Rising Inflation Means Global Recession Is Here

We're Past "Pending" And Well Into "Present"

Today was not a good day for US stock markets.

Alternative financial media site Zero Hedge views today’s financial market performance as a leading indicator that tomorrow’s CPI report will be worse than expected.

Does anyone else get the sense that this directional thrust ahead of tomorrow is just setting us up for a huge reversal higher on CPI?

What tomorrow’s exact CPI numbers will reveal is a question that will, of course, have to wait for tomorrow. However, the pending report on inflation in the United States is a good opportunity to review the global state of consumer prices. Inflation has not only been a growing global problem for a number of years, but since last fall the pace of inflation has picked up amost everywhere.

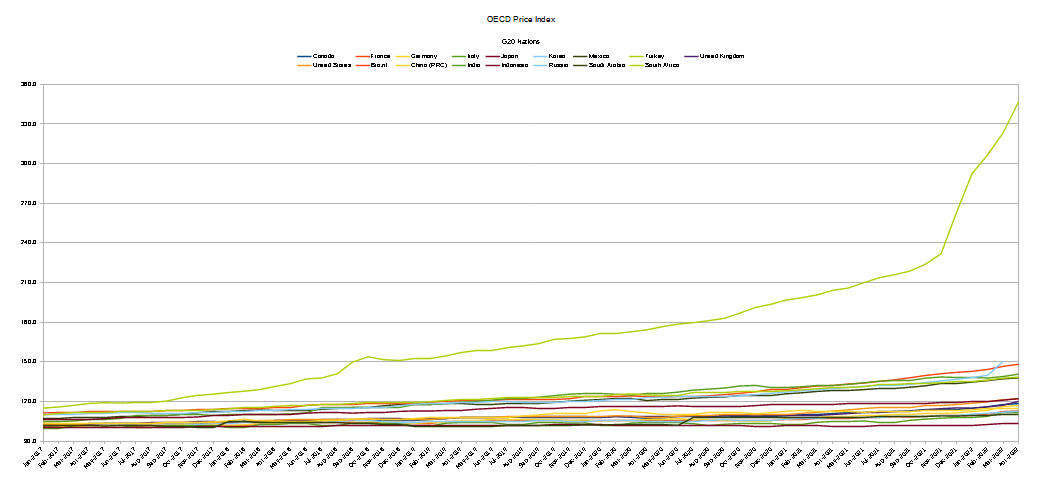

OECD G20 Price Indices Tell The Story

One of the few good things about entities such as the Organization for Economic Co-Operation and Development is that they are filled with bureaucrats who love to compile numbers—true manna from heaven for a geek like me who likes to look at numbers! Among the statistics the OECD makes available are the consumer price indices for the bulk of the G20 nations.

Setting aside questions about the tendency of governments to pad, manipulate, and at times outright falsify their data, such data sets give us a good glimpse into what governments around the world are experiencing—and reporting—on consumer price inflation.

In my previous commentaries on inflation in the US, I have pointed out that a fundamental aspect of rising inflation is that it represents economic disequilibrium. Inflation means prices—and thus the overall economy—is greatly out of balance.

Rising inflation means that disequilibrium is getting worse. Worse still, inflation, contrary to the pronouncements of economic experts, invariably represents a reduction in overall economic output.

Inflation literally means people pay more to buy less.

What is true for the US economy regarding inflation is true for all economies. Economic principles do not change merely because one crosses a national boundary. Markets are ubiquitous—wherever there is human society, there is human economy and human marketplaces driving economic events.

Thus the impacts of inflation on the US economy will be, broadly speaking similar across the G20, and around the world. The magnitude of the distortions caused by inflation may vary, but that there will be distortion caused by inflation is a universal economic reality.

For proof of this we need look no further than the OECD’s CPI data for the G20 nations.

