May ADP Jobs Report: From Jobs Recession To Jobs Recovery?

ADP Report The Latest In Growing List Of Jobs Recovery Signals

Could we really be seeing the end of the years-long jobs recession in this country?

The May ADP National Employment Report presents a case for a nascent jobs recovery that is difficult to ignore, with a jobs print showing 122,000 jobs were created last month.

It certainly is difficult to challenge ADP Chief Economist Dr. Nela Richardson’s assessment of the report.

Hiring was more broad-based in May than we’ve seen in the last few years. The labor market continues to show sustained momentum going into the summer hiring season.

The report surpassed Wall Street’s increasingly optimistic consensus projection, and completely blew pass the Trading Economics forecast.

Another encouraging note: ADP’s revisions to the April report amounted to a relatively minor reduction, from 109,000 jobs to 105,000 jobs—still a strong headline jobs figure.

Is the jobs recession really over? At the very least we must acknowledge the increasing number of signals that it is.

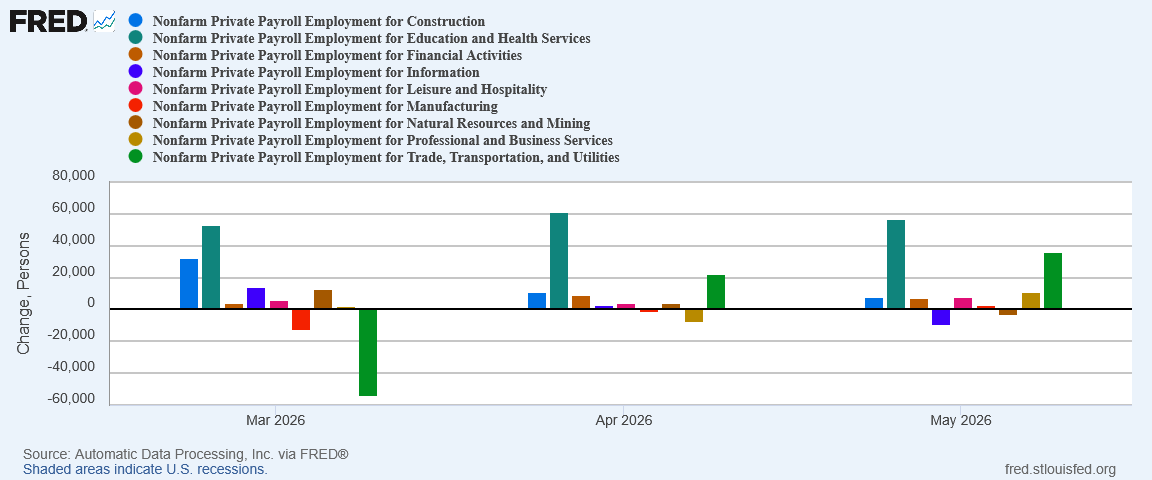

Across The Board Growth

What makes the ADP report compelling is not merely that there was broad based jobs growth, but that there is a growing trend of broad-based jobs growth. May was the third consecutive month that nearly all jobs sectors showed at least some employment increase.

Aside from the March bloodbath in Trade, Transportation, and Utilities, the ADP report has shown job growth across most every sector.

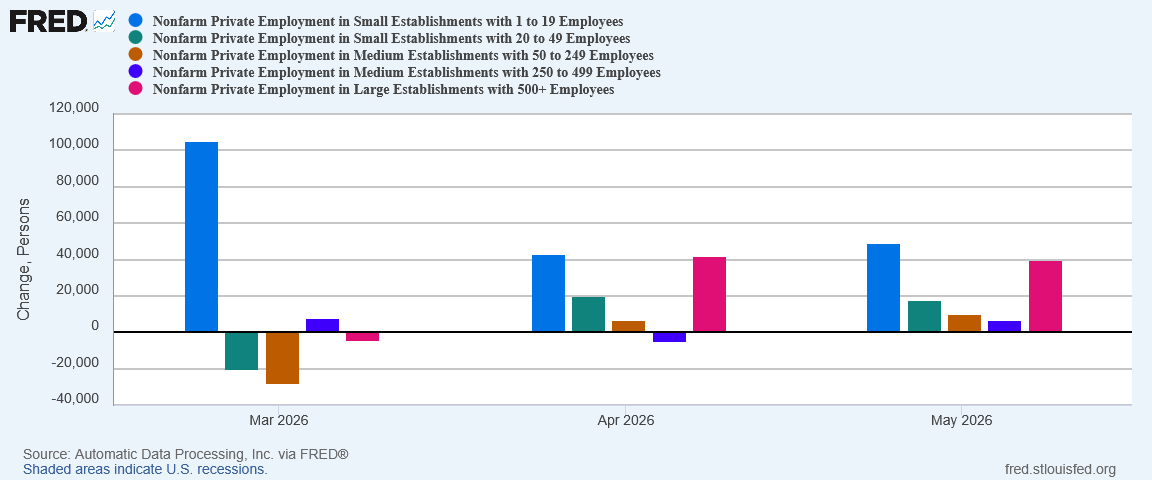

Equally encouraging is that job growth has been spreading across all employer sizes.

