Not Just Inflation. Stagflation.

Is The Worst Case Scenario Becoming The Likely Scenario?

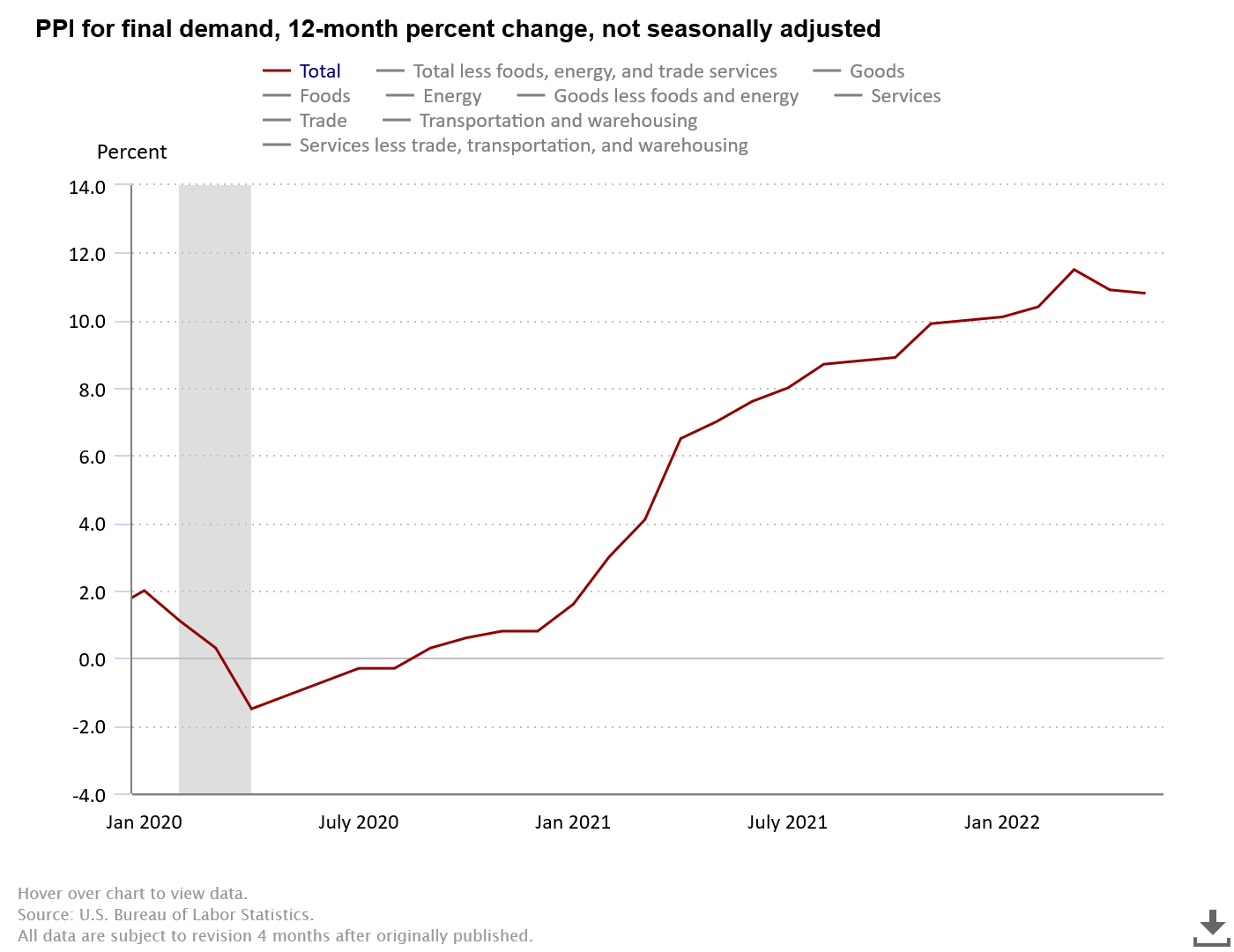

Previously, I have remarked how the leading indicators such as the Producer Price Index point to levels of inflation we have yet to experience, but are most likely coming.

Yet while prices are rising, other economic indicators suggest the recessions contractionary phase may be looming considerably closer than many prognosticators and pundits have suggested. Inflation plus real GDP decline (along with other indicators) leads to the phenomenon that was christened “stagflation” back in the 1970s—a portmanteau from “stagnation” and “inflation” that was used back then to describe the combination of rampant inflation coupled with general economic stagnation and decline.

