April Jobs Report: War Did Not Stop Hiring But....

Stagflation Is (Almost Certainly) Coming

On the surface, the April Employment Situation Summary appears to confirm what the March report, the March JOLTS report, and the April ADP Employment Report all assert: that hiring is on the upswing and the jobs recession is ending.

Total nonfarm payroll employment edged up by 115,000 in April, and the unemployment rate was unchanged at 4.3 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in health care, transportation and warehousing, and retail trade. Federal government employment continued to decline.

That figure was certainly a surprise to Wall Street, which had a much more conservative projection prior to the report’s release.

Yet on closer examination, the jobs report still carried distressing signals that all is still not well with US job markets.

Joblessness still rose, and the number of people no longer in the labor force still rose. That’s not a good sign.

Key sectors still experienced a drop in employment. That’s not a good sign.

Wages rose, but, in light of the March price shocks from the war with Iran, which are all but certain to be even greater in April when the Consumer Price Index data gets published next week, they are not gaining ground on inflation.

The headline jobs number was indisputably positive. The details underneath…not so much.

Stagflation is (almost certainly) coming.

Lou Costello Corrections

As with every Employment Situation Summary report, we have to take the headline numbers with a grain of salt. We know the April numbers will be revised in May and again in June, and we know that the revisions can be substantial.

The Bureau of Labor Statistics revised February’s job loss shocker down by an additional 23,000.

The change in total nonfarm payroll employment for February was revised down by 23,000, from -133,000 to -156,000, and the change for March was revised up by 7,000, from +178,000 to +185,000. With these revisions, employment in February and March combined is 16,000 lower than previously reported.

Of the 331,000 new jobs initially reported during the first four months of 2026, 27,000 of them never existed.

We should anticipate future downward revisions to the job numbers, for once again the Employment Level from the Current Population Survey (Household Survey) diverges sharply from the Current Employment Statistics (Establishment Survey) All Employees Data.

That is a strong sign that Lou Costello Labor Math is at work in the jobs numbers.

If the number of new jobs is rising, the number of employed people should also be rising. That, at least, is the theory.

Why the reality is different highlights the ongoing data inadequacies of the Employment Situation Summary, and necessarily colors any analysis.

Corporate Media Does Not Question The Numbers

In their usual demonstration of journalistic inadequacy, corporate media once again take the report at face value.

CNN maintains the fictitious narrative that US labor markets are healthy and robust at the moment (they are not).

April’s employment gains mark an expected retreat from March, when a revised 185,000 jobs were created, boosted by factors such as the end of large labor strikes as well as favorable weather.

However, the job growth seen last month was much stronger than the 65,000 that economists had estimated. No change in the unemployment rate was anticipated.

The war in the Middle East wasn’t expected to negatively affect April’s employment numbers but it still presents a risk. The health of the US labor market and the broader economy could be negatively affected if gas prices stay persistently high and cut into consumer spending, raise business costs, as well as trickle into higher prices for other goods and services.

CNBC touted the consistency of the unemployment rate as proof of labor market health.

Nonfarm payrolls rose by a seasonally adjusted115,000 for the month, down from the 185,000 created in an unusually strong March but better than the 55,000 forecast in the Dow Jones consensus estimate.

The unemployment rate held at 4.3%, further proof that the labor market has reached a point where only modest job creation is needed to keep the jobless level steady, given little growth in the labor force.

Politico touted the jobs report as a clear victory for President Trump.

The Labor Department on Friday reported that U.S. employers added 115,000 jobs in April — more than double the 55,000 projected by surveys of economic forecasters — and the jobless rate was unchanged at 4.3 percent. With unemployment hovering below historic averages, and private sector hiring showing signs of a revival, GOP and White House messaging shops quickly seized on the report as proof that Trump’s economy is humming.

“The April jobs report is a clear upside surprise,” Eric Merlis, a managing director and co-head of global markets at Citizens Bank, said in a note shortly after the report’s release. And “importantly, the data suggests the hostilities in the Middle East have had little visible impact on the U.S. job market.”

