Private sector employment increased by 242,000 jobs in February and annual pay was up 7.2 percent year-over-year, according to the February ADP® National Employment Report™ produced by the ADP Research Institute® in collaboration with the Stanford Digital Economy Lab (“Stanford Lab”)

Was the economy’s performance in February truly that good? Perhaps, but, then again, perhaps not—if one looks at the underlying details.

The first thing to note about the ADP numbers is that—just as with the BLS jobs numbers—the 242,000 new jobs metric is the seasonally adjusted figure. If we look at the raw unadjusted data, we see that total jobs in fact declined in February, by 166,000, according to the ADP report.

Why the discrepancy? In large part because there is a clear seasonal cycle in the ADP data, with a dip below trend during the winter months and a peak above trend during the summer months. The degree to which the seasonal adjustment factor is appropriate is always an eternal question, although ADP’s seasonal adjustment methodology does appear to smooth out the clearly seasonal peaks and troughs found in the raw data.

A concentration of workers in large businesses might be a boon for Big Business, but as a general rule such economic concentrations are less than optimal for the economy overall.

This is not a pattern that is indicative of a robust and growing economy; this is yet another pattern that is indicative of an economy in recession.

The January JOLTS report from the BLS similarly tells a tale of seeming resilience on the surface, which conceals problematic data and weakness underneath.

Job Openings

On the last business day of January, the number and rate of job openings decreased to 10.8 million (-410,000) and 6.5 percent, respectively. In January, the largest decreases in job openings were in construction (-240,000), accommodation and food services (-204,000), and finance and insurance (-100,000). The number of job openings increased in transportation, warehousing, and utilities (+94,000) and in nondurable goods manufacturing (+50,000). (See table 1.)

Hires

In January, the number and rate of hires changed little at 6.4 million and 4.1 percent, respectively. Hires changed little in all industries. (See table 2.)

Separations

Total separations include quits, layoffs and discharges, and other separations. Quits are generally voluntary separations initiated by the employee. Therefore, the quits rate can serve as a measure of workers’ willingness or ability to leave jobs. Layoffs and discharges are involuntary separations initiated by the employer. Other separations include separations due to retirement, death, disability, and transfers to other locations of the same firm.

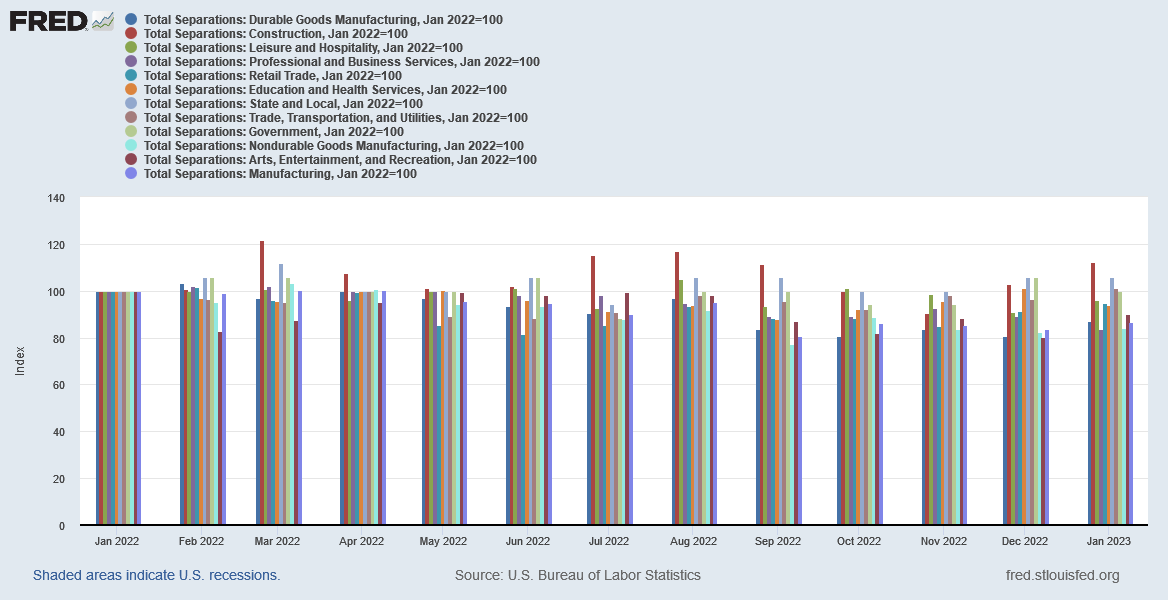

In January, the number of total separations changed little at 5.9 million. The rate was unchanged at 3.8 percent. The number of total separations decreased in federal government (-13,000). (See table 3.)