The latest indicators show the economy is heading into this “worst case” scenario.

Review: PPI Shows Still More Inflation To Come

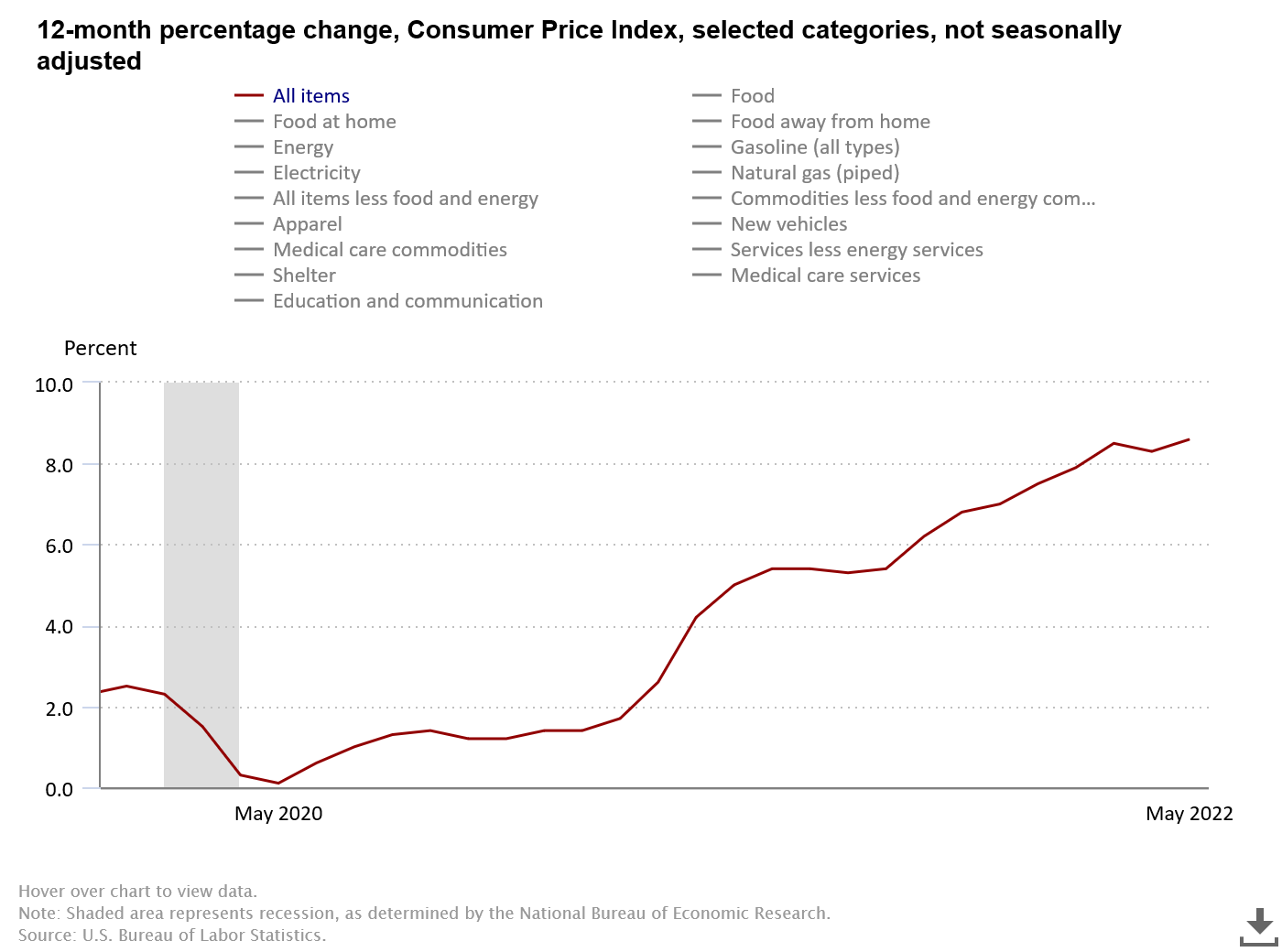

As mentioned before, the US Producer Price Index in the month of May clocked in a full 2 percentage points above the Consumer Price Index, rising an unadjusted 10.8% for the month.