In March, job growth was almost exclusively concentrated in small establishments. In May, while small establishments still led the way, larger firms are also adding jobs.

Just on these two metrics alone we can say that the ADP report is a strong signal that a jobs recovery is underway, with jobs growth that is both broad and increasingly deep.

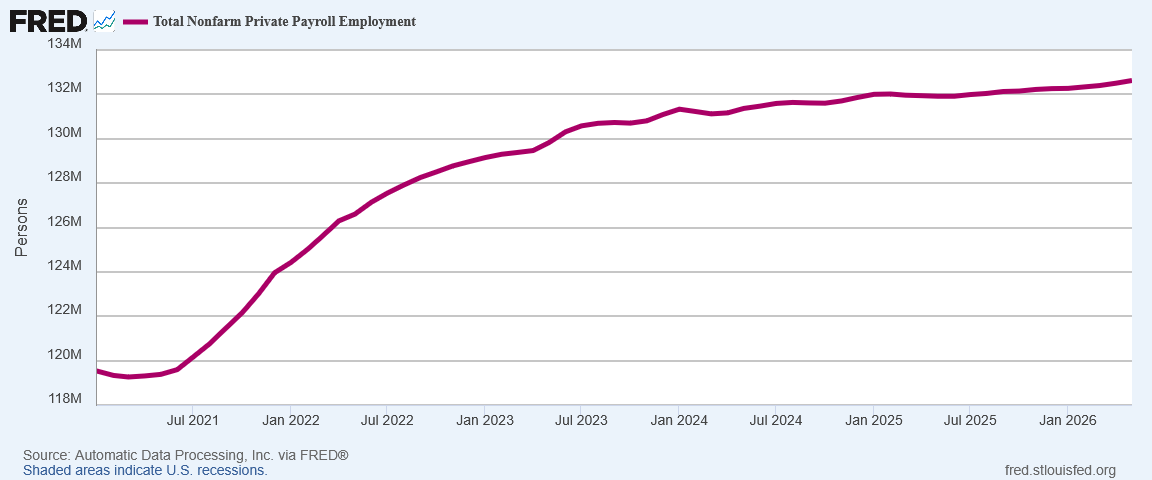

Stepping back and looking at a longer horizon, the ADP data also suggests that the pace of job growth has been trending up in recent months.

After the expected rebound in employment in 2021 following the 2020 COVID Pandemic Panic, job growth slowed markedly especially in 2023 and 2024. The first few months of 2025 even showed some job loss. Since last summer, however, the ADP data has been charting consistent job growth, and larger monthly jobs numbers since earlier this year.

There is no denying that this is what the beginnings of a jobs recovery looks like.

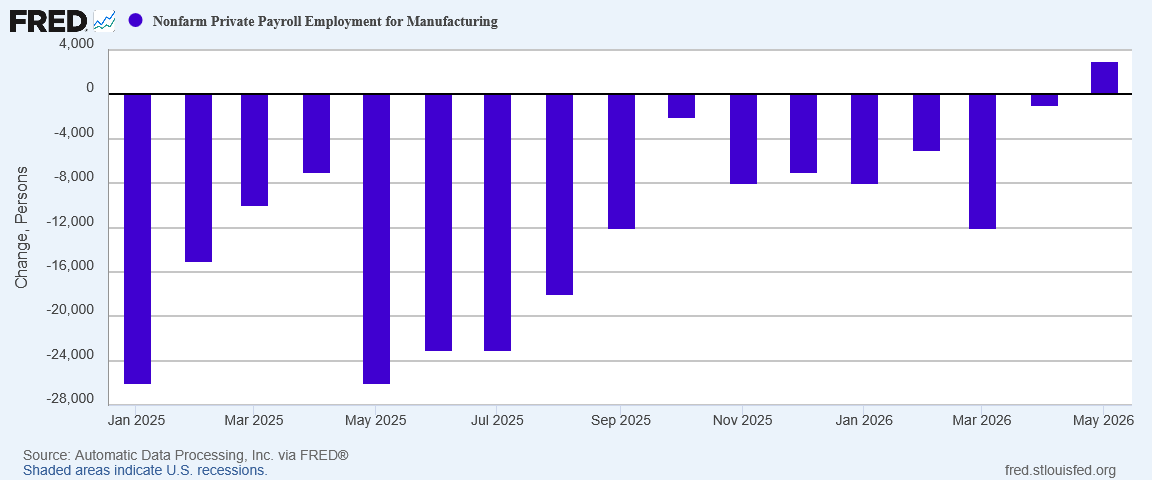

Manufacturing Job Growth…Yay!

As longtime readers are aware, the manufacturing sector is one to which I pay particular attention when assessing jobs numbers. Not only do manufacturing jobs generally pay more, but manufacturing employment is essential for President Trump to realize his Agenda 47 goal of making the United States a “manufacturing superpower.”

The past few years have not been kind for manufacturing. It is particularly good news, therefore, that the May report showed the first positive jobs print for manufacturing in two years.

