If we take the Bureau of Economic Analysis at face value (no, I do not recommend this!), the US economy grew at an annualized rate of 2.1% during the second quarter of the year.

Real gross domestic product (GDP) increased at an annual rate of 2.1 percent in the second quarter of 2023 (table 1), according to the "third" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 2.2 percent (revised).

The GDP estimate released today is based on more complete source data than were available for the "second" estimate issued last month. In the second estimate, the increase in GDP was also 2.1 percent. The update primarily reflected a downward revision to consumer spending that was partly offset by upward revisions to nonresidential fixed investment, exports, and inventory investment. Imports, which are a subtraction in the calculation of GDP, were revised down (refer to “Updates to GDP”).

The increase in real GDP reflected increases in nonresidential fixed investment, consumer spending, and state and local government spending that were partly offset by a decrease in exports. Imports decreased (table 2).

Unfortunately, when we drill down into the details of the BEA numbers, as per usual we see not an economy that is growing, but an economy that is growing softer. We see an economy that is either declining or stagnating.

The economy was one of many things about which the children pretending to be GOP Presidential candidates squabbled during their second debate, without really getting to the meat of what is unfolding within the economy.

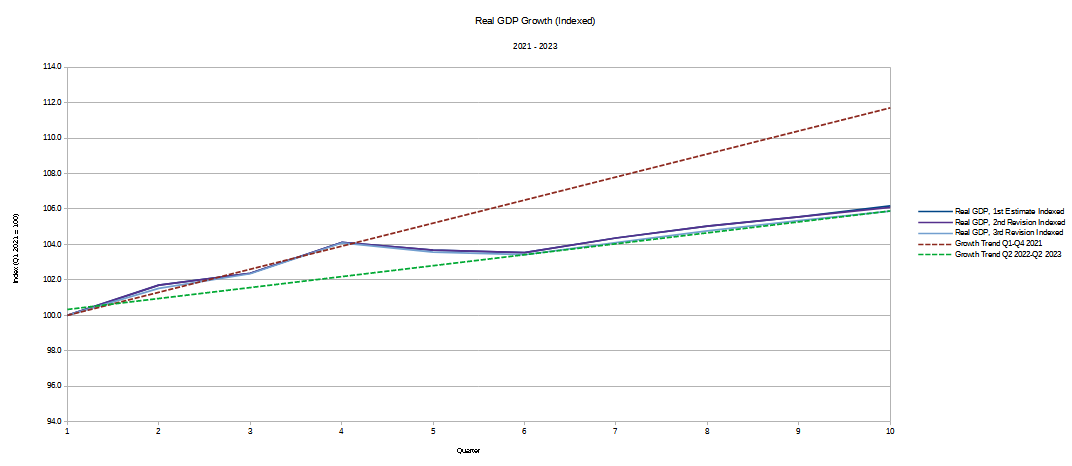

The blunt reality of the US economy is that, quarter by quarter, there is less growth, less momentum, less upside than before. That is plainly obvious through the long term trend in the real GDP numbers as well as in the revisions applied as the BEA completes the data assemblage on GDP.

What is even more disturbing is the softening that is being revealed during the revisions, because the BEA is also injecting a baseline change: the first two revisions to the second quarter real GDP data are reported using 2012 dollars as the baseline, but the third and final revision uses 2017 dollars. Nominally, this raises the reported values for each quarter.

However, the change quarter on quarter to real GDP reflects smaller changes—i.e., less growth—using 2017 dollars rather than 2012 dollars. This suggests that, were the baseline kept to 2012 dollars, there would be even less growth than is being reported in the official revisions.

We can see this also when we baseline each Q2 GDP revision to January of 2021. The weakest assessment of Q2 growth is the last revision to the data—5.9% growth from Q1 of 2021 through Q2 of 2023 in the last revision vs 6.2% growth in the initial estimate.

What has happened to the US economy is that, from the end of the second quarter 2022 onward, it has grown at about half the pace it did during 2021.

While the “experts” are talking about growth for the US economy, the reality of the BEA’s data is that the US economy is slowing, not growing.

We see this deceleration even more clearly when we look at the various components of GDP, particularly consumption and investment.

Virtually every metric is showing either contraction or less growth in recent quarters than in 2021. This is not an optimistic economic trend and it is not one that speaks to a healthy vibrant economy.