Inflation Has Been Here For Some Time

What the OECD data shows is that inflation has been a noteworthy global phenomenon for quite some time. Reporting in the US may have only glommed onto rising inflation just this past year or so, but the seeds of what we see now began sprouting much farther back in time.

First, the obvious: inflation is completely out of control in Turkey, where prices are spiraling upward in true hyperinflationary fashion, very reminiscent of the destablizing hyperinflation of the 1920s Weimar Republic that helped bring down Germany’s interwar flirtation with democratic governance.

However, looking past the obvious problems for Turkey, we see that not only are price indices rising across the G20 nations, but there is a growing separation between countries such as Brazil and Mexico, where prices are rising faster, and countries such as the UK and Japan, where prices are still rising, albeit much slower.

The distortions which inflation causes within an economy also arise between economies. Shifting inflation rates mean some countries are not only losing purchasing power internally, but also relative to other countries.

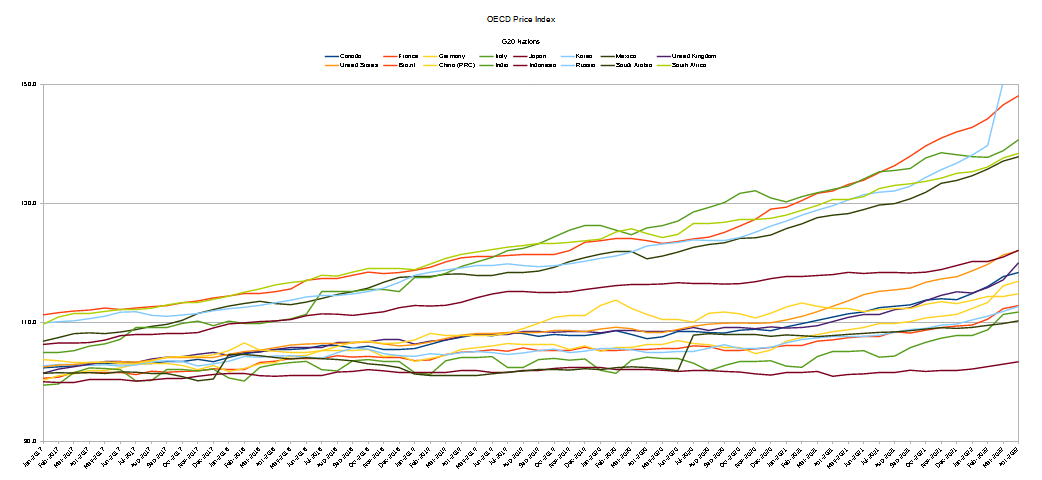

This becomes even clearer if we tune out the outlying inflation signal from Turkey to focus on the core trend:

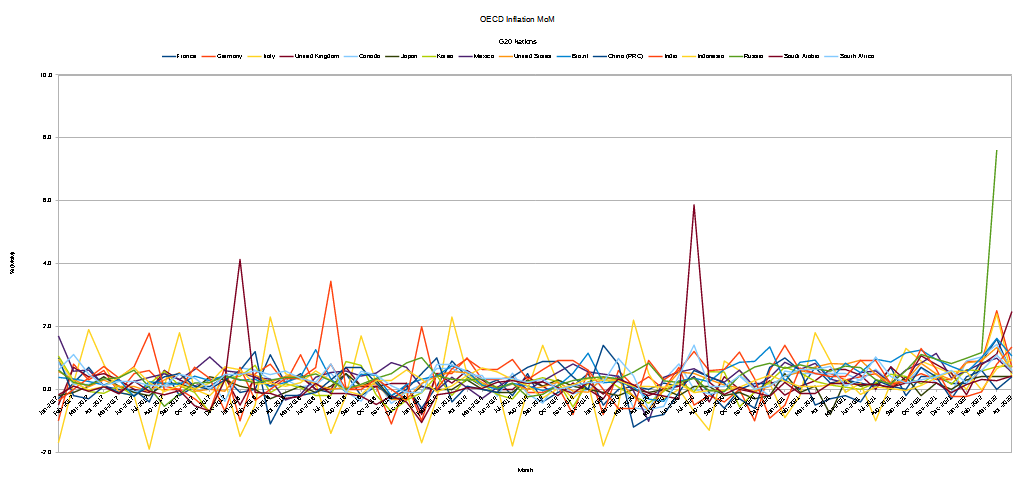

Monthly Fluctuations An Early Warning Of Rising Instability

If we look at the relative price index changes month-on-month (MoM), not only do we see some of the same bifurcations, but also clear evidence in some countries of rather dramatic price fluctuations—the very definition of “instability”.

Italy especially shows signs of inflationary duress, as their prices are rising significantly one month only to fall again by similar magnitude in the following months before rising yet again. Moreover, this has been the case for Italy at least back to 2017 (the cutoff for the data).

Yet it is not merely Italy that has shown such signs of economic duress. Saudia Arabia also shows significant month-on-month inflation spikes, as does India.

A note about Russia’s dramatic spike at the end of the data set: much of this is a direct consequence of the Russo-Ukrainian War and the attendant economic sanctions levied against Russia. Russia’s current hyperinflationary episode is one of the few times the underlying circumstances are readily identifiable.

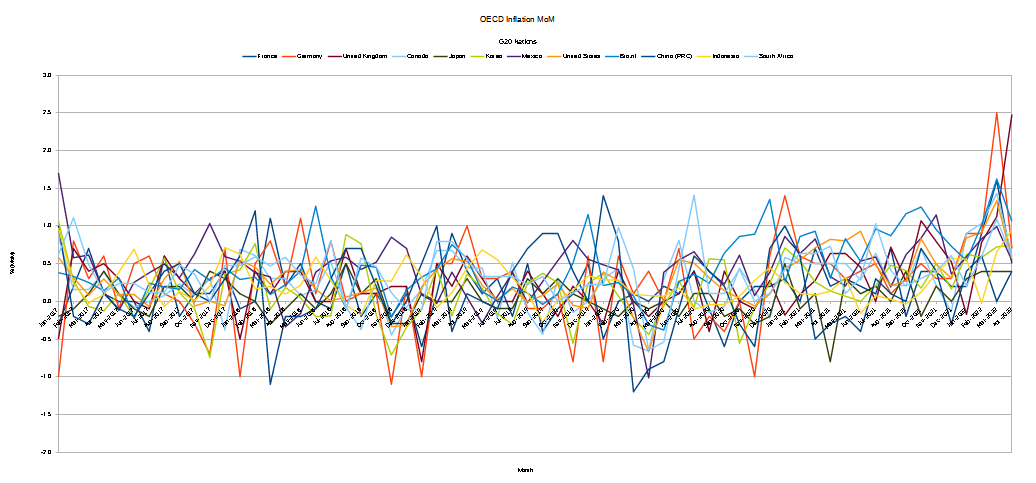

Having noted these extreme fluctuations, if we tune out these outliers we can get a clearer picture of the MoM trend across the bulk of the G20.

Excluding the outliers—and thus eliminating their outsized effect on the overall graph—we begin to see that not only has inflation been creating economic duress among the G20 going back to at least 2017, but beginning last year the situation started becoming incrementally worse.

