July CPI Print Awash In Surprises And Contradictions

Sudden Drop In Consumer Price Inflation Catches Everyone By Surprise--Including Me

My planned commentary on July’s Consumer Price Index Summary had been centered on the possibility of the Federal Reserve hiking interest rates by a full percentage point in September. Given my presumption as of Tuesday that inflation would come in around 9.3%, this morning’s CPI print putting consumer price inflation for July at 8.5% year-on-year was quite the shocker.

The all items index increased 8.5 percent for the 12 months ending July, a smaller figure than the 9.1-percent increase for the period ending June. The all items less food and energy index rose 5.9 percent over the last 12 months. The energy index increased 32.9 percent for the 12 months ending July, a smaller increase than the 41.6-percent increase for the period ending June. The food index increased 10.9 percent over the last year, the largest 12-month increase since the period ending

May 1979.

Nor was I alone in overestimating consumer price inflation: according to a survey by Bloomberg, a consensus of economists forecast inflation coming in at 8.7% for July. The Cleveland Federal Reserve’s CPI Nowcast projected July’s year-on-year inflation rate to be 8.8%.

This was the first time in eight months the CPI nowcast aimed too high rather than too low.

Suffice it to say, no one was expecting inflation to drop this far this fast.

Not Everything Dropped

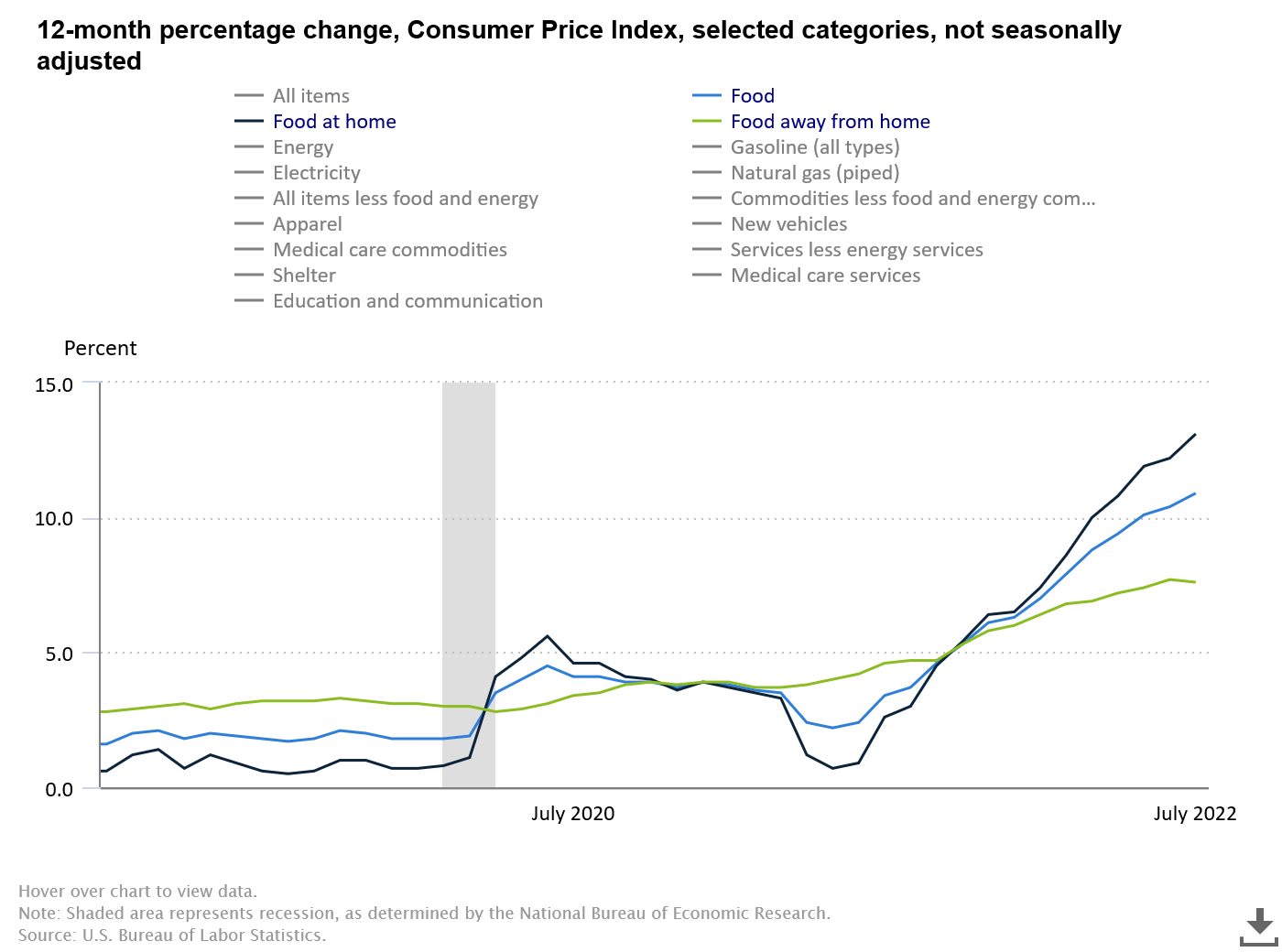

It is important to note once again the distortion that inflation inflicts on an economy. Even as overall consumer price inflation dropped by 0.6%, food price inflation actually increased—to the highest level in forty years.

The food price inflation picture gets even worse; food purchased for consumption at home—groceries—rose even higher tha overall food price inflation—while inflation for food eaten away from home (restaurant meals, et cetera) actually declined. It is becoming cheaper to eat out than it is to eat at home.

Thus, while overall inflation got better, one of the most crucial components of the Consumer Price Index—food—experienced some of the worst inflation in decades.

