I will begin by repeating a point I made yesterday, when the major stock indices were all severely down: bubbles, while easy to inflate, are not easily deflated.

If the media is correct, the stock market decline was a function of jitters over the Fed's much microanalysed new tighter monetary policy and jitters over a possible war with Russia over Ukraine.

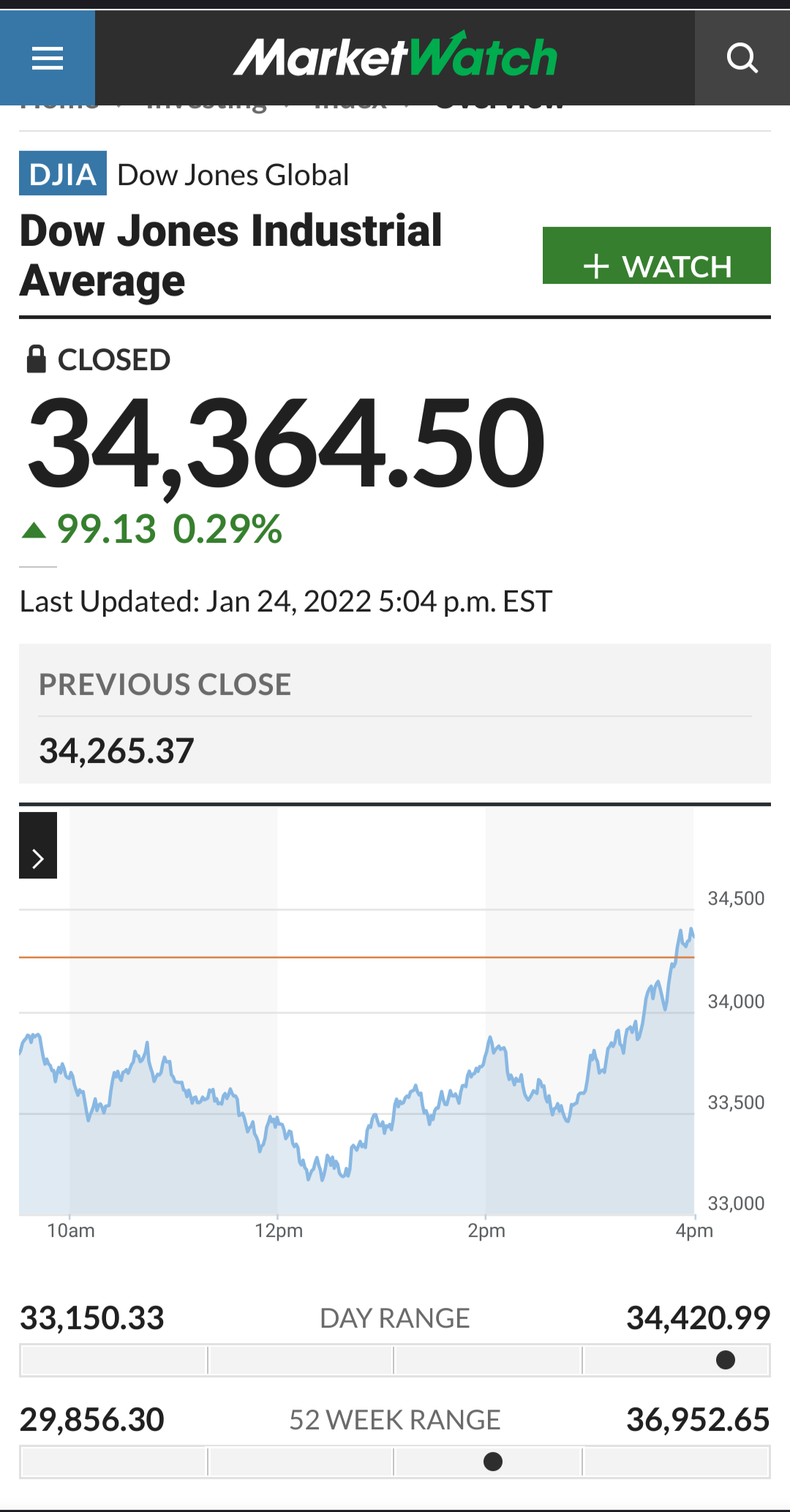

The Dow Jones Industrial Average has dropped more than 1,000 points Monday as financial markets buckled in anticipation of inflation-fighting measures from the Federal Reserve and the possibility of conflict between Russia and Ukraine.