By comparison, the CPI, although still running red hot, “only” rose 8.6% unadjusted.

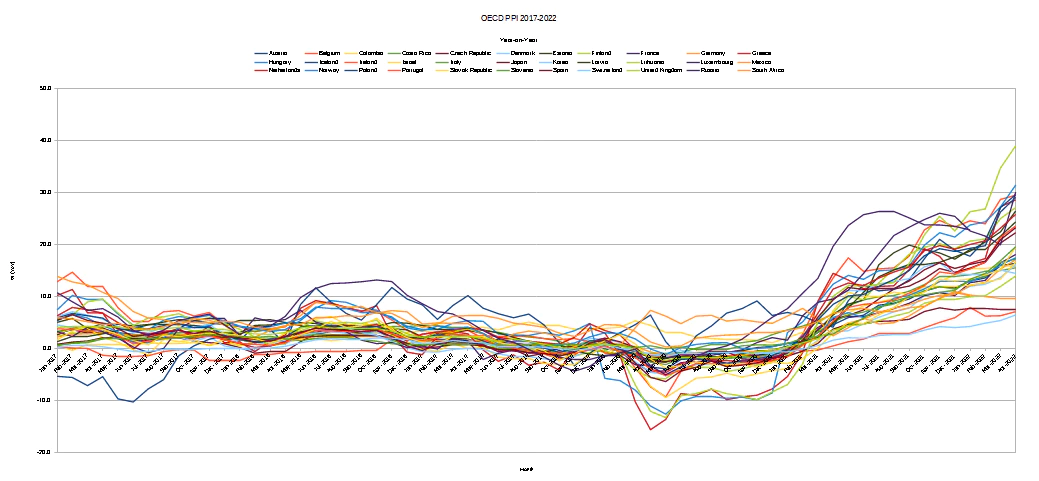

That PPI is indicating at least 2% more inflation has yet to be felt in the CPI is confirmed by the OECD PPI data globally, which reveals how much inflation is a global issue.

Now Include….Deflation?

While the price indices are flashing “inflation” globally, other indicators here are flashing an opposite signal, suggesting a deflationary episode is coming on quickly.

