Contagion Effects In Full Force As China's Economy Spirals Towards Collapse

The Real Estate Crash Is Producing Considerable Collateral Damage

“Contagion” is the four-dollar term economists use to describe what happens when a calamity in one market or economic sector drags down other markets or sectors—a process also known to many as “stuff” rolling down hill.

China has become a textbook example of contagion as the real estate crisis that largely began with Evergrande’s serial defaults has now spread to a full on debt/mortgage/banking crisis, a factory output crisis, and an industrial crisis.

The most visible sign of contagion is the collapse in July of home sales.

Sales at the country’s top 100 property developers fell 39.7% in July from the same period last year to the equivalent of $77.6 billion, or 523.14 billion yuan, according to data released Sunday by CRIC, a Chinese real-estate data provider.

July sales were down 28.6% from June, ending a two-month recovery in month-to-month sales growth. Apartment sales showed increases in May and June from the previous months, as activity picked up following Covid lockdowns in Shanghai and other Chinese cities earlier this year.

A 40% drop year-on-year and a nearly 30% drop month-on-month is no minor correction. This is a correction on the order of the US housing bubble collapse between 2005 and 2010—a true collapse of Chinese residential real estate.

Mortgage Boycott Fueling Banking Crisis

The drop in home sales represents the second part of a double-whammy for China’s banking sector. The drop in home sales equates to a drop in mortgage lending by banks and financial institutions—while at the same time the mortgage boycott that is catalyzing the sales decline is adding default stresses to those same banks. With approximatel 38 trillion yuan in outstanding mortgage debt, already some 2.4 trillion yuan of that amount is at risk of default due to the boycotts, and the amount of exposure grows as the boycott movement spreads.

In a worst-case scenario, S&P Global Ratings estimated that S$492 billion, or 6.4 per cent of mortgages, are at risk while Deutsche Bank AG is warning that at least 7 per cent of home loans are in danger.

So far, listed banks have reported just 2.1 billion yuan in delinquent mortgages as directly affected by the boycotts.

To illustrate the magnitude of the banking problem, with just a 10% drop in real estate investment, banks face a loss of 17% of their earnings.

A 10 percentage-point slowdown in real estate investment growth translates into a 28 basis-point increase in overall bad loans, meaning a 17 per cent decline in their 2022 earnings, Citigroup analysts led by Judy Zhang estimated in a July 19 report.

Unless there is a quick rebound in home sales, the banks are facing an earnings drop multiple times that 17% figure—furthering the parallels with the 2008 financial crisis here in the US.

Banking Crisis Magnifies Real Estate Crisis

The rise in the percentage of bad loans and the drop in home sales is creating a deadly feedback loop in liquidity for the real estate sector, magnifying the existing problems. With bank earnings under extreme duress, less capital is available to extend loans and credit to distressed developers.

“Banks are caught in the middle,” said Zhiwu Chen, a professor of finance at the University of Hong Kong Business School. “If they don’t help the developers finish the projects, they would end up losing much more. If they do, that of course would make the government happy, but they add more to their exposure to delayed real estate projects.”

Without fresh funding, however, the list of stalled and uncompleted housing projects is almost certain to expand—as will the mortgage boycott arising from those additional stalled developments, further fueling delinquencies and defaults, compressing bank earnings even further and constricting even more credit to distressed developers.

So far, Beijing’s response to the metastasizing crisis has been largely hands off, although recently there does appear to be progress being made on a state bailout fund to address stalled housing projects and bring them into completion (thereby alleviating the mortgage boycott situation).

Chinese authorities are promising to establish an initial rescue fund of $11.8 billion (80 billion yuan) to offset a looming crisis in the real estate sector, where home buyers routinely purchase residences from developers' plans and begin making mortgage payments before the dwellings are finished, media reports said.

With over 2 trillion yuan in mortgages at stake, however, the impact of an 80 billion yuan rescue fund is likely to be problematic at best. With over 320 stalled developments as of this writing, and more likely to follow, the liquidity needs of developers will almost certainly exceed the 80 billion yuan fund size reported thus far. Having delayed the creation of such a fund while leaning on local governments to resolve the real estate and banking issues within their jurisdictions, Beijing is at serious risk of compounding the “too late” error with a “too little” one.

From Collapsing Real Estate To Collapsing Steel

With real estate having been a primary driver of GDP growth in China over the past few years, the collapsing real estate sector is a major crisis all on its own for Beijing. However, the pain does not end with that one sector, nor even with that plus the banking sector under debt default stress. The cessation of construction work on the stalled projects has greatly diminished revenues for China’s steel mills, and a number of them are facing bankruptcy.

Almost a third of China's steel mills could go into bankruptcy in a squeeze that is likely to last five years, Mr Li Ganpo, founder and chairman of Hebei Jingye Steel Group, warned at a private company meeting in June.

"The whole sector is losing money and I cannot see a turning point for now," he said, according to a transcript of the gathering seen by Bloomberg News.

