Two years ago, when the Evergrande debacle began to burst upon the Chinese economy, I argued that China was, is, and has been the “sick man of Asia”.

The other day I pondered the possibility that the twin crises at Country Gardens and Zhongzhi Enterprises mean China is on the brink of its very own “Lehman Brothers” moment.

Yet over and above the immediate issues of China’s ailing economy, there lies an important lesson for the US as well: “Bidenomics” is simply BS.

China’s woes, and Beijing’s seeming incapacity to deal with them, are but the latest reminder that when it comes to economics, no one, not even totalitarian regimes, can push a string. Time and again, we see that governments are largely impotent when it comes to economic concerns, and that makes the White House’ incessant braggadocio over “Bidenomics” particularly foolish.

Country Gardens woes are largely Evergrande redux, so let us begin by focusing on Zhongzhi Enterprises, China’s sixth largest private wealth manager recently defaulted on numerous wealth management products.

Zhongrong International Trust Co. missed payments on dozens of products and has no immediate plan to make clients whole, indicating troubles at the embattled Chinese shadow bank are deeper than previously known.

Wang Qiang, board secretary of the firm partly owned by financial giant Zhongzhi Enterprise Group Co., told investors in a meeting earlier this week that the firm missed payments on a batch of products on Aug. 8, adding to delays on at least 10 others since late July, according people familiar with the matter. At least 30 products are now overdue and Zhongrong also halted redemptions on some short-term instruments, one of the people said.

Let that sink in for a moment: A Zhongzhi subsidiary has failed to make obligatory payments on numerous financial products, and the company has no plans on how it will correct this. Nor is this a one-time issue, but the culmination of a steadily worsening track record of late and/or missed payments in recent weeks. The seeming suddeness is merely an artifact of its coming to the media’s attention now.

Which China’s multi-trillion yuan shadow banking industry thus thrown into the hazard, one notionally would expect a swift and determined response from Beijing, which is also grappling with a number of sub-par economic metrics recently released.

Yet Beijing’s responses thus far have been a surprise cut on key interbank interest rates and vague exhortations for people to spend more. Even the “experts” amonog the corporate financial media do not believe these measures are likely to do much good.

China surprised by cutting its one-year medium-term lending facility (MLF) rates by 15bp to 2.50% today to give a jolt to its economy that has not only completely missed the expectation of a great post-Covid recovery, but that deals with deepening property crisis, morose consumer, and investor sentiment – which is worsened by Country Garden crisis and missed payments from the finance giant Zhongzhi Enterprises. Data-wise, things looked as worrying as we expected them to look when China released its latest set of economic data today. Growth in industrial production unexpectedly dipped to 3.7%, retail sales unexpectedly fell to 2.5%, unemployment worsened, while growth in fixed investments dropped further. Foreign investment in China fell to the lowest levels since 1998, and the 13F filings showed that Big Short’s Michael Burry already exited Alibaba and JD.com, just months after increasing his exposure to these Chinese tech giants. People’s Bank of China’s (PBoC) surprise rate cut will hardly reverse appetite for Chinese investments as meaningful fiscal stimulus becomes necessary to stop halting.

The significance of the crises at Zhongzhi Enterprises is that China’s economic misfortunes are of a magnitude that Beijing would historically take as a call to dramatic action. That has not happened here.

Nor can Beijing reasonably hope to ride out the Zhongzhi debacle as a momentary financial hiccup, after which markets can return to normal. Whatever the origin of Zhongzhi’s payment problems are, even Zhongzhi recognizes they are not transient, as they have retained international accounting and consulting firm KPMG to guide it in a large debt restructuring.

The Chinese shadow banking giant whose liquidity crisis has fanned fears about financial contagion is planning to restructure its debt and has hired KPMG LLP to conduct an audit of its balance sheet, people familiar with the matter said.

Zhongzhi Enterprise Group Co. hired KPMG in late July to review its balance sheet amid a worsening liquidity crunch, said the people, asking not to be identified as the matter is private. The Beijing-based company plans to restructure debt and sell assets after the review in order to repay investors, the people said. The company manages more than 1 trillion yuan ($137 billion) of assets.

