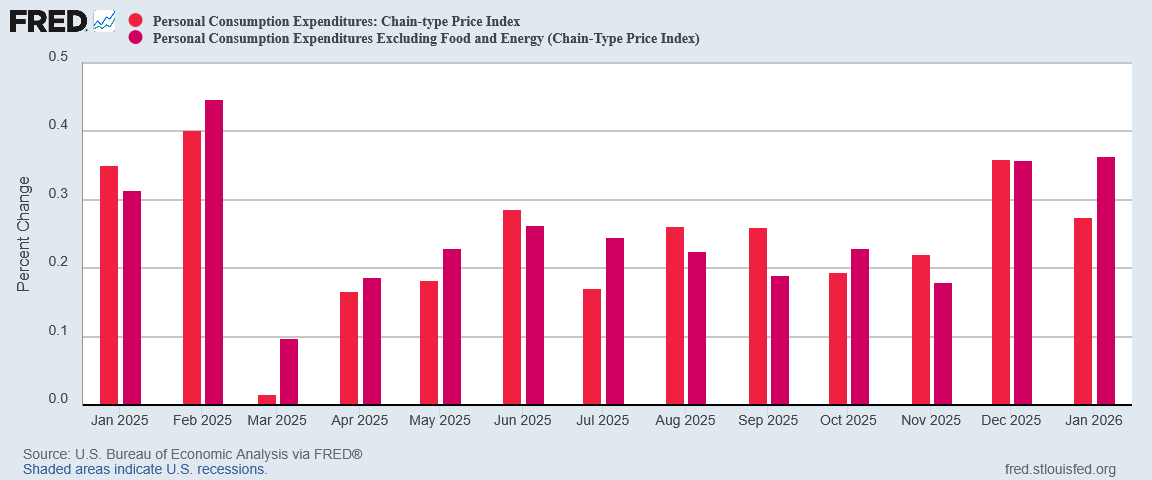

From the preceding month, the PCE price index for January increased 0.3 percent. Excluding food and energy, the PCE price index increased 0.4 percent.