A business that goes bankrupt, of course, is one that does not live to recover later—it is gone for good. A contraction of the steel industry in China would be a staggering blow to its vaunted industrial and manufacturing output.

Steel mills are facing a true deflationary spiral, as stalling real estate development is crushing the demand for construction steel which in turn is causing the prices for steel to collapse.

In the short term, the major obstacle for steel is the large stock of unfinished properties, highlighted by a recent wave of mortgage boycotts. Prices of construction steel have also plunged, with rebar - twisted steel rods that strengthen concrete - falling to a two-year low last week. This is even as output has dropped to the lowest in Mysteel data that goes back to 2015.

Local governments are pressuring steel mills to sustain current output levels even without the accompanying demand for steel—keeping overall costs high for the steel mills even as their revenue drops.

Steelmakers may have limited room for manoeuvre when it comes to trimming output. Local governments are putting pressure on mills to maintain activity to prevent weakness in economic data, according to executives from four producers, who asked not to be identified as the matter is sensitive.

Steel mills were once seen as champions of China's economic expansion, with some growing from rural casting workshops to multibillion-dollar conglomerates. While real estate activity should stop contracting at some point, the chances of it delivering the kind of booms that buoyed Asia's largest economy over the past few decades seem slim.

This sort of padding of economic data merely kicks the deflationary can down the road, as the steel mills can only sustain production costs in excess of revenues for only so long before they collapse into bankruptcy.

Steel Is Dragging Manufacturing Down Overall

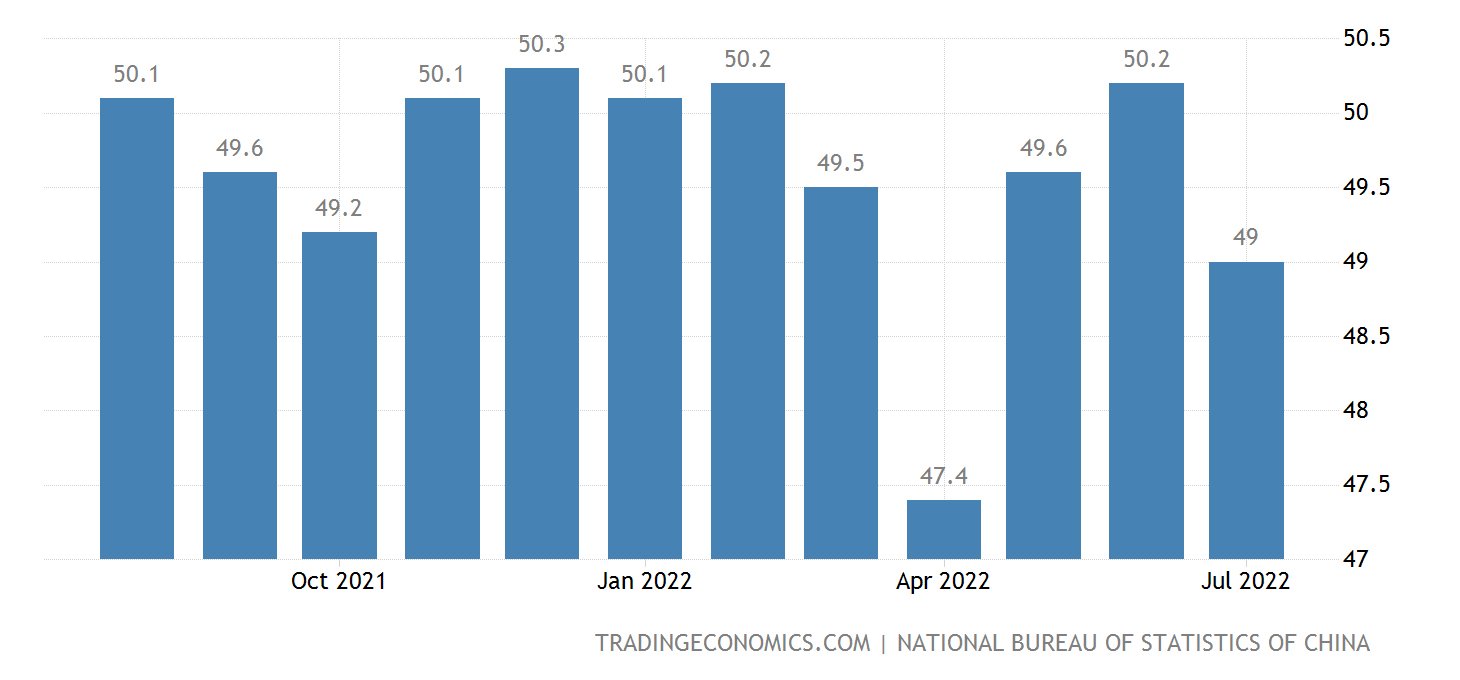

The steel industry’s woes are undoubtedly one factor behind the sudden contraction in China’s factory output in July, when marginal growth had been forecast.

