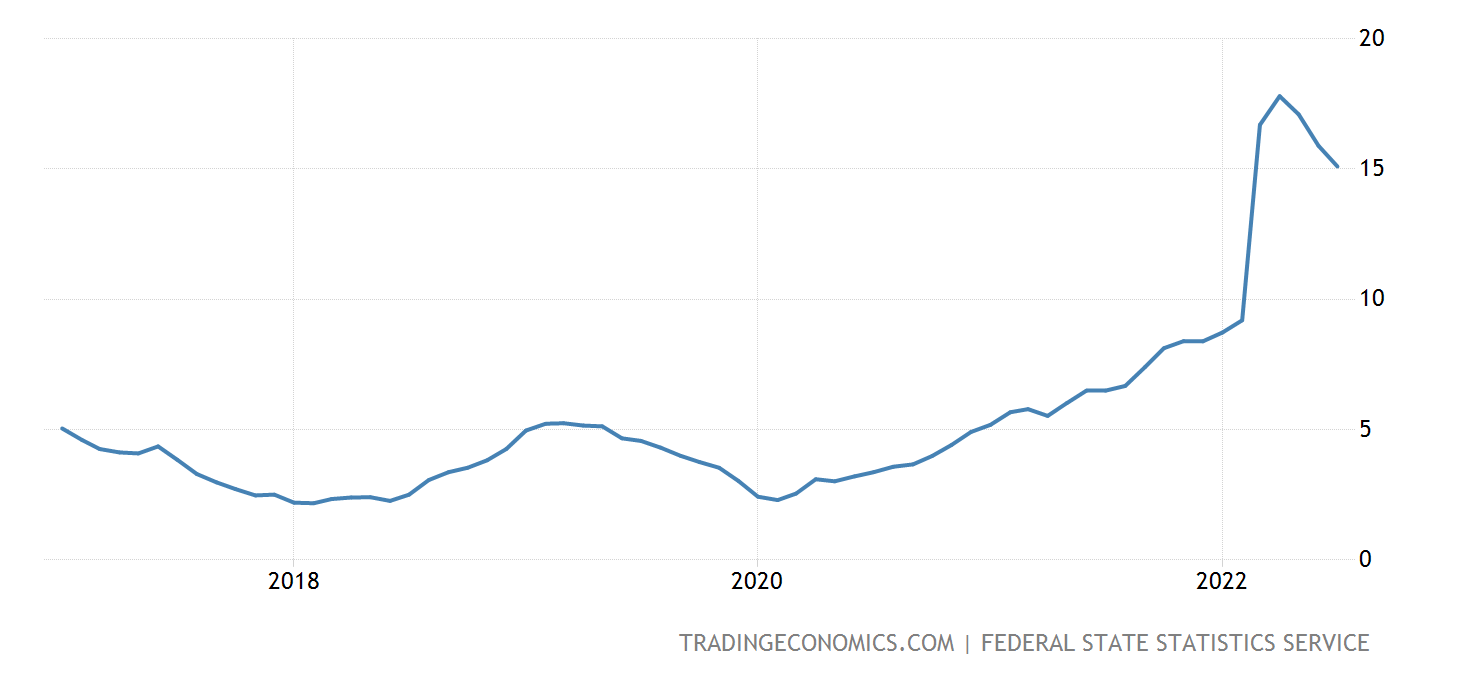

The economic contraction may have been a driving factor behind its decision to cut interest rates to 8%.

This despite persistently high inflation of over 15%—which, while not economically healthy, is still a decline from April’s peak inflation of approximately 18%.

Retail Sales Have Declined

Nor has the Russian consumer been a font of economic energy of late. While retail sales in July improved over June by 1.1%, they were still down year-on-year by 9.6%, the third consecutive month retail sales declined by ~10%.

No doubt the decline in sales is due in large part to declining real wages in Russia, which fell 6.1% year-on-year in May, after posting a similar decline in April.

Not Signs Of An Healthy Economy

None of these indicators portray the Russian economy as the picture of economic health. Whether due to the numerous sanctions imposed on Russia as a result of its war with Ukraine or other forces beyond that war, Russia is ailing.

Russia’s economic woes stand as a crucial indicator of the global nature of the economic recession unfolding around us. No nation is immune from its effects—not even one as well endowed with natural resources as Russia is. Despite Russia having an abundance of mineral wealth to sell to the world, the world is increasingly not in a position to buy, as inflation, ruptured supply chains, drought, and the lingering aftereffects of the serial lunacies of Pandemic Panic over COVID-19 wreak havoc on economies worldwide.

While many economic prognosticators—the “gold bugs” in particular, who see in every shift in the world’s fortunes a fresh opportunity for the precious metal—forecast a shift in economic power away from the West towards a more multi-polar economic regime, the more accurate depiction of the current situation is less a dispersion and more a disappearance of economic energy. America’s economic engine is failing, but so is China’s, so is Europe’s, and so is Russia’s. Economies everywhere are heading into leaner times, and while the likes of Jay Powell may pompously guarantee pain and suffering for the US, similar and even worse privation is spreading around the globe.

Chaos is not merely “coming” to the world. Particularly as regards the world economy, chaos is already here, and is going to stay for quite some time yet.

The economic data is drawn from the economic website Trading Economics, which in turn references Russian sources such as Russia’s Federal State Statistics Service (Rosstat). Direct access to Russian data sources has become problematic in recent months, potentially due to the war.

Considering the level of sanctions that have been imposed, it seems to me that Russia's economy is doing pretty well. I figure this winter, Russia will be one of the few places in the northern hemisphere where people won't be wondering if they can afford to heat their homes and businesses. :)