Were there any statements by the Fed yesterday to change “sell” to “buy”? Certainly there are no mentions of any in the media.

The Pentagon said Monday that Defense Secretary Lloyd Austin has put up to 8,500 troops on alert, so they will be prepared to deploy if needed to reassure NATO allies in the face of ongoing Russian aggression on the border of Ukraine.

If the AP original interpretation of the morning's declines was accurate, yesterday's news was hardly the sort of encouragement to spark the afternoon's reversal.

So how did a record down day turn into slim gain?

That is a very good question…for which there is at the moment no good answer.

The Mainstream Media View: The Correction Was Overdone

In the eyes of the mainstream financial media, the afternoon reversal was simply a case of cooler (or perhaps greedier) heads prevailing.

Selling may have reached a capitulation point with the CBOE Volatility Index (VIX), known on Wall Street as the market’s “fear gauge,” hitting its highest level since November 2020, surpassing the 38 level at its intraday highs.

Once the fear gauge hits those extremes, the market has a tendency to snap back, even if only temporarily.

Marketwatch expressed a similar interpretation of the day.

Monday’s early stock-market selloff “was a reflection of surprise and fear,” said Mike Zigmont, head of trading for Harvest Volatility Management in New York. “But despondency turned into optimism and potentially greed, and now investors are thinking about the profit opportunities instead of the risk of losses.”

Yet from where comes the optimism? Despite the good ending to the trading day, all the reasons for fear and pessimism at the start of the day remained at the end. That the US now has troops on alert due to the escalating Ukraine standoff with Russia should be magnifying those fears, not calming them.

Bloomberg Quint, quoting Credit Suisse Securities' Jonathan Golub, suggested that the day's upheavals were nothing extraordinary.

“If there was an event -- an announced change in Fed policy or a big problem with corporate profits -- this thing wouldn’t have reversed itself. It would have been a move lower,” Golub said. “What does this tell me? What it tells me is there was nothing fundamental here.”

If there was no event driving things, however, what turned the selloff into a rally? It is one thing for a selling rout to halt late in the trading day, but it is quite another for the Dow to stage a record rebound as it did yesterday.

While the mainstream media argues that there is nothing abnormal about a record-setting rollercoaster trading day, such a day is abnormal by definition.

“Something” drove the late day rally. The mainstream media does not tell us what. That alone invites speculation.

Enter The “Plunge Protection Team”

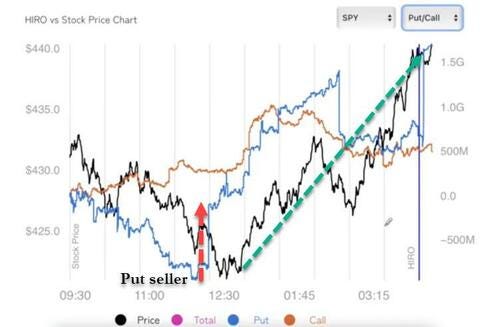

In the alternative media (to which, technically, this newsletter belongs), the primary speculation is that the government's Working Group on Financial Markets, colloquially labeled the “Plunge Protection Team” intervened behind the scenes to halt the slide and prop up the markets. As ZeroHedge argues, the turnaround was driven by the sudden sale of a tremendous number of “put" options from an unknown party at midday, at the height of the morning's carnage.

As shown in the chart below, which in addition to the S&P in black also shows put (blue) and call (orange) deltas, a massive put seller suddenly appeared (which via the negative gamma feedback loop also means dealers suddenly reverse from selling S&P futures to buying) just around noon, that was responsible for the slowdown in dealer selling and subsequent reversal, as a huge short squeeze kicked in and sent stocks sharply higher for the rest of the day.