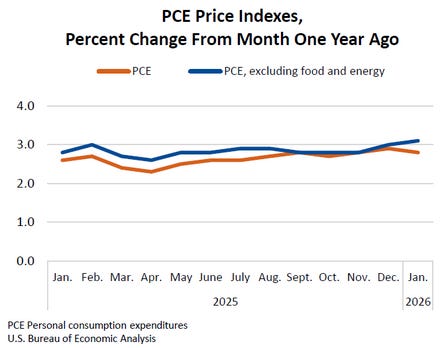

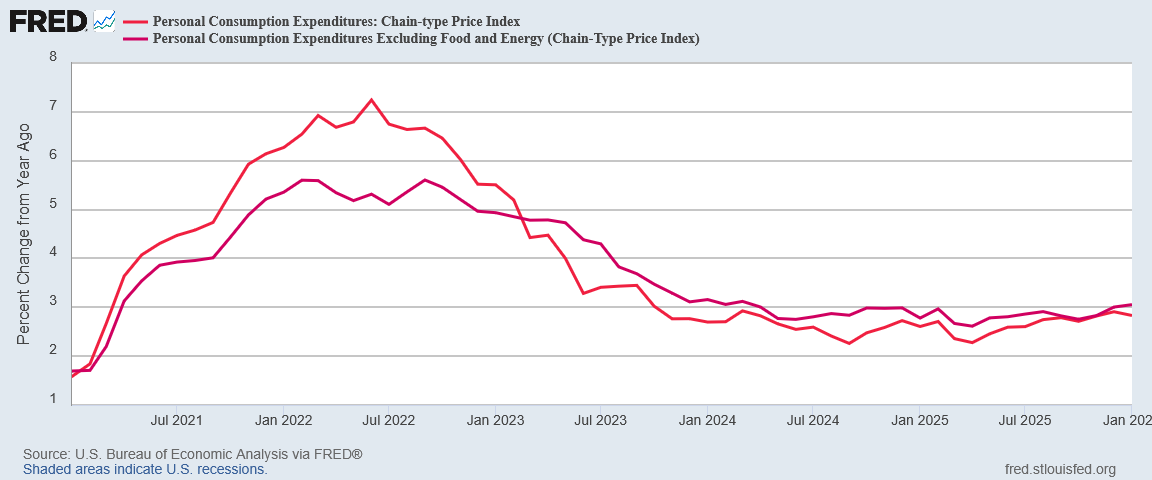

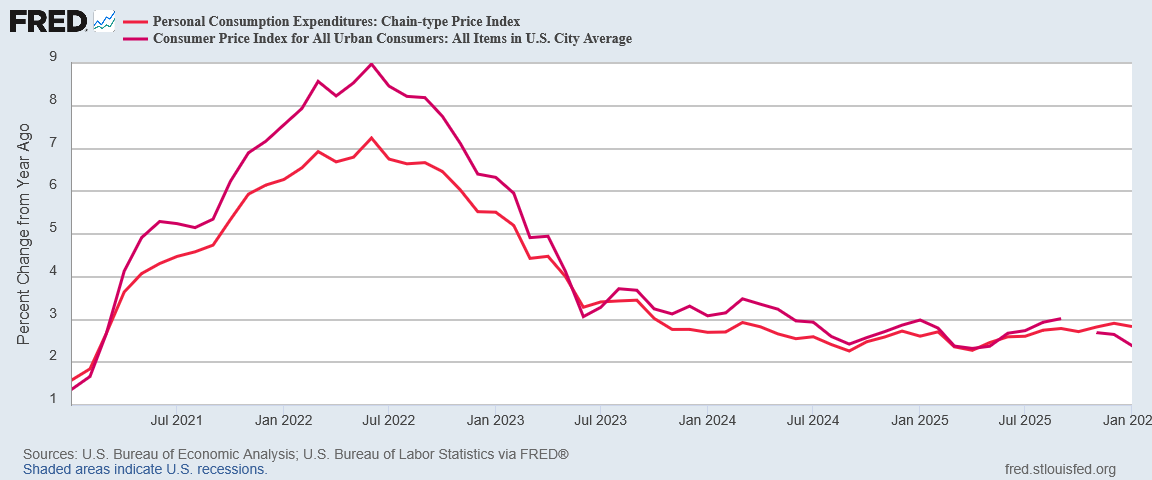

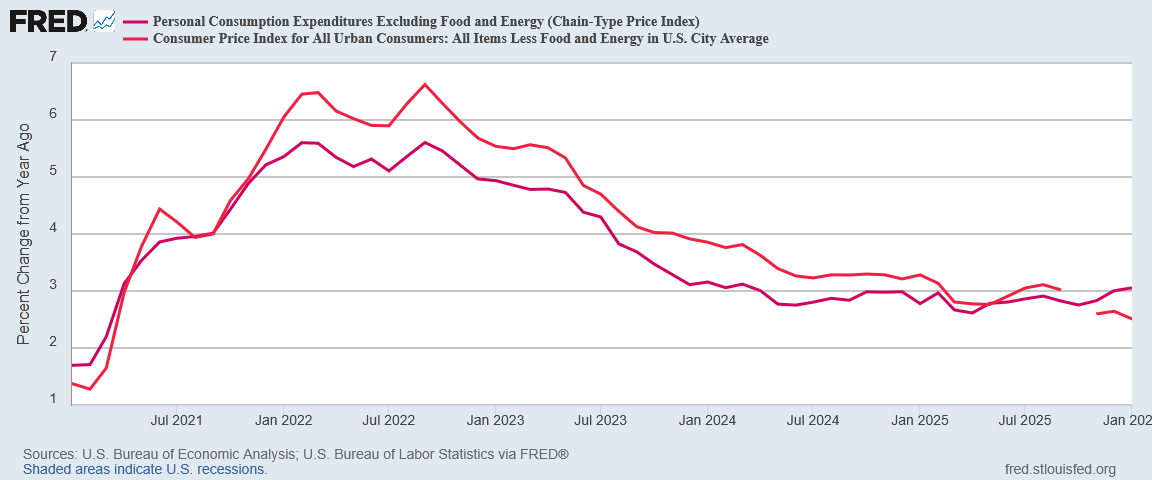

From the same month one year ago, the PCE price index for January increased 2.8 percent. Excluding food and energy, the PCE price index increased 3.1 percent from one year ago.

Headline inflation was almost exactly where Trading Economics projected it would be.