Alternative media is not necessarily any better, with Breitbart insisting that labor demand is strong and that the “break even” jobs number is close to zero (it clearly isn’t.

That world is gone. What replaced it is a labor market in which the constraint has flipped to the supply side. The era of mass immigration supplying a steady stream of excess labor is over. As a result, the break-even rate — the number of new jobs the economy needs each month just to keep the unemployment rate stable — has fallen from the roughly 250,000 per month figure that became conventional wisdom during the Obama years to something closer to zero. Research from the Dallas Fed and the Federal Reserve Board has been pointing in this direction for quite some time, but the implications still haven’t sunk in for most analysts.

What’s more, demand for labor is extraordinarily strong. Except for the pandemic lockdown period, for years now we’ve been consistently below levels of unemployment that economists once thought were the markers of a healthy economy. Unemployment rates that once would have been seen as evidence the economy was overheating are now the norm.

Even the usually cynical ZeroHedge, while it acknowledged the negative signals in the report, led with the Employment Situation Summary turning in the first back to back pair of job gains month on month in over a year.

In his preview of today’s NFP report, Goldman’s Delta One head wrote that “NFP almost feels like a sideshow at this point. You can argue weak labor data gives a Warsh led Fed enough cover to cut, but with oil and input inflation still elevated there’s also an argument that a weakening labor market alongside a constrained Fed is actually the more difficult combination for risk assets.” With that in mind, moments ago the BLS reported that in April the US added a red hot 115K, above the median consensus of 65K (and near the upper end of the forecast range which peaked at 133K), down from an upward revised (for once) 185K (originally 178K). This was the first back to back gain in jobs in a year.

Given the disparity between the Employment Level and All Employees payroll level, we should not expect either the March or the April figures to remain at their elevated levels. I shall be happy to be proven wrong, but the divergence strongly suggests the ESS jobs data remains sketchy and problematic at best.

Uneven Job Growth

Also of concern is the uneven nature of the reported job growth.

Unlike the March JOLTS data, which showed across the board job growth, the April data is tempered by job losses in notable sectors.

Of particular concern is Manufacturing once again shedding jobs, which has been its pattern for far too many months now.

That is a sobering reminder that, even with job gains in Mining and Construction, goods producing jobs are still not in perfect health.

Among service providing jobs, one positive note was the increase in Trade, Transportation, and Utilities jobs.

For a change, TTU job growth outpaced Healthcare job growth.

The strong gains in these two sectors served to counter the job losses in Information and Finance.

Leisure and Professional Services posted unremarkable job growth.

At a time when Artificial Intelligence is generating much hype and hooplah in the media, the continued loss of Information sector jobs should stand as a reminder that AI is far from the proven economic revolution many proclaim it to be.

There is strong growth reported in some job sectors. Other job sectors continue to underperform, with minimal job growth or actual job loss.

This is not a rising tide of employment which is lifting all job ships.

Joblessness Rises

While the official unemployment rate is reported as remaining unchanged, that assessment is a result of rounding at the first decimal place rather than the second.

When the ratio of unemployed persons to the overall workforce is carried another decimal place, the official unemployment rate shows a rise from 4.26% to 4.34%.

More significantly, the “real” unemployment rate—the official count of unemployed plus those not in the labor force but who want a job now—rose from 7.49% to 7.60%.

The actual count of unemployed workers rose 7,373,000 in April.

While this is still down from a November 2025 peak, it is still significantly higher than where it was at the start of the Trump Presidency.

The peak was earlier for those Not in the Labor Force who Want a Job Now, but the longer term trend is still rising.

The overall category of workers Not in the Labor force has been trending up since January 2025.

Whatever the “break even” jobs number is for the US economy, it is clearly somewhere north of 115,000. A break even figure would leave both unemployment numbers and those not in the labor force decreasing rather than increasing.

This rise in joblessness is consistent with the ongoing decline in the overall Employment Level.

The current decline is the third such period of stalled or negative employment growth in the US since 2021. Aside from brief episodic bursts of employment, employment growth has been problematic since the beginning of 2022.

This lack of employment growth shows up as a persistent decline in the Employment Population Ratio since 2023.