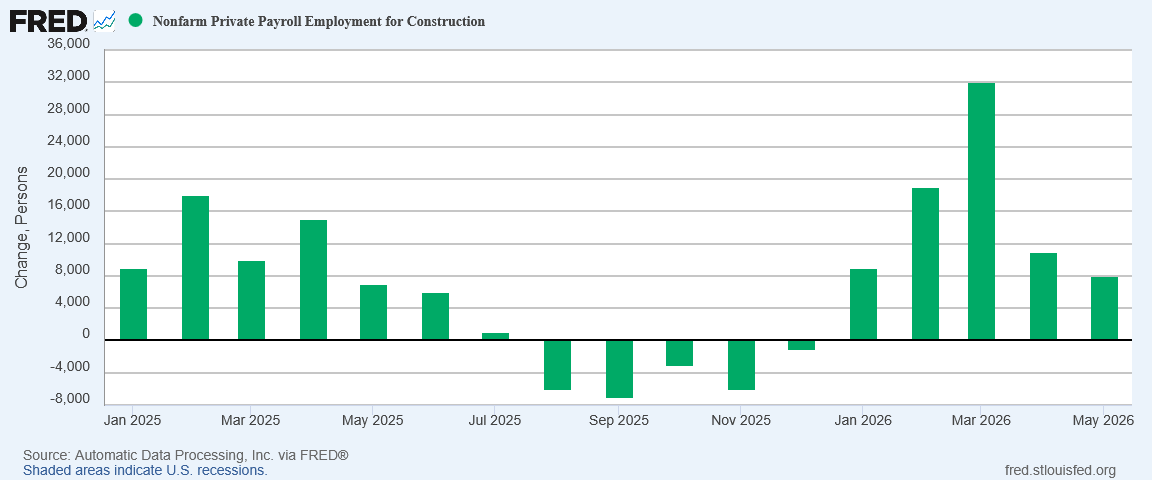

Construction job growth continued, although it showed further cooling from April.

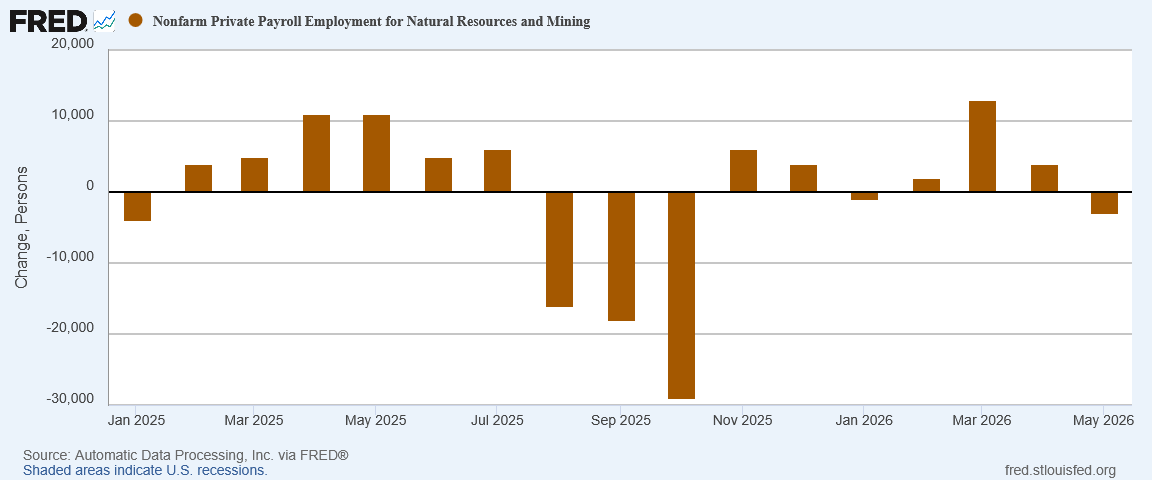

Among goods producing jobs, only Natural Resources and Mining showed job loss.

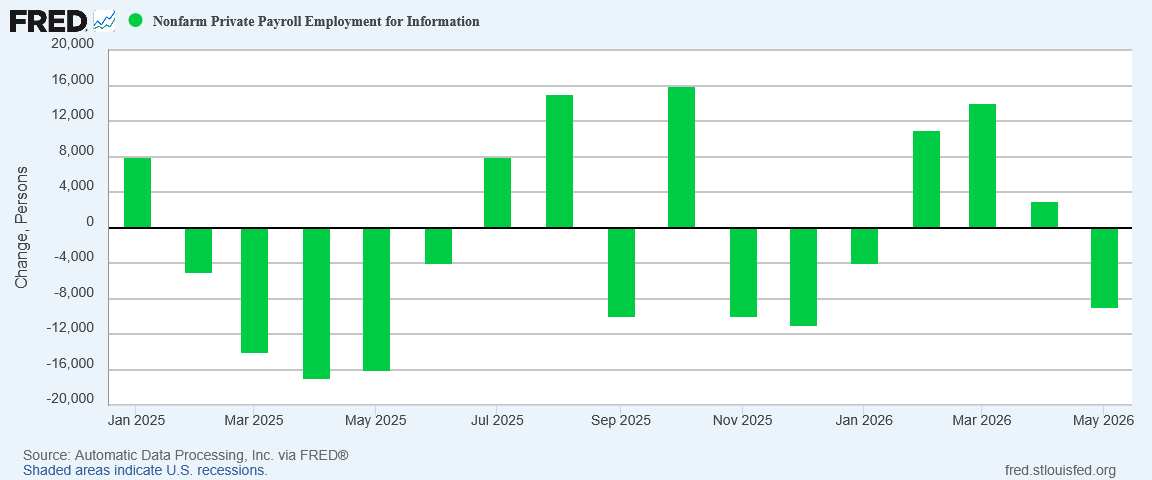

Among service providing jobs, only the Information sector showed job loss.

