First we saw red flags galore in commercial real estate, signalling a coming crisis.

Then we saw trouble brewing in bond markets, signs of fund managers unable or unwilling to follow their own market data.

Now comes the news that mortgage rates are spiking to 8%.

The average rate on the popular 30-year fixed mortgage rate hit 8% Wednesday morning, according to Mortgage News Daily. That is the highest level since mid-2000.

The milestone came as bond yields soar to levels not seen since 2007. Mortgage rates follow loosely the yield on the 10-year U.S. Treasury.

Is housing about to make for a financial crisis trifecta? Is the US about to enter a financial “perfect storm”?

There is, of course, no way to say with certainty, but it is nevertheless certain that the signs are there, and the signs are ominous.

In truth, we should not be surprised that mortgages are pushing up towards 8% (and even exceeding 8%, based on Mortgage News Daily data). Mortgage rates generally track longer term Treasury yields (and the 10-Year Treasury yield in particular), which have been rising steadily for the past several weeks.

While the mortgage rates chart a bit more smoothly (as they are released weekly rather than daily), the charts follow the same basic trends as Treasuries.

While Mortgage News Daily reports higher rates than the Freddie Mac rates captured in the Federal Reserve’s FRED system, the MND chart also follows the same trends as the 10-Year and 30-Year Treasury.

MND’s jump to 8% is a bit unexpected, but the overall trend is exactly what should be happening, given where Treasury yields have been heading.

High mortgage rates greatly increase the cost of home ownership, enough so that mortgage applications have been falling as mortgage rates have been rising.

High mortgage rates have dramatically slowed the housing market, since homebuyers have balked at the stiff borrowing costs, and home sellers have opted to stay put with mortgages that lock them into comparatively low rates.

Mortgage applications have fallen to their lowest level since 1996, the Mortgage Brokers Association said earlier this month.

Sales of previously owned homes, meanwhile, plummeted more than 15% in August compared to a year ago, according to the National Association of Realtors. The slowdown has coincided with a sharp rise in costs for potential homebuyers.

Decline in mortgage applications is particularly worrisome, because mortgage applications have been decreasing in more months than they have been increasing since at least the beginning of 2022.

This decline in mortgage applications is also reflected in the Mortgage Market Index, which tracks demand in mortgages.

Since mid-2021, not only has mortgage demand declined, it has positively crashed, reaching the lowest levels since the mid-1990s.

Mortgage demand is lower today—and has been lower—than it was in the aftermath of the 2008 Great Financial Crisis, which was catalyzed by a property bubble here in the United States.

The plunge of mortgage demand into the abyss ties into a larger trend which also encompasses the aforementioned commercial real estate market, that of declining bank credit, which has been trending lower all year.

Particularly in the wake of this past spring’s mini-banking and liquidity crisis, bank credit—the basic benchmark of bank lending activity—has been moving steadily down. Simply put, banks are lending less and less, even as interest rates are rising more and more.

At first glance, this might not be apparent looking at the residential real estate loans (mortgages) banks are carrying on their balance sheets. However, while the total amount of residential real estate loans banks carry on the books has been increasing, the total amount of mortgage backed securities (MBS) has been declining since mid-2022.

What has been happening is that banks are writing mortgages and holding them, rather than securitizing them into MBS tranches. Given the far greater volatility within the MBS portfolios over straight mortgages, the shift confirms the drop in mortgage demand.

The drop in mortgage demand presents another challenge for Wall Street: drop in the value of mortgages and mortgage-backed securities. Once again using relevant Exchange Traded Funds as a proxy for mortgage and MBS market value, we see that these MBS-related funds have been shedding value since 2021 at least.

As with bonds and commercial real estate, rising interest rates tends to erode asset values.