Note the chronology of that decision. A full two weeks before the financial media took note of Zhongzhi’s problems, they had already started on a path of debt restructuring. Whatever else we may surmise about those challenges, we may be certain they are not amenable to quick fixes, else there would have been one.

China’s shadowbanking crisis could not have come at a worse time. Not only is Country Gardens, China’s largest privately owned property developer, teetering on the brink of default on at least two dollar-denominated bonds, but recent economic data has confirmed China has officially slipped into consumer price deflation.

With exports and imports both having fallen by double digits in July, retail sales faltering, and with property prices continuing to decline, a crisis in China’s ginormous shadow banking sector was the very last thing the economic mavens in Beijing wanted to see.

Yet a crisis within China’s ginormous shadow banking sector is exactly what Beijing is now compelled to see. The markets have seen, and so Beijing cannot ignore.

What are they seeing? In a word: contagion. Zhongzhi’s problems are not contained to just the one company. As a partial owner of Zhongrong Trust, when some of Zhongrong’s products joined Zhongzhi’s in arrears, it meant that the problem, whatever it is (and we as of this writing still do not know the precise origin of Zhongzhi’s liquidity issues), is spreading beyond Zhongzhi Enterprise. How much beyond Zhongzhi we do not know—and for the markets, that is a problem.

Two listed companies said last week Zhongrong had failed to repay trust products, which offer savers and companies higher returns than traditional banks. This followed weeks of speculation over separate missed payments to retail investors from Zhongzhi’s wealth management businesses, which also direct billions of renminbi into savings products.

“When the crisis was only concentrated around Zhongzhi wealth management companies, the market was not so panicked,” said Karen Wu, an analyst at CreditSights. With Zhongrong, “the crisis has actually accelerated”.

One fear is that Zhongzhi’s problems either stem from or are contributing to the financial stresses facing Country Garden—a distinct probability given the propensity of wealth management companies to invest clients’ funds in real estate projects.

Given that shadow financing often flows into the property sector in China, the Zhongzhi group’s woes have fuelled deeper fears of spillover effects from a slowdown in the country’s once-booming real estate industry, which has already driven dozens of developers into default.

China’s trust industry typically “organises capital from companies and individuals” at higher rates than banks can provide, according to one former senior employee of a bank in mainland China. He added that trust companies in general “probably are overly exposed to real estate”.

Country Gardens own severe financial issues thus becomes at a minimum a painful reminder of this or a cause of Zhongzhi’s own liquidity concerns. Both crises in turn become a painful reminder of the ongoing (and perhaps worsening) debt issues among the many Local Government Financing Vehicles (LGFVs), with nearly 50 LGFVs in arrears on debt payments.

A total of 48 LGFVs were overdue on commercial paper, which typically carries a maturity of less than a year, up from 29 in June, according to a Huaan Securities Co. report citing data from the Shanghai Commercial Paper Exchange. Their missed payments amounted to 1.86 billion yuan ($259 million), versus 780 million yuan in June.

LGFVs missing debt payments. Country Gardens missing debt payments. Zhongzhi missing required wealth management payments. Zhongrong Trust missing required wealth management payments.

The reason there are pronounced fears about contagion effects from these various crises is because there is mounting evidence that contagion effects are exactly what is happening. If that is the case, then China’s financial problems are going to get a whole lot worse before they get better, and the “Lehman Brothers” moment thesis would have to be considered as proven.

While much of the corporate media is rather surprised at China’s “perfect storm” of economic problems, Michael Pettis, professor at Peking University, tweeted out a timely reminder that this is how systemic problems resolve themselves.

Somewhat equally surprising has been Beijing’s response to this perfect storm of debt issues. Rather than executing a strong and significant intervention to head off these growing issues and prevent contagion, Beijing has been consistently reactive and even hesitant in its response.

Last month, China’s state banks offered a series of 25-year loans to heavily indebted LGFVs at low or no interest to alleviate some of their debt burden.

Last month, the National Development and Reform Commission issued a “plan” to “restore and expand” domestic consumption—a plan that was long on policy pronouncements and short on details.