The PCEPI inflation story for January is almost a replica of the PCEPI inflation story for December. The warning signals of both inflation and deflation from December persisted in January, making skepticism and even pessimism by far the more appropriate perspective for the start of 2026.

The lack of significant change is a warning sign that stagnation and even deflation may be around the corner for the US economy. The economy has flirted with that slow-motion decline for a number of years now, and we may be seeing signs that flirtation is not yet finished.

Every article I publish takes time, care, and independence. A paid subscription fuels that work and shields it from outside pressure. If you’re able, join me today.

PCEPI And CPI Diverging, Signalling A Pricing Shift Of Some Kind

Headline inflation eased down 0.1pp year on year in the January PCEPI to 2.8%, while core inflation rose to 3.1% year on year.

Month on month, headline inflation also dropped 0.1pp, to 0.3%, while core inflation remained largely unchanged.

January was at least the third straight month we see the PCEPI and CPI inflation data diverging to an increasing degree. Even though headline inflation declined for both year on year, the CPI inflation decreases have been much greater in recent months, so that the cooling trend visible in the CPI data has not been readily apparent in the PCEPI data.

We cannot infer that one index is “right” and the other index is “wrong”, but the divergence does tell us that the two data sets are picking up different signals to different degrees. A pricing shift of some sort is emerging, although we cannot say yet whether that shift is going to be more deflationary than inflationary.