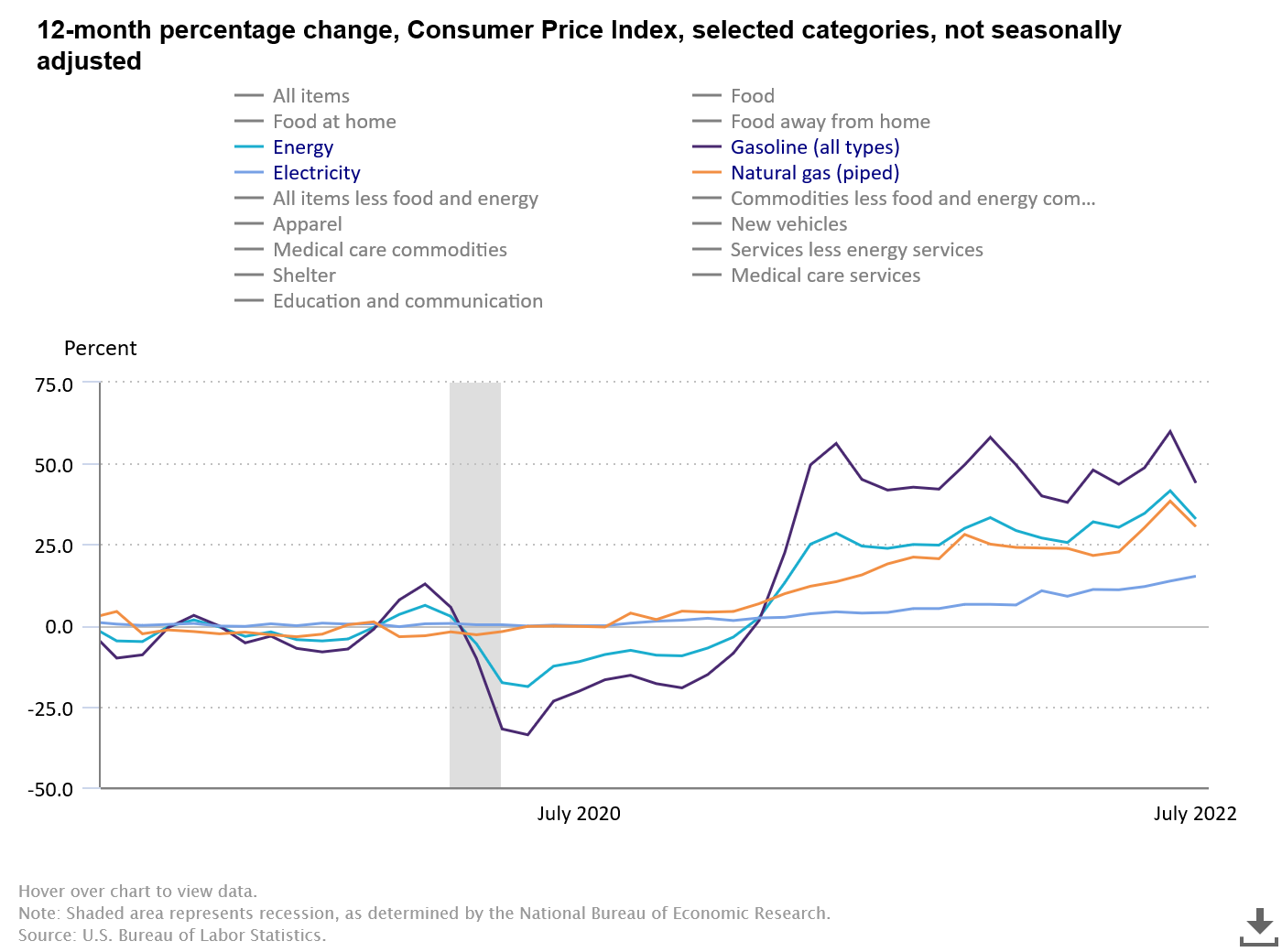

On the other hand, energy price levels moderated and even declined during July—although energy price inflation year-on-year remains extremely and distressingly high.