Professional and Business Services, Trade, Transportation, and Utilities, Healthcare, Finance, and Leisure all showed some level of job growth.

Not only did all but two sectors print job growth in May, but even sectors that have been shedding jobs in recent months are now picking up jobs. Information is the lone standout in this regard, as it had been showing job loss more often than not since the start of 2025.

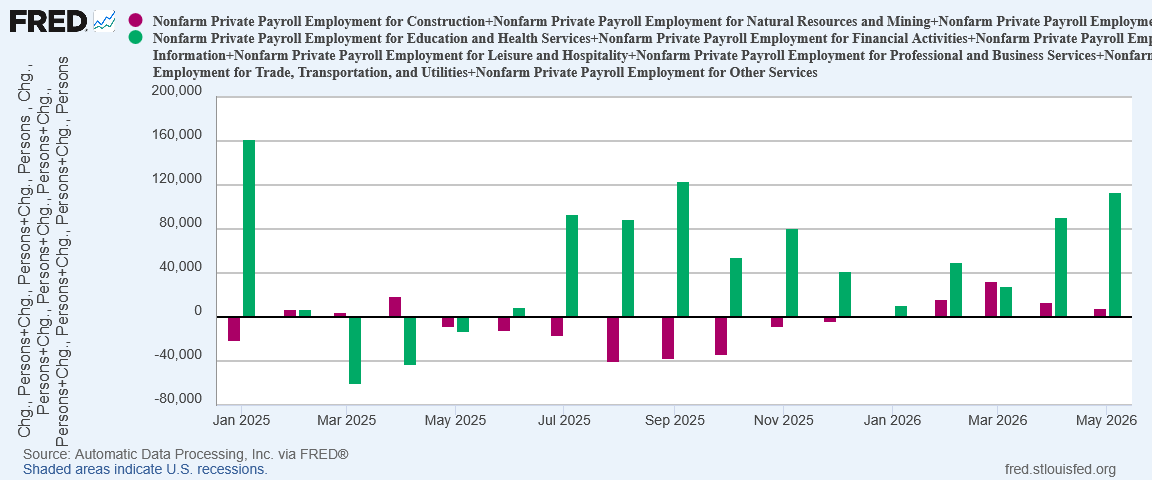

Service providing jobs grew substantially more than goods producing jobs. Perhaps more significantly, service providing jobs have been on the upswing in recent months, even as goods producing job growth has cooled somewhat.

I have said before that sustained broad job growth was needed before we could say with confidence that the jobs recession has ended. The May ADP jobs report printed sustained broad job growth.

