Interest Rates And Recessions

Some Observations On Interest Rate Dynamics Leading Into Recessions

Economists and financial market pundits enjoy spinning various market metrics into predictive tools of when the economy is about to tip into recession. How well any of these actually work is a matter of much debate and much conjecture.

However, there is one dynamic that, for the past fifty-plus years, has been positively correlated with contractions in real gross domestic product—with recession. That dynamic is the yield spread across the entirety of the yield curve.

In periods of normal economic expansion, longer term debt yields (i.e., interest rates), tend to be significantly higher than shorter term debt yields

However, ever since 1970, each time the economy has tipped into a contractionary phase, yield spreads have collapsed, with short term debt yields frequently exceeding longer term yields (an inversion phenomenon for the yield curve), but only by a few basis points, where as normal spreads tend to be by larger amounts—500bps or more.

For clarity, here is the same yield spread across the spectrum of Treasury debt from 1967 forward, without the highlights included above.

Inversions along the yield curve are easily understood to be red flags regarding economic outlook, as they indicate a negative prevailing perception of the short-term economic situation relative to the longer-term. Things are believed to be bad right now and in the near future, and better farther along.

The narrowing of the yield spread also is readily understood as a leading indicator of a deteriorating economy. Rising interest rates are reflective of increased interest rate risk on debt securities, which indicates greater uncertainty about future economic conditions both in the short and longer terms. As the uncertainty rises in the shorter term, it becomes indistinguishable from the uncertainty which is naturally associated with longer term debt securities.

When we overlay a graph of Real GDP growth for the same time period, we see that, right after a yield spread collapse, Real GDP tends to contract, meaning there is a recession.

Given the collapse in yield spreads since the Fed began hiking the Federal Funds rate, what does this tell us about the current state of the economy?

Real GDP contracted in the first two quarters of this year. During that same period, while yield spreads did not “collapse”, during that period of GDP contraction there was clear tightening of yield spreads, with the total spread shrinking from 195bps in October of last year to 72bps in April of this year.

Moreover, yield spreads have continued to tighten as the Fed has raised rates, suggesting that, even though Real GDP increased in the third quarter, the recession is far from over.

While tighter spreads within Treasury debt appears to be indicative of an ongoing or impending economic contraction, greater yield spreads with other forms of debt appear to be the recessionary indicator. During the 2001, 2008-2009, and 2020 recessions, yield spreads between corporate debt (AAA and BAA ratings levels) rose during periods of recession, and in particular during the 2008-2009 and 2020 recessions, where the rise in yield spreads was significant.

With yield spreads between both corporate debt and mortgage debt, relative to Treasury yields, continuing to rise, we again are faced with an indicator suggesting that, contrary to the representations of the Federal Reserve and Wall Street, the US economy is already in recession, making any notion of a “soft landing” where the economy does not go into actual contraction completely absurd at this point, as the extant data has already mooted the question.

Rising spreads between various forms of non-Treasury debt and 10 Year Treasuries also speaks to a rising risk premium attaching to various forms of credit within the US economy. Overall, credit is tightening across the economy, and at a pace greater than that indicated by the rise in Treasury yields alone.

Tighter credit helps to explain why banks are seeing a general drop in loan demand of late.

Tighter credit conditions are diminishing the appetite for loans and broader use of credit across the economy, and is impacting both consumer and corporate loan demand. The yield spreads and overall interest rate data admit of no other explanation.

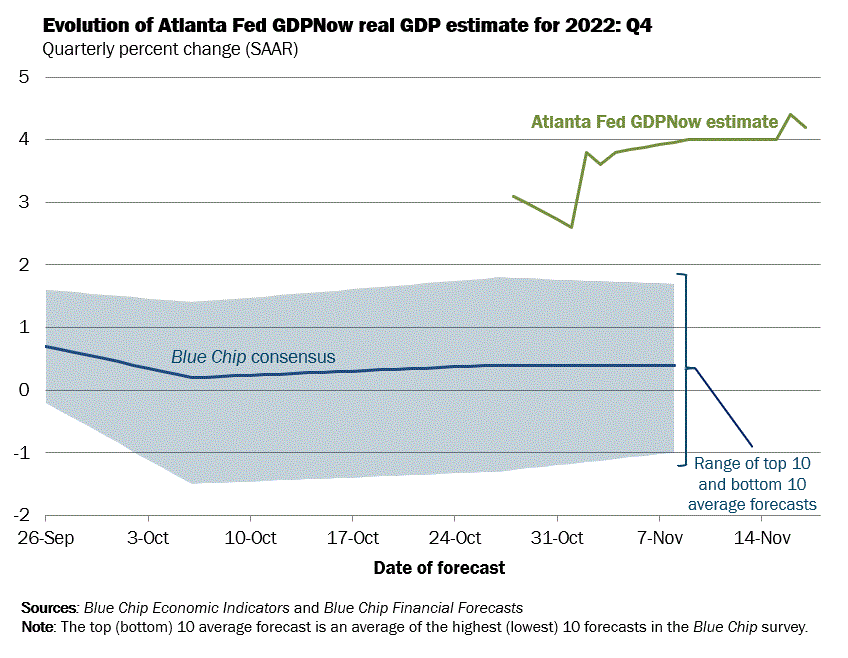

Which brings us back to a point that must be mentioned yet again—the very bizarre insistence of the Atlanta Fed that the US economy is growing at an annualized rate of 4% during this current quarter.

The Atlanta Fed’s GDPNow nowcast, in charting an increasingly robust economic performance this quarter has pointed to a variety of factors, many of which revolve around increased consumption, even as commercial and residential investment declines.

Yet with inflation continuing to erode real earnings, and a general tightening of credit across the economy, the question arises of how is the reported increased consumption being funded? Does the rising trend of credit card accounts where only the minimum monthly payment is being made indicate that consumers are funding this increased consumption with by leveraging increasingly expensive credit card debt, which in turn they are increasingly unable to fund properly?

Such use of credit card debt is hardly an indicator of a robust economy experiencing robust growth, but of a shaky economy with consumption resting on an increasingly unstable and unreliable foundation.

Increasingly, the depictions of the US economy as not in recession are becoming the clear outlier, and the signs of economic weakness and contraction are multiplying, with recessionary signals flashing just about everywhere. Collapsing yield spreads among Treasury debt, and rising yield spreads between Treasury debt and all but the best AAA corporate debt are merely the latest red flags waving in the economic headwinds into which we are heading.