We see this softness in the changes to private inventory levels since January 2021.

After a burst of inventory growth in late 2021 through 2022, private inventories have hardly changed at all. When inventories manage to change little across multiple quarters, the consumption side of the economy is almost certainly either stagnating or contracting. Either trend is not good.

The unfolding trend is even worse when we look at consumption of durable goods over time.

Since the first quarter of 2022, over a year ago, there has been almost no growth in consumption spending on durable goods. The only exception has been the first quarter of 2023, but other than that one anomalous quarter, consumption growth in durable goods has not been happening for about a year.

Consumption for nondurable goods has been even softer than consumption for durable goods.

Put simply, all significant growth in consumption of non-durable goods in the US occurred during 2021. Consumption of non-durable goods even declined during most of 2022, and what growth has occurred from the fourth quarter of 2022 onward has been extremely marginal.

While services consumption has been stronger overall, it too has been slowing for over a year.

Not only has services consumption growth slowed sharply from the middle of 2021, but it has slowed noticeably upon further revision even in the current quarter.

American consumers are steadily consuming less and less, in both goods and services. This is not economic growth at all. Whether this economic contraction or economic stagnation is something of a debating point, perhaps, but in terms of impact on the overall economy that is a distinction without much difference. In every scenario the reality is there is less consumption happening today than in 2021.

Nonresidential fixed investment is arguably a brighter picture, although it is not much brighter.

Nonresidential fixed investment has grown over the past two quarters, but there is significantly less growth during Q2 of 2023 than there was in Q2 of 2021. We can hope that investment growth will continue, but as we have seen in previous quarters sustained investment growth has not been exactly a feature of this economy.

Since 2021 two quarters of growth in nonresidential fixed investment has been followed by successive quarters of decline in nonresidential fixed investment. If that pattern holds, the last half of 2023 is not going to be kind to this investment component of GDP.

As for residential fixed investment in the US, it has been more or less a disaster since 2021.

Residential fixed investment has been contracting quarter on quarter since early 2021, without exception. We have had nine successive quarters of less residential fixed investment than before. The closest we get to positive news in the first half of 2023 is that the decline has been slower than in the last half of 2022.

News that is less bad than before is still not good news. That is where we are with residential fixed investment in the US: the news lately is less bad than it was last year, and that is all.

Even corporate media is unable to avoid the obvious signs of growing weakness in the economy.

The Commerce Department’s final revision of second-quarter gross domestic product, the broadest measure of economic output, showed that economic growth was unchanged from the second estimate, holding at an annualized rate of 2.1%.

However, consumer spending, America’s economic engine, was revised much lower, to a 0.8% annualized rate, according to data released Thursday. That’s down from the 1.7% rate reflected in the previous estimate. Spending in the second quarter grew at its weakest pace since the first quarter of 2022, when it was flat.

Such admissions from corporate media make Jay Powell’s recent assessments of the US economy even more bizarre in their optimism.

While corporate media is shying away from the dreaded “R” word (Recession), the latest BEA numbers are yet more confirmation that we are in a “rolling recession”, where contraction happens in different economic sectors at different intervals rather than broadly at the same time.

The BEA numbers are signalling confirmation that the protracted period of stagflation indicated by the latest producer price indices is already unfolding.

Whether we derisively call this ongoing economic deterioration “Bidenomics” or we point the finger squarely at the Federal Reserve’s failed strategies on inflation is at this juncture irrelevant. Neither the White House nor the Federal Reserve have proven themselves to be competent managers of the nation’s economy. Both the White House and the Federal Reserve have contributed mightily to the current weaknesses we are seeing unfold in the nation’s economy.

With neither the White House nor the Federal Reserve even able to comprehend the magnitude of their failures regarding the economy, there is little reason to hope these latest estimates by the BEA will prove a teachable moment for either camp. There is certainly no reason to believe anyone in the Washington DC swamp is prepared to heed the warning signals being flashed out now by the BEA.

Instead, we seem fated to hear continued propaganda about how “resilient” the US economy is. For everyone outside of Washington and Wall Street, this is very bad news, because what is needed are not paeans to “resiliency” but proposals on repairing the damage.

Do not hold your breath expecting to get anything like that any time soon.

Even with a Trump election (I know, very doubtful), we will not get anything like the last bump in the economic side of things because of all the destruction by the Biden Administration.