Unemployment Trending Downward

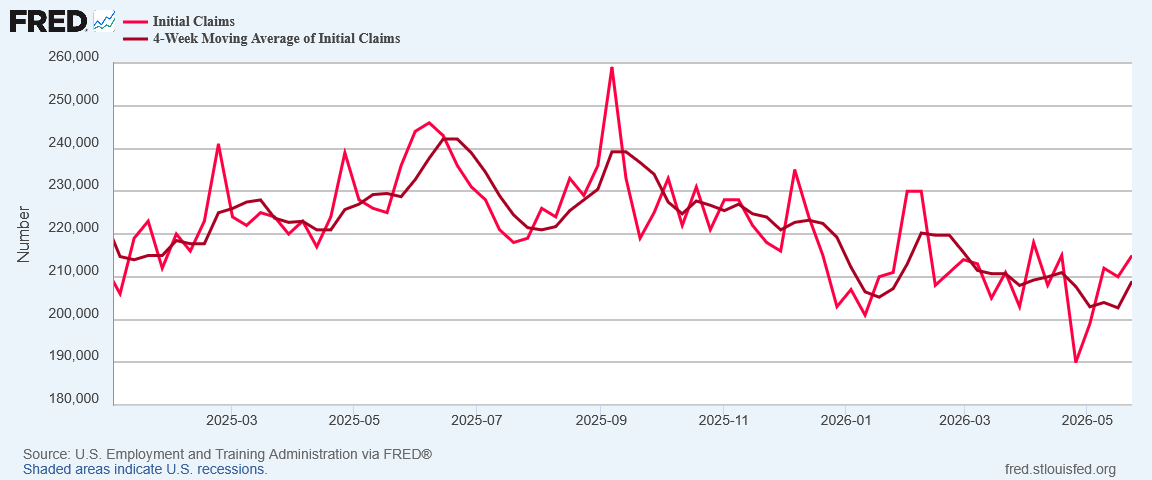

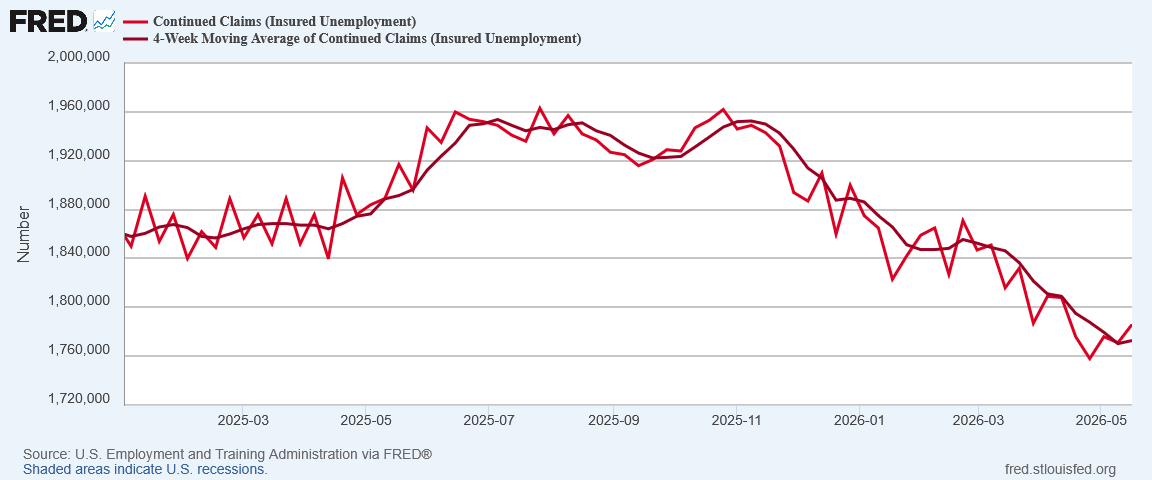

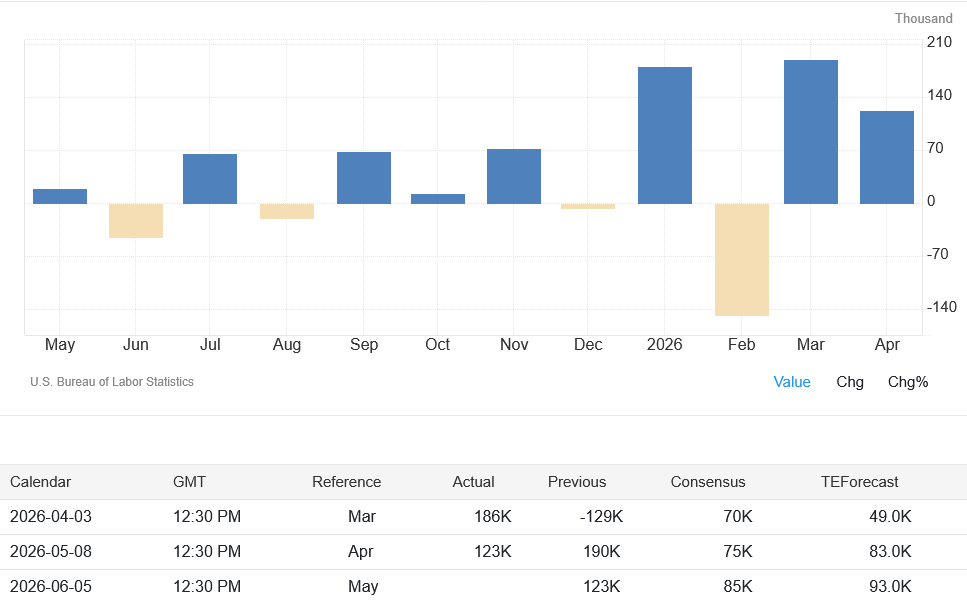

When we look outside the ADP report to the weekly unemployment claims data, in both initial and continuing claims we are seeing a downward trend that points to steady improvement in the unemployment outlook.

We do need to apply some caveats to the unemployment data. Not only has the claims data moved up in recent weeks, but the longer-term unemployment picture from the BLS Employment Situation Summary is still showing rising joblessness dating back to mid-2023.

The ADP report is printing strong jobs growth and is clearly signalling a jobs recovery is underway, but that recovery is unquestionably in its early stages, and it is still extremely fragile. A negative jobs Employment Situation Summary report, or even an underperforming one, would be a serious challenge to a jobs recovery narrative.

The May Employment Situation Summary comes out on Friday. Whether the BLS data confirms or rebuts the ADP data will go a long way towards solidifying or weakening the case for a jobs recovery in this country.

