When the data is “convenient”, it pays to be doubly skeptical of it.

The Bureau of Economic Analysis’ third and final estimate of GDP growth for the fourth quarter of 2023 is just that: “convenient.” It conveniently puts forward a claim that the US economy grew more than was first thought.

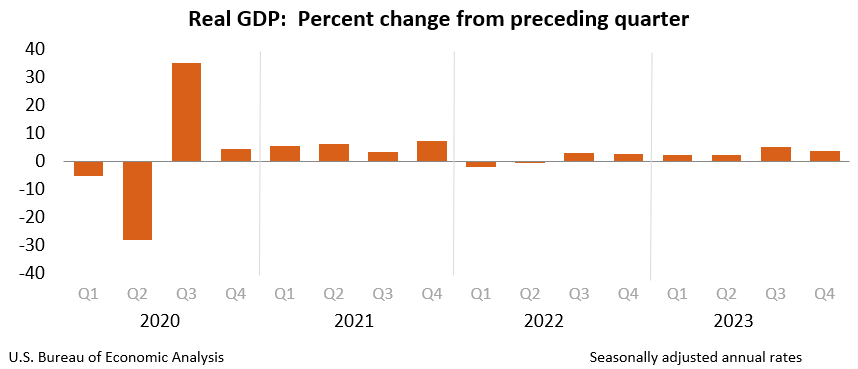

Real gross domestic product (GDP) increased at an annual rate of 3.4 percent in the fourth quarter of 2023 (table 1), according to the "third" estimate released by the Bureau of Economic Analysis. In the third quarter, real GDP increased 4.9 percent.

The GDP estimate released today is based on more complete source data than were available for the "second" estimate issued last month. In the second estimate, the increase in real GDP was 3.2 percent. The update primarily reflected upward revisions to consumer spending and nonresidential fixed investment that were partly offset by a downward revision to private inventory investment (refer to "Updates to GDP").

The BEA charts that real GDP grew by a tenth of a percentage point more than first thought. This is, of course, good news—if it is accurate, and if it is true.

Of course, in the second estimate, the BEA revised the GDP estimates down a tenth of a percentage point, which, as I noted at the time, had at least a soupcon of credibility to it.

The BEA took a very small step towards acknowledging the “weak and getting weaker” state of the US economy by trimming its GDP growth estimate every so slightly. Unfortunately, such half steps towards reality still leave the BEA assessment itself in the realm of fantasy and fiction, which is what the BEA headline numbers ultimately are.

Compared to the second estimate, it appears that the BEA took two steps back in the opposite direction. If the second estimate was only marginally credible because it trimmed the growth estimate slightly, it is surely a convenient realization that the economy actually grew more rather than less.

Of course, that would imply that the BEA was “goal-seeking” its news releases—working backwards from a desired result to publish to fill in the “estimates” to support that result. A US government agency would never stoop to such mendacity and dissembling...why would you ever think such a thing? (Because they would and they possibly did).

While some might think my insinuation of mendacity and dissembling at the BEA rather outre, Wall Street was fairly blase about the Q4 GDP numbers. Only the Russell 2000 index showed any real life during yesterday’s trading, with the Dow Jones, NASDAQ, and S&P 500 indices all either charting negative or minimally positive on the day.

Treasury yields responded somewhat positively, moving down slightly on the day.

One sure sign that the numbers were not anything to crow about is that Dementia Joe’s handlers were not posting on Twitter crowing about them. As luck would have it, neither the President nor his Press Secretary had anything to say about the Q4 GDP numbers.

Yet if the numbers are to be believed, the economy is growing, and just a little bit more than the first assessment indicated, and especially more than the second assessment indicated.

Why is the President and/or his Press Secretary not talking good economic data up?

One reason for the President’s silence might be that, even with the upward revision, the GDP figure is still soft and getting softer. Despite media narratives about the health of the economy, the fourth quarter of last year was considerably softer, economically speaking, than the third quarter, with far less GDP growth per the BEA.

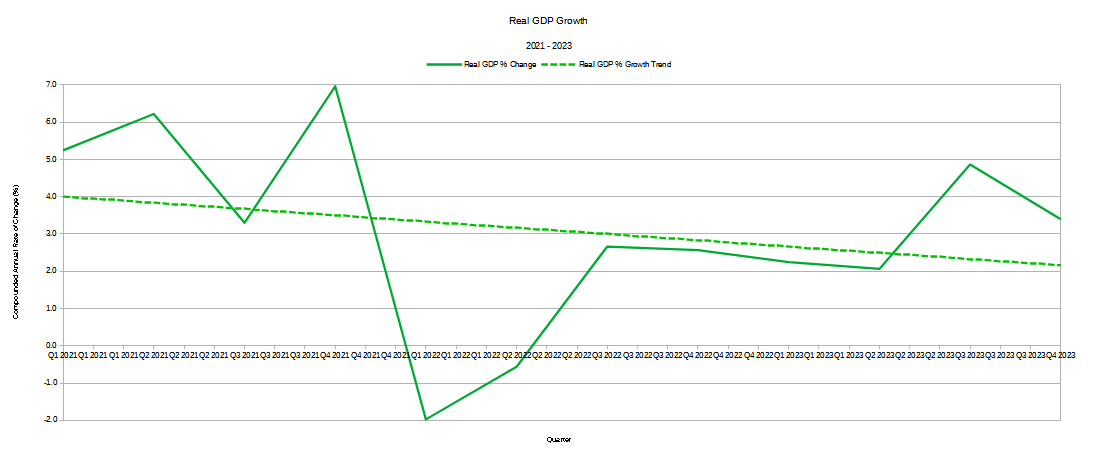

Moreover, that softness is not a fluke. The overall trend in Real GDP growth since the start of Dementia Joe’s Reign of Error has been one of decline: there is less economic growth today than there was in 2021.