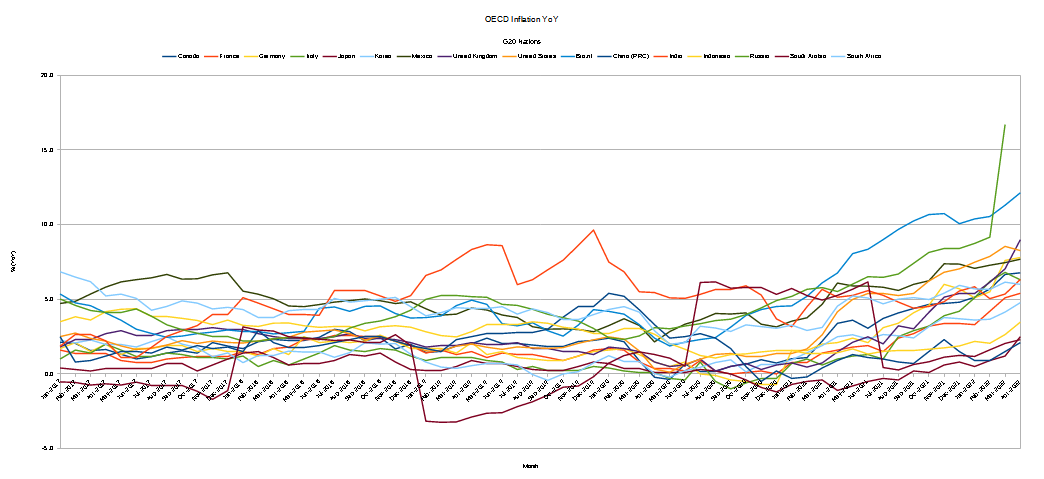

Yearly Inflation Tells The Tale

Annual inflation—the inflation rate most commonly reported and the figure which will be updated by tomorrow’s CPI report—across the G20 brings the overall inflation picture more clearly into focus.

India, for example, while experiencing rising inflation at the present time, actually endured even worse inflation in 2019. While the pace of inflation ameliorated for them somewhat in 2020 and the first part of 2021 before rising again at the end of 2021, the annual inflation trend for India articulates the ongoing weakness in the economy of the world’s second most populous country.

At the same time, Saudi Arabia has experienced periods of consumer price disinflation, which have abruptly reversed into significant inflation. As with Italy’s MoM inflation shifts, the abrupt fluctuations for Saudi Arabia are the epitome of economic instability—economic weakness that has been an ongoing phenomenon for a number of years.

Tuning out these outliers we see not just rising inflation in 2021 and 2022 across the board, but also a rising disparity—at the start of 2017 inflation varied from Japan’s 0.4% to South Africa’s 6.8% (a delta of 6.4%), and by April of this year the variance was from China’s 2.1% to Brazil’s 12.1% (a delta of 10%). Even comparing China’s 2.1% to the UK’s 9% inflation rate in April yields a delta of 6.9%, a half-percentage point greater spread than before.

Even with the outliers included, the disparity in inflation rates has grown, with the spread between Saudi Arabia’s 0.5% price decline and South Africa’s 6.8% price increase at the start of 2017—a delta of 7.3%—widening significantly.

Around the world, prices are rising, yet they are not rising everywhere the same. Imbalances within the global economy are increasing, and have been for quite some time.

The OECD data shows us that inflation is not a recent phenomenon, merely one we have recently begun to notice.

What Will Tomorrow’s CPI Report Bring?

While US inflation actually declined somewhat from March to April, the overall trend for 2022 is still one of rising prices, very much in keeping with the global trend.

Zero Hedge’s prognostication that tomorrow’s report will show a higher rate of inflation than might be expected is thus very much in line with the overall global trend.

Yet even if the CPI report should confound and turn in a lower number than anticipated, any decrease in inflation for the US is likely to be merely incremental, similar to the 0.2% decline in annual inflation reported last month. Such a change would not alter the growing disparity in price levels and inflation rates globally.

The “best case” for tomorrow’s inflation report is that the US economy has weakened only modestly for the month, and that things are considerably worse elsewhere. The “worst case” is that the US economy has weakened dramatically, which is likely to make things worse elsewhere.

In every case, the OECD consumer price data shows that the global recession has in fact already begun. We are past the point of a “pending” recession and well into the period where recession is a present problem.

Which means tomorrow’s CPI report will either contain less bad news or more bad news, but is not likely to contain any good news.

ZH got it right, higher again. I’m looking forward to the Shadowstats update.