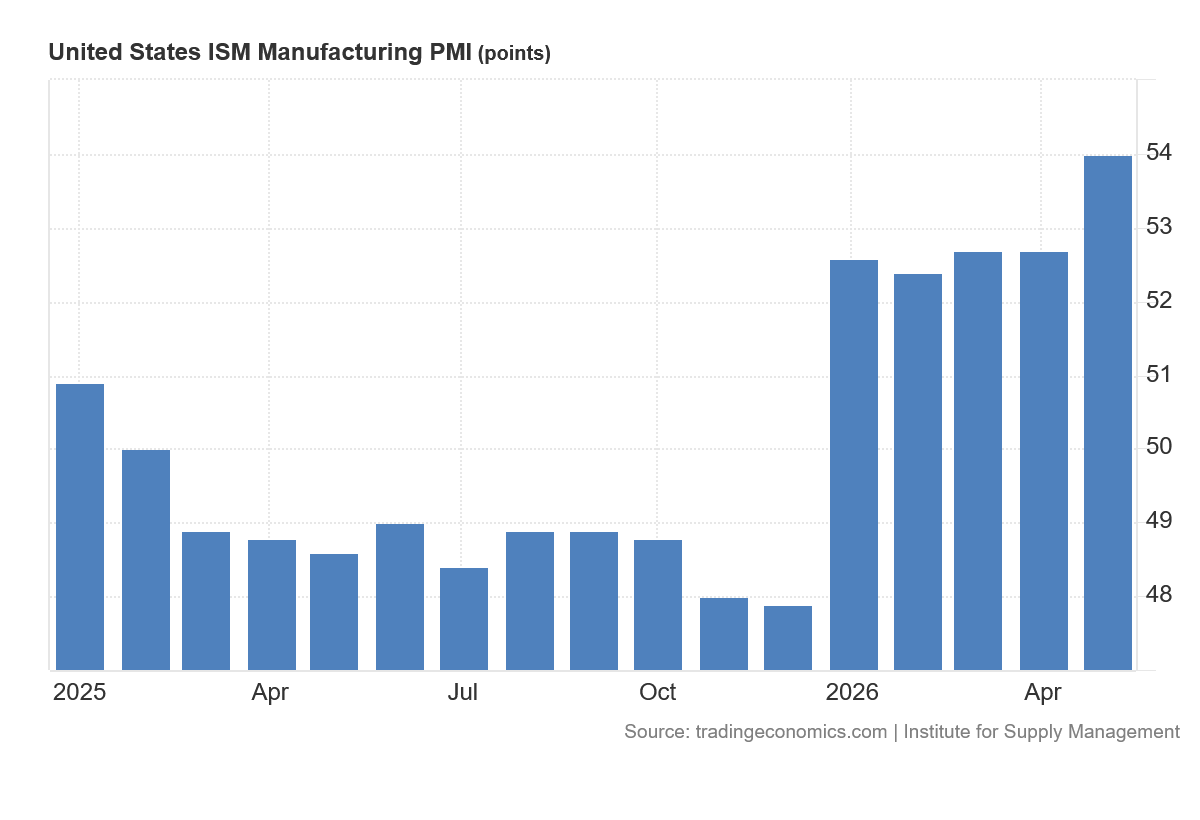

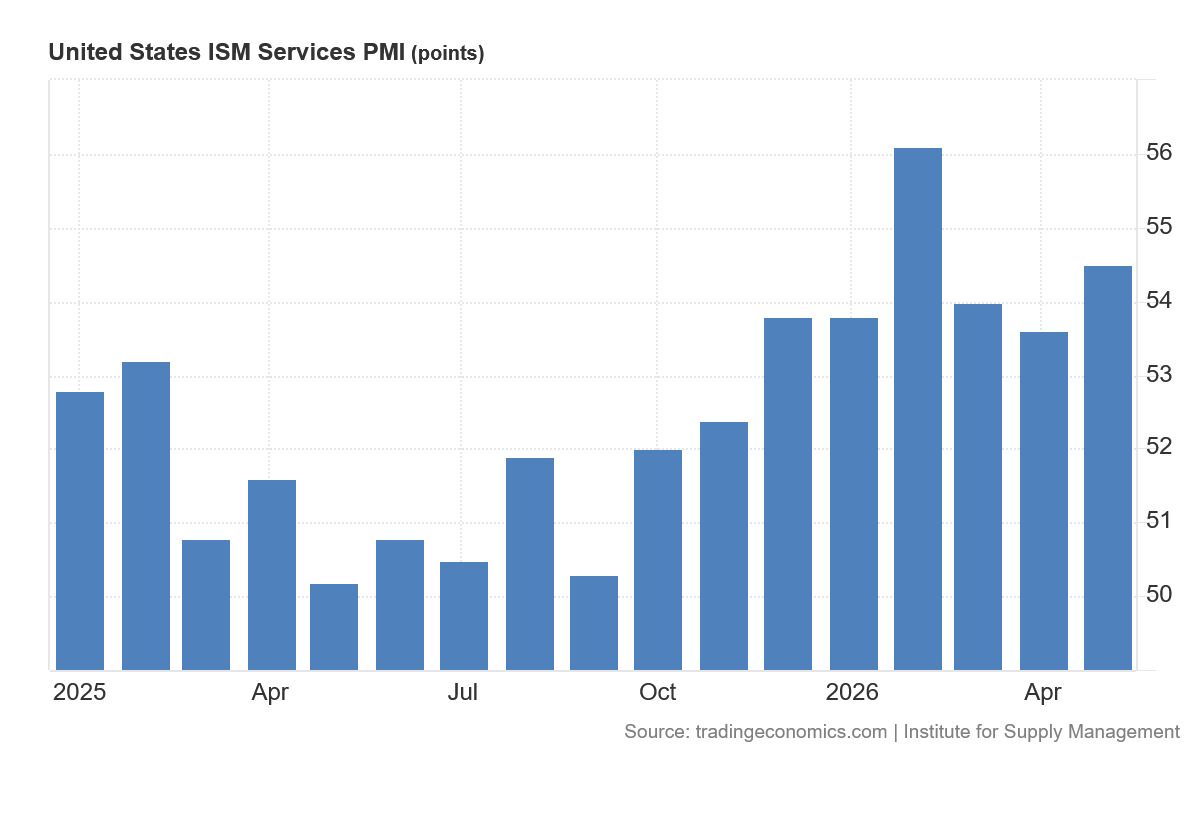

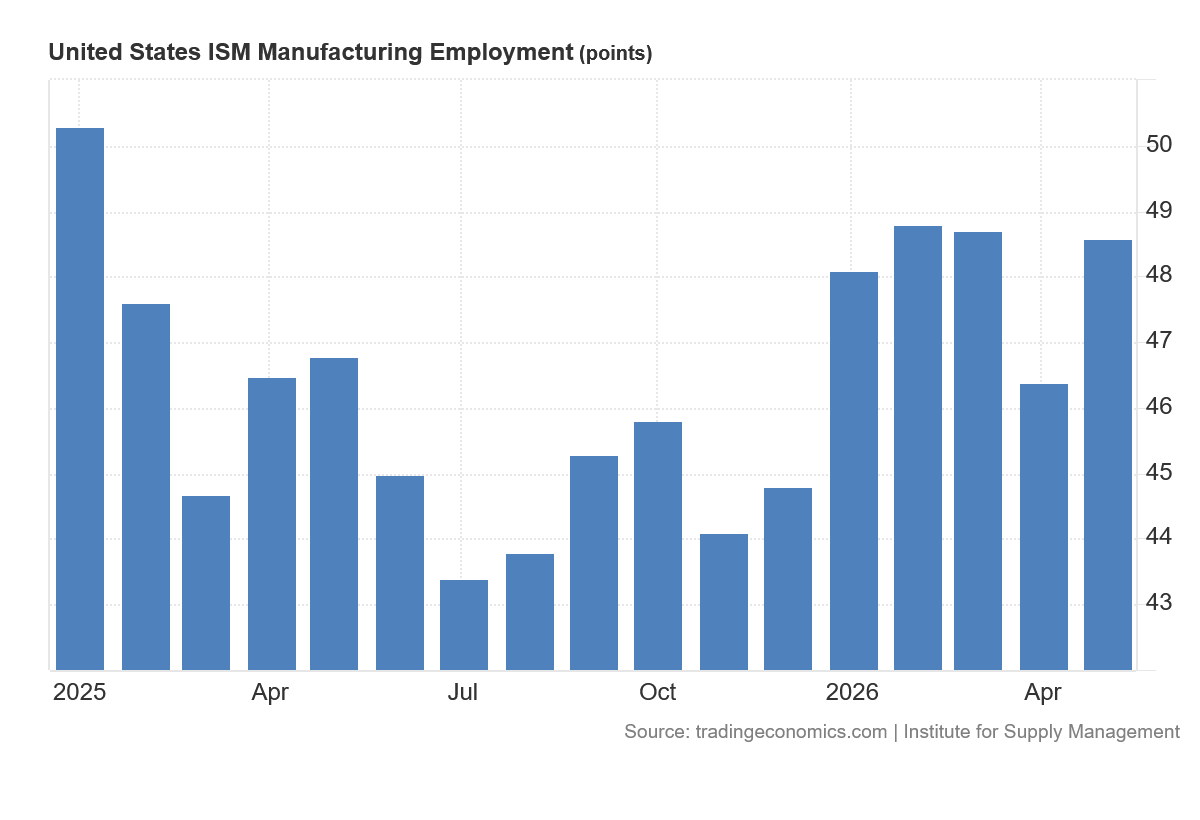

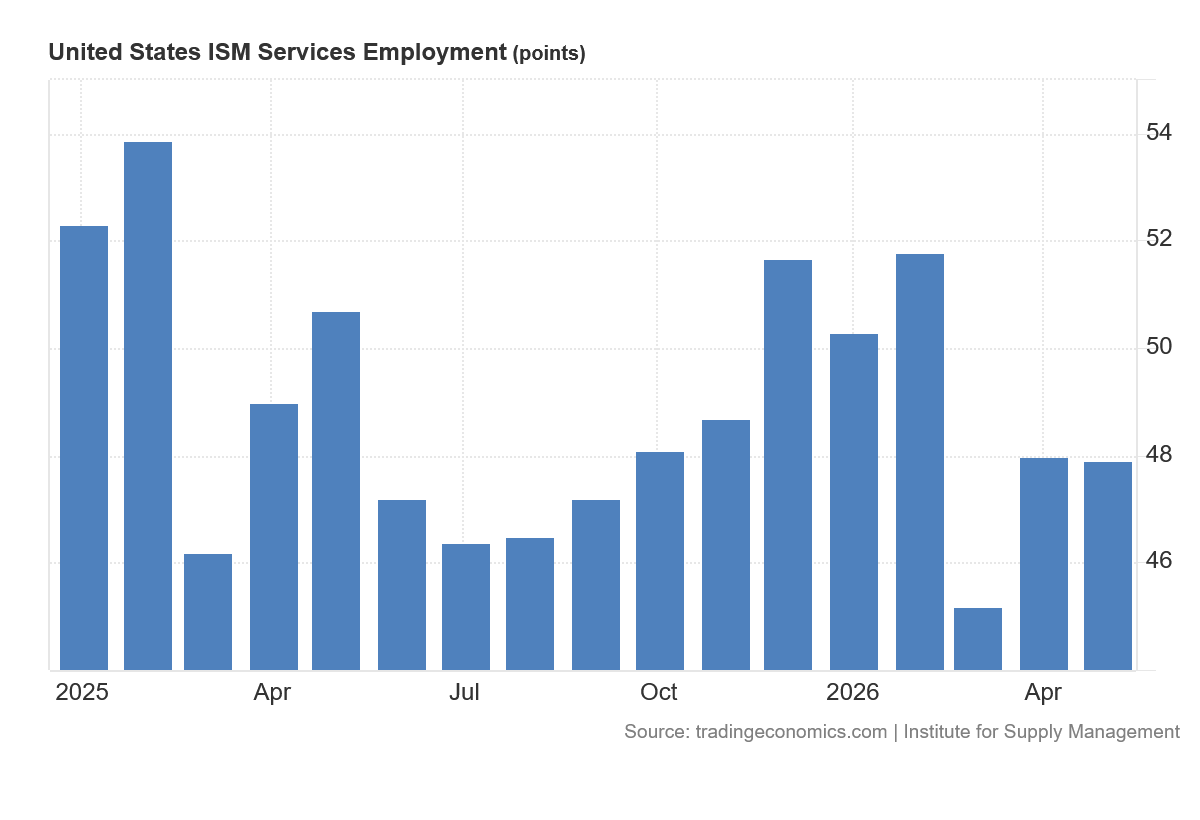

PMI Data Still Invites Skepticism

As noted the other day, the PMI data from the Institute for Supply Management is both a case for a jobs recovery and a case against it.

The case for is that both the Manufacturing PMI data and the Services PMI data have been printing expansion since the first of the year.

The case against is that both Manufacturing Employment and Services Employment have been printing contraction.

How can industry surveys be printing job growth on the one hand and employment contraction on the other? If we presume pristine data sets then the answer is clearly that they cannot—one data set or the other must be incorrect.

However, this is also where we have to remember that we do not have pristine data sets, and even ADP has in the past succumbed to the temptations of fudged Lou Costello Labor Math to present rosier metrics than were really warranted.

The ADP data may be highly inaccurate. The ISM PMI data may be highly inaccurate. Both data sets may be inaccurate to varying degrees.