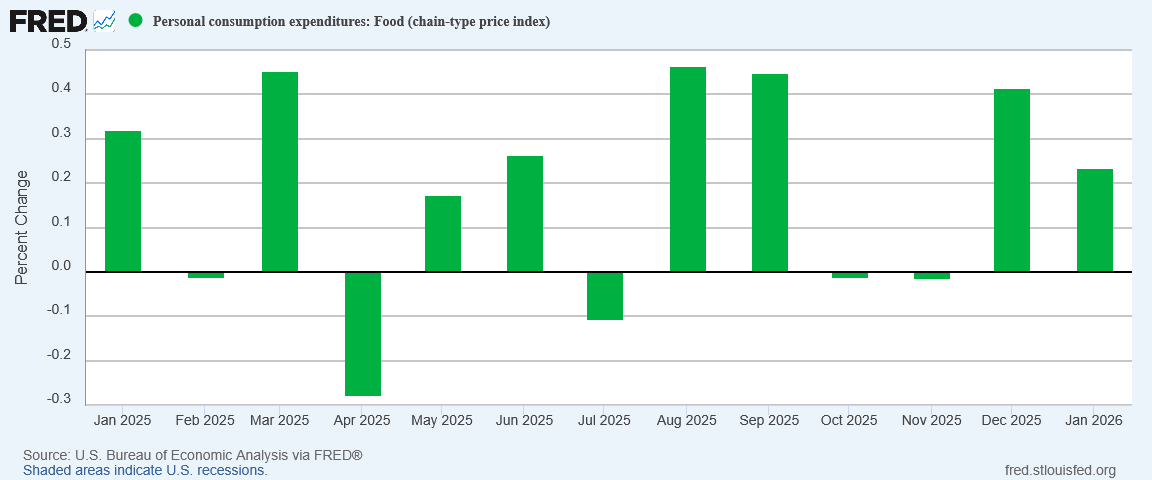

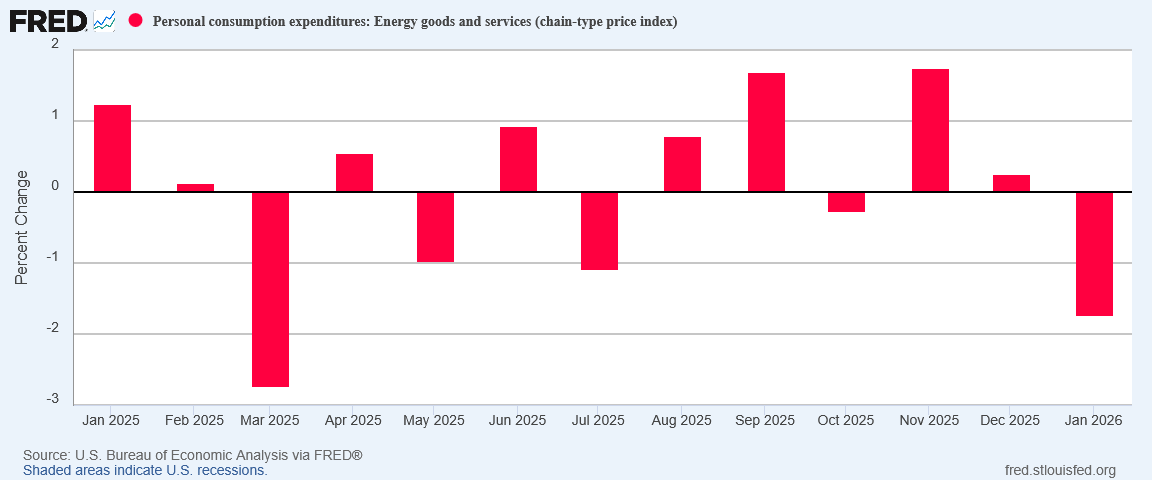

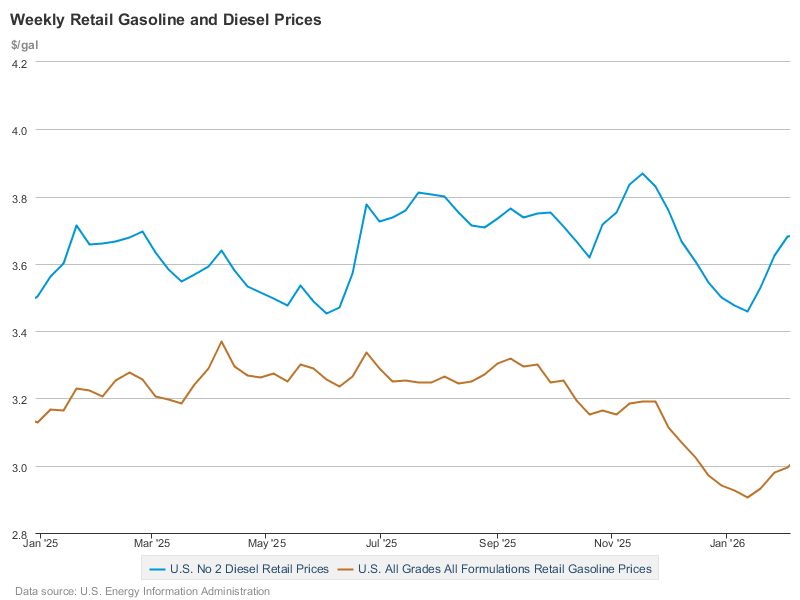

That gasoline prices fell at the pump in January, according to the EIA, arguably kept energy price inflation from heating up.

While falling energy prices are always welcome, the price indices can only ignore the underlying price data for so long. At some point corporate America is going to pass along the inflationary impulses and price pressures it has accumulated.