The NDRC went on to issue more policy statements voicing support for private enterprise within the Chinese economy.

The Chinese Politburo hinted at relaxation of real estate purchase restrictions in several major Chinese cities during the second have of 2023.

China’s National Financial Regulatory Administration, Beijing’s banking regulator, set up a task force to investigate debt and risk issues at Zhongrong Trust.

The People’s Bank of China recently issued a surprise 15bps cut on their one-year medium-term lending facility, lowering the rate from 2.65% to 2.5%. This was the second rate reduction in three months.

On top of the rate cut, the PBOC also injected 297 billion yuan into financial markets through the bank’s repo mechanisms.

China’s State Council promised more “targeted and forceful” macroeconomic controls to boost domestic consumption and meet Beijing’s annual economic growth targets.

The assessment of these measures by most of the corporate financial media is that they are too little and come too late to have much beneficial impact. As economist Michael Pettis said of the rate cut:

One reason why China may be perpetually backfooted is that President Xi Jinping’s recent national security focus may be working at cross purposes to economic concerns.

So why has China's response been so tepid?

The view of several China watchers is that President Xi Jinping's focus on national security is restricting and working counter to the economic effort, scaring off the money Beijing says it is seeking to attract.

While national security taking priority might be a natural reaction by Beijing to recent tensions with the United States, that is of little comfort to participants in China’s ailing economic sectors who would welcome fresh traunches of investment capital. Moreover, vague and imprecise high-level policy guidance is proving sparse on details, leaving lower bureaucrats and administrators caught in policy paralysis, where their safest personal course of action is to do nothing.

"The core problem this year is that the leadership has given vague, high-level instructions for officials to balance economic development against national security," said Christopher Beddor, deputy director of China research at Gavekal Dragonomics.

"If officials are unsure what the leadership wants them to do, they're likely to put off any action until they receive more information. The result is policy paralysis, even if that comes at a substantial cost."

Another reason may be even more elemental: China could just simply be running out of money. More precisely, China may be limited on how much more debt financing it can utilize to stimulate economic growth.

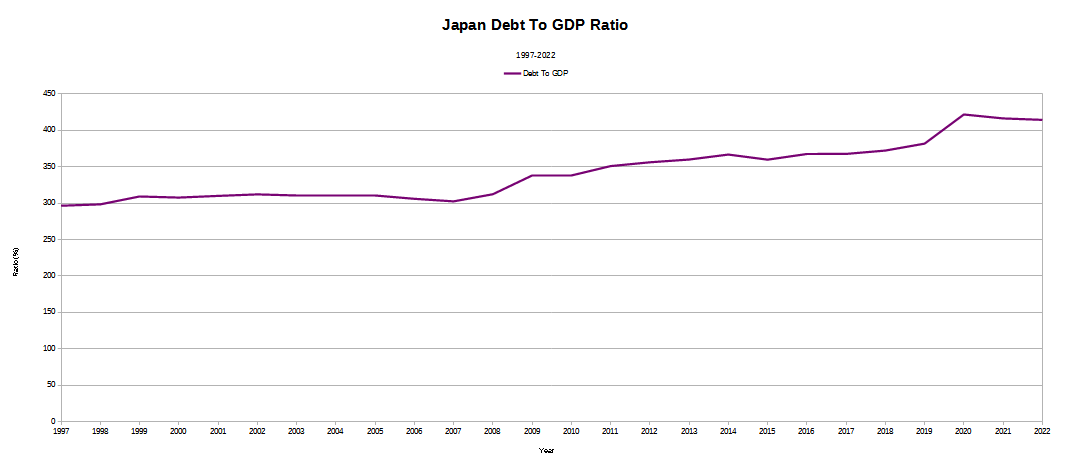

To understand how this can be, one has to recall that, as of the end of 2022, China’s debt-to-GDP ratio stands near 300%, per the Bank of International Settlements. Not only is it among the highest in the world, since the 2007-2009 Great Financial Crisis, China has been steadily ramping up debt relative to GDP in order to stimulate the economy.