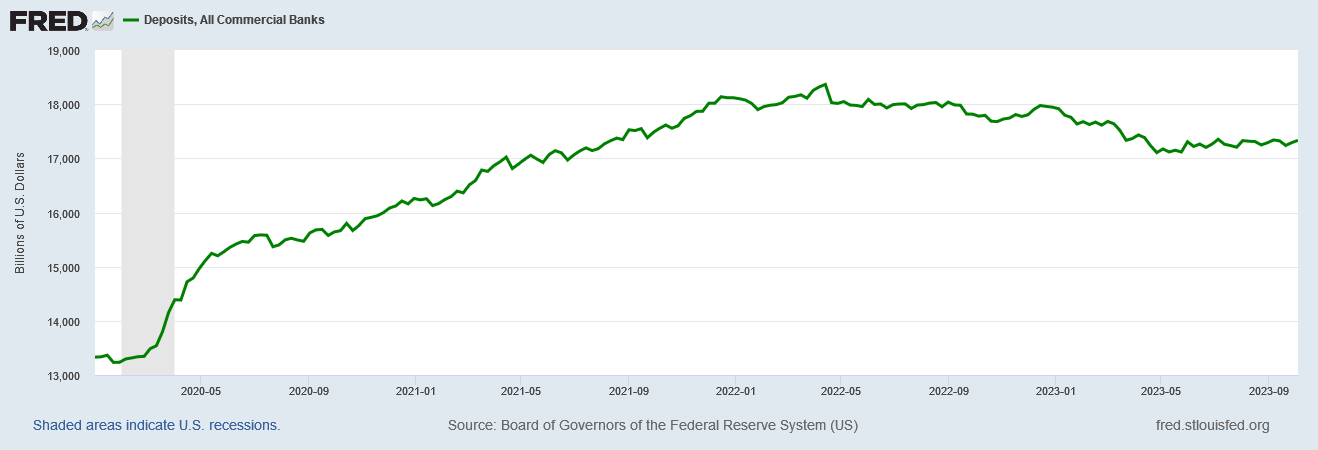

As mentioned previously, these declining asset values have been accompanied by an overall decline in bank deposits. Although bank deposits have largely stabilized, they remain significantly below where they were prior to the Fed kicking off its rate-hike strategy to counter inflation.

If bank deposits decline further, with bank balance sheets losing value through market declines, the banking system could find itself heading into another liquidity crunch, as banks are unable to come up with the cash to satisfy demands of exiting depositors.

Yet it is not merely that mortgage activity is down. Housing starts are also down, which means there going to be fewer homes being held out for sale.

These are the somewhat arcane dynamics of residential real estate in this country, where rising home prices do not automatically result in increased housing starts. As of July the Case-Shiller Home Price Index is at record levels, even though overall home sales are down.

After staging a mini-recovery earlier this year, home sales have now receded to levels last seen just before the 2008 Great Financial Crisis and concurrent Great Recession.

Merely reaching this level does not automatically mean a financial crisis is imminent, yet a decline after having just returned to levels that existed prior to the housing bubble of the early 2000’s does not augur well for the future of residential real estate or the banking activity necessary to support it.

The disturbing picture that is forming within US financial markets is not that of any one part facing imminent collapse. We cannot yet look at mortgage data, or commercial real estate data, or even Treasury yield data and conclude that these sectors are but moments away from a major meltdown.

Rather, the disturbing element is that virtually every facet of investment finance, in particular real estate investment finance, are flashing warning signs. There is considerable instability within commercial real estate, Treasury and bond investing, and now residential real estate. All these weaknesses are ultimately reflected within bank balance sheets and directly impact overall bank health.

Banks’ securities portfolios are shedding value pretty much across the board. Bank loan books are not far behind. Bank credit is contracting. All these trends are happening at the same time. If they all continue long enough, the potential for a fresh banking and liquidity crisis becomes significant; such a crisis might even become inevitable.

That is the real message to take from mortgage rates spiking to 8%. The high rates are but the latest reminder that the US financial system is nowhere near as sound as the prevailing narratives are wont to believe.

A financial crisis might not be inevitable, but should there be a financial crisis, there is little reason to believe it will be either small or easily contained. It is far more likely to be the perfect financial storm.

My question is regarding all of these flashing warning signs, and the outbreak of World War 3.

When I was studying Econ in the ‘70s, economists were still debating cause and effect during the Great Depression. Some said that the Depression ended not because of any New Deal policies, but because the economy roared back to life when America had to gear up to fight World War 2.

But many aspects of today’s financial markets and the world’s macroeconomics are much, much different. So, if -God forbid - WW3 breaks out next week, how would you expect it to affect these flashing warning signs? (And yes, a book could be written about it, but a paragraph of your ever-insightful analysis would be all I’d ask.)

As long as the big banks are not raising interest rates on saving accounts, this means they are having plenty of cash. Smaller banks have been raising rates (or not and seeing outflow and going bankrupt).

I did get an arrogant offer from Bank of America for higher rates - but only on deposits on top of my current balance. So it seems they are having plenty of margin to catch the decrease in bonds evaluation. Interest rates on savings have always been a bell whether.

Rates are now not higher than they were pre-2000 before Greenspan started the money press. Mortage rates are also not an historic high or even historically unusually high.

Unless of course they are driving us all off a cliff ... :-)