If the job growth trends reported by ADP are real, then in due course we should expect to see the ISM PMI data on employment move into expansion territory. Similarly, if the Manufacturing and Services PMI metrics themselves continue to print expansion, we should expect to see that industry growth percolate down into employment growth.

The longer the PMI employment data shows contraction, the more we should be cautious about accepting the ADP jobs data at face value.

The ADP Report Is A Strong Report

Despite the caveats and precautions, there is no denying that the ADP Employment Report is a strong jobs report. There is no denying that it is the latest in a string of increasingly stronger jobs reports.

On its own, the ADP data is signalling that a jobs recovery is starting to take hold in this country.

Will the BLS Employment Situation Summary due out on Friday show the same strong jobs numbers? Wall Street is guardedly optimistic, with a consensus projection of “only” 85,000 private sector jobs.

In March and April the projections were conservative, and the BLS job prints blew right past them. Will we see the same again for May?

That is, of course, the hope. Labor markets have languished in this country for far too long as it is, and a turnaround is absolutely overdue. A strong jobs report from the BLS, coming on the heels of a strong ADP report, with both reports the latest in a series of strong jobs reports, would be the strongest signal yet that a jobs recovery is finally taking hold in this country, and that it has been for the past few months.

We have more than a few reasons to believe that hope is not in vain. We still have a few reasons to remain somewhat skeptical.

Is a jobs recovery underway in this country? The ADP jobs report is the latest indication that it is.

“…the longer-term unemployment picture from the BLS Employment Situation Summary is still showing rising joblessness dating back to mid-2023.”

Peter, you have shown several times that the BLS produced unreliable - even fudged - data. Are you more confident now in their competence, since Trump took office?

Also, Republicans running for office this year will claim today’s new positive jobs growth data as being the result of Trump’s policies, such as the tariffs that have driven new domestic investment. Maybe there is not conclusive proof yet, but if there is before the midterm elections, I hope you will post the proof? Thanks, Peter!

With the jobs data today, I’m curious if you saw the breakdown in hiring between foreigners and native born Americans?