The Bureau of Economic Analysis released their initial “advance” estimate of what the US economy did during the third quarter, and it’s presumably very good news: the economy grew like gangbusters.

Real gross domestic product (GDP) increased at an annual rate of 4.9 percent in the third quarter of 2023 (table 1), according to the "advance" estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP increased 2.1 percent.

Unsurprisingly, corporate media describes the third quarter estimate as a “surge”.

The United States economy surged in the third quarter as a strong job market and falling inflation gave consumers the confidence to spend freely on goods and services.

If you take the data at face value, it is not hard to see why the “surge” language gets used. According to the BEA’s own press release, GDP growth in the third quarter was double that of the second quarter. That does sound like a “surge”!

Intriguingly, Wall Street did not take the data at face value and did not see the BEA report as good news, with all major indices posting declines on the day.

Perhaps even more intriguingly, Treasury yields also moved lower on the day.

Apparently, the GDP data was not all bad, from Wall Street’s perspective.

The devil of a detail is, of course, the predicate “if you take the data at face value.” As long-time readers already know, that’s rarely a safe assumption, especially when government statistics are involved!

First, we do well to have a bit of clarity on the language: an “annual rate of 4.9 percent” is a four-dollar way of saying that seasonally adjusted real GDP grew 1.2% over the third quarter.

The unadjusted real GDP printed at 1.15% for the third quarter.

Right away, we are forced to ponder the degree to with the seasonal adjustment process is accurate. However, as the unadjusted and seasonally adjusted numbers do not vary by all that much, we can work with the unadjusted numbers without risking any grave inaccuracies.

However, when we look at nominal vs “real” GDP (that is, GDP adjusted for inflation), we get a bit of a reality check: the disparity between the nominal and real values for GDP is increasing steadily over time, and has been since the emergence of hyperinflation in 2021.

The widening gap between nominal and real GDP means inflation is not only still a problem, but a growing problem.

If we index both nominal and real GDP to the end of the Pandemic Panic Recession (second quarter of 2020), we can begin to gauge the magnitude of the distortion inflation is imposing on the BEA numbers.

At the end of the second quarter, the difference between nominal and real GDP growth since Q2 of 2020 was 19.1% of Q2 GDP. Through the third quarter, that gap widened by a full percentage point, to 20.1%. Inflation reduced real GDP by an additional 1% during the third quarter.

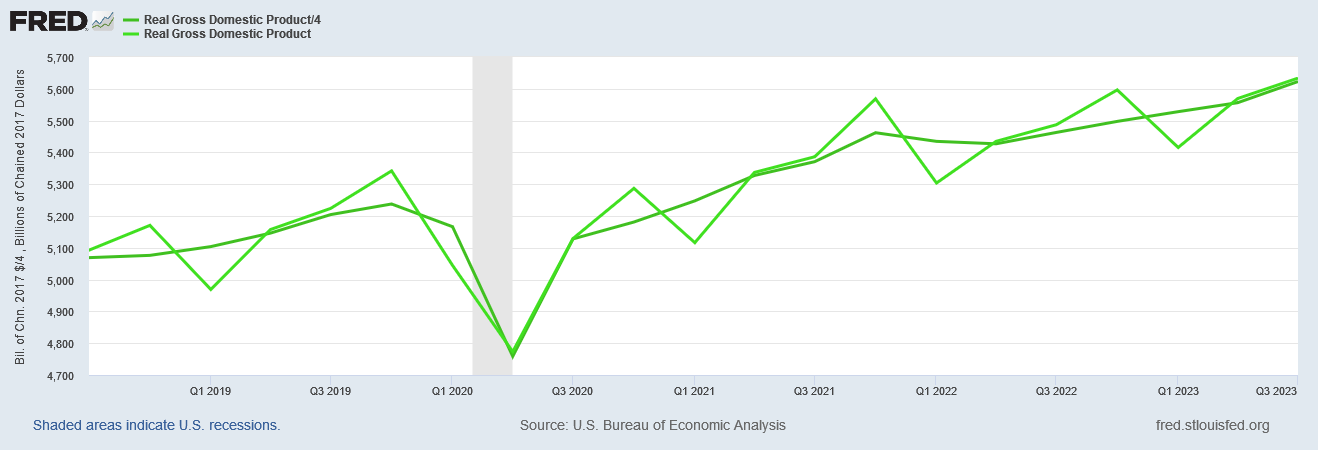

Yet we also have to address another problem presented by inflation: from the fourth quarter of 2021 through the third quarter of 2022, real GDP effectively declined, and didn’t achieve any further growth until the fourth quarter of 2022, even as nominal GDP posted increases.

If we index the GDP numbers to the fourth quarter of 2021, we see that from that point until the end of the third quarter of 2023, real GDP grew by a mere 1.2%

1.2% GDP growth over seven quarters does not sound like quite so much of a “surge”.

If we look at percentage GDP growth year on year we also see that, after a peak in the second quarter of 2021, the pace of GDP growth for both nominal and real GDP growth has been steadily slowing—and the real GDP pace of growth has been slowing more than the nominal pace.

We do see an increase in the pace of real GDP growth beginning in the first quarter of this year, which suggests a moderation in the weakening of GDP growth.

However, returning to the indexed data as of the second quarter of 2020, we also see that the disparity between nominal and real GDP growth has been increasing over recent quarters, and for the third quarter is greater than it has been since the third quarter of last year.

This suggests that inflation is showing signs of heating up again.

It is helpful to remember that the difference between nominal and real GDP growth is by definition inflation. Accordingly, if we look at the difference between percent year on year growth for both nominal and real GDP, we see that it closely hews to year on year percent consumer price inflation via the Consumer Price Index.

If we look for a moment at the seasonally adjusted data, we see that the differential between nominal and real GDP more or less falls midway between the year on year inflation rates for both the Consumer Price Index and the PCE Price Index (the PCE Price Index is the Fed’s preferred inflation gauge).

Note also that the seasonally adjusted CPI print is also showing rising inflation, something we see on the unadjusted data as well, when we look at the CPI data by month.

Thus we are left with two principal takeaways just from looking at the surface data from the BEA:

First, the “surge” encountered in this most recent quarter is in reality not much more than a recovery of the economy to 2021 levels, with a modest 1.2% growth beyond that. By implication this also confirms a point I have made multiple times in this newsletter: the US economy has been in recession for the bulk of the last couple of years, and certainly through most of 2022.

The second takeaway is that inflation continues to be a major drag on the economy, and is poised to become even more of one over the near term. Even before we consider the implications of a widening conflict in the Middle East, we were already facing an inflation scenario where consumer price inflation was “stuck” at a higher level than the Fed deemed desirable.

While oil prices have eased in recent days, they are currently about as volatile as events in the Middle East, and could move upward again quite easily.

As the September inflation report demonstrated, energy prices have comprised the bulk of inflation fluctuations, and any rise in energy prices translates almost immediately into a rise in consumer prices across the board. With energy prices in te current month already appreciably higher than they have been, the probability of consumer price inflation rising in the near term is quite significant, which means the drag of inflation on the economy will likewise be quite significant.

The optimistic take on the BEA numbers is that the US economy has in fact recovered to 2021 levels, and recovery is always the first step to genuine economic growth.

However, the inescapable reality is that said “recovery” is equally weighed down by persisting high consumer price inflation, leaving the economy far more fragile than robust, and quite vulnerable to all manner of reversal.

The BEA posted good economic numbers for the third quarter. Unfortunately, there is little to suggest those good numbers will extend into the fourth quarter, and quite a lot to suggest that they won’t.