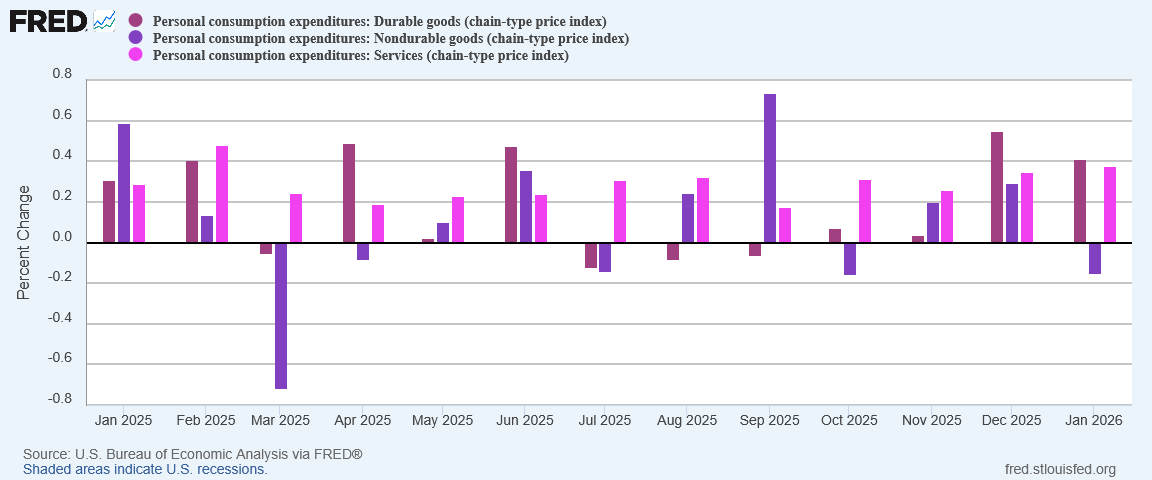

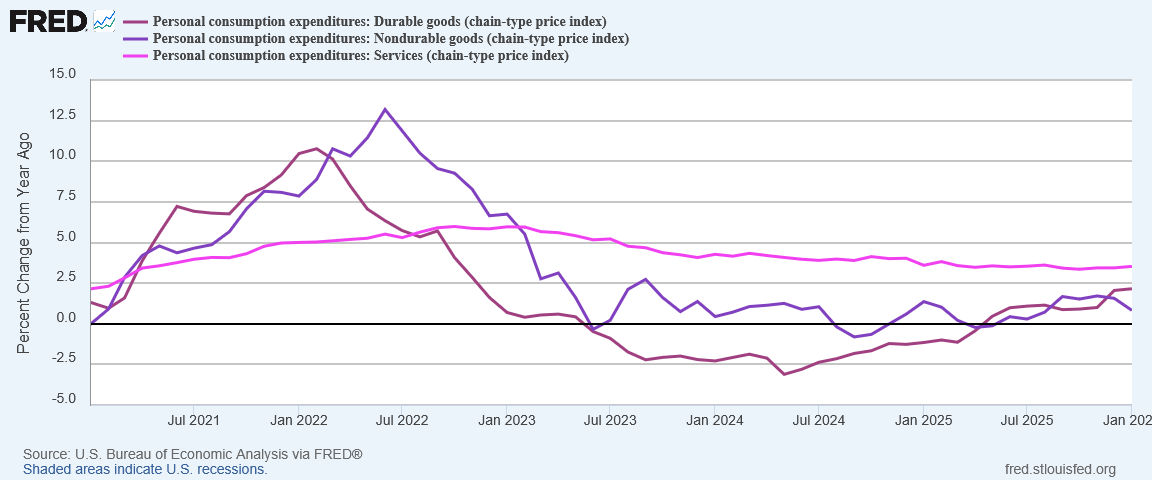

Within core inflation, nondurable goods prices actually fell month on month, while durable goods inflation cooled considerably.

Service price inflation heated up slightly, but the overarching trend for core inflation is disinflation.

This is not going to last.

We should anticipate significant increases for inflation in both the CPI and PCEPI once March rolls around. As I have observed more than once, the late-February price surge in benchmark crude oil prices is sure to produce significant inflation for March. Not only will headline inflation surge with rising energy prices, but rising energy costs very likely will percolate through to other goods and services.

Enjoy the cooler inflation levels now, because they are about to change.

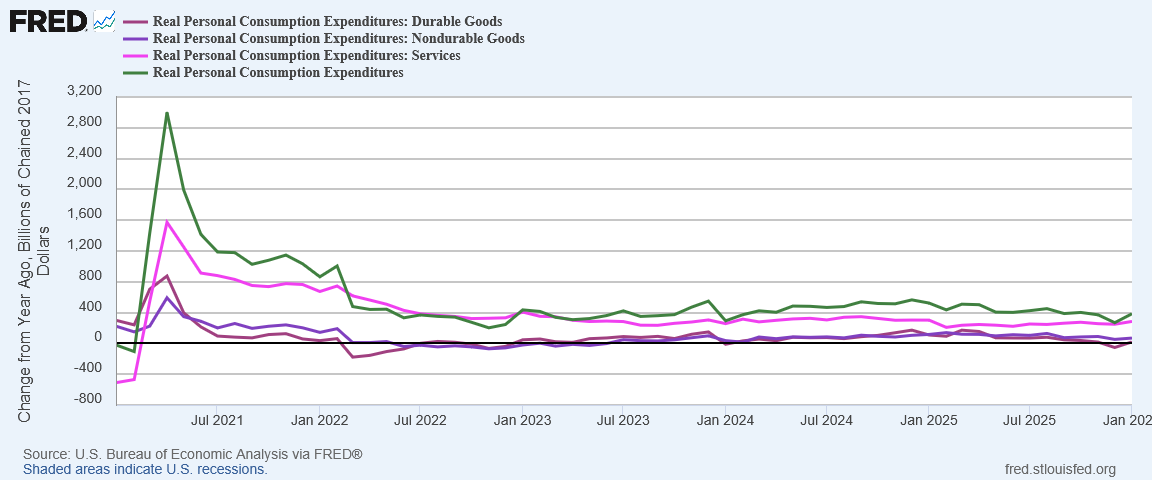

One reason for the cooling of goods price inflation is that, for the second month in a row, people spent less money on goods, while spending more money on services.