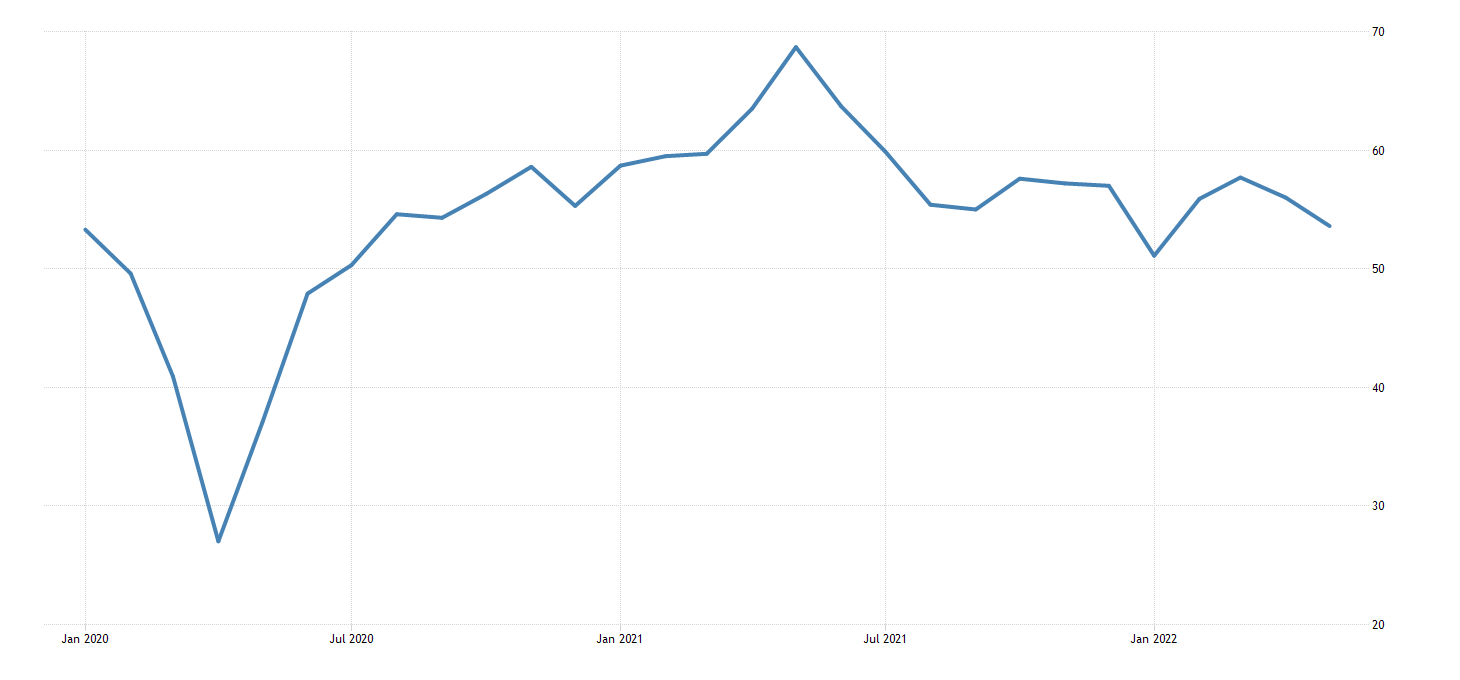

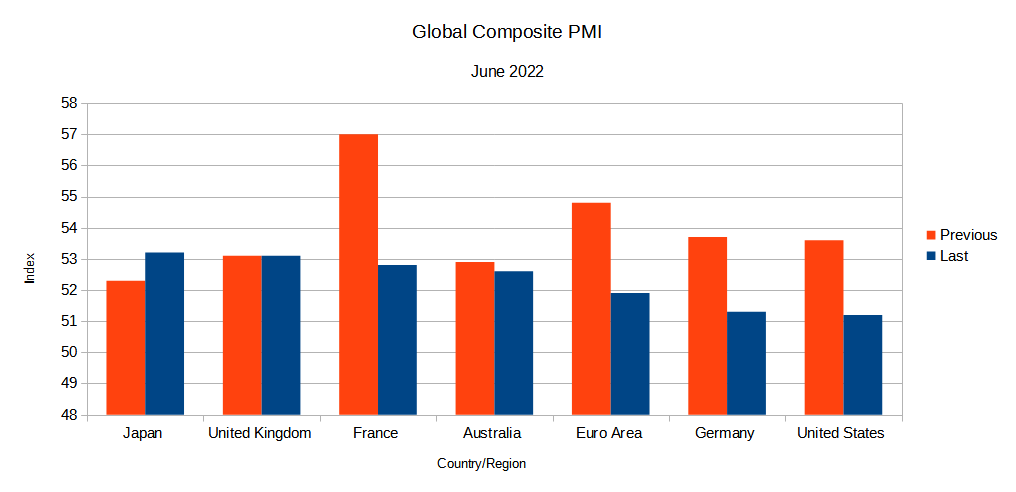

Last week, the June Purchasing Managers’ Index for the US slumped from 53.6 to 51.2, suggesting a significant slowdown in business activity is looming.

The US PMI is joined by PMI metrics from Europe and elsewhere also pointing to a deep decline in business activity.