Thus we have the raw data showing a significant dip in hiring in November and December of last year, and a significant reversal in January—which the seasonally adjusted data nets and smooths out to show the minimal change reported by the BLS.

This means we need to take the JOLTS data with more than a few grains of salt. Significant decreases and increases are surely relevant to what the data reveals about labor markets, and the seasonal adjustment that makes those fluctuations just disappear.

While not as pronounced as with the ADP jobs data, this softening of the JOLTS figures nevertheless is consistent across virtually all economic sectors. Moreover, this particular chart uses the seasonal data, so straight away the possibility of this being a seasonal artifact is largely eliminated.

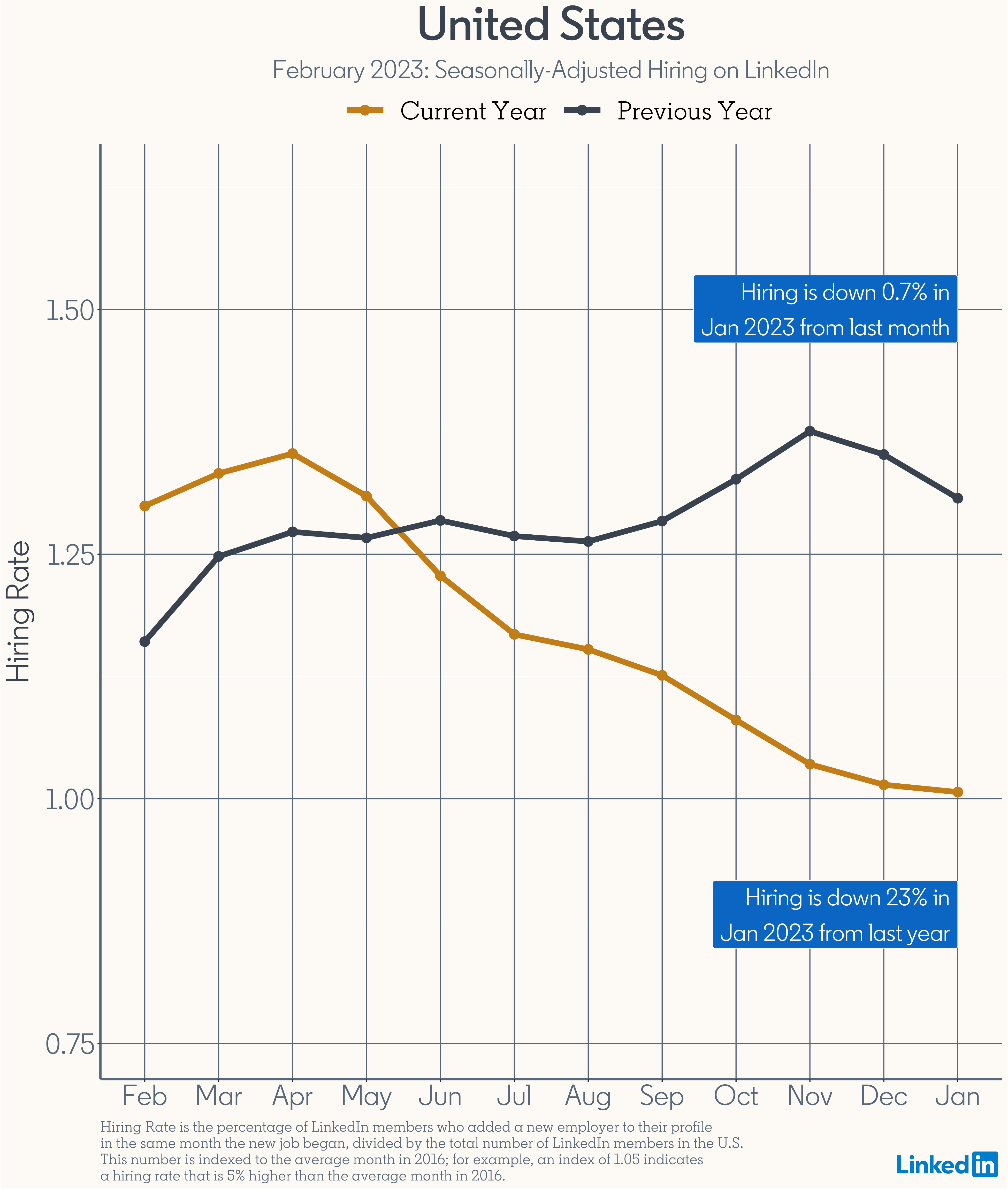

This also dovetails with hiring information from other sources. The LinkedIn Workforce Report for February (detailing hiring trends within the LinkedIn membership for January) actually shows a greater and more persistent decline in hiring than the BLS JOLTS report.

The LinkedIn hiring rate is a measure of hires divided by LinkedIn membership. Nationally, across all industries, hiring in the U.S. was 0.7% lower in January 2023 compared to last month December 2022. National hiring was 23% lower in January 2023 compared to last year January 2022.

No matter how many job openings employers say they have, they are also saying they are hiring less, despite the large number of job openings.

Overall, people are a lot less confident now about changing jobs than they have been. That’s not behavior one expects to see in a “tight” jobs market.

Despite what the official interpretation of the report says, the JOLTS report shows a jobs outlook for the US with measurable deterioration in 2022, deterioration which has not resolved itself so far in 2023. This is not something one expects to see in an economy that is robust and growing.

As is immediately apparent from the comparison between the raw data and the seasonally adjusted data, the need is always to look at the jobs numbers, be they from the ADP employment report or the BLS JOLTS report, with a certain amount of skepticism. The numbers are not as clear cut as the media narratives make them out to be, and the media narrative that presents the jobs data as clear and compelling evidence of a robust and resilient economy only holds up so long as one does not look critically past the headline numbers.