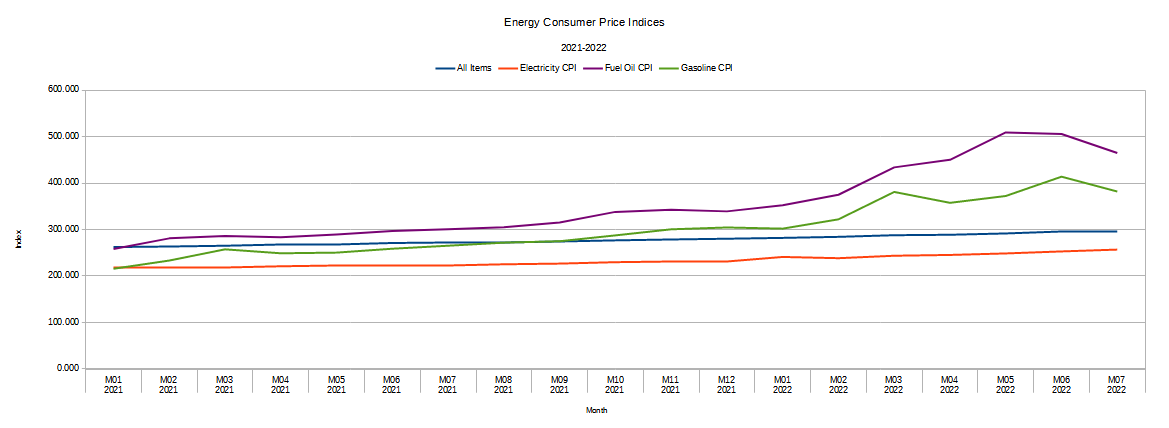

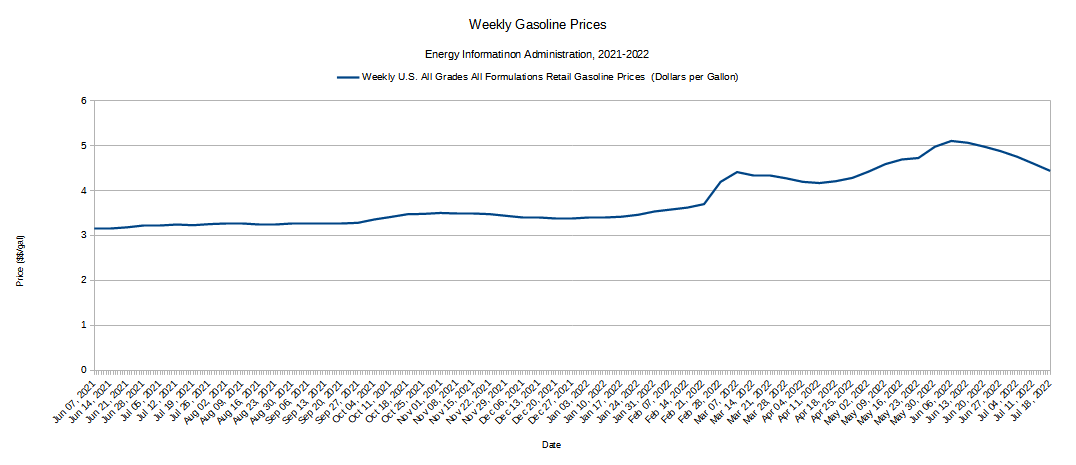

While energy prices are considerably higher than a year ago, gasoline and fuel oils posted monthly declines, with gasoline dropping 7.7% from it’s June levels.

Putting these price shifts in a more real-world context, the Energy Information Administration showed the price of a gallon of gasoline falling $4.879/gal during the first week of July to $4.44/gal during the last week.

Despite the monthly decline, however, the EIA’s average gasoline price reflects the reality that gas prices are considerably higher than in July of 2021.

Thus, even the undeniably good news of energy price declines during July must be tempered by the realization of how far prices had risen during the preceding 12 months.

Peak Inflation?

One question upon which much of the corporate media commentariat remains justifiably focused is whether or not the US has finally reached “peak” inflation, after which inflation rates should begin trending downward overall. A one month decline, no matter how dramatic, is not enough data to form an actual trend, so it is far too soon to tell if inflation is finally heading back down to (hopefully) pre-pandemic levels.