When people buy less, the impact of inflationary pressures is blunted—without buying behavior, there is no support for a particular price level for any good or service. That much is economics 101.

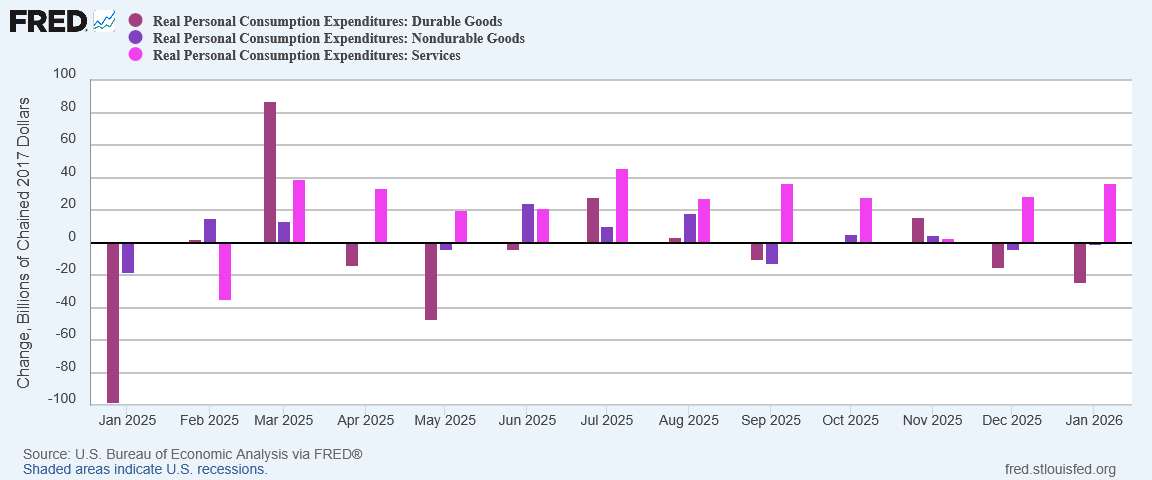

As I speculated for December, falling goods consumption arguably acted as a restraint on goods price inflation. Declining consumption invariably means people are choosing not to purchase things, or are postponing those purchases. Both consumption behaviors are indicative of deflation rather than inflation.

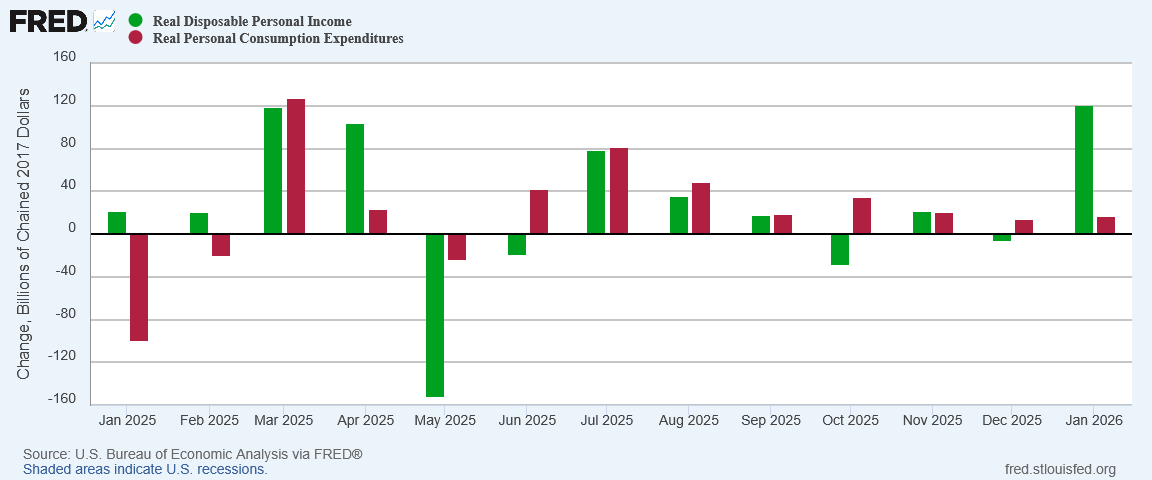

Remarkably, the decline in durable goods consumption occurred during a month when real disposable personal income surged, far outpacing overall consumption.

