The narrative is making less and less sense.

Presumably, oil demand rose above its pre-COVID peak in September, while oil supply did not.

Global oil demand rose seasonally in September to the second-highest level of this year, according to the JODI data shared by the Riyadh-based International Energy Forum (IEF).

In September, global oil demand was at 101 percent of pre-Covid levels, while crude production was at 99 percent of those levels, the data showed.

That 101% of pre-COVID demand equates to an additional 1 million barrels per day of oil demand.

Global oil demand climbed seasonally in September to the second-highest level of the year and nearly 1 mb/d above September 2019 levels, according to new data from the Joint Organizations Data Initiative (JODI). Demand growth was driven by diesel consumption in China and gasoline demand in the US.

One would expect oil prices to rise given a 2% deficit in production.

However, oil prices fell in September.

West Texas Intermediate prices moved steadily down throughout September.

Brent Crude did likewise.

Even in October, WTI crude rose for a week, then dropped to lower than the October 1 price, before climbing again through the rest of the month.

WTI has been declining thus far in November.

And while Brent crude trades at a structurally higher price than WTI, the pricing pattern is the same both for October…

…and in November.

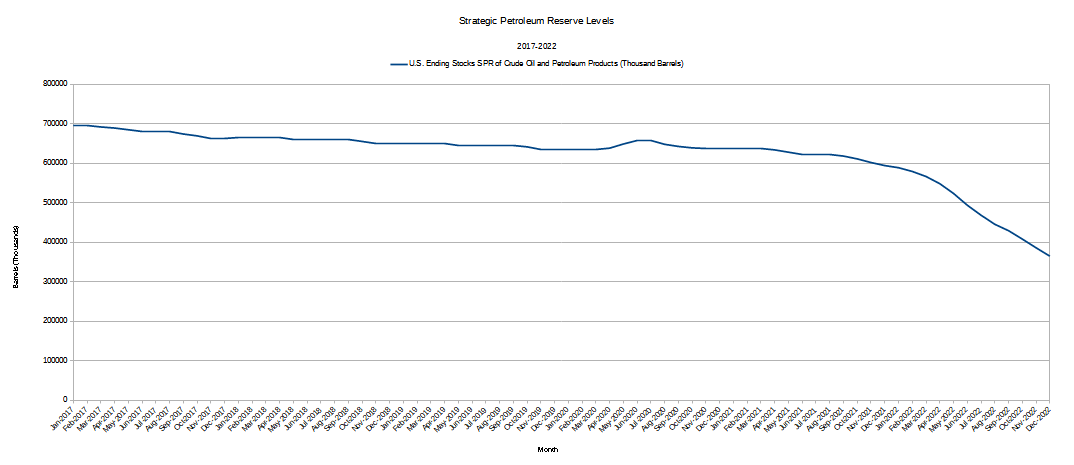

Even releases from the Strategic Petroleum Reserve do not account for the lack of rising oil prices. 1 million barrels per day of additional demand in September amounts to 30 million barrels of additional demand for the month.

While the release data from the Strategic Petroleum Reserve is only available through August, a simple extrapolation from that data suggests that only ~16 million barrels were released in September, and a total of 60 million barrels of oil will have been released by the end of November.

The SPR probable releases for September, October, and November do not account for the 2% variance between available supply and rising demand. According to the narrative, the demand for oil is running well in excess of the SPR releases.

In other words, demand is presumably exceeding available oil supply, and yet oil prices are not climbing.

Something is wrong with this picture. The narrative says energy price inflation is here, and the data says it's not.