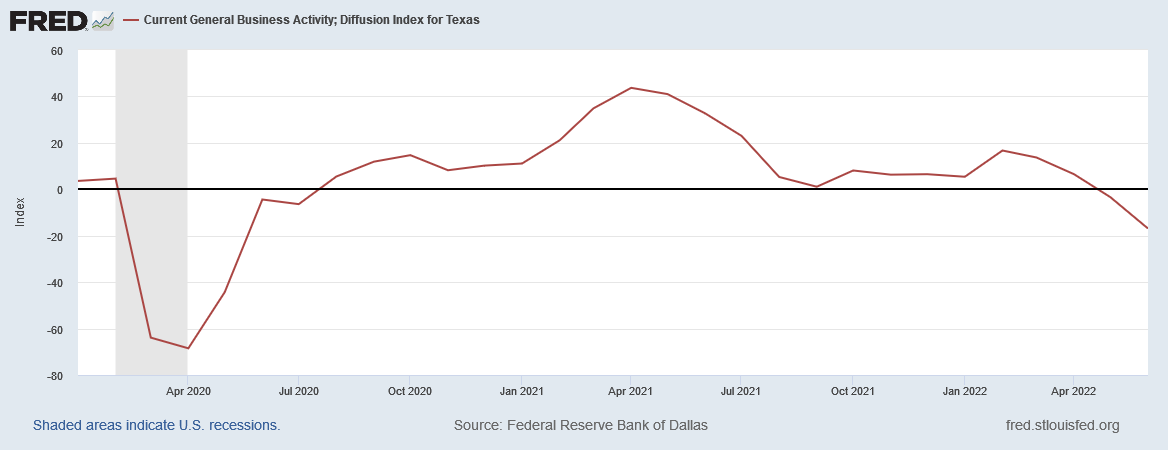

This strong deflationary signal was joined yesterday by the Dallas Federal Reserve’s monthly Texas Manufacturing Business Survey, which shows factory output in the Lone Star State falling off a cliff, showing the lowest numbers since the pandemic-induced recession of 2020.

Perceptions of broader business conditions worsened again in June. The general business activity index declined 10 points to -17.7. The company outlook index also fell 10 points, from -10.0 to -20.2. Both indexes reached lows last seen in May 2020. The outlook uncertainty index shot up to 43.7, a 17-point jump from May.

Note that both the PMI and the Business Survey have been trending down since peaking last spring and summer, indicating the deflationary impulse is fairly deep.

Add Them All Together And You Get Stagflation

While the deflationary signals of the PMI and Dallas Fed Business Survey might seem contrarian to the inflationary signals of the Consumer Price and Producer Price Indices, such a combination of indicators generally points to what has been labeled “stagflation.”

Stagflation is characterized by slow economic growth and relatively high unemployment—or economic stagnation—which is at the same time accompanied by rising prices (i.e., inflation). Stagflation can be alternatively defined as a period of inflation combined with a decline in the gross domestic product (GDP).

Rising inflation and declining manufacturing and production activity certainly qualifies as stagflation.

Put simply, the wheels are coming off the economy. The distortions and dislocation within the US economy that have been growing for months, with each rising measure of the CPI, are taking their toll. Even though there is likely still inflation yet to move through the economy, there are indications of a deep decline in overall demand, which is becoming increasingly clear in the PMI data and now the Business Survey.

Even with continued upward pressure on prices, the economy as a whole, both here in the US as well as globally, is slowing down.

Recession Is Not Merely Here, But Deep And Getting Deeper

The PMI and Business Survey data are merely the latest data points to confirm what I have been saying for some time now: Contrary to the pontifications of the “experts” and the media, economic recession is very much a present reality, not a future possibility.

Moreover, if production and general business activity continue to decline, any notion of the Fed—or any central bank anywhere—being able to engineer a “soft landing”, where the recession will be relatively mild and hopefully of short duration, must be discarded as so much wishful thinking. This recession is here, is global, is deep, and is getting deeper.

The Fed is not in control of this economic contraction. The government is not in control of this economic contraction. Nobody is in control of this economic contraction.

Which is the constant reminder and eternal cautionary for all government economic interventions. Despite the persistent expectations of many, governments do not control economic outcomes. Even when government policy creates the conditions and sets the stage for economic distress, the consequences are always chains of events that, once started, must play out however they will.

This recession was set in motion the moment the governments of the world opted to lock down nearly everywhere in response to COVID-19. Every supply chain everywhere was completely disrupted if not broken altogether. The normal flows of goods that are the essence of all economy were abruptly halted; restoring those flows was never going to be automatic, or particularly easy, and in some regards might not even be possible.

Unlike the corporate media, I do not claim to have a crystal ball. I cannot say, for no one can know, exactly how deep the recession will be, or how long it will last, or what things will be like when at last the world emerges from this gathering economic gloom.

Yet while we cannot know with certainty what will be, the data plainly tells us what is. The data is telling us that global economic conditions are not good and are getting worse. The data is telling us that the situation is dire, and the indications are that it will be so for some time yet to come.

We are not yet done with these “interesting times.”

Not to worry. All we need to do is keep sending more weapons to Ukraine for Russia to blow up & desperate Ukrainians to sell on the dark web, to jeep the MilitaryIC buying replacement weapons to blow up Ukraine. When we run out of Ukraine infrastructure & Ukrainians to blow up, we can just move ops to the ME or Taiwan.

And release a new bioweapon to sell a magical vaccine to jab useless eaters with to send them to the hospital to keep the MedicalIC humming along.

After we've killed off enough useless eaters we won't need as much production & the leftovers will live happily ever after.