Notably, rise in disposable income did not translate into a rise in consumption. That lack of a consumption increase is a clear signal that deflation either is emerging or is a potential imminent risk in the economy.

If lack of consumption is a deflationary signal, does the continued rise in durable goods prices mean we are seeing at long last the results of President Trump’s Liberation Day tariffs?

We should also note the shrinking amount of deflation measured from June 2024 onward. That decrease in deflation means various inflationary pressures were becoming more prominent in overall goods prices. That trend predates the Liberation Day tariffs by at least a year.

What other inflationary pressures might exist besides tariffs? Overall consumption is the most likely candidate, and moving into last spring durable goods consumption had been increasing year on year, becoming a more significant part of overall consumption.

We should also note that whatever inflationary pressure exists because of tariffs, the ultimate impact on durable and nondurable goods prices has been modest, with durable goods inflation not getting up to 2.5% year on year and nondurable goods inflation running at half that.

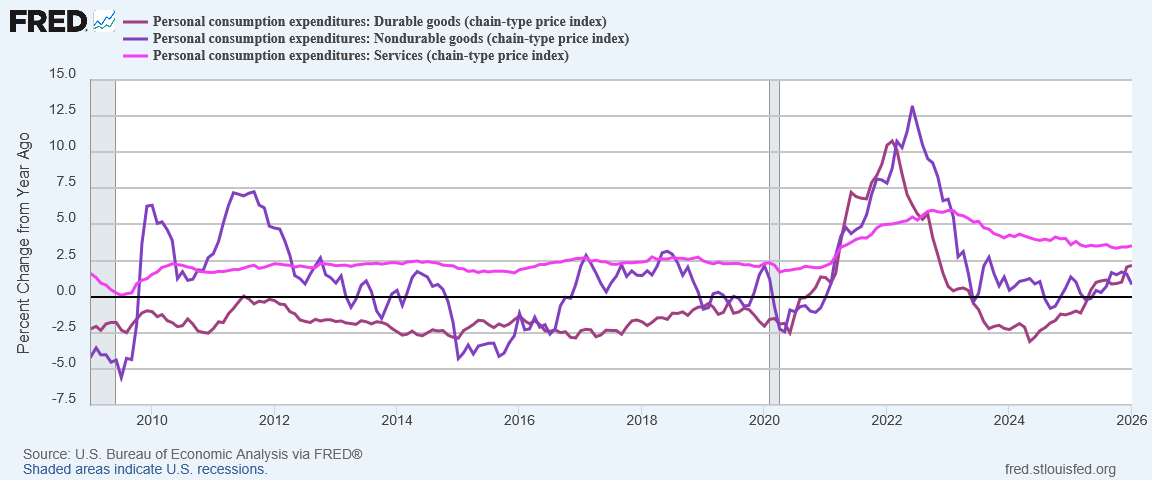

With durable goods having been in deflation for over a decade prior to the 2022 hyperinflation cycle, rising goods prices now may simply represent a long-overdue reversion to mean within durable goods pricing.

Are tariffs a factor? Absolutely. However, they are not the only factor and it is still far from clear that they are a primary factor even for durable goods. Inflation and deflation are the resolution of all pressures on prices, making the relationship between overall inflation and various factors not a linear relationship but a differential one.