However, a recent survey by the New York Federal Reserve does show that consumer expectations are for lower inflation in the future.

Median one- and three-year-ahead inflation expectations both declined sharply in July, to 6.2% and 3.2% from 6.8% and 3.6% in June respectively. Both decreases were broad based across income groups, but largest among respondents with annual household incomes under $50k and respondents with no more than a high school education. The measures of disagreement across respondents (the difference between the 75th and 25th percentiles of inflation expectations) increased at the one-year-ahead horizon and decreased noticeably at the three-year-ahead horizon.

If June was not peak inflation, at a minimum consumer expectations are that we are very close to that peak.

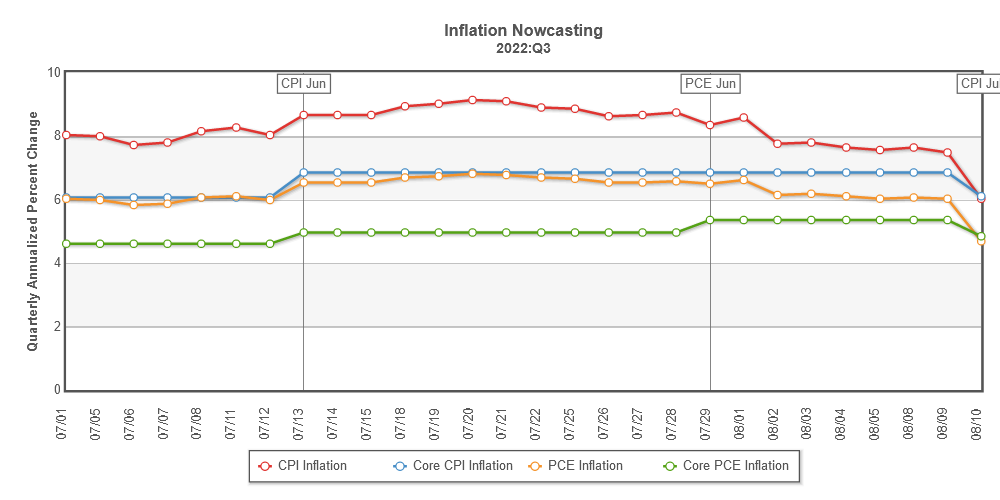

The Cleveland Fed’s CPI nowcast is currently charting lower inflation both for August and the third quarter of 2022 more broadly, with declines occuring in all inflation indices.