If employment is declining, if the employment population ratio is declining, and if joblessness is rising, the one thing we cannot say is that labor demand is “strong”. Certainly it is not “strong enough.”

At the macro-economic level, that’s a problem.

Wages Remain Soft

While wages are increasing in nominal terms, only goods producing wages have fully recovered from the 2022 hyperinflation cycle. Service producing wages and overall private sector wages remain very much behind inflation.

Also of concern is that, broadly, wage growth by sector has been getting softer as we move through 2026.

Even though manufacturing wages had just caught up with inflation at the start of the year, the recent price shocks and consequent inflation increases make it unlikely that manufacturing wages will continue to remain above the rise of inflation.

Most service providing wages remain below the inflation curve and have not recovered any real ground after the 2022 hyperinflation cycle.

When the Consumer Price Index data comes out next week, these sectors are all but certain to have lost even more ground—even Healthcare, which has been the mainstay of job growth in the US.

Nor should we be surprised that wages remain soft. When there is rising joblessness, by definition labor supply is outstripping labor demand. When supply is plentiful and demand is scarce, prices—in this case, wages—drop.

Soft wages and rising joblessness tell us in unequivocal terms that we still are not producing the numbers of jobs we need to keep joblessness at bay or on the decline.

If the economy were producing jobs above the much-ballyhooed “break even” number, wages would be rising. In sector after sector, they are not.

That’s a problem.

Signs Of Stagflation?

With signs of soft labor markets within the jobs report, the coming (and by now unavoidable) inflation shocks lead to a very uncomfortable question: is the US about to experience a stagflation crisis such as it saw in the 1970s?

Certainly the risks of stagflation are real. I have written about those risks quite a bit in the past and the war with Iran give those risks an immediacy they did not have before.

Nor can we overlook the reality of a growing stagflation crisis in China, as their petroleum supply chains get disrupted from the war with Iran.

On Friday, Maersk Shipping CEO Vincent Clerc warned that price increases were heading into most economies, as shipping companies grapple with the increased costs of bunker fuel. Such increases are likely to entail at least a measure of demand destruction.

“As some of these costs make their way all the way up to the end consumer, will we see demand destruction at the consumer level? And will that then reverberate throughout the supply chain with softer demand in the second part of the year?” he questioned.

“That is certainly something that we’re looking out for very, very closely, because it would suddenly change the equation on how this crisis is going to impact the global supply chain and our industry in particular.”