When one does look critically past the headline numbers, signs of weakness and recession are easily seen:

The ADP report shows hiring all but disappearing in the latter half of 2022, with no real improvement in January of 2023.

Both the ADP report and the JOLTS report show significant deterioration in the jobs market throughout 2022.

The JOLTS report continues to show a level of job openings that is not merely wildly inconsistent with the pace of hiring but is historically disproportionate to the pace of hiring.

The year-ending surge in layoffs seen in the JOLTS report runs completely counter to any narrative of companies actively looking to fill record numbers of jobs.

The headline numbers might appear strong and robust, but compared to the detail underneath, that is merely a facade easily penetrated. A mere moment’s scrutiny of the details is sufficient to see that both reports are substantially less positive than the headline numbers appear to be.

It has ceased to be surprising that the corporate media does not engage in such critical thinking. The “official” narrative is that the economy is strong and the jobs market is “tight”, and the corporate media are simply refusing to challenge that narrative.

Yet it has also ceased to be surprising that the underlying data simply does not reconcile to that narrative. The economy is far less robust than the narrative presents, and the jobs market is far more “toxic” than “tight”, and the corporate media are simply refusing to do the fairly straightforward analyses which immediately bring these realities to light.

The constant caveat on all narratives applies doubly so to that on jobs and the US labor market: handle both the ADP Employment Report and the BLS JOLTS report with care. Regard the headline numbers with an extra dose of skepticism, and recognize that beneath those seemingly positive headline numbers are details with a considerable amount of economic negatives.

Trust nothing. Verify everything.

All Facts Matter is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber. Alternatively, please consider leaving a tip through Ko-Fi. Thank you always for your support!

Hiring is down 23% from Jan 2022 to Jan 2023? How can the mainstream media not acknowledge that fact? I swear, true journalism is dead, except for independent thinkers like you!

Hiring is down 23% from Jan 2022 to Jan 2023? How can the mainstream media not acknowledge that fact? I swear, true journalism is dead, except for independent thinkers like you!