Lack Of Consumption Is A Bigger Concern Than Tariffs

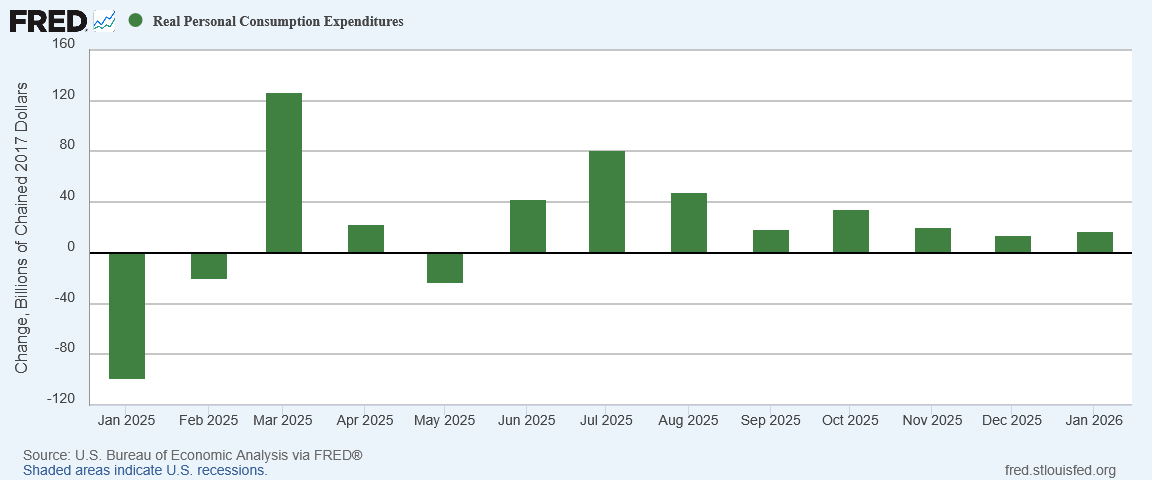

Regardless of corporate media hyperventilations about “muh tariffs”, that consumption overall has been in long-term decline is by far the greater worry.

As I have discussed numerous times previously, the potential for stagflation and even deflation in the US economy is a real concern, and one that has been present in the data for a number of years.

We only have to look at China’s deflating economy to see the perils of anemic and declining consumption.

Despite all the propaganda narratives to the contrary, lack of consumption remains China’s singular economic vulnerability. If lack of consumption is bad news for China, it is bad news for the United States as well.

Lack of strong consumption growth also once again cuts against President Trump’s “Golden Age” rhetoric. It is difficult to argue persuasively that this represents an economic “Golden Age” for the United States when people are displaying reluctance to purchase goods and consume things.

When the middle economic strata are feeling flush with cash they tend to consume more, as a rule, as they will have already satisfied their desire for savings and defensive measures such as paying down debt. If we are not seeing significant consumption growth, and we have not seen that for the past six months especially, then we do not have good evidence the middle economic strata are feeling flush with cash, even after January’s increase in disposable income.

This also highlights the perverse nature of deflation within an economy. Where inflation comes on fast and is easily seen as an immediate economic shock, deflation tends to be a slow decline. Deflation does not meant the economy collapses, but merely withers way gradually over time.

Are we seeing a rising risk of deflation in the economy? We are. We’re not there yet, but the concern is real and should not be ignored. That we are seeing inflation signals on top of that means what could be unfolding is a stagflation scenario, with strong inflation and deflation pressures occurring simultaneously.

Inflation in the January Personal Income and Outlays report did not change much from December—and that very likely is cause for concern. We’ve endured “lost decades” of stagnation and deflation already. Signs that we may be about to go through that again are not at all comforting.

If this story gave you real value, help me keep going. All Facts Matter is powered by readers who believe facts should stand on their own. Your subscription makes that possible.

“Notably, rise in disposable income did not translate into a rise in consumption.” Peter, are there any data sets- maybe from consumer surveys - indicating that people are saving up for major purchases, such as houses or new cars?

Also, we get a new captain at the helm of the Fed in a few weeks. He had probably planned on aggressive interest-rate action to bring the Fed more in line with Trump’s agenda, but that was before the Epic Fury campaign drove oil prices up. What action would you now figure the Fed will implement?

“Notably, rise in disposable income did not translate into a rise in consumption.” Peter, are there any data sets- maybe from consumer surveys - indicating that people are saving up for major purchases, such as houses or new cars?

Also, we get a new captain at the helm of the Fed in a few weeks. He had probably planned on aggressive interest-rate action to bring the Fed more in line with Trump’s agenda, but that was before the Epic Fury campaign drove oil prices up. What action would you now figure the Fed will implement?

AGI 🤖🪙💱 TOKEN market pricing ‘splainer:

https://claude.ai/public/artifacts/8977751d-31fb-4240-b282-8ee15ddb2e25

.....follow the money, Boomtown Cycle!⚒️🎲