While the CPI nowcast has proven itself not to be the most reliable barometer of future inflation, if the current forecasting trend holds true, the possibility that we have finally gotten past peak inflation in this country becomes considerably stronger.

With any luck, while we are by no means near the beginning of the end of the inflation saga in this country, there is reason to hope we have finally reached the end of the beginning.

Future Inflation Threats

By far the largest determinant over whether we have seen peak inflation, or whether there will be further inflation shocks down the road, is the likelihood of future supply disruptions and dislocations such as those initially occasioned by the lunatic lockdowns over COVID and, most recently, over the Russo-Ukrainian War.

Will there be future supply shocks? Potentially, yes.

While some supply-chain issues may have moderated or been resolved, not all of them have, and some may even get worse. For example, the global shortage of semiconductor computer chips is still very much the present reality, and has not been resolved at all.

Shanton Wilcox, U.S. manufacturing lead at PA Consulting, thinks that supply chain issues are not easing. Instead, they have been overshadowed by the media headlines by inflation and gas prices. He cited U.K. car sales falling 9% in July, while Toyota and Lucid lowered production targets due to supply chain issues like plant shutdowns in China and the ongoing chip shortage.

“The chip shortage also caused Nintendo to miss its forecast for the Switch console," Wilcox said. "There are warnings from utilities in Florida that recovering from a hurricane this year may take months to even a year as manufacturers of transformers and other components have historic backlogs and are even declining new orders."

Additionally, while container ships bringing imported goods to America’s shores are spread across more ports, the net effect of that disbursal has been largely to spread the container ship backlog across those additional ports. In the aggregate, the container ship backlog in US ports is as bad as it has ever been.

In January and February, when North American congestion previously peaked, there were just under 150 container vessels waiting off the coastlines. Two-thirds were in the Los Angeles/Long Beach queue.

As of Thursday morning, there were 153, the majority off East and Gulf Coast ports. Whereas the earlier West Coast pileup was centralized, highly publicized and relatively easy to track, today’s ship queue is more widely disbursed and attracting less attention.

A new peak in port congestion during July is a strong signal of a coming shortage across a wide range of consumer goods—most if not all of which fall into the category of “core CPI” and thus reflect “core inflation” (CPI ex food and energy), which had declined during the month of July.

Additionally, while gasoline prices may be trending down, rents and shelter costs are still trending up.

Median rent payments for Bank of America customers increased by 7.4% year over year in July, a slight pickup from 7.2% in June. Increases were seen across all income groups, but middle-income and younger Americans saw the largest increases, the report said.

Thus despite the unexpected drop in inflation for July, supply chain and other pressures remain lurking in the background, and are likely to continue to exert upward pressure on prices for the foreseeable future. It remains quite possible that peak inflation has yet to be reached.

The Economy Remains Broken

While July’s CPI print is a most welcome relief from unrestrained inflation, it does not change the distressing reality that the US economy—and the world economy as a whole—remains fundamentally broken. Not only is inflation continuing to distort prices both here and abroad, but labor markets remain fundamentally dysfunctional, despite the government’s efforts to paper that over with heavy uses of Lou Costello Labor Math. Inflation has already inflicted lasting damage to US manufacturing, as cost pressures have forced plant closures in several industries. One month’s decline in headline consumer price inflation does not ameliorate any of this.

The July Consumer Price Index Summary shows some prices in the US have stopped rising, although some price increases have gotten even worse. While consumers no doubt welcome falling gasoline and energy prices, rising food and shelter prices continue their assault on the average American’s wallet.

Inflation may have slowed down a little in July, but it has not stopped. As the second half of 2022 unfolds, inflation is poised to continue spreading its toxic effects throughout the economy. The inflation saga is by no means anywhere near its conclusion.

There's such a disconnect, grocery shopping is painful and real world inflation in my cart is 30-65% and filling the car is also 50% more expensive, and companies are laying off. I'm glad markets are up, some say Bull has begun, but so detached from reality. It feels like climbing up one of those Drop Tower amusement rides and waiting for the big drop.

Great analysis.