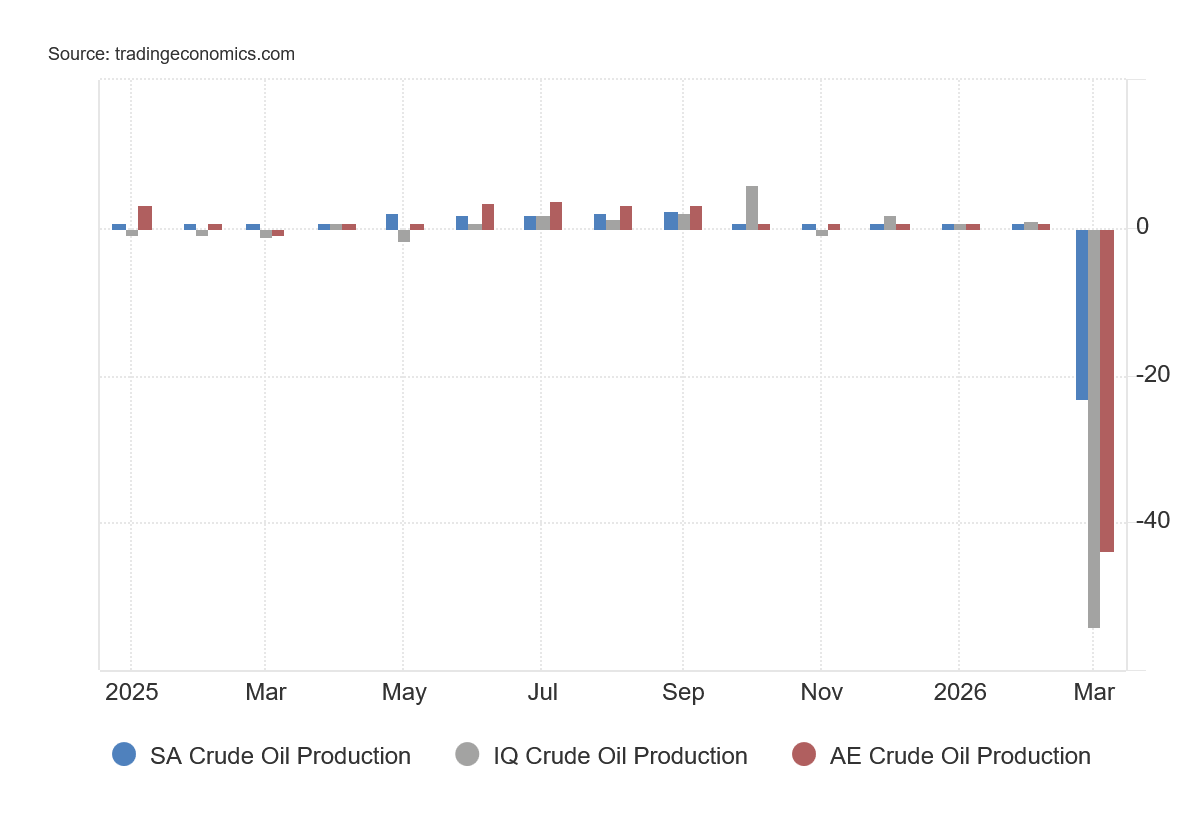

Nor can we assume that Clerc is merely using the war as a cover to push through price increases as a form of rent-seeking behavior. That Persian Gulf oil production has fallen precipitously just through March is already established.

While bunker fuel rates had been declining in the start of April, by the end of the month they were clearly trending up.

Additionally, signs of global oil supply disruption are increasing, as observed global oil inventories, which had been rising in 2025, are anticipated to decline as the disruptions from the Persian Gulf take hold.

An oil supply shock may even be in store for the US, as crude inventories—including those in the Strategic Petroleum Reserve—are declining at present.

Exactly how great a supply shock there might be is problematic, because while production has not varied much over the past year—and has even dropped off in recent weeks—there has been growth in US exports of refined products.

There are definite stresses to US oil supply due to emerge within the US economy, but there is also a not insignificant export buffer which can cushion some of the shock.

If the war with Iran persists, we are very likely looking at a global economic scenario where the question is not if there will be stagflation, but how much stagflation will there be? Right now, that estimate is rising.

Good But Not Good Enough?

The April jobs report shows there was job growth in the United States. That report echoes the ADP report and is a continuation of reporting trends from March. Even if we anticipate significant corrections to the data (and I do), we are still looking at a report that shows a greater level of job growth than we have seen in recent months.

Job growth is always a good thing, and on that basis the April jobs report is a good report. Yet job growth that does not meet or exceed the available labor supply—job growth that comes in below the “break even” threshold, is ultimately a net negative.

We need to create more jobs in this country, and we need to create significantly more jobs than the 115,000 reported as the headline figure for the April report.

We need significant increase in labor demand because that is the only way we can get increases in wages, allowing workers to finally catch up to the 2022 hyperinflation cycle. Wage increases are likely to become a particularly thorny topic, as the war with Iran is quite probably going to give rise to at least a brief surge in inflation, if not a completely new hyperinflation cycle.

In April we got significant job growth. Unfortunately, we did not get enough job growth. We certainly are not getting needed wage growth.

March and April have produced sizeable jobs numbers, and that has lent them an optimistic, upbeat appearance.

However, with joblessness rising and wages not rising, we are faced with the blunt reality that March and April were not good enough. With corrections still yet to be made, March and April should be anticipated to be seen as less good than they are now.

Without the war with Iran, this would have been a good jobs report. With the war with Iran, this is a cautionary jobs report, and a warning that future months are not likely to be at all as good.

Stagflation is (almost certainly) coming.

This is terrible - thanks for the heads up.