The official manufacturing purchasing managers’ Index (PMI) fell to 49.0 in July from 50.2 in June, below the 50-point mark that separates contraction from growth, the National Bureau of Statistics (NBS) said.

Analysts polled by Reuters had expected it to improve to 50.4.

Even Caixin’s alternate PMI metric shows softening, although still remaining above the 50 mark that separates expansion from contraction.

Between collapsing real estate construction and the knock-on effects of the recent COVID lockdowns, China’s manufacturers are in a perfect storm of weak and diminishing demand coupled with high (and rising) raw materials costs.

Chinese manufacturers continue to wrestle with high raw material prices, which are squeezing profit margins, as the export outlook remains clouded with fears of a global recession.

Weak demand has constrained recovery, Bruce Pang, chief economist and head of research at Jones Lang Lasalle Inc, said in a research note. “Q3 growth may face greater challenges than expected, as recovery is slow and fragile.”

The global economic recession serves only to compound these woes, as global demand for Chinese output is itself deteriorating.

Monetary Stimulus Has Not Helped

Previously, I have noted how the People’s Bank of China has opted to pursue a contrarian “loose money” policy very much the polar opposite of the Federal Reserve’s current campaign of higher interest rates and money supply tightening.

That policy is notionally in keeping with the state of economic thinking among western Central Banks, and it has been plagued with a similar drop in monetary velocity that neutralizes much of the stimulative effect money supply expansion is thought to provide.

Cash-rich lenders and funds have been using the money to buy policy bank bonds and high-grade corporate debt, as well as the dollar as the growing interest-rate differential between China and the US boosts the currency’s appeal, according to data compiled by Bloomberg.

The result of this behavior by lenders is that money which otherwise would be flowing into the general economy (and, for example, funding embattled developers)—a scenario that bears uncanny resemblance to the drop in monetary velocity here in the US even as asset prices rose.

While the PBOC has not done the gargantuan “quantitative easing” the Fed has done, since 2020 the bank has been steadily increasing China’s M1 money supply—ostensibly to provide monetary stimulus to an embattled economy, but with little to show for it.

That China is engaging in some measure of easing is made plain the concurrent rise in the PBoC balance sheet since 2020.

Zero COVID—The Engine Of Zero Growth

No assessment of China’s economic collapse would be complete without acknowledging the tremendous economic shock China has willingly inflicted upon itself with Beijing’s dogged insistence on “Zero COVID” protocols for dealing with the SARS-CoV-2 virus. All of Beijing’s various efforts to stabilize and stimulate the economy have been confounded and completely countered by the intentional economic damage of “Zero COVID” policies.

With COVID cases continuing to crop up—and forcing cities to return again and again to various degrees of lockdown—not only is Zero COVID a proven failure at disease containment, it makes any sustained effort to confront China’s metastasizing economic crises impossible. There is no amount of policy, fiscal, or monetary stimulus that can work when portions of the economy are shut down by decree.

Is Collapse Inevitable?

China’s notorious lack of transparency on economic matters makes any prediction of what will be the outcome of these multiple crises exceedingly problematic. Certainly, should the mortgage boycott trend continue, should the banks suffer increasing debt delinquencies as a result, should the real estate sector continue its precipitous decline, there is no credible scenario for any sort of “soft landing” left.

With Beijing already committing to a limited (and probably inadequate) bailout of real estate developers, a refusal to bail out the banks should the debt delinquencies approach a critical mass is almost certainly a political impossibility. However, such a bailout would require the very sort of central bank balance sheet expansion that Beijing has so far shied away from—the “QE on steroids” approach the Federal Reserve deployed in 2020. If the debt contagion threatens state-owned banks, there will be no other source of capital to sustain the banks save the PBoC.

Even without a bank bailout, however, the reality of China’s economy is that it is shrinking, and there are no external nor internal engines of growth available to arrest that trend. Should the worst case scenario for China’s steel industry come to pass—a five year slump with one-third of steel mills going out of business—China’s trajectory to economic superpower status will be well and truly derailed.

What that would mean for the CCP and Xi Jinping one can only guess. Would the CCP lose the “Mandate of Heaven” and fall from power? While it seems unlikely, given the lack of any acknowledged organized opposition to the CCP within China, the speed with which the former Soviet Union faded into nothingness leaves that possibility very much on the table.

Even if the CCP should remain in control of China, it is far from certain that Xi Jinping will remain in control of the CCP. With the party Congress coming up this fall, where Xi is widely believed to seek a third term as President, these economic woes could not come at a worse time for him and his ambitions to remain in power effectively for life. Who would assume the leadership of the party should Xi be forced out is unknown, and so, too, are the consequences for China’s policies within China and abroad.

Is collapse inevitable? Perhaps not inevitable—but it is extremely difficult to see the current state of affairs not ending extremely painfully for China. If not collapse, a “hard landing” for the Middle Kingdom seems very much in China’s near future.