Was the unknown put seller the Working Group, or someone acting at the behest of the Working Group? At the moment, no one knows.

Who was the put seller? Was it some contrarian dealer who had finally had enough of the waterfall selling, or was it some major hedge fund with little to lose, or perhaps it was the infamous plunge protection team? We don't know….

Critics fear the Plunge Protection Team doesn't just advise, but actively intervenes to prop up stock prices—colluding with banks to rig the market, in effect.

Unsurprisingly, this suspicion is considered “conspiracy theory” by the financial mainstream. However, as Investopedia points out, there have been similar late day reversals as seemingly arbitrary and as unaccountable as yesterday.

On Monday, February 5, 2018, the Dow Jones Industrial Average (DJIA) experienced a drop that was twice as large as its biggest point decline in history. However, arbitrary and aggressive buying cut the decline in half in one day. On Tuesday and Wednesday of that week, stocks opened lower, and each time aggressive buying buoyed the markets. That aggressive buying, some say, was being orchestrated by the Plunge Protection Team.

Or, to take a more recent example: The Plunge Protection Team's aforementioned teleconference on Dec. 24, 2018. That whole month, the S&P 500 had been heading towards a record decline—the motive for the team's meeting—and the DJIA dropped 650 on the 24th alone. But when trading resumed after Christmas, the DJIA rallied over 1,000 points. On the 27th, it lost half those gains, until a late-day reversal stopped the slide, and caused the market to close 600 points up. That's no coincidence, conspiracy theorists argue.

At first glance, yesterday's market rollercoaster certainly appears to be a replay of these earlier unusual reversals--record market losses suddenly reversed with no good explanation for the sudden put options sale which catalyzed the shift.

Still, even ZeroHedge does not have conclusive evidence the Working Group is actively rigging the markets, merely speculation. While that speculation is tantalizing to some, speculation is not evidence, and we should not presume that it is, even when the speculation fits all the known facts. We know the Working Group exists, and that it is alleged to have manipulated the markets in the past; we do not know with certainty the allegations are true.

The Drop Can Be Explained. The Reversal Cannot

At this time, the facts are that the mainstream and alternative media broadly concur on the forces which drove yesterday morning's market declines…and there is no concurrence on the reasons for the reversal. We know it happened, but we do not know why it happened.

We also know that, despite the reversal, the fundamental driver of the market’s decline is once again the money supply manipulations of the Federal Reserve. Just as happened in 2001, 2008, and, to a lesser extent, 2018, monetary tightening—or, in this instance, the mere mention of the intent to tighten—pushes financial markets down, just as the Fed's magic money printing pushes them up.

We know one more thing as well: we know the late-day reversal, despite its record-setting magnitude, changes nothing overall. The Fed is still planning on tightening monetary policy (at least for now…whether recent market behavior results in a change of plans at today's FOMC meeting remains to be seen). Tighter monetary policy will force financial markets down; just as the Fed's loose policies caused asset price inflation within those markets, tightening those policies will cause asset price deflation, to the inevitable chagrin of investors.

What the late-day reversal demonstrates is the near total disconnect between the financial markets and financial reality. The historical fundamental drivers of asset values—metrics such as corporate earnings that have made market indices useful albeit extremely broad proxies for the direction of the economy—are no longer significant factors in financial market behavior. The only relevant factor in today's markets is what the Fed (and, by imputation, the rest of the world's central banks) is doing or will do next.

Thanks to the Fed's persistently delusional monetary policies, which have stubbornly ignored the economic reality surrounding them, financial markets are now a fantasy land, complete with last-minute knights (“plunge protection team”?) riding in to save the day. Yet the day will come when there will be no knights riding in, when economic reality will reassert itself, Fed policy be damned.

When that day comes, financial markets will be left little more than a fantasy wasteland.