Even the United States, which at one time had a higher debt-to-GDP ratio than China, managed to at least pause its debt accumulations relative to GDP in the years prior to the COVID Pandemic Panic.

While the US did dramatically increase its overall debt relative to GDP in response to the Pandemic Panic, since then the ratio has returned to near the overall norm that has been in place since 2010. China has not managed to do this, and so its ratio has overtaken that of the US.

Based on the prevailing trend, China is not on pace to stop increasing debt relative to GDP any time soon—and this is without a fresh burst of fiscal stimulus. Even Japan—home to the ultra-profligate “Abenomics”—has, relatively speaking, shown more fiscal restraint, as it has at least trimmed its borrowings recently.

Of the heavily indebted nations, China is the one leading economy that has yet to demonstrate any significant post-COVID restraint on debt financing. Quite simply, China may very well have maxed out the metaphorical credit card, and simply has no upward room to manuever in terms of debt financing.

With limited ability to ramp up fresh debt-driven stimulus, Beijing is reduced to offering anodyne policy positions with no real guidance on implementation, nor any substantive guarantees of financial commitment by Beijing. Alas for Beijing, one cannot simply jawbone a country’s way into increased consumption. Unless and until Chinese households have greater income relative to price levels, consumption increases will be marginal at best.

Without real transfers to households or other means of boosting household real incomes, all the policy statements imaginable will not boost consumption sufficiently to lift China’s economy off the deflationary shoals.

Simply put, Beijing is largely powerless to do anything about China’s moribund economy. All it can do is sit back and watch—which if it had done years and even decades previously, China would not be in the mess that it is today.

Beijing is well and truly hoisted by its own misbegotten policy petard on matters economic. While there are a number of macroeconomic forces at play even globally which are entirely beyond the control of anyone, including central banks, much of China’s current woes are directly traceable to various policy errors made over the past years and decades. It is not an exaggeration to say China’s problems are substantially unforced errors by Beijing.

China’s experience with government intervention in and manipulation of the Chinese economy also offers up a teachable moment on why government interventions in the economy are a bad idea—inevitably, they only produce greater problems.

This same teachable moment also shows why the White House’ inane victory lap tweets over the “success” of “Bidenomics” are utterly absurd. Let us be clear, the White House does take undeserved victory laps and credit for any seeming economic good news.

Yet what “Bidenomics”—just as with “Abenomics” and with every other program or agenda of government intervention in the economy—fails to grasp is that government intervention is by definition the creation of economic disequilibrium. The economic scales are being moved in one direction or another, regardless of whether the purpose is good or ill. To put the government thumb on the economic scale is to unbalance that scale, and to skew the results.

China has had its thumb on the scale for decades, and the inevitable correction that must come from such enforced economic imbalance, shows that to attempt to “fix” the economy is ultimately to help break the economy. So, too, has it been and will it be with Bidenomics and the current state of the US economy. What the White House wants to celebrate as Bidenomics “working” is at most the economic calm before the storm.

As China is experiencing now, when the imbalances arising from the government pushing the economy always in one direction coaelsce and opt to push back, the resultant crisis is invariably an order of magnitude worse than the problems government originally thought it was solving. Where the White House is tweeting out victory laps over the direction it is pushing the US economy, it really should be tweeting out warnings of the correction that invariably must come.

2023 is proving to be the year China’s economic chickens come home to roost. Sometime soon the same fate awaits “Bidenomics” economic chickens as well.

The inexorable trend throughout the universe is one towards equilibrium. Any attempt to inject disequilibrium into an economy must ultimately end in a correction at least as large as the initial unbalancing.

Just as in China, that correction is what Bidenomics truly is—and what awaits us all.

Yep, they are following us "over the cliff."

The real bet is which one of us will hit the valley floor first.

For me the Laffer Curve is the best illustration of how widespread economic ignorance is. Using the back of an envelope, a sixth-grader could become an almost instant expert on the Laffer Curve. Yet Biden travels the country calling it "Trickle Down Economics," and, here's the most disheartening part, Republicans let him get away with it because they don't understand it either.