As a comparison, when we look at the overall trend in Real GDP growth in the first three years of Donald Trump’s first term as President, we see a growth trend. There was more economic growth in 2019 than there was in 2017.

I am not suggesting that the BEA might be tempted (or perhaps pressured) to shade the GDP data so as to downplay this trend within Dementia Joe’s regime of softening GDP growth even by their own metrics, but if the second revision was plausibly a step towards a more realistic estimate of actual economic growth, the reversal in the third has to be two steps away from that more realistic estimate by definition.

Even with the shaded GDP numbers for the fourth quarter of 2023, the reality of real GDP growth in this country is that it has been demonstrably lagging over the past two years at least. The mini-recession of Q4 2021 through Q1 2022 resulted almost a flat GDP growth line until Q3 of 2023, even as nominal GDP keeps going up.

No such extended flat line appears when we chart Real GDP growth from 2017 through 2019.

Even with the upwardly revised GDP data, the trend of GDP growth under Dementia Joe has been decidedly less than that same trend under Donald Trump. Going strictly “by the numbers”, there is no refuting that the US economy performed better when Donald Trump was in office.

Not all of this should be laid at Joe Biden’s feet, however. When we look at the amount of federal debt outstanding, there is no denying that, under Biden and the Democrats, federal debt as a percentage of GDP has been declining.

This despite the recent growth in federal debt as a percentage of GDP happened throughout 2023.

Donald Trump’s administration, on the other hand, oversaw growth in the federal debt as a percentage of GDP.

Yet it would be inaccurate to let the simple comparison between the trends for the two administrations stand. To an extent, it is relatively easy for the Biden regime to achieve a declining federal debt as a percentage of GDP. Given the explosion of federal debt in 2020, it would be almost impossible for Biden’s regime to achieve anything other than a declining debt trend.

It is no small irony that Dementia Joe’s success in reducing federal debt as a percentage of GDP is due in large measure to Donald Trump’s decisions to explode federal debt as a percentage of GDP.

Nor should we overlook the reality that while the BEA may be reporting GDP growth overall, the BEA is also reporting diminished real disposable income among workers, and a widening gulf between personal income and real disposable income.

The economy may be growing, but people are not getting more money in their pockets because of it, and that’s a problem.

The economic data put out by the BEA did not show this under Donald Trump.

There is no doubt but that Donald Trump was better for people’s wallets than Joe Biden.

This also plays out when we look at the consumption data put forth by the BEA. While there was some growth in the consumption of services in Q4, consumption of both goods and services has been much weaker in 2022 and 2023 than it was at the start of 2021.

Unsurprisingly, consumption for most of Biden’s Reign of Error has been considerably less than it was under Donald Trump.

It is not a good sign for overall economic development when people are generally buying and consuming less than they were before, or when the rate of growth is slowing or even turning negative. Yet the rate of consumption growth from 2021 through 2023 is demonstrably less for both goods and services than it was from 2017 through 2019.

Yet we should not reduce this to a simple “Biden Bad, Trump Good” narrative. Yes, the data shows the economy performing better under Donald Trump from 2017 through 2019 than under Joe Biden from 2021 through 2023, but we should also remember that 2020 happened on Donald Trump’s watch. The Pandemic Panic Recession was the product of his administration’s policies, and not Joe Biden’s.

Rather, we must understand that the best use of economic data especially is to look at it over time. What the news releases from not just the BEA but the BLS do extremely poorly is discuss what the trends are within the data. There is no assessment on where the data says we have been and where the data suggests we might be going.

It is one thing to note that real disposable income rose slightly in Q4 of 2023, but it is another thing entirely to recognize that whatever minimal rise there was does not alter the disparity and the vastly different growth trajectories for aggregate personal income and real disposable income. Income growth is better than income loss, but income growth that does not begin to overcome prior income loss leaves the individual still very much in a worse off economic position—and that is an important dimension that needs to be acknowledged.

It is one thing for the BEA to speak of the third revision noting an increase in consumption, but it is another thing entirely to recognize that even with that marginal increase consumption growth in Q4 2023, consumption growth in Q4 2019 was still significantly higher.

Can we really say the economy is robust and healthy when in so many ways it is noticeably less than before?

Are we truly on a pathway to prosperity when we are seeing less economic growth growth and slower economic growth than we were before?

The reality of the BEA data is that, even with the upwards revisions, it still shows an economy that is soft and not robust, and one that is getting softer and not healthier. Wall Street may think all is well, but is highly unlikely Main Street is going to share that sentiment, when you consider all of the data.

Really excellent work, Peter. And you’re right, there are a couple of data points that one would think the Biden administration would be spinning and bragging about today, so close to the Election. (Although, as you so admirably show, the spin would not stand up to scrutiny.) One thought that comes to mind is that most Americans right now are doing their taxes. For many families, tax-preparation time is the only time each year when they closely look at their expenses, investments, yearly spreadsheets, etc. I would bet that this assessment right now would get many people fuming that they are NOT better off than they were a year ago, and they will be looking for something to blame - hey, Bidenomics! So maybe Biden’s handlers are strategically waiting until a few weeks after April 15 to bring attention to economics. What do you think, Peter - could this be a factor in how they are dealing with this data, or too small to be of importance?